Which of the following trial balances is used as a source for preparing the income

statement?

A) Unadjusted trial balance

B) Pre-adjusted trial balance

C) Adjusted trial balance

D) Post-closing trial balance

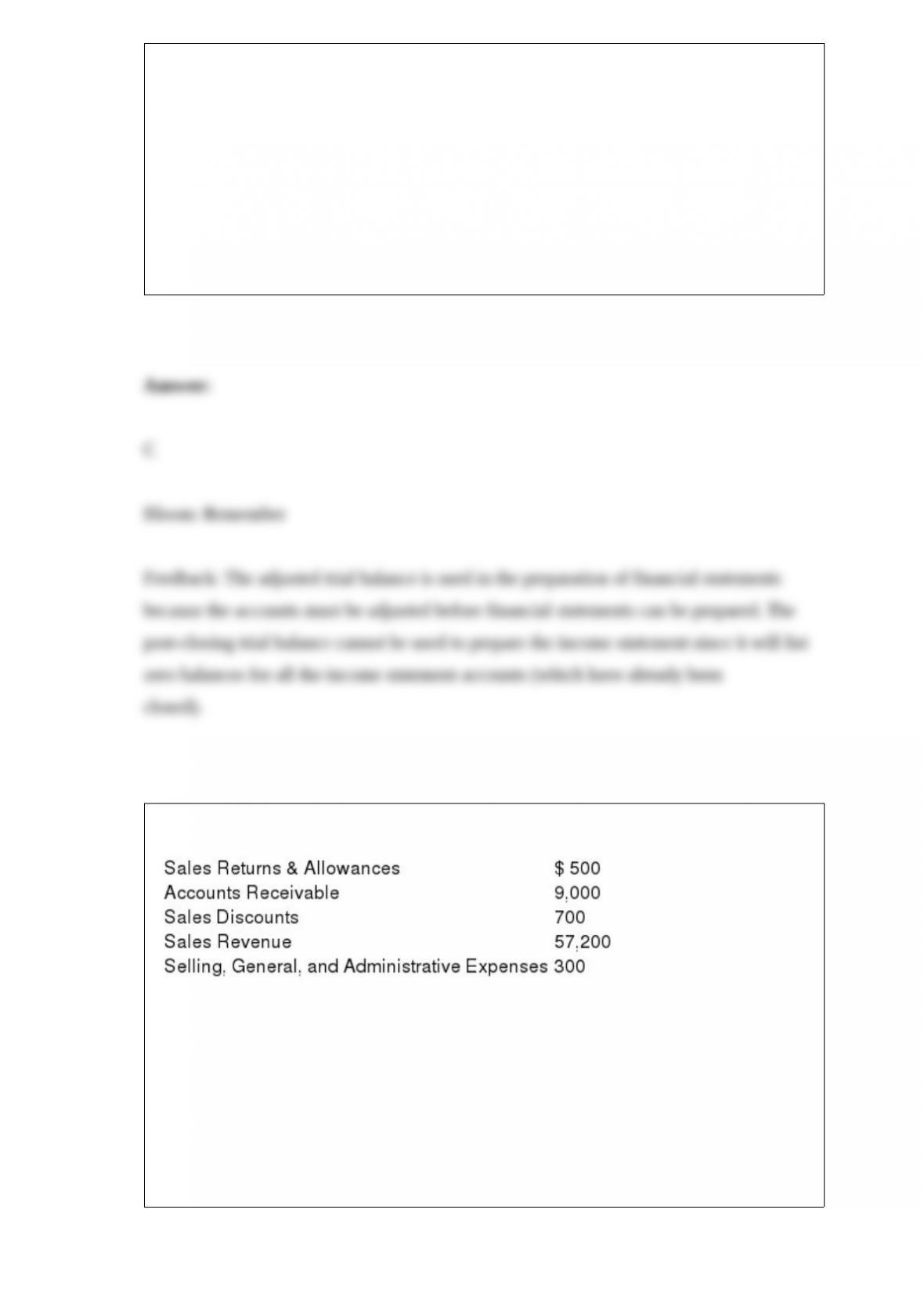

The following account balances appeared on the company’s trial balance at year-end:

The amount of net sales reported on the income statement would be:

A) $57,200.

