Which of the following cost items is not allocable as joint costs when a single

manufacturing process produces several main products and several by-products?

A. Direct materials

B. Variable overhead

C. Direct labor

D. Fixed overhead

E. Freight-out

Answer:

Which of the following is a nonvalue-added activity?

A. Product design

B. Customer service

C. Research and development

D. Rework of defective items

Answer:

Metalbinders, Inc., has two divisions for its metal fabrication business. Division A

stamps the objects and then transfers them to Division B, which finishes and sells them.

Last year, Division A had administrative expenses of $40,000. Division B incurred

additional production costs of $120,000 (exclusive of amounts paid to Division A for

the stamped steel) to process 120,000 units. Division B sold the finished goods for

$500,000 and incurred $80,000 in variable selling and administrative expenses.

Required:

a) Prepare income statements for each division. Use a transfer price of Division A’s total

cost plus 5%. Assume Cost of Goods Sold for Division B is $351,000.

b) Repeat (a), using a transfer price of $2.00 per unit; this is also the market price.

c) Repeat (a), using a negotiated transfer price of $1.90 per unit.

d) Which transfer price results in higher income to Metalbinders, Inc.?

Answer:

The Work-in-Process Inventory of the Rapid Fabricating Corp. was $3,000 higher on

December 31, 2010 than it was on January 1, 2010. This implies that in 2010

A. cost of goods manufactured was higher than cost of goods sold.

B. cost of goods manufactured was less than total manufacturing costs.

C. manufacturing costs were higher than cost of goods sold.

D. manufacturing costs were less than cost of goods manufactured.

E. cost of goods manufactured was less than cost of goods sold.

Answer:

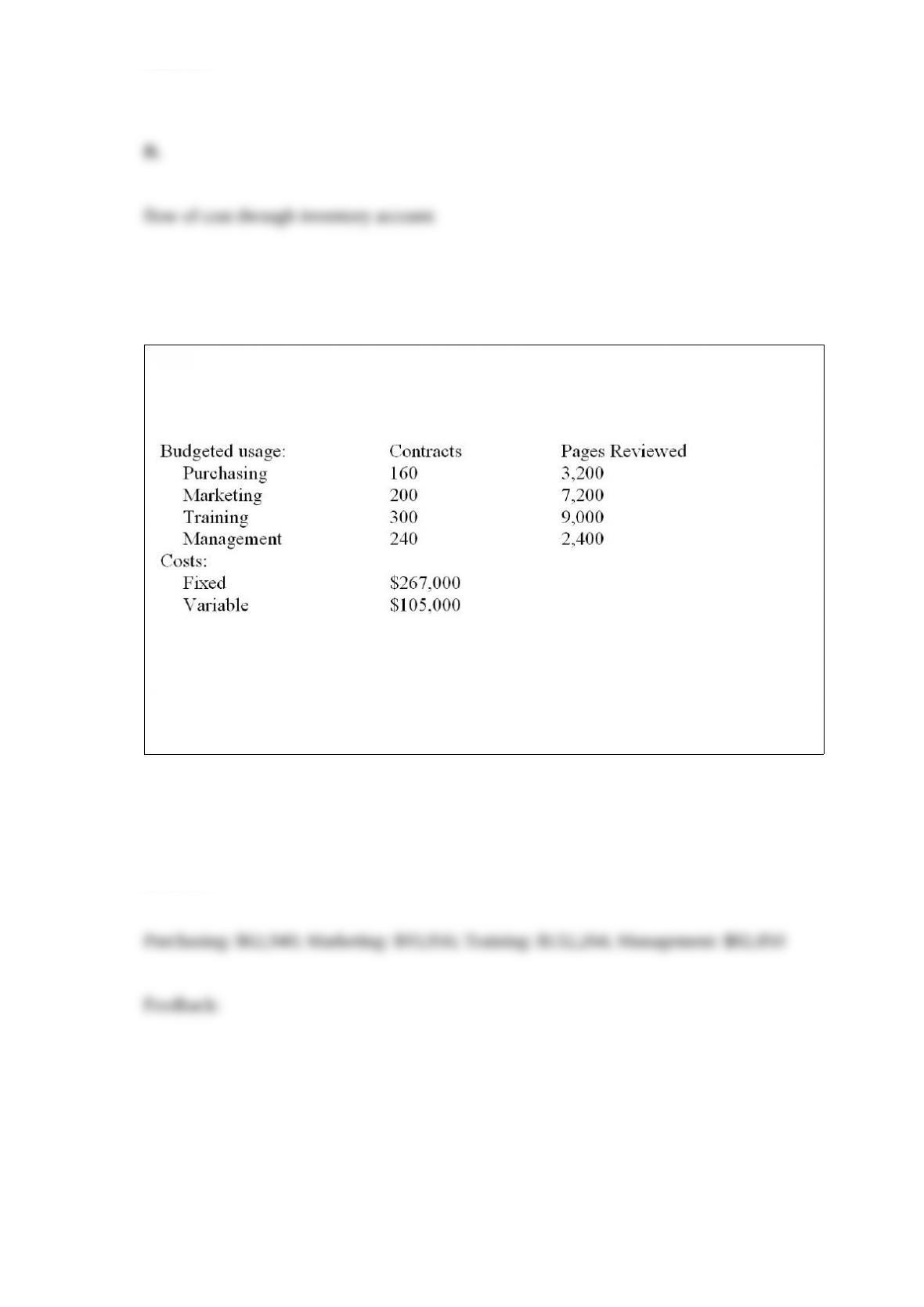

The legal department for Buffet Corp. provides legal services for four departments in

the Omaha office. The following budget has been prepared for the month.

Required (use three decimal places in your calculations):

a) If Buffet uses a dual rate for allocating its costs, allocating fixed costs based on

number of contracts and variable costs based on number of pages reviewed, how much

cost will be allocated to the four user departments?

Answer:

The UVW Manufacturing Company produces a single uniform product throughout the

year. Which of the following product costing systems should be used by UVW?

A. job-order costing

B. process costing

C. operation costing

D. batch costing

Answer:

The Miller Company manufactures wiring tools. The company is currently producing

well below its full capacity. The Brisbois Company has approached Miller with an offer

to buy 5,000 tools at $17.50 each. Miller sells its tools wholesale for $18.50 each; the

average cost per unit is $18.30, of which $2.70 is fixed costs.

Required:

a) If Miller were to accept Brisbois’s offer, what would be the increase in Miller’s

operating profits?

b) Assume that Miller is operating at full capacity. If Miller were to accept Brisbois’s

offer, what would be the change in Miller’s operating profits?

Answer:

KR Sales had $1,200,000 in sales last month. The variable cost ratio was 60% and

operating profits were $80,000. What sales volume does KR’s need to yield a $200,000

operating profit?

A. $1,000,000

B. $1,200,000

C. $1,500,000

D. $2,000,000

Answer:

Assets invested in a responsibility center are included in a performance report of

A. a

B. b

C. c

D. d

Answer:

The Finishing Department had 5,000 incomplete units in its beginning Work-in-Process

Inventory which were 100% complete as to materials and 30% complete as to

conversion costs. 15,000 units were received from the previous department. The ending

Work-in-Process Inventory consisted of 2,000 units which were 50% complete as to

materials and 30% complete as to conversion costs. The Finishing Department uses

first-in, first-out (FIFO) process costing. The How many units were started and

completed during the period?

A. 12,000

B. 13,000

C. 18,000

D. 20,000

Answer:

The starting point in preparing a comprehensive budget for a manufacturing company

limited by its ability to produce and not by its ability to sell is

A. a sales forecast.

B. an estimate of productive capacity.

C. an estimate of cash receipts and disbursements.

D. a projection of fixed asset acquisitions.

Answer:

Property taxes on the manufacturing facility are an element of

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

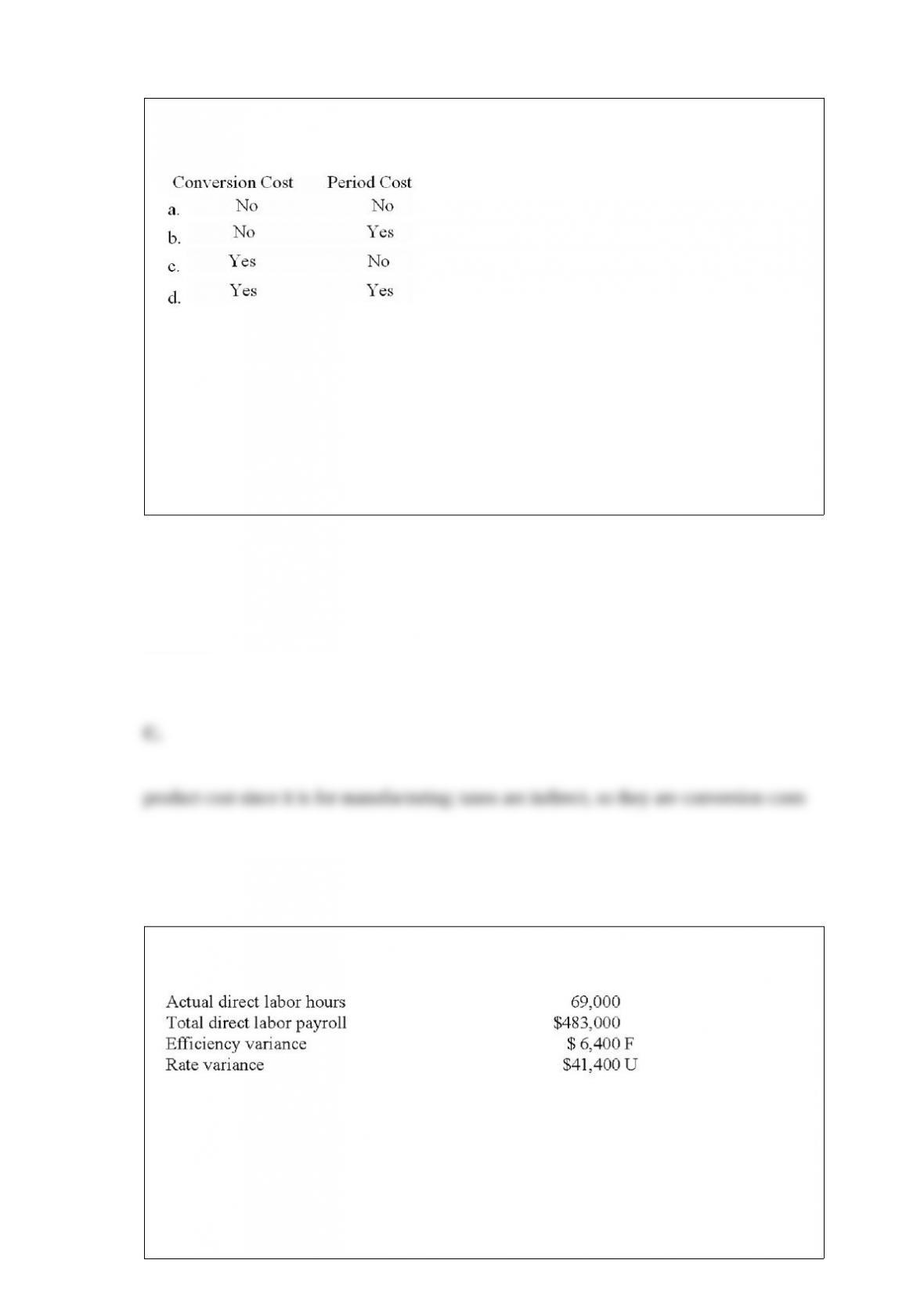

Information for Nighttime Company’s direct labor cost for February is as follows:

What were the standard direct labor hours for February?

A. 70,000

B. 69,000

C. 72,000

D. 71,400

Answer:

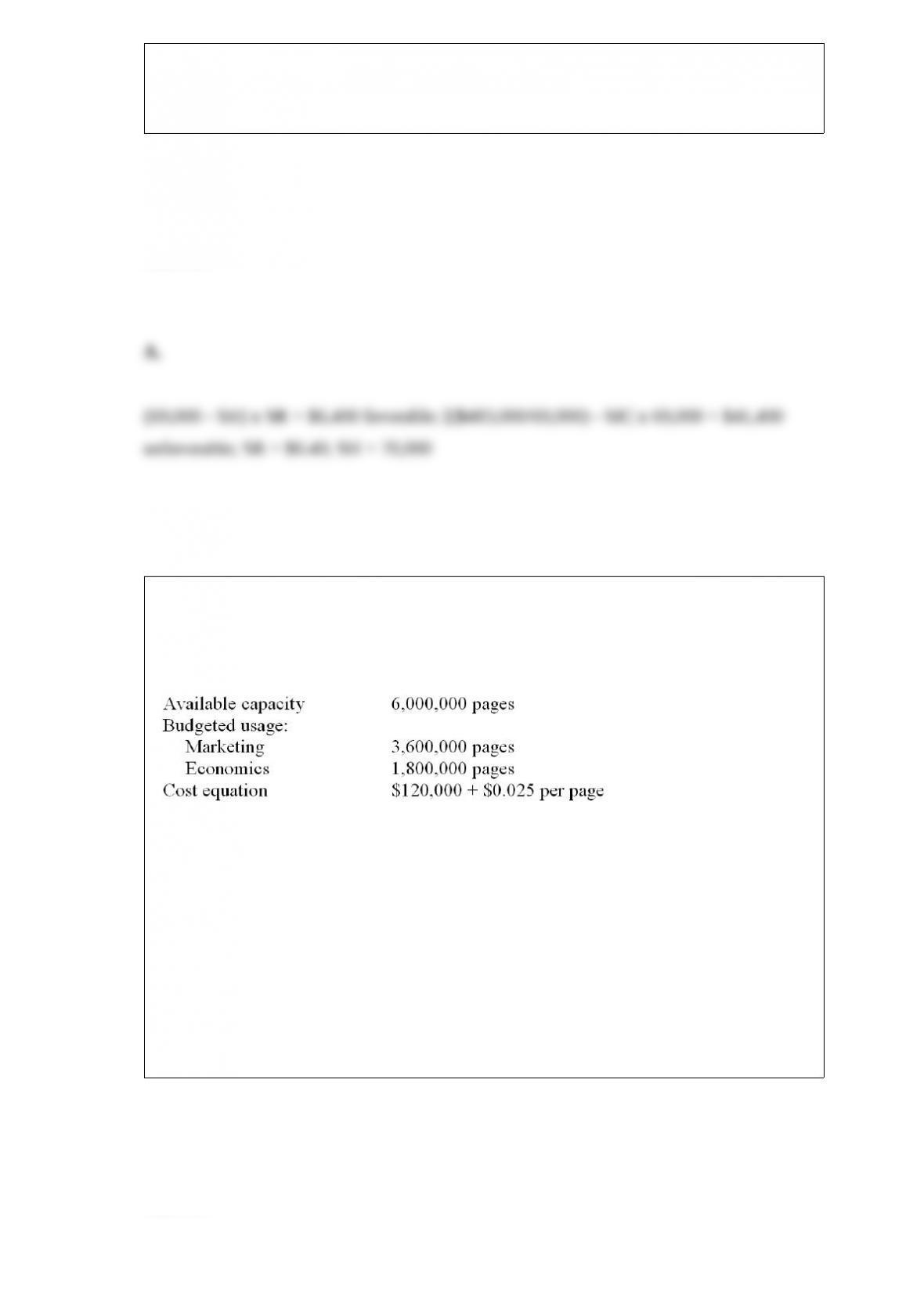

The Copy Department in the College of Business at State University provides

photocopying service for both the Marketing and Economics Department. The

following budget has been prepared for the year.

If the Copy Department uses a dual rate for allocating its costs based on usage, how

much cost will be allocated to the Economics Department?

A. $85,000

B. $90,000

C. $105,000

D. $120,000

Answer:

A manager makes a decision that is beneficial for a specific investment center but not

for the entire organization. From the organization’s perspective, this decision results in

A. goal congruence.

B. decentralization.

C. contingent compensation.

D. fixed compensation.

Answer:

Cascade Cliffs, Inc., operates two divisions: (1) a management division that owns and

manages bulk carriers on the Great Lakes and (2) a repair division that operates a dry

dock in Cheboygan, Michigan. The repair division works on company ships, as well as

other large-hull ships.

The repair division has an estimated variable cost of $37 per labor-hour. The repair

division has a backlog of work for outside ships. They charge $70.00 per hour for labor,

which is standard for this type of work. The management division complained that it

could hire its own repair workers for $45.00 per hour, including leasing an adequate

work area.

What is the minimum transfer price per hour that the repair division should obtain for

its services, assuming it is operating at capacity?

A. $33.00

B. $37.00

C. $45.00

D. $70.00

E. $82.00

Answer:

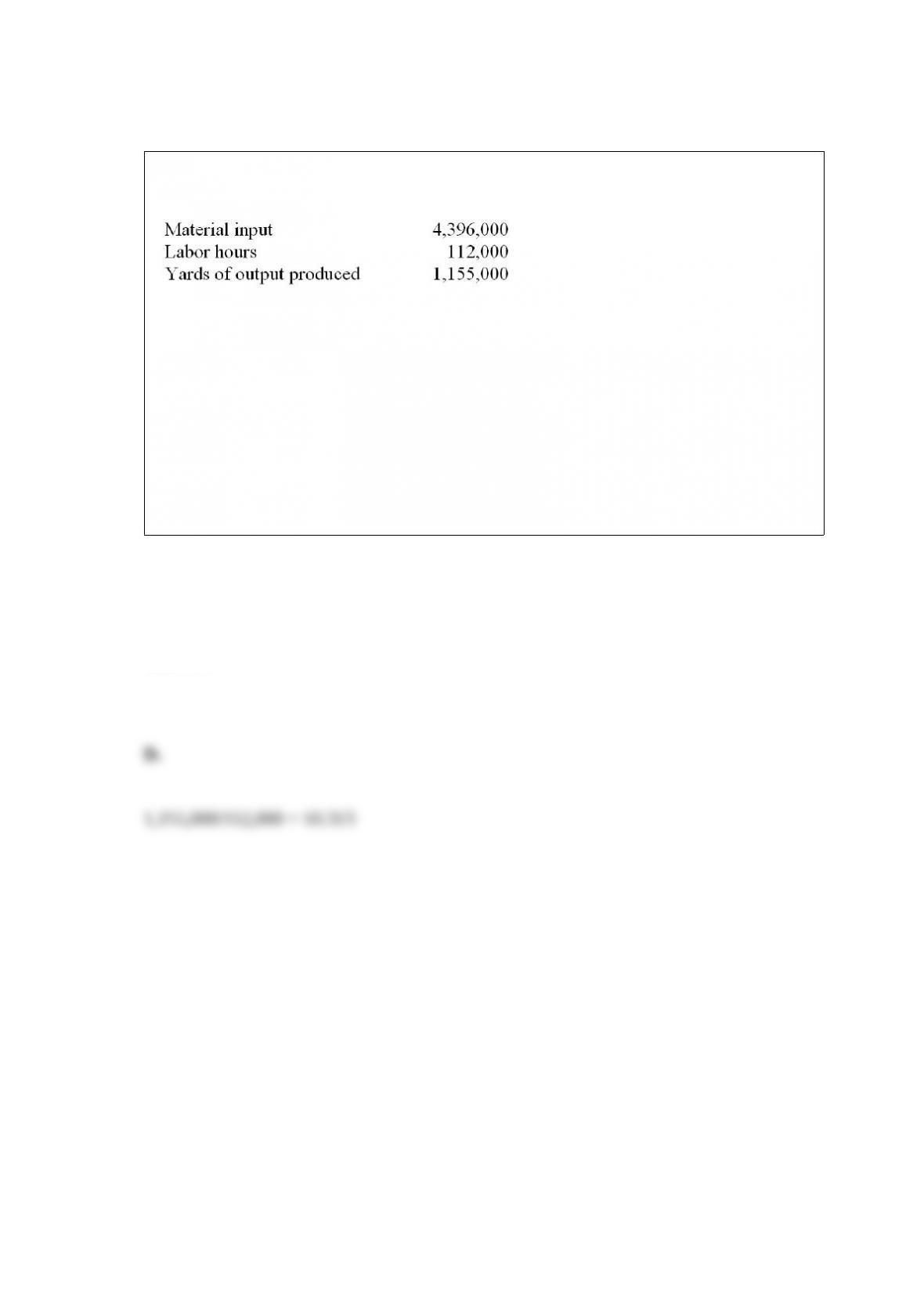

Laguna Co. has provided the following information for last year:

Required:

a) Calculate the total factor productivity measure.

Answer:

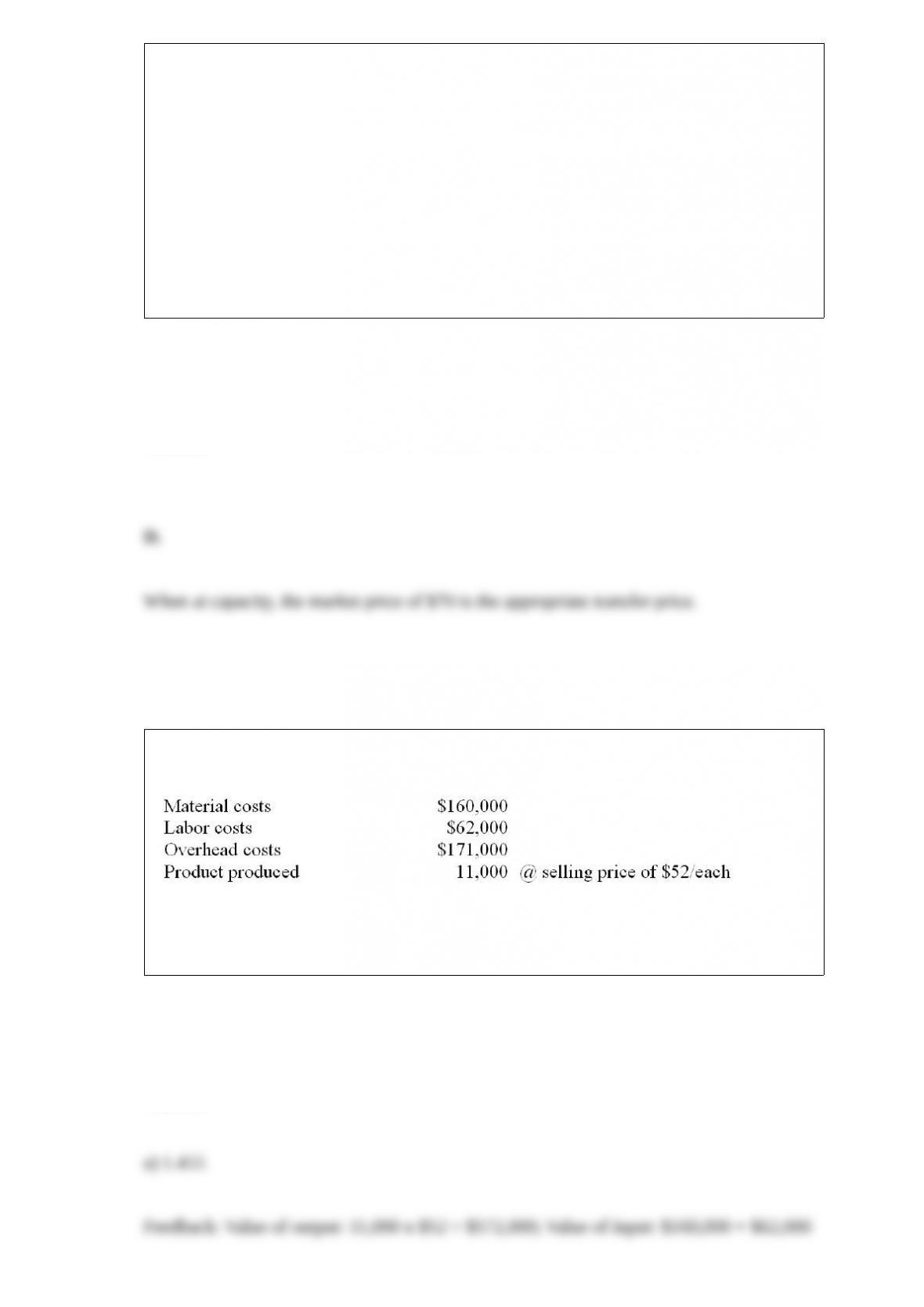

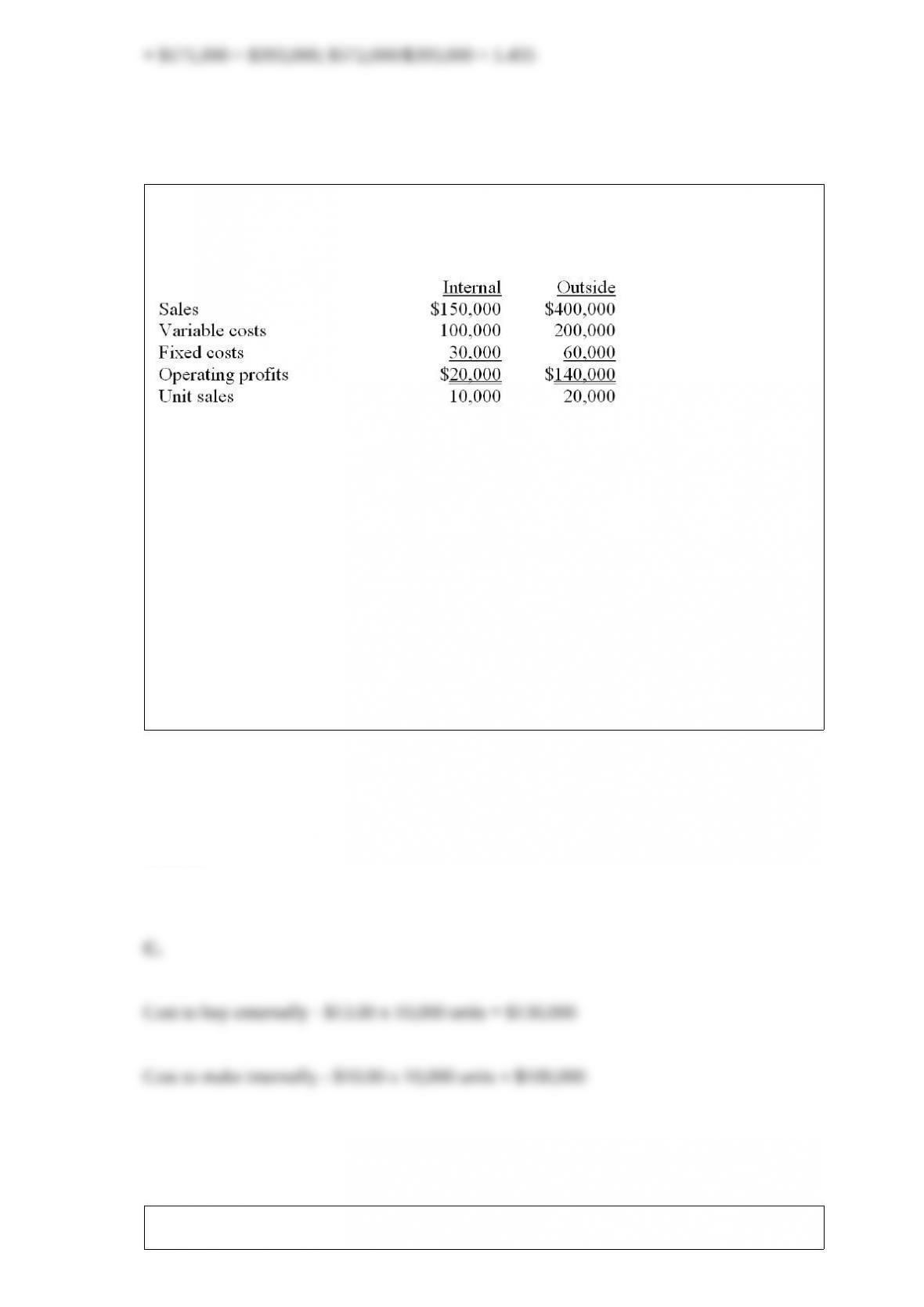

The Axle Division of Becker Company produces axles for off-road sport vehicles.

One-third of Axle’s output is sold to an internal division of Becker; the remainder is

sold to outside customers. Axle’s estimated operating profit for the year is:

The internal division has an opportunity to purchase 10,000 axles of the same quality

from an outside supplier on a continuing basis. The Axle Division cannot sell any

additional products to outside customers. Should the Becker Company allow its internal

division to purchase the axles from the outside supplier at $13.00 per unit?

A. No; making the axles will save Becker $15,000.

B. Yes; buying the axles will save Becker $15,000.

C. No; making the axles will save Becker $30,000.

D. Yes; buying the axles will save Becker $30,000.

Answer:

How will increases in the following items affect return on investment (ROI)?

A. a

B. b

C. c

D. d

Answer:

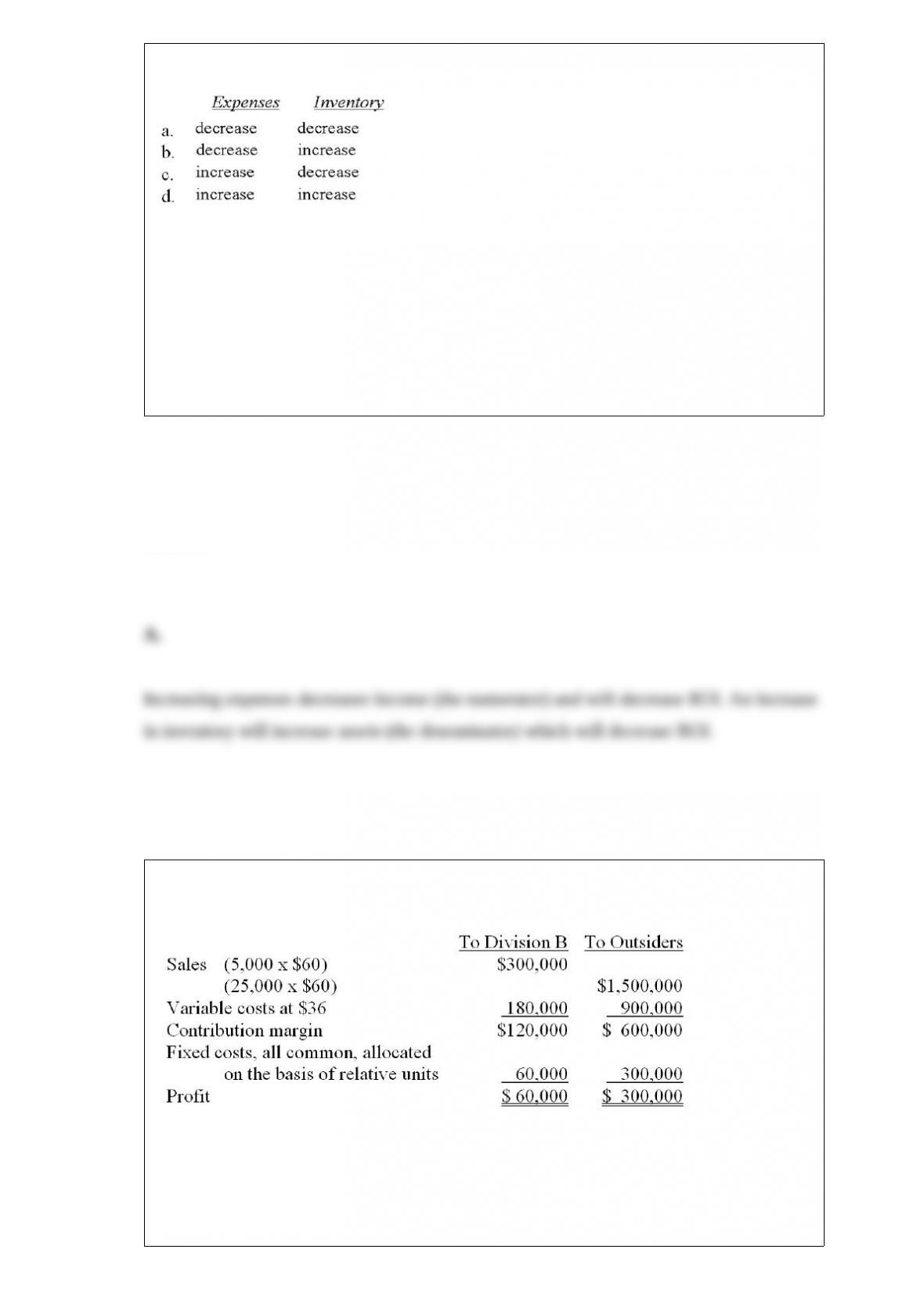

Division A of Stills Company expects the following results:

Division B has the opportunity to buy its needs of 5,000 units from an outside supplier

at $45 each. Assume that Division A cannot increase sales to outsiders.

Required:

a) What would be the optimal transfer price?

b) Assume that Stills allows the divisional managers to negotiate transfer prices. What

would the maximum transfer price be?

c) Assume that Stills allows the divisional managers to negotiate transfer prices. What

would the minimum transfer price be?

Answer:

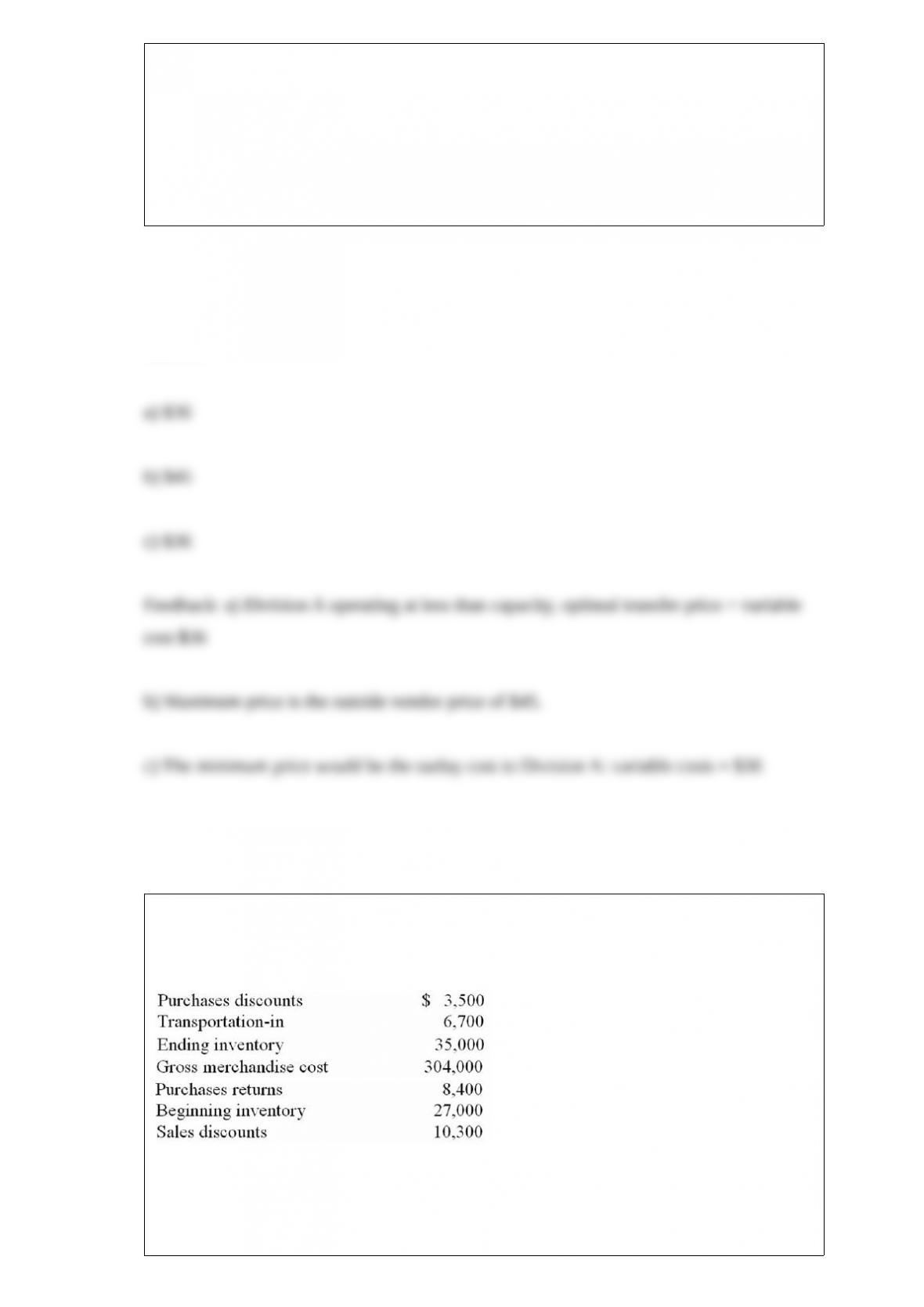

Given the following information for a retail company, what is the total cost of goods

purchased for the period?

A. $298,800

B. $290,800

C. $282,100

D. $304,000

Answer:

The FGH Company has an asset turnover of 3.0 times, using assets of $45,000. The

company also has a return on investment (ROI) of 20%. What was the company’s

operating profit margin?

A. 5.0%

B. 6.0%

C. 6.7%

D. 8.3%

Answer:

Cruises, Inc., operates two divisions: (1) a management division that owns and

manages cruise ships in the Florida Keys and (2) a repair division that operates a dry

dock in Marble Sand Florida. The repair division works on company ships, as well as

other large-hull ships.

The repair division has an estimated variable cost of $28.50 per labor-hour. The repair

division has a backlog of work for outside ships. They charge $48.00 per hour for labor,

which is standard for this type of work. The management division complained that it

could hire its own repair workers for $30.00 per hour, including leasing an adequate

work area.

What is the maximum transfer price per hour that the management division should

pay?

A. $28.50

B. $30.00

C. $39.00

D. $46.50

E. $48.00

Answer:

Redmond Company produces precision components. Redmond has 11 customers, one

accounts for 60 percent of the sales, with the remaining ten accounting for the rest of

the sales. The ten smaller customers purchase components in roughly equal quantities.

Orders placed by the smaller customers are about the same size. Data concerning

Redmond’s customer activity follow:

Order-filling costs for Redmond Company total $360,000, and sales-force costs are

$300,000.

Required:

a) Allocate the order-filling and sales force costs to the customers based on sales

volume?

b) Allocate the order-filling and sales force costs to the customers using an

activity-based costing approach?

Answer:

Which of the following activities would not be considered a value-added activity?

A. Production

B. Marketing

C. Accounting

D. Distribution

Answer:

The basic difference between a master budget and a flexible budget is that a

A. flexible budget considers only variable costs but a master budget considers all costs.

B. flexible budget allows management latitude in meeting goals whereas a master

budget is based upon a fixed standard.

C. master budget is for an entire production facility but a flexible budget is applicable

to single departments only.

D. master budget is based on one specific level of production and a flexible budget can

be prepared for any production level within a relevant range.

Answer:

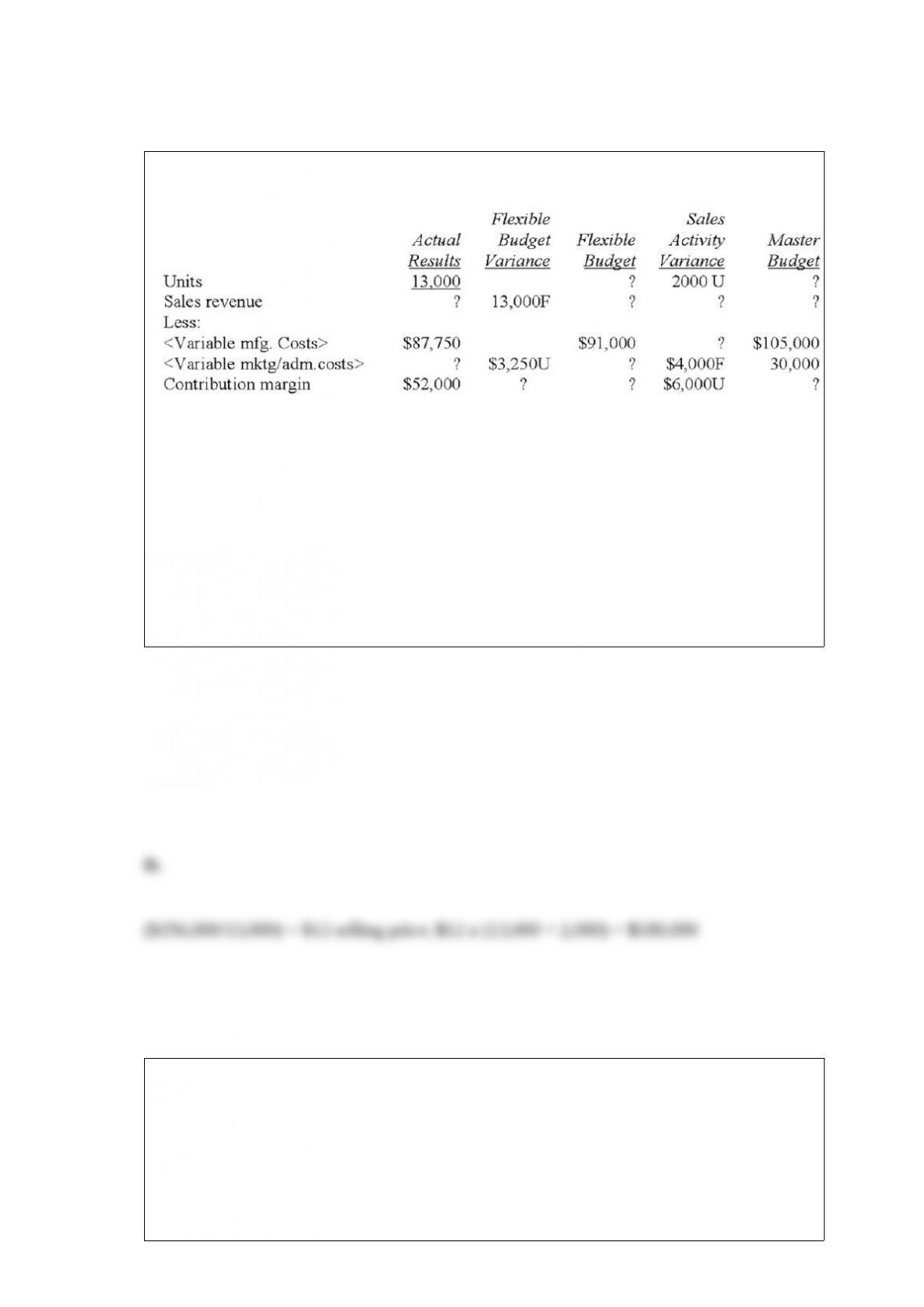

What is the master budget sales revenue?

A. $124,000.

B. $148,000.

C. $156,000.

D. $180,000.

Answer:

In 2010, the MoreForLess Company had revenues of $2,000,000 while costs were

$1,500,000. In 2011, MoreForLess will be introducing a new product line that will

generate $200,000 in sales revenues and $160,000 in costs. Assuming no changes are

expected for the other products, the differential operating profit for 2011 is

A. $540,000.

B. $200,000.

C. $160,000.

D. $40,000.

Answer:

The Sun Company manufactures a special line of graphic tubing items. The company

estimates it will sell 75,000 units of this item in 2008. The beginning finished goods

inventory contains 20,000 units. The target for each year’s ending inventory is 10,000

units.

Each unit requires five feet of plastic tubing. The tubing inventory currently includes

70,000 feet of the required tubing. Materials on hand are targeted to equal three month’s

production. Any shortage in materials will be made up by the immediate purchase of

materials. Sales take place evenly throughout the year.

What are the materials requirements (in feet) for 2008?

A. 313,750

B. 336,250

C. 363,750

D. 386,250

Answer:

Scottso Corporation applies overhead using a normal costing approach based upon

machine-hours. Budgeted factory overhead was $266,400, budgeted machine-hours

were 18,500. Actual factory overhead was $287,920, actual machine-hours were

19,050. How much overhead would be applied to production?

A. $266,400.

B. $274,320.

C. $279,607.

D. $287,920.

Answer:

The Eastern division sells goods internally to the Western division of the same

company. The quoted external price in industry publications from a supplier near

Eastern is $200 per ton plus transportation. It costs $20 per ton to transport the goods to

Western. Eastern’s actual market cost per ton to buy the direct materials to make the

transferred product is $100. Actual per-ton direct labor is $50. Other actual costs of

storage and handling are $40. The company president selects a $220 transfer price. This

is an example of (CIA adapted)

A. market-based transfer pricing.

B. cost-based transfer pricing.

C. negotiated transfer pricing.

D. cost plus 20% transfer pricing.

Answer:

Read, Inc. instituted a new process in October 2008. During October, 10,000 units were

started in Department A. Of the units started, 8,000 were transferred to Department B,

and 2,000 remained in Work-in-Process at October 31, 2008. The Work-in-Process at

October 31, 2008, was 100% complete as to material costs and 50% complete as to

conversion costs. Material costs of $27,000 and conversion costs of $36,000 were

charged to Department A in October. What were the total costs transferred to

Department B assuming Department A uses weighted-average process costing?

A. $46,900

B. $53,600

C. $56,000

D. $57,120

Answer:

The Albertville Co has the following information for last year

The partial productivity for labor is

A. 0.097

B. 0.256

C. 3.906

D. 10.313

Answer: