Once selected for existing assets, a company must consistently use the same method of

depreciation for all subsequent fixed asset acquisitions.

When available-for-sale securities are sold, the amount of gain or loss realized from the

date of purchase is included in before-tax net income.

A net operating loss (NOL) carryforward creates a deferred tax liability that should be

classified as current to the extent that the NOL will be recovered in the following year.

In a bank reconciliation, adjustments to the bank balance could include adding deposits

in transit and deducting bank service charges.

The difference between pension plan assets and the PBO is equal to the funded status of

the plan.

When treasury shares are resold at a price below cost:

a. Paid-in capital and/or retained earnings is reduced.

b. Paid-in capital and/or retained earnings is increased.

c. Retained earnings is always reduced.

d. A loss is taken on the income statement.

Broadway Ltd. purchased equipment on January 1, 2014, for $800,000, estimating a

five-year useful life and no residual value. In 2014 and 2015, Broadway depreciated the

asset using the straight-line method. In 2016, Broadway changed to sum-of-years’-digits

depreciation for this equipment. What depreciation would Broadway record for the year

2016 on this equipment?

a. $120,000.

b. $160,000.

c. $200,000.

d. $240,000.

MSG Corporation issued $100,000 of 3-year, 6% bonds outstanding on December 31,

2015 for $106,000. MSG uses straight-line amortization. On May 1, 2016, $10,000 of

the bonds were retired at 112. As a result of the retirement, MSG will report:

a. a $600 loss.

b. a $667 loss.

c. a $1,200 loss.

d. a $1,200 gain.

Portelli Services provides room-cleaning arrangements for hotels in Pennsylvania. On

April 1, Silvia Hotels & Resorts signed an agreement to outsource its room-cleaning

functions to Portelli. The contract specifies the service fee to be $15,000 per month, and

all payments are to be made shortly after the end of each quarter. It also specifies that

Portelli will receive an additional quarterly bonus of $3,000 if, during that quarter,

Silvia receives no more than five complaints from customers about room cleanliness. –

On April 1, based on historical experience, Portelli estimated that there is a 75% chance

that it will earn the quarterly bonus.

– On May 5, Portelli learned that, during March, there were two complaints from

customers related to room cleanliness. Based on this new information, Portelli revised

its estimate downward to 40% that it would earn the quarterly bonus.

– On June 30, Silvia notified Portelli that, for the quarter ended, there were four

complaints associated with room cleanliness, so Portelli would receive the bonus. Two

days later, Portelli received all payments due for all services rendered in the second

quarter, including the bonus. Portelli bases estimates of variable consideration on the

most likely amount it expects to receive.

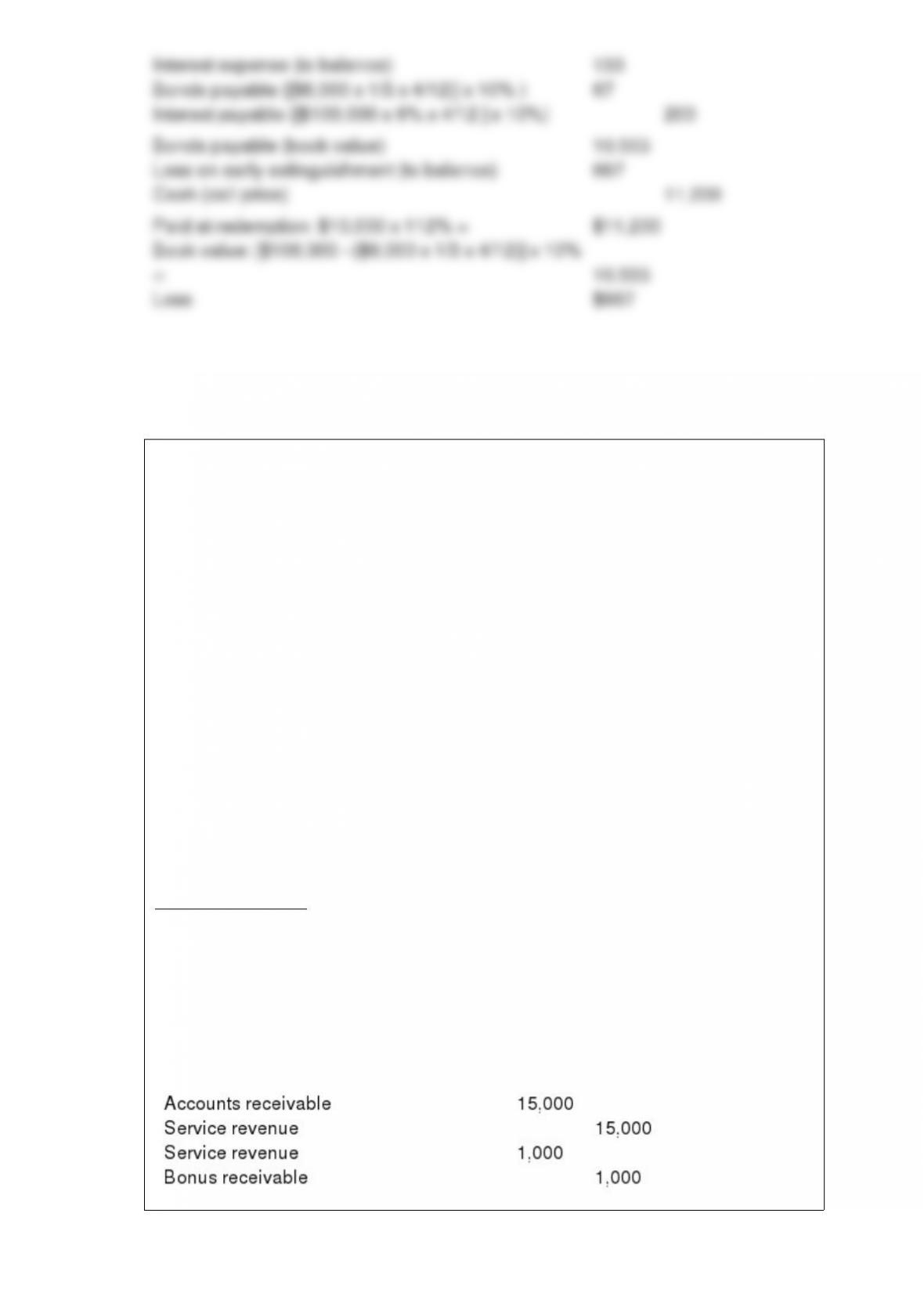

Prepare Portelli’s May 31 journal entry to record the revenue earned in May, as well as

any appropriate adjustments to the revenue earned in April. During the month of May,

Portelli earns service revenue of another $15,000. At this point, Portelli estimates that it

will most likely not be able to earn the quarterly bonus, based on the trend in the

number of customer complaints. Thus, Portelli must reduce its bonus receivable

recorded in April to zero and record the offsetting adjustment in revenue.

Jung Inc. owns a patent for which it paid $66 million. At the end of 2016, it had

accumulated amortization on the patent of $16 million. Due to adverse economic

conditions, Jung’s management determined that it should assess whether an impairment

loss should be recognized for the patent. The estimated undiscounted future cash flows

to be provided by the patent total $43 million, and the patent’s fair value at that point is

$35 million. Under these circumstances, Lester:

a. Would record no impairment loss on the patent.

b. Would record a $7 million impairment loss on the patent.

c. Would record a $15 million impairment loss on the patent.

d. Would record a $31 million impairment loss on the patent.

Dave’s Duds reported cost of goods sold of $2,000,000 this year. The inventory account

increased by $200,000 during the year to an ending balance of $400,000. What was the

cost of merchandise that Dave’s purchased during the year?

a. $1,600,000.

b. $1,800,000.

c. $2,200,000.

d. $2,400,000.

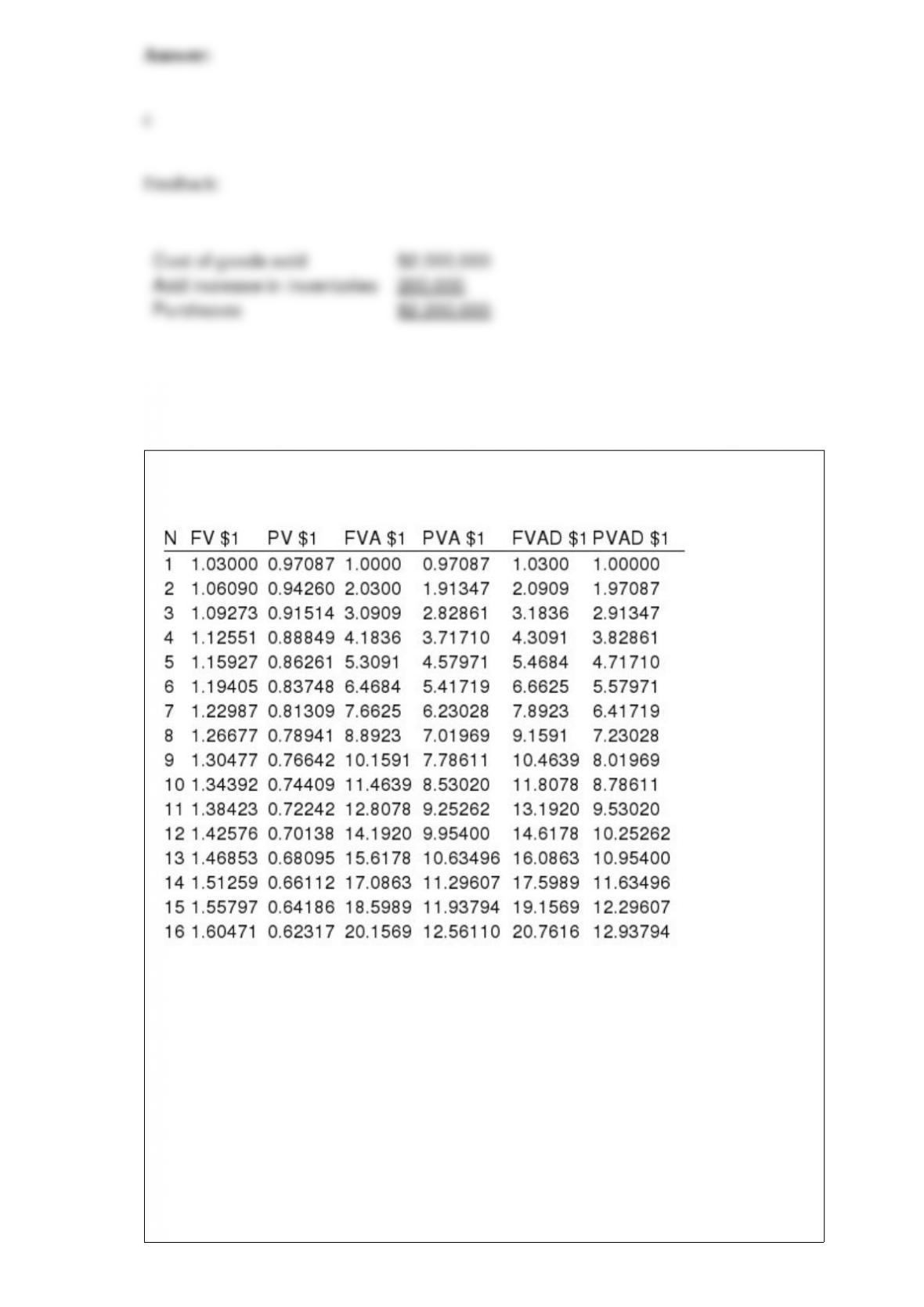

Present and future value tables of $1 at 3% are presented below:

A firm leases equipment under a capital lease (analogous to an installment purchase)

that calls for 12 semiannual payments of $39,014.40. The first payment is due at the

inception of the lease. The annual rate on the lease is 6%. What is the value of the

leased asset at inception of the lease?

a. $388,349.

b. $400,000.

c. $454,128.

d. $440,082.

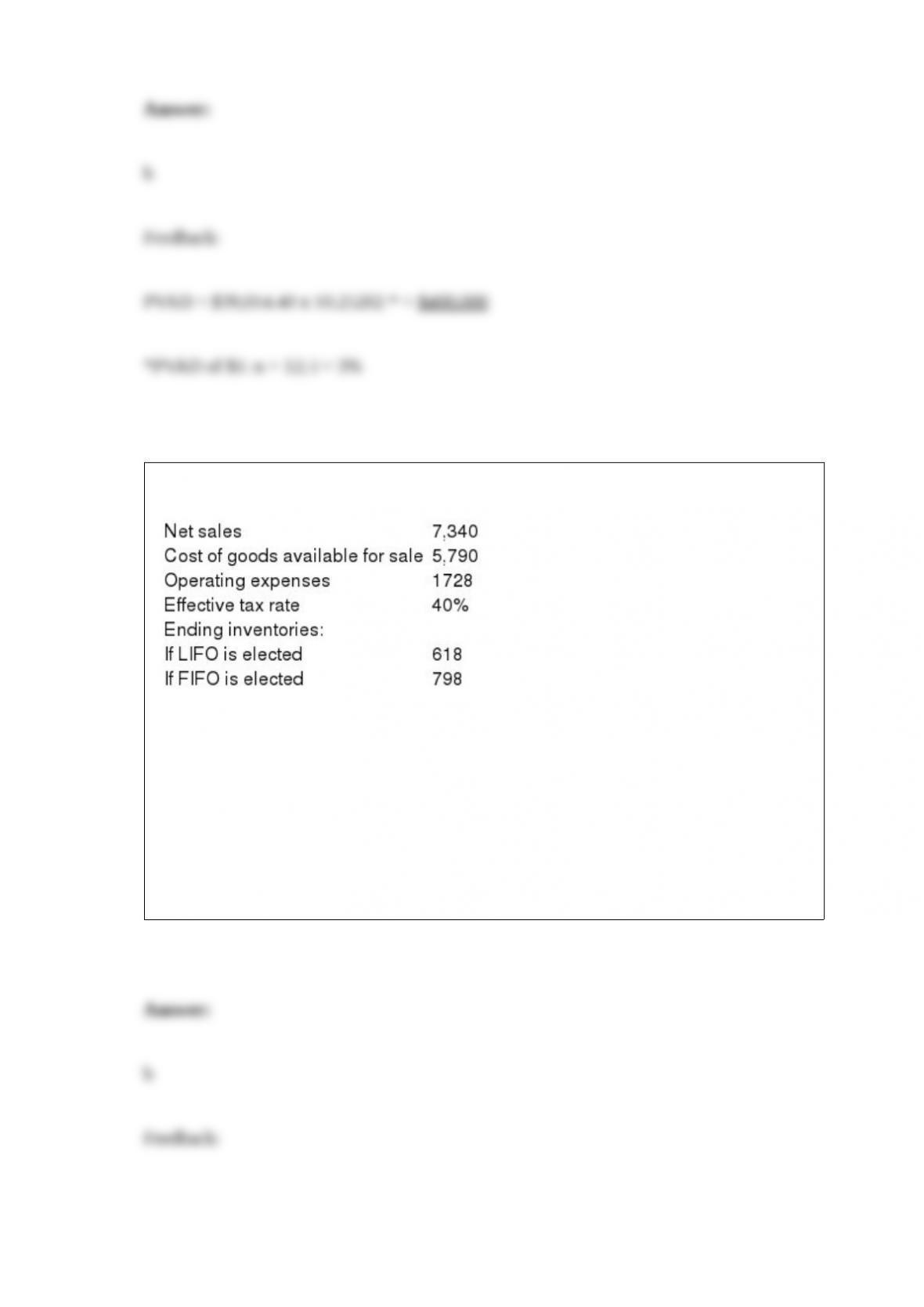

Nueva Company reported the following pretax data for its first year of operations.

What is Nueva’s net income if it elects LIFO?

a. $440.

b. $264.

c. $620.

d. $372.

Janson Corporation Co.’s trial balance included the following account balances at

December 31, 2016:

Investments consist of treasury bills that were purchased in November and mature in

January. Prepaid insurance is for the next two years. What amount should be included in

the current asset section of Janson’s December 31, 2016, balance sheet? a. $ 88.000.

b. $ 85,000.

c. $ 55,000.

d. $135,000.

Under its executive stock option plan, W Corporation granted options on January 1,

2016, that permit executives to purchase 15 million of the company’s $1 par common

shares within the next eight years, but not before December 31, 2018 (the vesting date).

The exercise price is the market price of the shares on the date of grant, $18 per share.

The fair value of the options, estimated by an appropriate option pricing model, is $4

per option. No forfeitures are anticipated. The options are exercised on April 2, 2019,

when the market price is $21 per share. By what amount will W’s shareholder’s equity

be increased when the options are exercised?

a. $ 60 million.

b. $270 million.

c. $315 million.

d. $330 million.

Examples of internal transactions include all of the following except:

a. Writing off an uncollectible account.

b. Recording the expiration of prepaid insurance.

c. Recording unpaid salaries.

d. Paying salaries to company employees.

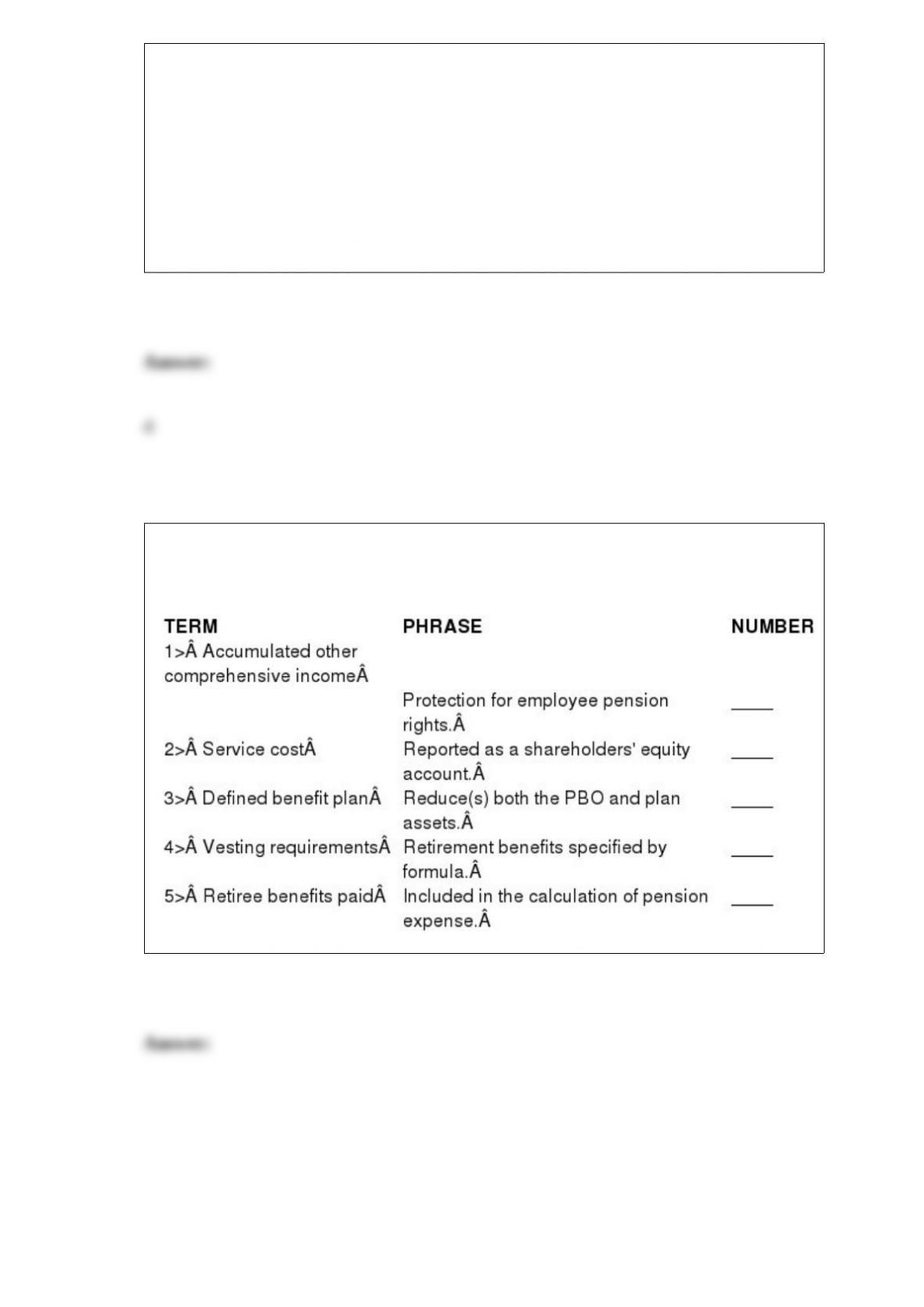

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the most correct term.

In the previous year, a firm failed to record premium amortization of $40,000 and

$30,000, respectively, on its bonds payable and held to maturity bond investments.

These errors affect both income before tax and taxable income. The firm’s tax rate is

30%. As a result of this error, net income was:

a. Understated by $7,000.

b. Overstated by $7,000.

c. Understated by $33,000.

d. Overstated by $33,000.

Under current tax law a net operating loss may be carried forward up to:

a. 5 years.

b. 10 years.

c. 15 years.

d. 20 years.

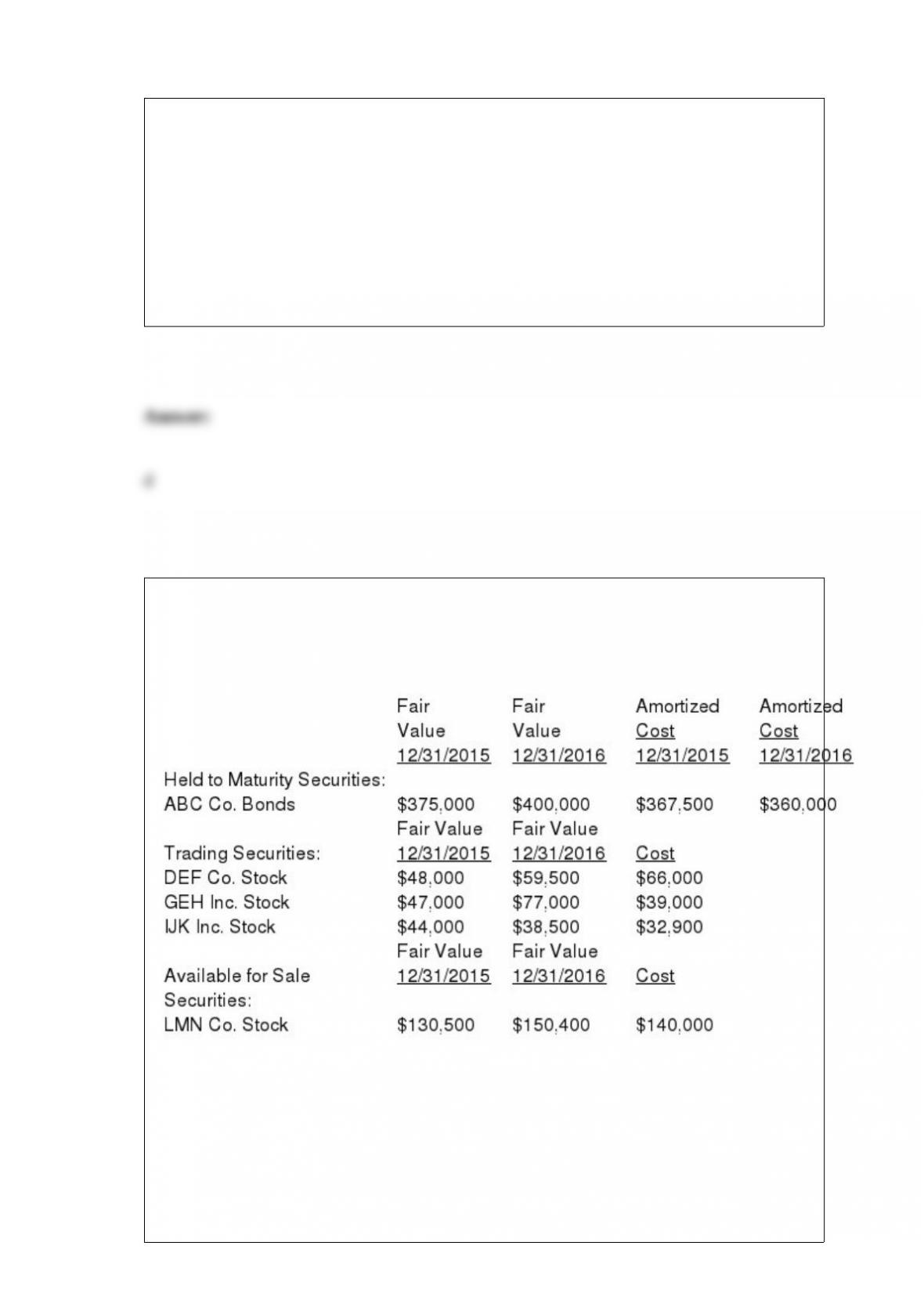

Beresford Inc. purchased several investment securities during 2015, its first year of

operations. The following information pertains to these securities. The fluctuations in

their fair values are not considered permanent.

What balance sheet amount would Beresford report for its total investment securities at

12/31/2015?

a. $637,000.

b. $644,500.

c. $645,400.

d. None of these answer choices is correct.

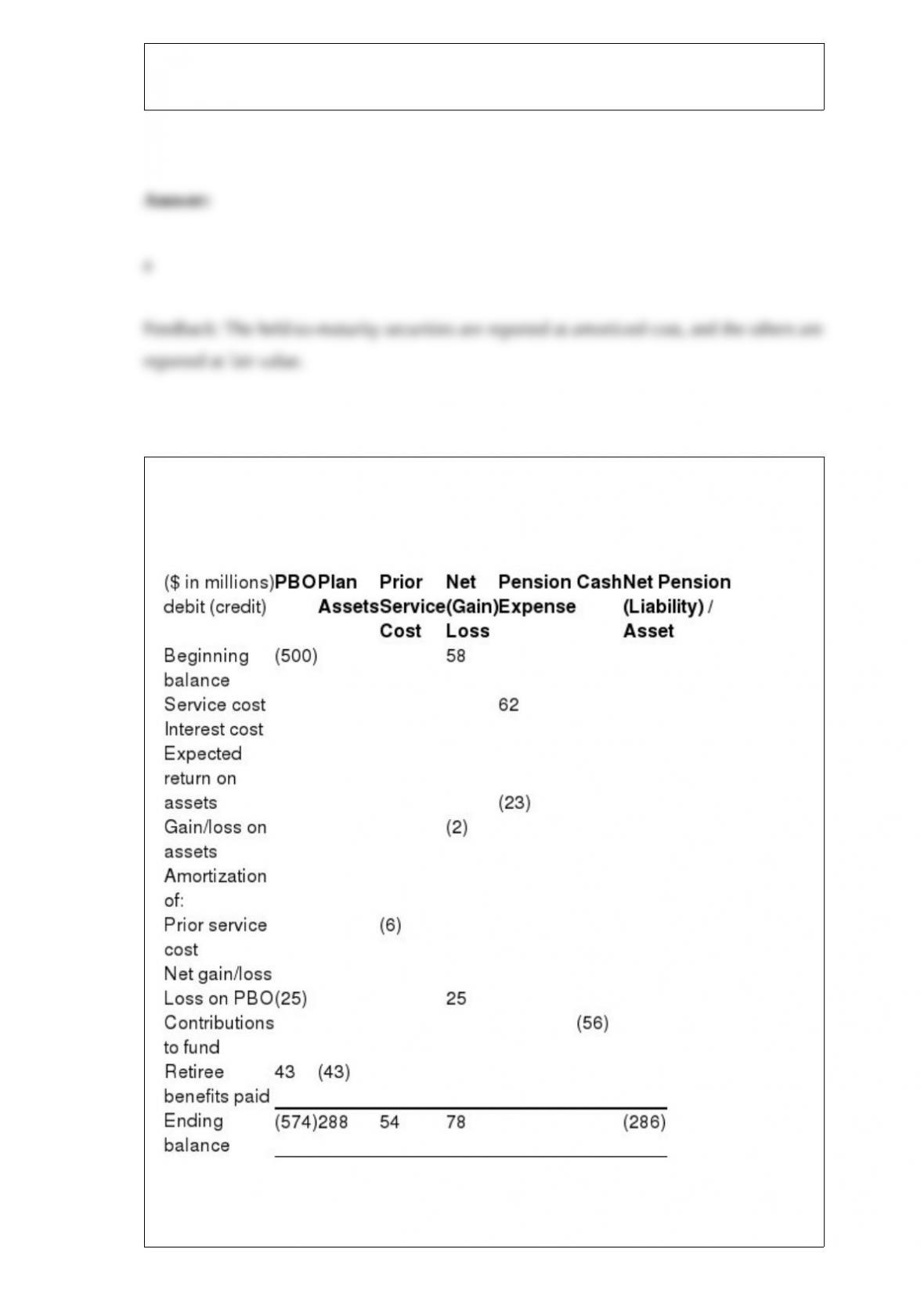

The following incomplete (columns have missing amounts) pension spreadsheet is for

Old Tucson Corporation (OTC).

What was the balance of the net pension asset / liability reported in the balance sheet at

the end of the previous year?

a. Net pension asset of $250.

b. Net pension asset of $442.

c. Net pension liability of $250.

d. Net pension liability of $442.

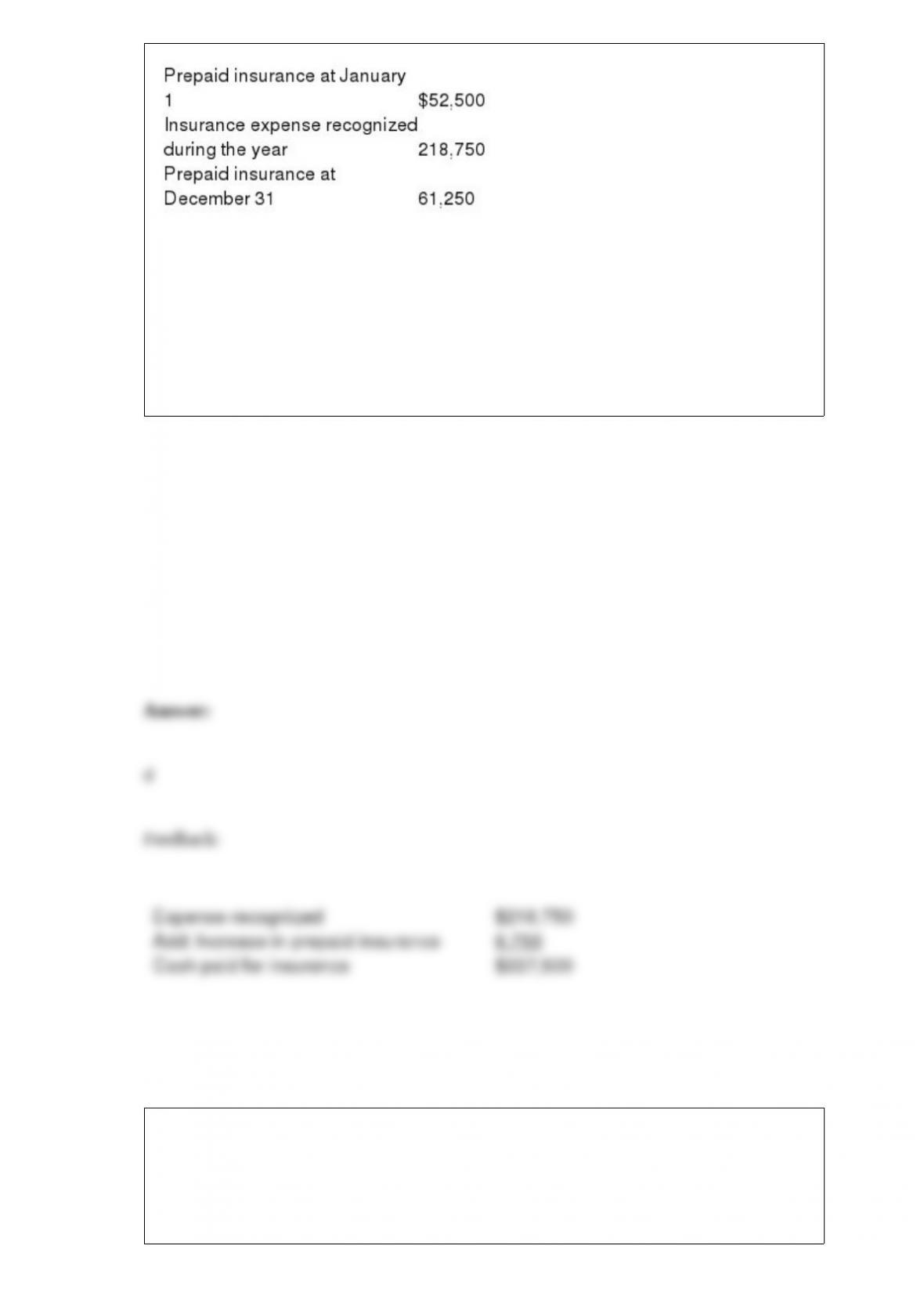

When Castle Corporation pays insurance premiums, the transaction is recorded as a

debit to prepaid insurance. Additional information for the year ended December 31 is as

follows:

What was the total amount of cash paid by Castle for insurance premiums during the

year?

a. $218,750

b. $166,250

c. $210,000

•

$227,500

When using the equity method to account for an investment, cash dividends received by

the investor from the investee should be recorded:

a. As a reduction in the investment account.

b. As an increase in the investment account.

c. As dividend income.

d. As a contra item to stockholders’ equity.

“VSOE” stands for:

a. “Vendor-specific objective evidence.”

b. “Vendor substantiation of earnings.”

c. “Value-specified operating earnings.”

d. “Variable set overhead earned.”

Why are earnings per share figures for prior years adjusted for stock splits and stock

dividends when data from prior years is presented in comparative financial statements?

($ in millions)

Service cost-2016 150

Past service cost 24

‘ƒDBO 174

Net interest cost (10% x [$960 – 600]) 36

Plan assets (10% x $600: interest income) 60

‘ƒDBO (10% x $960: interest cost) 96

DBO 44

Remeasurement gain from assumption change-OCI 44

Remeasurement loss-OCI ($40 – [10% x $600]) 20

Plan assets (actual return below 10%) 20

When Dharma adds its annual cash investment to its plan assets, the value of those plan

assets increases by $120 million:

To Record Funding

Plan assets 120

‘ƒCash (contribution to plan assets) 120

Retired employees were paid benefits of $72 million in 2016. Paying those benefits, of

course, reduces the obligation to pay benefits (the DBO), and since the payments are

made from the plan assets, that balance is reduced as well:

To Record Payment of Benefits

DBO 72

‘ƒPlan assets 72

Samson Inc. is contemplating the purchase of a machine that will provide it with net

after-tax cash savings of $100,000 per year for eight years. Interest is 10%. Assume the

cash savings occur at the end of each year.

Required: Calculate the present value of the cash savings.

Dharma Initiative, Inc., has a defined benefit pension plan. Characteristics of the plan

during 2016 are as follows:

($ in 000s)

‘ƒPBO balance, January 1 $960

Plan assets balance, January 1 600

Service cost 150

‘ƒInterest cost 90

‘ƒGain from change in actuarial assumption 44

Benefits paid (72)

‘ƒActual return on plan assets 40

‘ƒContributions 2016 120

The expected long-term rate of return on plan assets was 8%. There were no AOCI

balances related to pensions on January 1, 2016, but at the end of 2016, the company

amended the pension formula creating a prior service cost of $24 million.

Required:

1> Calculate the pension expense for 2016.

2> Prepare the journal entry to record pension expense, gains or losses, past service

cost, funding, and payment of benefits for 2016.

3> What amount will Dharma Initiative report in its 2016 balance sheet as a net pension

asset or net pension liability?

In its 2016 annual report to shareholders, Hyer Aviation Group Inc. included the

following disclosure:

On October 6, 2015, the company’s subsidiary, Pyro Aeroplex, filed suit against Syntex,

an unincorporated division of Bright American Corporation, for breach of contract and

fraud with regard to the supply of deficient wire rope that is installed as aircraft flight

control cables on WD-50 aircraft. The case, filed in the circuit court of Bell County,

Arkansas, was brought to trial and on September 20, 2016, a jury returned with a

verdict in favor of the company in the amount of $17.5 million. The Court, upon a

post-judgment motion filed by Pyro, reduced the judgment to $4.5 million. Pyro has

appealed that Order to the Supreme Court of Arkansas. The company believes the

appeal is without merit and will continue to pursue final judgment on the Order. The

company, pending appeal, has not recorded the $4.5 million favorable judgment.

Required:

What journal entries, if any, has Hyer recorded regarding this contingency? Explain its

rationale.