B) $64,200.

C) $56,000.

D) $55,700.

Carrington Company uses the allowance method for recording bad debts. On February

1, Carrington wrote off a $3,500 customer account balance when it became clear that

the particular customer would never pay. On May 29, Carrington unexpectedly received

a check for $3,500 from the customer. On May 29, Carrington will:

A) Debit Cash and credit Bad Debt Expense for $3,500; debit Accounts Receivable and

credit Allowance for Doubtful Accounts for $3,500.

B) Debit Allowance for Doubtful Accounts and credit Accounts Receivable for $3,500;

debit Cash and credit Bad Debt Expense for $3,500.

C) Debit Accounts Receivable and credit Allowance for Doubtful Accounts for $3,500;

debit Cash and credit Accounts Receivable for $3,500.

D) Debit Allowance for Doubtful Accounts and credit Bad Debt Expense for $3,500;

debit Cash and credit Accounts Receivable for $3,500.

Which of the following accounts could have a non-zero balance on a post-closing trial

balance?

A) Salaries and Wages Expense

B) Premium on Bonds Payable

C) Income Tax Expense

D) Interest Expense

The gross profit equation is:

A) (Sales Revenue + Sales Returns & Allowances) – Cost of Goods Sold

B) (Sales + Sales Discounts) – Cost of Goods Sold

C) (Sales Revenue – Sales Returns & Allowances – Sales Discounts) – Cost of Goods

Sold

D) (Sales Revenue – Sales Returns & Allowances – Sales Discounts) + Cost of Goods

Sold

A company issues 100,000 shares of preferred stock for $40 a share. The stock has

fixed annual dividend rate of 5% and a par value of $3 per share. If sufficient dividends

are declared, preferred stockholders can anticipate receiving dividends of:

A) $5,000 each year.

B) $15,000 each year.

C) 5% of net income each year.

D) $3 per share.

Which of the following would not be classified as a current asset?

A) Cash

B) Accounts Payable

C) Supplies

D) Inventory

CSI Inc. uses accrual basis accounting. During April, the company recorded sales

revenue of $50,000 from sales of goods to customers who promised to pay in May.

During May, the company received payment from these customers of $45,000. No other

transactions with customers took place during these two months. Which of the

following statements about income statement accounts is correct?

A) The Sales Revenue account will have a $45,000 balance at April 30.

B) The Accounts Receivable account has a balance of $5,000 at May 31.

C) The Accounts Payable account has a balance of $5,000 at May 31.

D) The Sales Revenue account will have a $45,000 balance at May 31.

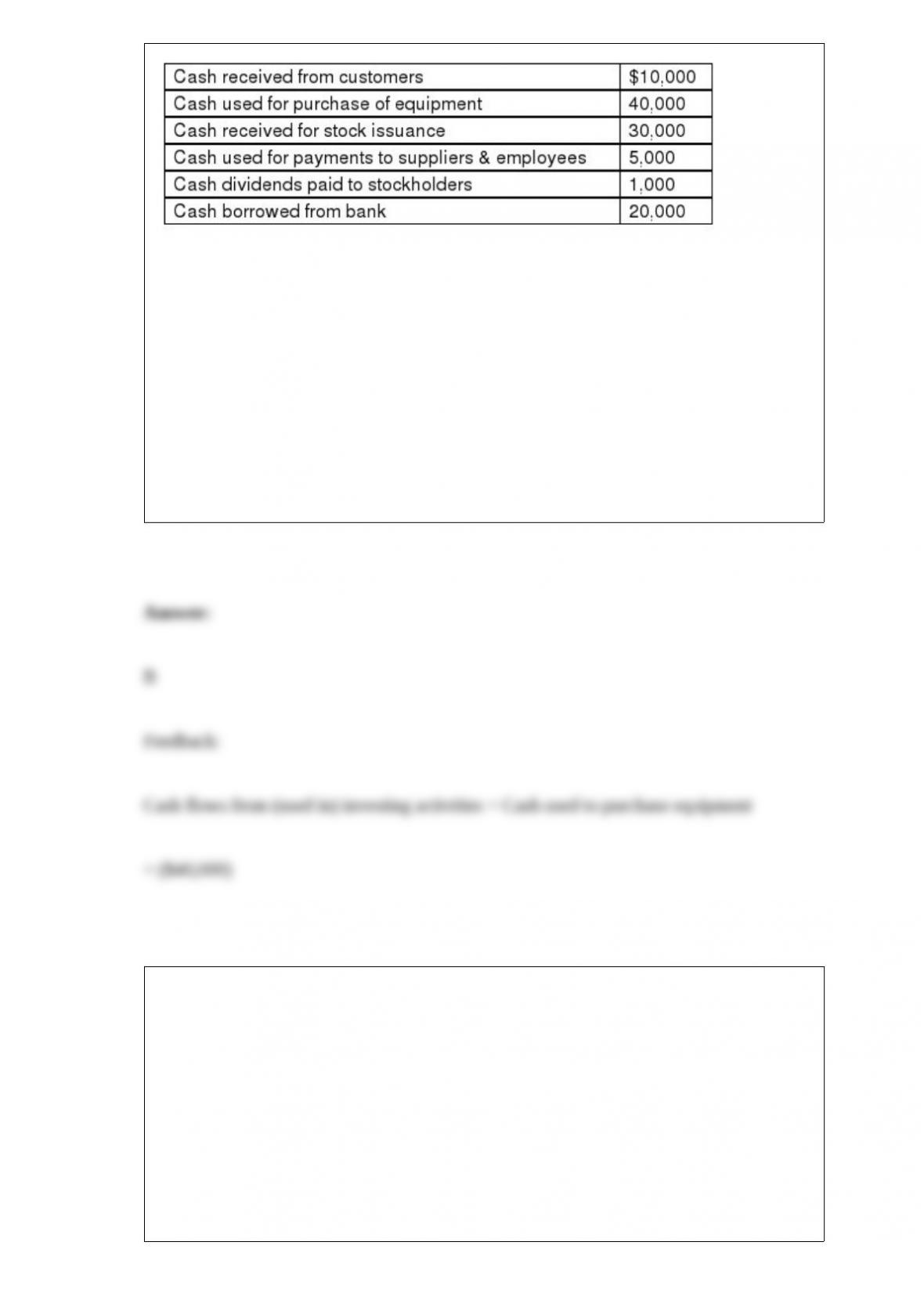

The Statement of Cash Flows for the current year contained the following:

The change in cash for the current year was an increase of $14,000.

Use the information above to answer the following question. What was the amount of

cash flows from (used in) investing activities?

A) ($1,000)

B) ($40,000)

C) ($10,000)

D) $10,000

Wasco Company has experienced bad debt losses of 5% of credit sales in prior periods.

At the end of the year, the balance of Accounts Receivable is $100,000 and the

Allowance for Doubtful Accounts has an unadjusted credit balance of $500. Net credit

sales during the year were $150,000. Using the percentage of credit sales method, what

is the estimated Bad Debt Expense for the year?

A) $5,000

B) $7,000

C) $7,500

D) $8,000

Which of the following would not be reported as a liability on the balance sheet?

A) Accounts Payable

B) Common Stock

C) Notes Payable

D) Salaries and Wages Payable

Which of the following statements about liquidity and solvency ratios is correct?

A) Unlike solvency ratios, liquidity ratios relate to the company’s long-run survival.

B) Both liquidity ratios and solvency ratios measure a company’s ability to meet its

financial obligations.

C) Liquidity ratios include the return on equity ratio and the times interest earned ratio.

D) Solvency ratios include the current ratio and the net profit margin ratio.