Under IFRS, the role of the conceptual framework: A.Primarily involves guiding

standard setters to make sure that standards are consistent with each other.

B.Includes serving as a guide for practitioners when a specific standard does not apply.

C.Is less important than in U.S. GAAP.

D.Has resulted primarily from a convergence with U.S. GAAP.

Answer:

Reliable Enterprises sells distressed merchandise on extended credit terms. Collections

on these sales are not reasonably assured, and bad debt losses cannot be reasonably

predicted. It is unlikely that repossessed merchandise is in condition to be re-sold.

Therefore, Reliable uses the cost recovery method. Merchandise costing $30,000 was

sold for $55,000 in 2012. Collections on this sale were $20,000 in 2012, $15,000 in

2013, and $20,000 in 2014.

In its 2013 year-end balance sheet, Reliable would report installment receivables (net)

of:A. $0.

B. $20,000.

C. $4,000.

D. $15,000.

Answer:

Disclosure notes related to a change in accounting principle under the retrospective

approach should include: A. The effect of the change on executive compensation.

B. The auditor’s approval of the change.

C. The SEC’s permission to change.

D. Justification for the change.

Answer:

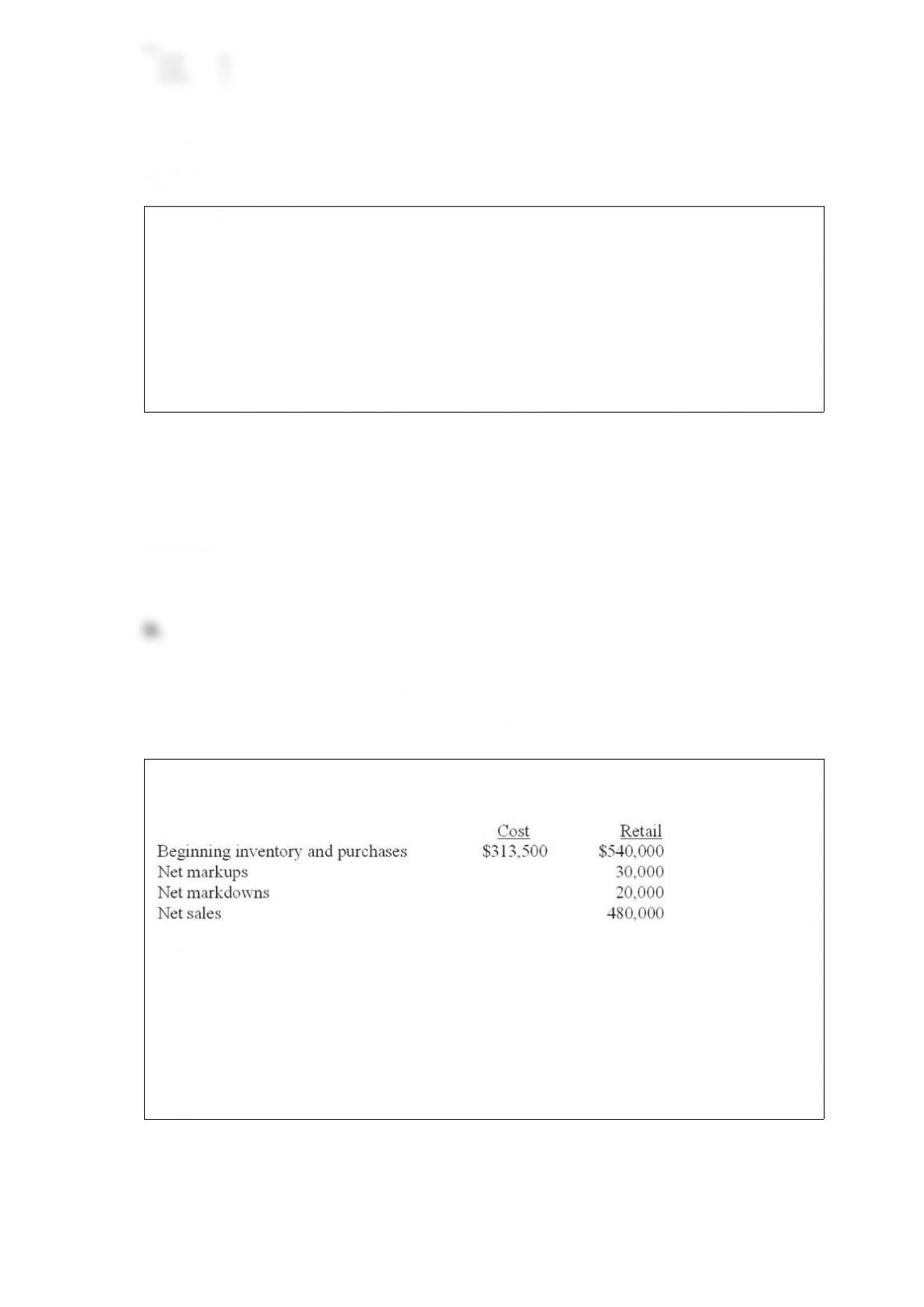

Cloverdale, Inc., uses the conventional retail inventory method to account for inventory.

The following information relates to current year’s operations:

What amount should be reported as cost of goods sold for the year? A. $273,600.

B. $272,861.

C. $275,000.

D. None of the above.

Answer:

On July 1, 2013, Cromartie Furniture established a $150 petty cash fund. A check for

$150 was made out to the petty cash custodian. During July, the petty cash custodian

paid the following bills from the petty cash fund:

At the end of July the petty cash fund was replenished.

The journal entry to replenish the petty cash fund includes: A. A credit to petty cash and

a debit to various expenses for $126.

B. A debit to petty cash and a credit to cash for $150.

C. A credit to cash and a debit to various expenses for $126.

D. None of the above.

Answer:

When computing diluted earnings per share, which of the following will not be

considered in the calculation? A. Dividends paid on common stock.

