1) Pahm Corporation owns 80% of the outstanding voting common stock of Abussi

Corporation, which was purchased for $60,000 over Abussi’s book value. The excess

purchase price was attributable to goodwill. Abussi Corporation owns 60% of the

outstanding common stock of Badock Corporation, which was purchased at book value.

The separate net incomes of Pahm, Abussi, and Badock (excluding investment income)

for the year are $200,000, $240,000, and $260,000, respectively. There were no fair

value/book value differences in the assets and liabilities of Pahm, Abussi and Badock.

The amount of income for the current year assigned to the noncontrolling shareholders

of Abussi Corporation is

A) $48,000

B) $53,200

C) $74,000

D) $79,200

2) Dott Corporation experienced a $100,000 extraordinary loss in the second quarter of

2011 in their East Coast operating segment. The loss should be recognized

A) only at the consolidated report level at the end of the year

B) entirely in the second quarter of 2011 in the East Coast operating segment

C) in equal amounts allocated to the remaining three quarters of 2011 at the corporate

level

D) in equal amounts allocated to the remaining three quarters of 2011 of the East Coast

segment

3) Que, Rae, and Sye are in the process of liquidating their partnership. Sye has agreed

to accept the inventory, which has a fair value of $60,000, as part of her settlement. A

balance sheet and the residual profit and loss sharing percentages are as follows:

Cash$248,000Accounts payable$180,000

Inventory100,000Que, capital (40%)98,000

Plant assets280,000Rae, capital (40%)175,000

Sye, capital (20%)175,000

Total assets$628,000Total liab./equity$628,000

If the partners then distribute the available cash using a safe payments schedule, Sye

will receive

A) $ 41,000 cash

B) $ 51,000 cash

C) $107,000 cash

D) $175,000 cash

4) On June 30, 2011, the Able, Baker, and Charlie partnership had the following fiscal

year-end balance sheet:

Cash$8,000Accounts payable$14,000

Accounts receivable12,000Loan from Charlie10,000

Inventory28,000Able, capital (20%)28,000

Plant assets-net24,000Baker, capital (20%)20,000

Loan to Able12,000Charlie,capital (60%)12,000

Total assets$84,000Total liab./equity$84,000

The percentages shown are the residual profit and loss sharing ratios. The partners

dissolved the partnership on July 1, 2011, and began the liquidation process. During

July the following events occurred:

*Receivables of $6,000 were collected.

*All inventory was sold for $8,000.

*All available cash was distributed on July 31, except for

$4,000 that was set aside for contingent expenses.

How much cash would Able receive from the cash that is available for distribution on

July 31? (Assume a safe payments schedule is used.)

A) $ 0

B) $ 800

C) $2,400

D) $4,000

5) Bird Corporation has several subsidiaries that are included in its consolidated

financial statements and several other investments in corporations that are not

consolidated. In its year-end trial balance, the following intercompany balances appear.

Ostrich Corporation is the unconsolidated company; the rest are consolidated.

Due from Pheasant Corporation$25,000

Due from Turkey Corporation5,000

Cash advance to Skylark Company8,000

Cash advance to Starling15,000

Current receivable from Ostrich10,000

What amount should Bird report as intercompany receivables on its consolidated

balance sheet?

A) $0

B) $10,000

C) $30,000

D) $63,000

6) Plenny Corporation sold equipment to its 90%-owned subsidiary, Sourdough Corp.,

on January 1, 2012 . Plenny sold the equipment for $100,000 when its book value was

$75,000 and it had a 5-year remaining useful life with no expected salvage value.

Straight-line depreciation is used by both companies. Separate balance sheets for

Plenny and Sourdough included the following equipment and accumulated depreciation

amounts on December 31, 2012:

Plenny Sourdough

Equipment$850,000 $300,000

Less: Accumulated depreciation(200,000)(60,000)

Equipment-net$650,000 $240,000

Consolidated amounts for equipment and accumulated depreciation at December 31,

2012 were respectively

A) $1,125,000 and $255,000

B) $1,125,000 and $260,000

C) $1,150,000 and $255,000

D) $1,150,000 and $260,000

7) Which of the following statements about variable interest entities (VIE) is false?

A) Under GAAP, a VIE may be a corporation, partnership, limited liability company or

trust

B) Under GAAP, pension plans are excluded from VIE accounting

C) A potential VIE must be a separate entity, not a subset, branch or division of another

entity

D) VIEs do not require the identification of a primary beneficiary

8) The financial statements of proprietary funds are similar to business enterprises with

the exception that proprietary funds do not

A) report fixed assets

B) report property taxes

C) separate current and noncurrent assets

D) report noncurrent liabilities

9) The spread between interest rates on low quality corporate bonds and US

government bonds

A) widened significantly during the Great Depression

B) narrowed significantly during the Great Depression

C) narrowed moderately during the Great Depression

D) did not change during the Great Depression

10) Pickle Incorporated acquired a $10,000 bond originally issued by its 80%-owned

subsidiary on January 2, 2011 . The bond was issued in a prior year for $11,250,

matures January 1, 2016, and pays 9% interest at December 31 . The bond’s book value

at January 2, 2011 is $10,625, and Pickle paid $9,500 to purchase it. Straight-line

amortization is used by both companies. How much interest income should be

eliminated in 2011?

A) $720

B) $800

C) $900

D) $1,000

11) Historically, much of the controversy concerning accounting requirements for

business combinations involved the ________ method.

A) purchase

B) pooling of interests

C) equity

D) acquisition

12) Maxtil Corporation estimates its income by calendar quarter as follows for 2011:

1st2nd3rd4th2011

QuarterQuarterQuarterQuarterTotal

Est. Income$40,000$30,000$20,000$20,000$110,000

Income tax rates applicable to Maxtil:

From: $0 to $50,00015%

From: $50,001 to $75,00025%

Over: $75,00035%

Required:

Determine Maxtil’s estimated effective tax rate.

13) Warren Peace passed away, with his will leaving the bulk of all his worldly

possessions to his friend Leo. The following transactions occurred with respect to

Warren’s estate.

1>Warren’s estate inventory included 10,000 shares of Newberry Industries, selling at

the time of Warren’s death at $56 per share. There were no outstanding dividends at the

time Warren died, but two weeks later, a $1.00 per share dividend was declared.

2>Warren only designated one item that was not to be left to Leo. Warren’s family had a

signed, first-edition copy of a classic novel that was valued and included in the estate

inventory at $67,000, which Warren left to the local library. The book is located and

delivered.

3>Funeral expenses are paid in the amount of $7,880.

4>A statement comes from the insurance company indicating there are multiple charges

from Warren’s final hospital stay that will not be covered and are the responsibility of

the estate. These fees amount to $39,000 and were not known at the time the estate

inventory was prepared. The charges are confirmed and will be paid when the separate

bills arrive from the hospital and professionals who billed them to the insurance

company.

5>A check is received from Newberry Industries for the dividends declared in the first

transaction, above.

Required:

Prepare the journal entries for the listed transactions. Disregard the impact of estate and

income taxes.

14) Carson County had the following transactions for their General Fund relating to the

levy and collection of property taxes.

1>Property tax bills for $1,000,000 are sent to property tax owners. Taxes are due in 45

days. History shows that Carson County should expect 1.5% of the property taxes to be

uncollectible.

2>$850,000 in property taxes is collected. The remaining receivables are past due.

3>An additional $80,000 of the delinquent taxes is collected.

4>Wrote off $10,000 of delinquent taxes determined to be uncollectible.

Required:

Prepare the journal entries in the General Fund for the transactions.

15) Identify the fund type of the fund being described.

1>A fund used to account for the external portion of investment pools reported by the

sponsoring government.

2>A fund used to account for resources that are legally restricted to use of the earnings

only for government programs or activities.

3>A fund used to account for resources used to pay for a new stadium.

4>A fund used to account for local taxes withheld on behalf of another county.

5>A fund used to account for resources used to pay interest on a long-term bond issue.

6>A fund used to account for specific revenues that are restricted in use.

7>A fund used to account for the local swimming pool that is owned by the city and

used by residents for a membership fee.

8>A fund used to account for the centralized data processing services of the state

government.

9>A fund used to account for all funds except those required to be accounted for in

another fund.

10>A fund that accounts for government pension plans if the government is the trustee

16) Faled Company has the following assets and liabilities, stated at fair value in

liquidation.

Assets pledged with secured creditors$100,000

Assets pledged with partially secured creditors75,000

Other assets160,000

Secured liabilities50,000

Partially secured liabilities110,000

Unsecured liabilities with priority80,000

Unsecured liabilities215,000

Required:

Determine the amount of cash that will be available to pay unsecured creditors, and the

percentage of unsecured liabilities that will be paid.

17) A summary balance sheet for the Akerly, Baskin, and Crow partnership on

December 31, 2011 is shown below. Partners Akerly, Baskin, and Crow allocate profit

and loss in their respective ratios of 3:2:1 . The partnership agreed to pay partner Baskin

$500,000 for his partnership interest upon his retirement from the partnership on

January 1, 2012 . The partnership financials on January 1, 2012 are:

Assets

Cash$ 70,000

Marketable securities190,000

Inventory360,000

Land110,000

Building-net570,000

Total assets$1,300,000

Equities

Akerly, capital$630,000

Baskin, capital420,000

Crow, capital250,000

Total equities$1,300,000

Required:

Prepare the journal entry to reflect Baskin’s retirement from the partnership:

1>Assuming a bonus to Baskin.

2>Assuming a revaluation of total partnership capital based on excess payment.

3>Assuming goodwill equal to the excess payment is recorded.

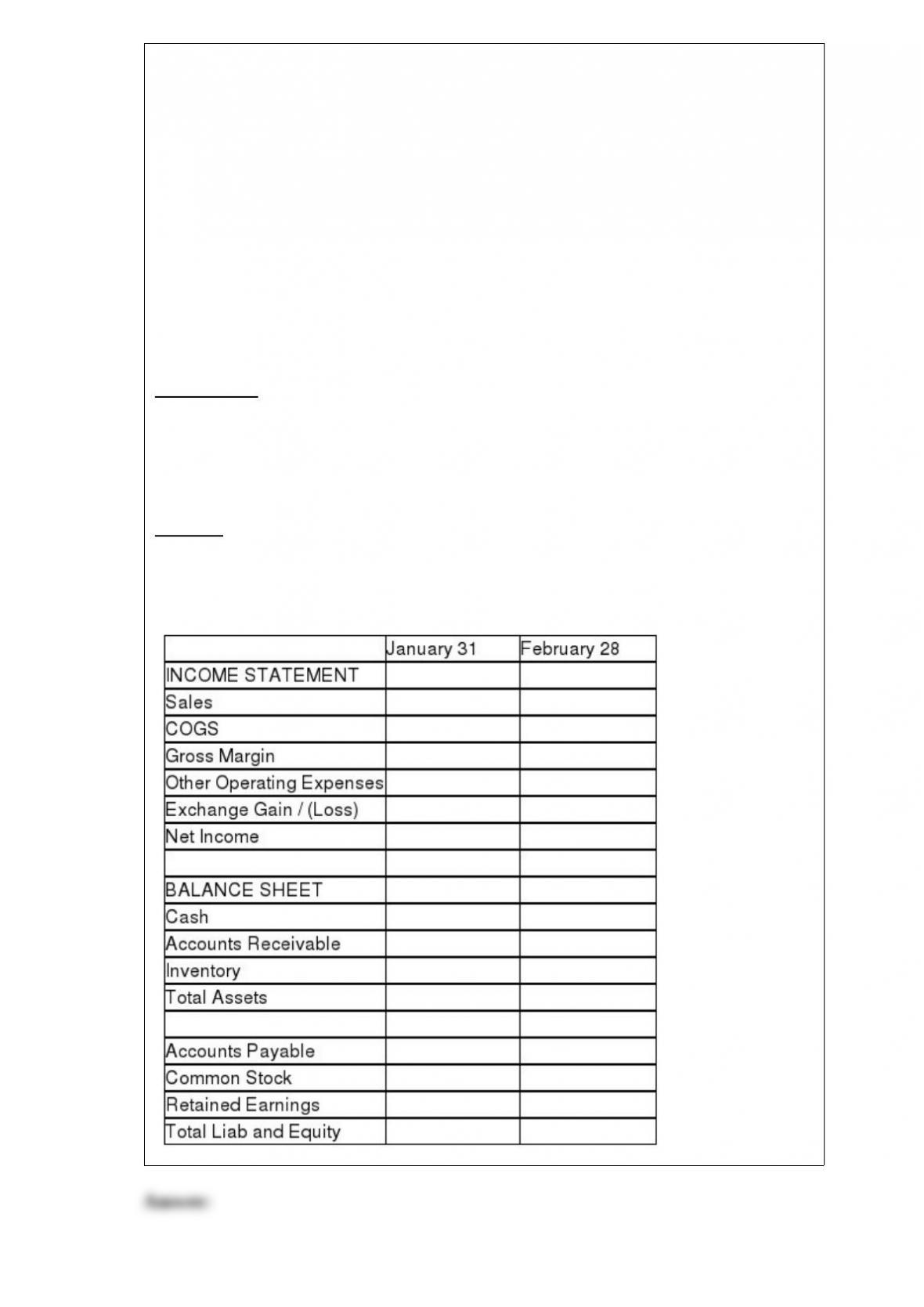

18) Piel Corporation (a U.S. company) began operations on January 1, 2011, when

common stock was issued for $250,000. In the first two months of operations, Piel had

the following transactions:

January 15, 2011Bought inventory for 100,000 Mexican pesos on account

January 26, 2011Sold 70% of inventory acquired on 1/15/11 for 44,000 Saudi riyals on

account

January 27, 2011Paid $1,000 in other operating expenses

February 2, 2011Sold additional inventory that cost $1,000 for $3,000 cash to a U.S.

company.

February 15, 2011Acquired and paid the 100,000 pesos owed to the Mexican supplier

February 21, 2011Paid $1,500 in other operating expenses

February 28, 2011Collected the 44,000 riyals from the Saudi customer and immediately

converted them into U.S. dollars

The following exchange rates apply:

DateRateRate

January 15$.11 = 1 peso$.23 = 1 riyal

January 26$.12 = 1 peso$.24 = 1 riyal

January 31$.13 = 1 peso$.25 = 1 riyal

February 15$.14 = 1 peso$.26 = 1 riyal

February 28$.15 = 1 peso$.27 = 1 riyal

Required:

Complete the summary income statement and balance sheet for the month ended

January 31, 2011 and February 28, 2011, assuming there were no other transactions.