B. The weighted average common shares.

C. The effect of stock splits.

D. The number of common shares represented by stock purchase warrants.

Answer:

During 2013, M Co. had the following two classes of stock issued and outstanding for

the entire year:

– 400,000 shares of common stock, $1 par.

– 2,000 shares of 4% preferred stock, $100 par, convertible share-for-share into

common stock.

M’s 2013 net income was $1,800,000, and its income tax rate for the year was 30%. In

the computation of diluted earnings per share for 2013, the amount to be used in the

numerator is: A. $1,792,000.

B. $1,796,000.

C. $1,800,000.

D. $1,802,400.

Answer:

On January 1, 2013, Blue Inc. issued stock options for 200,000 shares to a division

manager. The options have an estimated fair value of $6 each. To provide additional

incentive for managerial achievement, the options are not exercisable unless divisional

revenue increases by 6% in three years. Blue initially estimates that it is not probable

the goal will be achieved, but in 2014, after one year, Blue estimates that it is probable

that divisional revenue will increase by 6% by the end of 2015. Ignoring taxes, what is

the effect on earnings in 2014? A. $200,000.

B. $400,000.

C. $600,000.

D. $800,000.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Intangible assets

2)Goodwill

3)Depreciation

4)Patents

5)Depletion

A. Consideration given less fair value of net identifiable assets.

B. The cost allocation of equipment

C. The allocation of cost of natural resources

D. Protects against infringements on manufactured products.

E. Long-term assets that generally represent various types of rights

Answer:

Which of the following creates a deferred tax asset? A. An unrealized loss from

recording investments at fair value.

B. Prepaid insurance.

C. An unrealized gain from recording investments at fair value.

D. Accelerated depreciation in the tax return.

Answer:

Nickel Inc. bought $100,000 of 3-year, 6% bonds as an investment on December 31,

2012 for $106,000. Nickel uses straight-line amortization. On May 1, 2013, $10,000 of

the bonds were redeemed at 110. How much, and what type of gain or loss, most likely

results from this redemption? A. $467 ordinary gain.

B. $467 extraordinary gain.

C. $467 extraordinary loss.

D. $467 ordinary loss.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1) Investor’s share of

investee income

2) Consolidation

3) Equity method

4) Additional depreciation

5) Dividends

A. Recognized as revenue for equity-method investments, but not for available-for-sale

investments

B. Can be required in the future when, at the time an equity-method investment is

made, the fair value of investee’s identifiable net assets exceeds their carrying value

C. Used when investor can significantly influence investee

D. Used when investor has effective control of investee

E. Recognized as revenue for available-for-sale investments, but not equity-method

investments.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term by placing the letter

designating the best term in the space provided by the phrase. 1) Equity

2) Distributions to owners

3) Expenses

4) Investments by owners

5) Liabilities

A. Outflows of resources to generate revenues.

B. Net assets.

C. Cash dividends.

D. Transfers of resources in exchange for common and preferred stock.

E. Claims of creditors against the assets of a business.

Answer:

Listed below are 5 terms followed by a list of phrases that describe or characterize each

of the terms. Match each phrase with the most correct term. 1)Interperiod tax allocation

2)Deferred tax liability

3)Operating loss carryforward

4)Prior period adjustment

5)Permanent difference

A. Is the process of allocating income taxes among two or more reporting periods by

B. Would be either debited or credited to retained earnings net of any tax effect

C. Arises when future taxable amounts are created by temporary differences

D. Will always create a deferred tax asset

E. Is usually a revenue or expense item that is excluded or not deductible in

determining

Answer:

R Co. has outstanding 100 million shares, $1 par common stock, selling for $8 per

share. After a 1 for 4 reverse stock split:A. R would have 25 million shares, $4 par per

share.

B. The market price per share would be about $2.

C. Fractional shares would be issued.

D. Retained earnings would be reduced.

Answer:

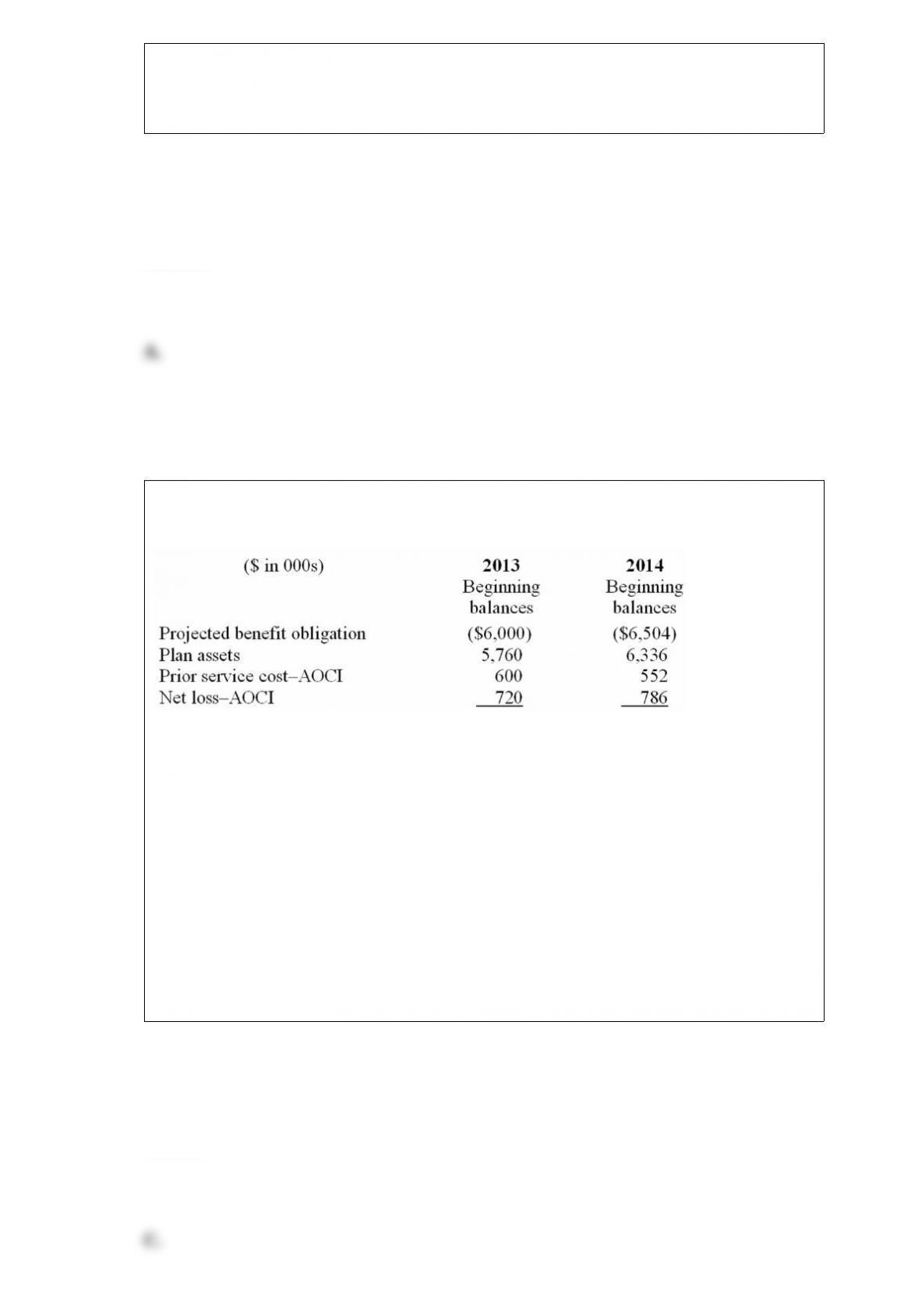

The following information pertains to Havana Corporation’s defined benefit pension

plan:

At the end of 2013, Havana contributed $696 thousand to the pension fund and benefit

payments of $624 thousand were made to retirees. The expected rate of return on plan

assets was 10%, and the actuary’s discount rate is 8%. There were no changes in

actuarial estimates and assumptions regarding the PBO.

What is the 2013 service cost for Havana’s plan?A. $276 thousand.

B. $528 thousand.

C. $648 thousand.

D. Cannot be determined from the given information.

Answer:

a) What non-accounting factors are important before evaluating whether a pending

lawsuit should be accrued as a liability and reflected in the financial statements?

b) What accounting factors should be considered in determining whether a pending

lawsuit should be accrued as a liability and reflected in the financial statements?

Answer:

Due to an error in computing depreciation expense, Prewitt Corporation overstated

accumulated depreciation by $20 million as of December 31, 2013. Prewitt has a tax

rate of 30%. Prewitt’s retained earnings as of December 31, 2013, would be: A.

Overstated by $14 million.

B. Understated by $14 million.

C. Overstated by $6 million.

D. Understated by $6 million.

Answer:

If a company uses the balance sheet approach to estimate bad debt expense, bad debt

expense for a period can be determined by: A. Multiplying net credit sales by the bad

debt experience ratio.

B. Adding the beginning balance in the allowance for uncollectible accounts to the

provision for uncollectible accounts and deducting the desired ending balance in the

allowance for uncollectible accounts.

C. Multiplying ending accounts receivable in each age category by the expected loss

ratio for each age category.

D. Taking the difference between the unadjusted balance in the allowance account and

the desired balance.

Answer:

Which of the following causes a permanent difference between taxable income and

pretax accounting income? A. The installment method used for sales of property.

B. MACRS depreciation method used for equipment.

C. Interest income on municipal bonds.

D. Percentage-of-completion method for long-term construction contracts.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1) Changes in accounting

estimates

2) Prior period adjustment

3) Current period adjustment to income statement only

4) Pro forma disclosure

5) Prospective approach

A. Handled prospectively

B. No longer used for changes in accounting principle

C. Adjustment to retained earnings of earliest year reported

D. journal entry needed, but disclosure is required

E. “As if” amounts for net income and EPS

Answer:

The following is the 2011 report of the independent registered public accounting firm

for The Great Atlantic & Pacific Tea Company, Inc., a large supermarket chain:

In our opinion, the accompanying consolidated balance sheets and the related

consolidated statements of operations, stockholders’ deficit and comprehensive loss, and

cash flows present fairly, in all material respects, the financial position of The Great

Atlantic & Pacific Tea Company, Inc. and its subsidiaries (debtor-in-possession) at

February 26, 2011 and February 27, 2010, and the results of their operations and their

cash flows for each of the three years in the period ended February 26, 2011 in

conformity with accounting principles generally accepted in the United States of

America. In addition, in our opinion, the financial statement schedule listed in Item

15(a)(2) presents fairly, in all material respects, the information set forth therein when

read in conjunction with the related consolidated financial statements. Also in our

opinion, the Company maintained, in all material respects, effective internal control

over financial reporting as of February 26, 2011, based on criteria established in

Internal Control – Integrated Framework issued by the Committee of Sponsoring

Organizations of the Treadway Commission (COSO). The Company’s management is

responsible for these financial statements and financial statement schedule, for

maintaining effective internal control over financial reporting and for its assessment of

the effectiveness of internal control over financial reporting, included in Management’s

Annual Report on Internal Control over Financial Reporting appearing under Item 9A.

Our responsibility is to express opinions on these financial statements, on the financial

statement schedule, and on the Company’s internal control over financial reporting

based on our integrated audits. We conducted our audits in accordance with the

standards of the Public Company Accounting Oversight Board (United States). Those

standards require that we plan and perform the audits to obtain reasonable assurance

about whether the financial statements are free of material misstatement and whether

effective internal control over financial reporting was maintained in all material

respects. Our audits of the financial statements included examining, on a test basis,

evidence supporting the amounts and disclosures in the financial statements, assessing

the accounting principles used and significant estimates made by management, and

evaluating the overall financial statement presentation. Our audit of internal control

over financial reporting included obtaining an understanding of internal control over

financial reporting, assessing the risk that a material weakness exists, and testing and

evaluating the design and operating effectiveness of internal control based on the

assessed risk. Our audits also included performing such other procedures as we

considered necessary in the circumstances. We believe that our audits provide a

reasonable basis for our opinions.

The accompanying financial statements have been prepared assuming that the Company

will continue as a going concern. However, the Company is currently operating

pursuant to a Chapter 11 bankruptcy filing which, together with the uncertain outcomes

of the matters discussed in Note 1 to the consolidated financial statements, raise

substantial doubt about the Company’s ability to continue as a going concern.

Management’s plans in regard to these matters are also described in Note 1. The

consolidated financial statements do not include any adjustments that might result from

the outcome of these uncertainties.

As discussed in Note 1 to the consolidated financial statements, the Company changed

the manner in which it accounts for share lending arrangements during fiscal 2010.

A company’s internal control over financial reporting is a process designed to provide

reasonable assurance regarding the reliability of financial reporting and the preparation

of financial statements for external purposes in accordance with generally accepted

accounting principles. A company’s internal control over financial reporting includes

those policies and procedures that (i) pertain to the maintenance of records that, in

reasonable detail, accurately and fairly reflect the transactions and dispositions of the

assets of the company; (ii) provide reasonable assurance that transactions are recorded

as necessary to permit preparation of financial statements in accordance with generally

accepted accounting principles, and that receipts and expenditures of the company are

being made only in accordance with authorizations of management and directors of the

company; and (iii) provide reasonable assurance regarding prevention or timely

detection of unauthorized acquisition, use, or disposition of the company’s assets that

could have a material effect on the financial statements.

Required:

Interpret the main points indicated in this report by A&P’s auditors.

Answer:

Under its executive stock option plan, W Corporation granted options on January 1,

2013, that permit executives to purchase 15 million of the company’s $1 par common

shares within the next eight years, but not before December 31, 2015 (the vesting date).

The exercise price is the market price of the shares on the date of grant, $18 per share.

The fair value of the options, estimated by an appropriate option pricing model, is $4

per option. No forfeitures are anticipated. The options are exercised on April 2, 2016,

when the market price is $21 per share. By what amount will W’s shareholder’s equity

be increased when the options are exercised? A. $60 million.

B. $270 million.

C. $315 million.

D. $330 million.

Answer:

Companies should report the cumulative effect of an accounting change in the income

statement: A. In the quarter in which the change is made.

B. In the annual financial statements only.

C. In the first quarter of the fiscal year in which the change is made.

D. Never.

Answer:

Archie Co. purchased a framing machine for $45,000 on January 1, 2013. The machine

is expected to have a four-year life, with a residual value of $5,000 at the end of four

years.

Using the sum-of-the-years’-digits method, depreciation for 2013 and book value at

December 31, 2013, would be: A. $18,000 and $27,000.

B. $16,000 and $29,000.

C. $16,000 and $24,000.

D. $18,000 and $22,000.

Answer:

The net pension liability (PBO minus plan assets) is increased by: A. Service cost.

B. Expected return on plan assets.

C. Amortization of prior service cost.

D. Cash contributions to plan assets.

Answer:

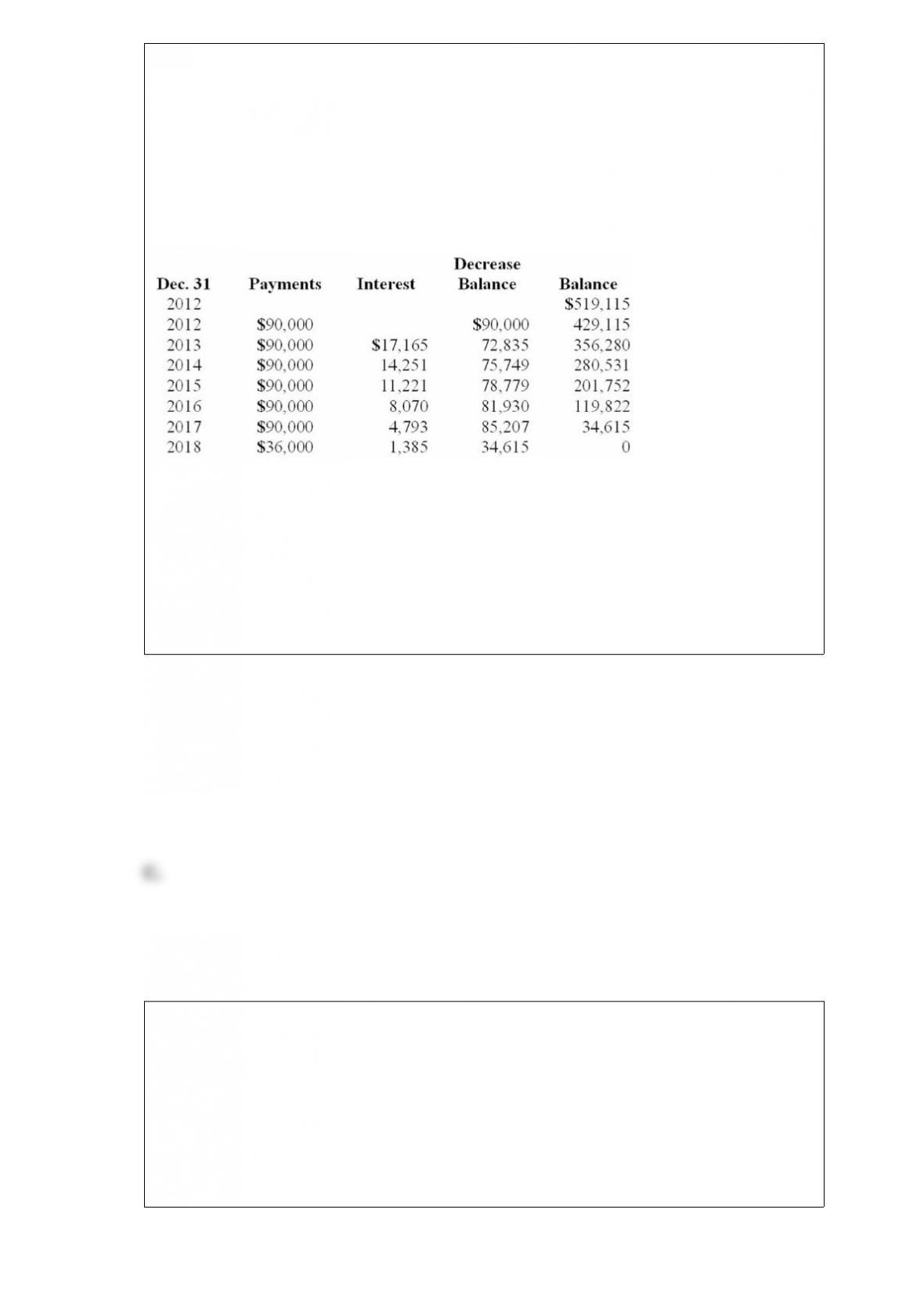

On December 31, 2012, Reagan Inc. signed a lease for some equipment having a

eight-year useful life with Silver Leasing Co. The lease payments are made by Reagan

annually, beginning at signing date. Title does not transfer to the lessee, so the

equipment will be returned to the lessor on December 31, 2018. There is no bargain

purchase option, and Reagan guarantees a residual value to the lessor on termination of

the lease.

Reagan’s lease amortization schedule appears below:

What is the amount of residual value guaranteed by Reagan to the lessor? A. $1,385.

B. $34,615.

C. $36,000.

D. Cannot be determined from the given information.

Answer:

The income statement reports changes in fair value for which type of securities? A.

Securities reported under the equity method.

B. Trading securities.

C. Held-to-maturity securities.

D. Securities available for sale.

Answer:

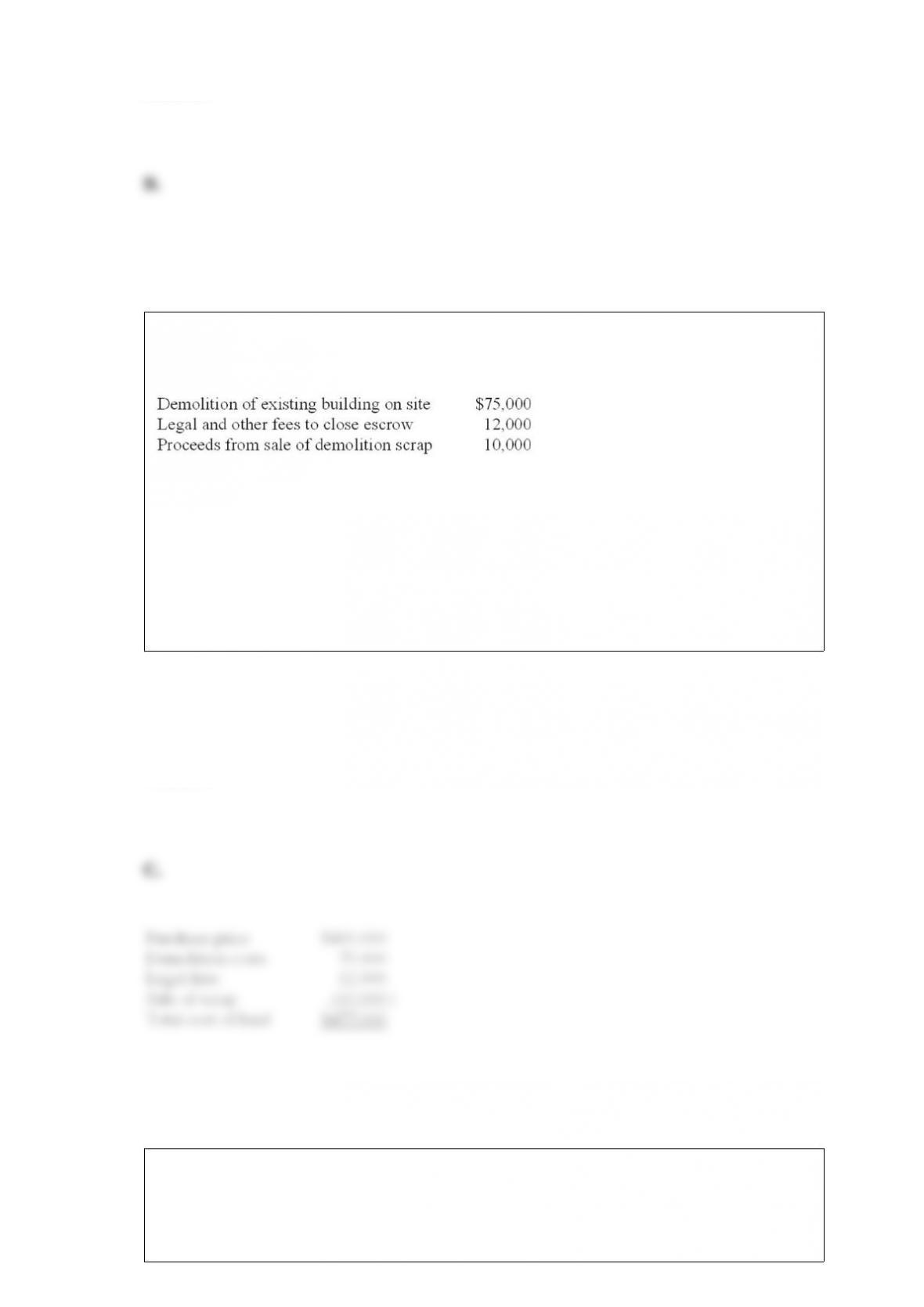

On July 1, 2013, Larkin Co. purchased a $400,000 tract of land that is intended to be

the site of a new office complex. Larkin incurred additional costs and realized salvage

proceeds during 2013 as follows:

What would be the balance in the land account as of December 31, 2013? A. $400,000.

B. $475,000.

C. $477,000.

D. $487,000.

Answer:

Universal Travel Inc. borrowed $500,000 on November 1, 2013, and signed a 12-month

note bearing interest at 6%. Interest is payable in full at maturity on October 31, 2014.

In connection with this note, Universal Travel Inc. should report interest payable at

December 31, 2013, in the amount of: A. $8,000.

B. $30,000.

C. $5,000.

D. $25,000.

Answer:

Hope Company bought 30% of Faith Corporation in the beginning of 2013. Hope’s

purchase price equaled 30% of the book value of Faith’s net identifiable assets, which

also equaled 30% of the fair value of Faith. During 2013, Faith reported net income in

the amount of $4,000,000 and declared and paid dividends in the amount of $500,000.

Hope mistakenly accounted for the investment as available for sale instead of using the

equity method. What effect would this error have on the investment account and net

income, respectively, for 2013? A. Overstated by $1,050,000; understated by

$1,050,000.

B. Understated by $1,050,000; understated by $1,050,000.

C. Overstated by $1,200,000; overstated by $1,200,000.

D. Understated by $1,200,000; overstated by $1,050,000.

Answer: