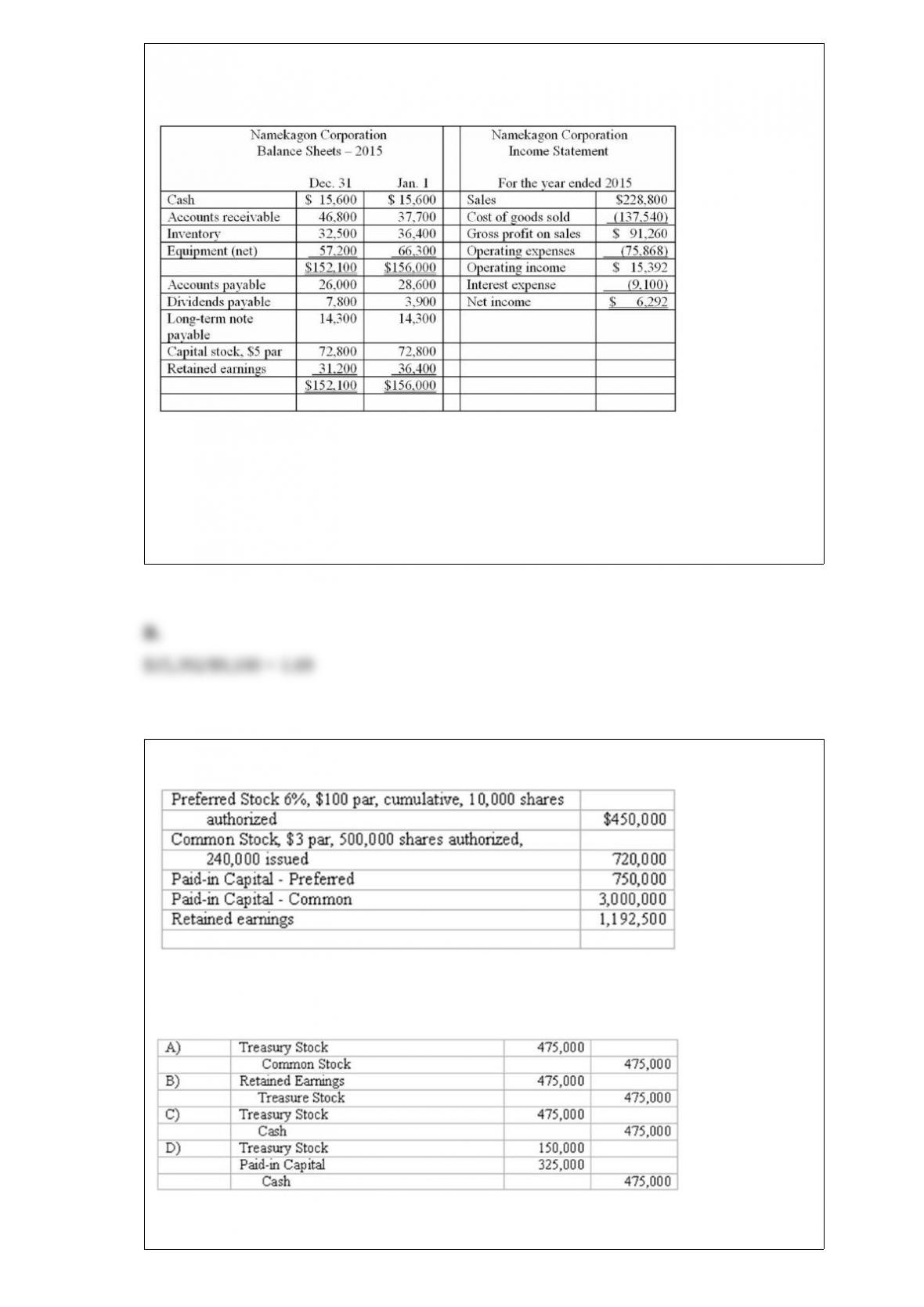

Given below are comparative balance sheets and an income statement for Namekagon

Corporation.

Refer to the information above. Namekagon Corporation’s interest coverage ratio for

2015 is:

A. 1.45.

B. 1.69.

C. 2.45.

D. 4.92.

Vision Corporation has the following information on its financial statement:

Refer to the information above. If Vision decided to purchase 50,000 shares of its

common stock to be used for future stock option plans at $9.50 per share, what journal

entry would they make?

A. Option A

B. Option B

C. Option C

D. Option D

Internal control over cash transactions

(a.) Describe two measures contributing to strong internal control over cash receipts.

(b.) Describe two measures contributing to effective internal control over cash

disbursements.

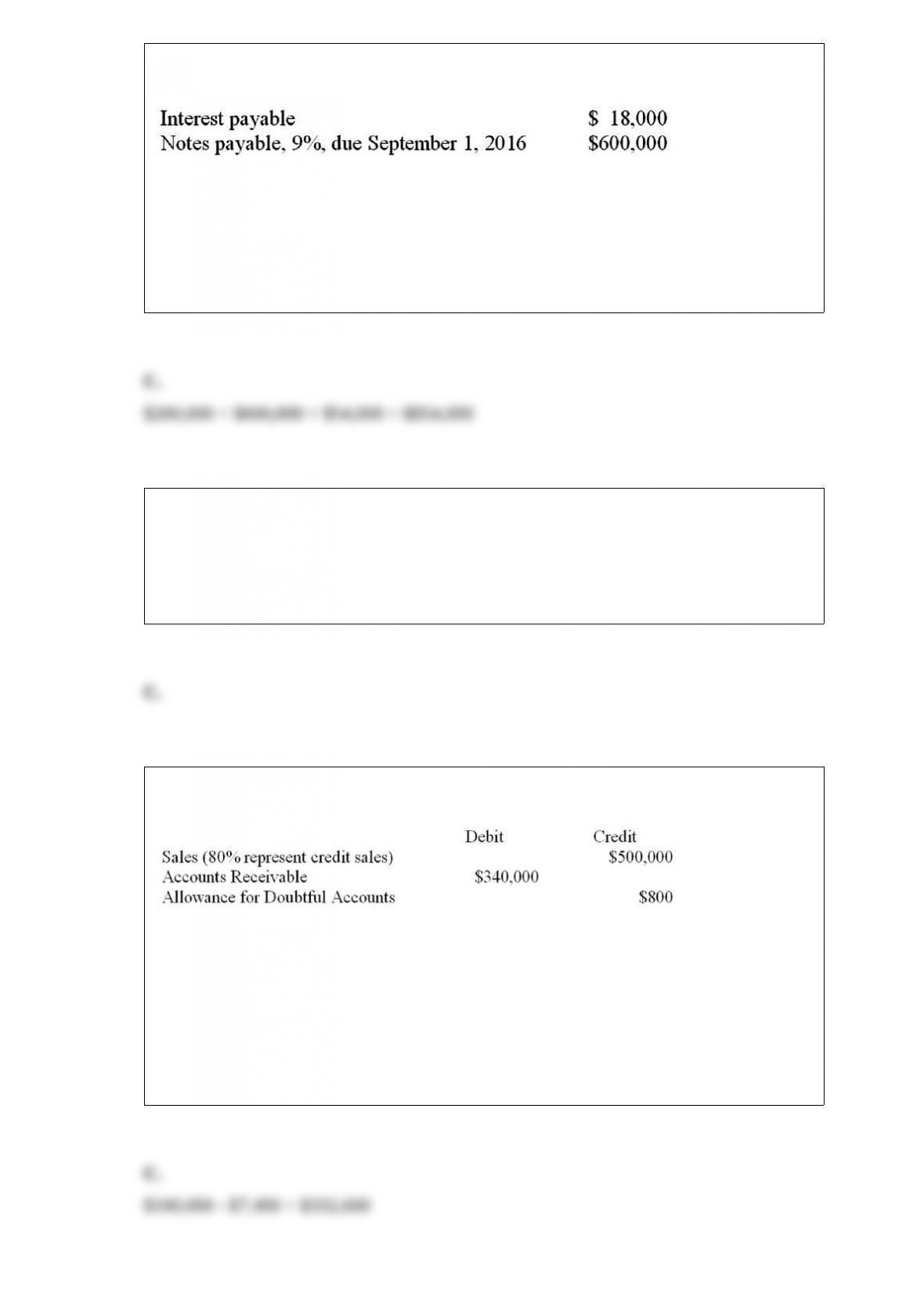

On September 1, 2015, Able Company purchased a building from Regal Corporation by

paying $200,000 cash and issuing a one-year note payable for the balance of the

purchase price. Interest on the note is stated at an annual rate of 9% and is paid at

maturity. In its December 31, 2015, balance sheet, Able correctly presented the note and

interest payable as follows:

Refer to the information above. What is the total cash (including interest) paid for the

building purchased by Able?

A. $800,000.

B. $836,000.

C. $854,000.

D. $816,000.

Examples of value-added activities include all of the following except:

A. Product design.

B. Assembly activities.

C. Machinery set-up activities.

D. Establishing efficient distribution channels.

At the end of January, the unadjusted trial balance of Windsor, Inc. included the

following accounts:

Refer to the information above. Windsor uses the balance sheet approach in estimating

uncollectible accounts expense, and aging the accounts receivable indicates the

estimated uncollectible portion to be $7,400. The net realizable value of Windsor’s

accounts receivable in the January 31 balance sheet is:

A. $331,800.

B. $340,000.

C. $332,600.

D. $347,400.

In a responsibility accounting system, the recording of revenue and costs begins with

the:

A. Most profitable segments of the business.

B. Least profitable segments of the business.

C. Broadest areas of management responsibility.

D. Smallest areas of management responsibility.

The year-end balance in the Materials Inventory controlling account is equal to:

A. The total of the various materials subsidiary ledger accounts (the materials on hand

at the end of the period.)

B. The total amount of materials requisitioned during the period.

C. The total amount of materials purchased during the period.

D. The amount of materials debited to the Work-in-Process Inventory account during

the period.

The concept of adequate disclosure requires a company to inform financial statement

users of each of the following, except:

A. The accounting methods in use.

B. The due dates of major liabilities.

C. Destruction of a large portion of the company’s inventory on January 20, three weeks

after the balance sheet date, but prior to issuance of the financial statements.

D. Income projections for the next five years based upon anticipated market share of a

new product; the new product was introduced a few days before the balance sheet date.

When using the net present value method for evaluating an investment, an increase in

the required rate of return will:

A. Make it more difficult to accept the investment.

B. Make it less difficult to accept the investment.

C. Not affect the decision, if the length of the investment’s benefits remain constant.

D. Not be a consideration because it is not used in the net present value method.

Traceable fixed costs that the manager of a department cannot change are called:

A. Controllable.

B. Committed.

C. Conditional.

D. Common.

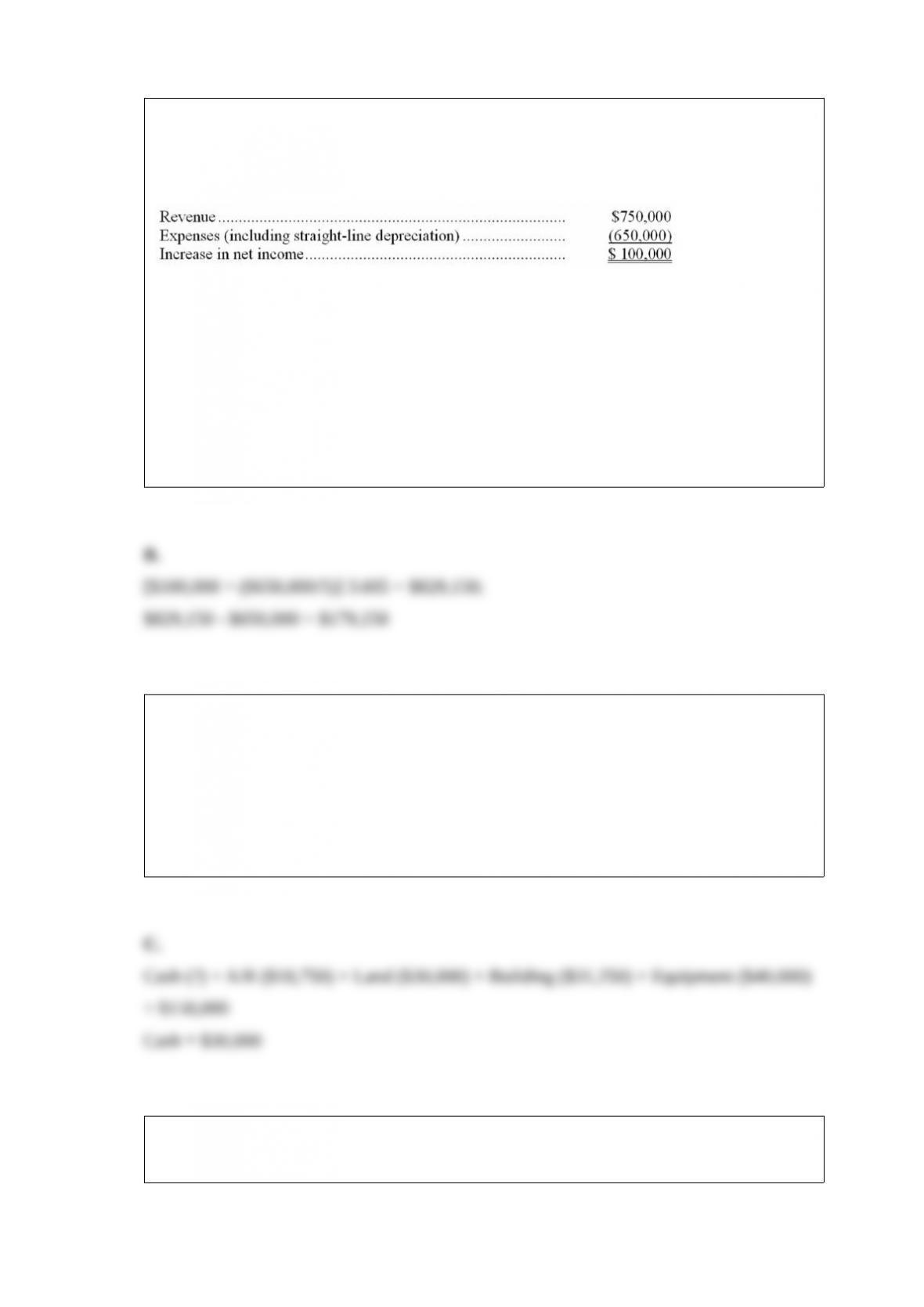

Rent expense in Marrin Company’s 2015 income statement is $420,000. If Prepaid Rent

was $70,000 at December 31, 2014, and is $95,000 at December 31, 2015, the cash paid

for rent during 2015 is:

A. $420,000.

B. $445,000.

C. $395,000.

D. $480,000.

In a process costing system, the number of units started and completed for a period is

equal to:

A. Units transferred out less units in beginning work in process.

B. Units transferred out less units in ending work in process.

C. Units transferred out plus units in beginning work in process.

D. Units transferred out plus units in ending work in process.

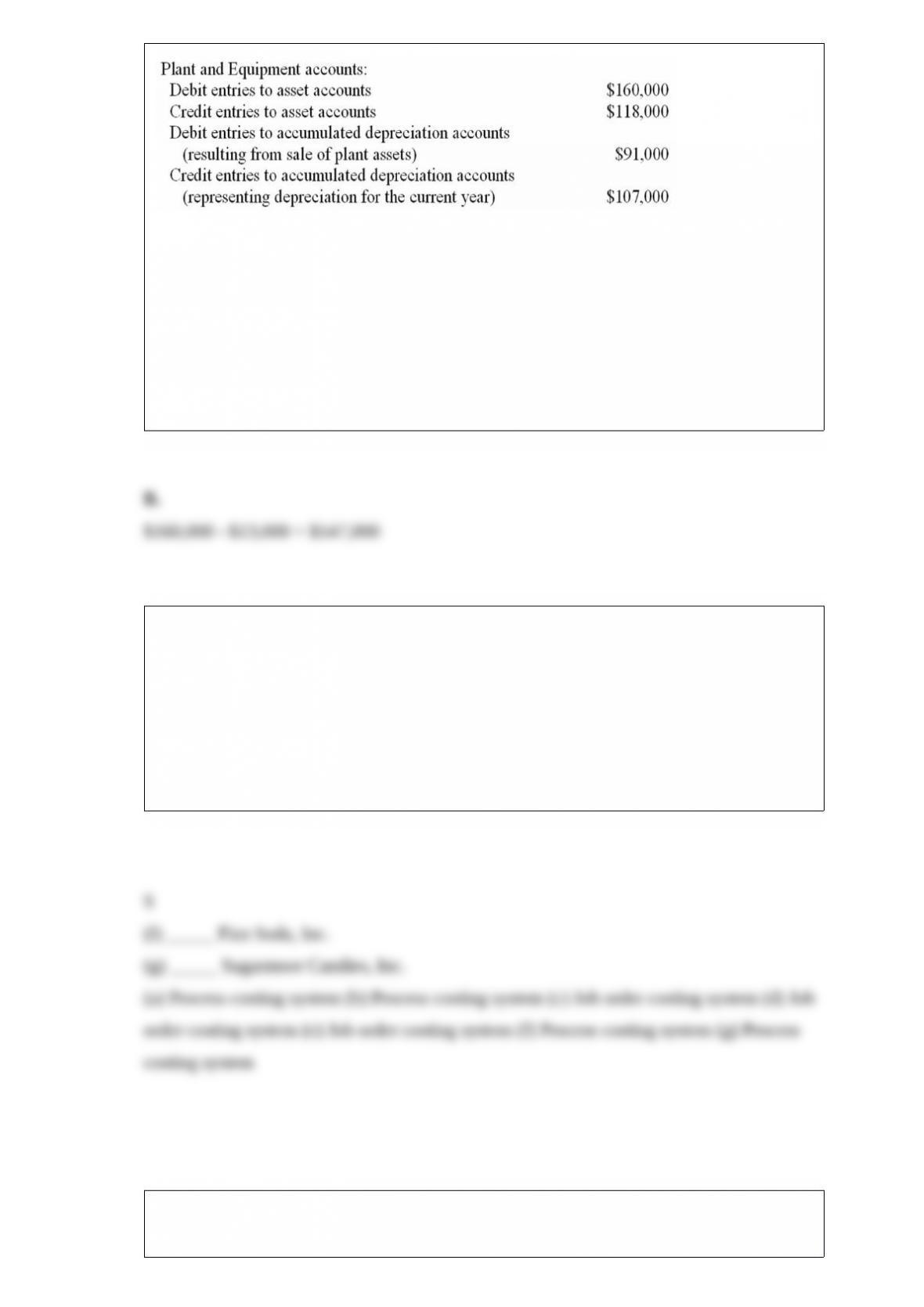

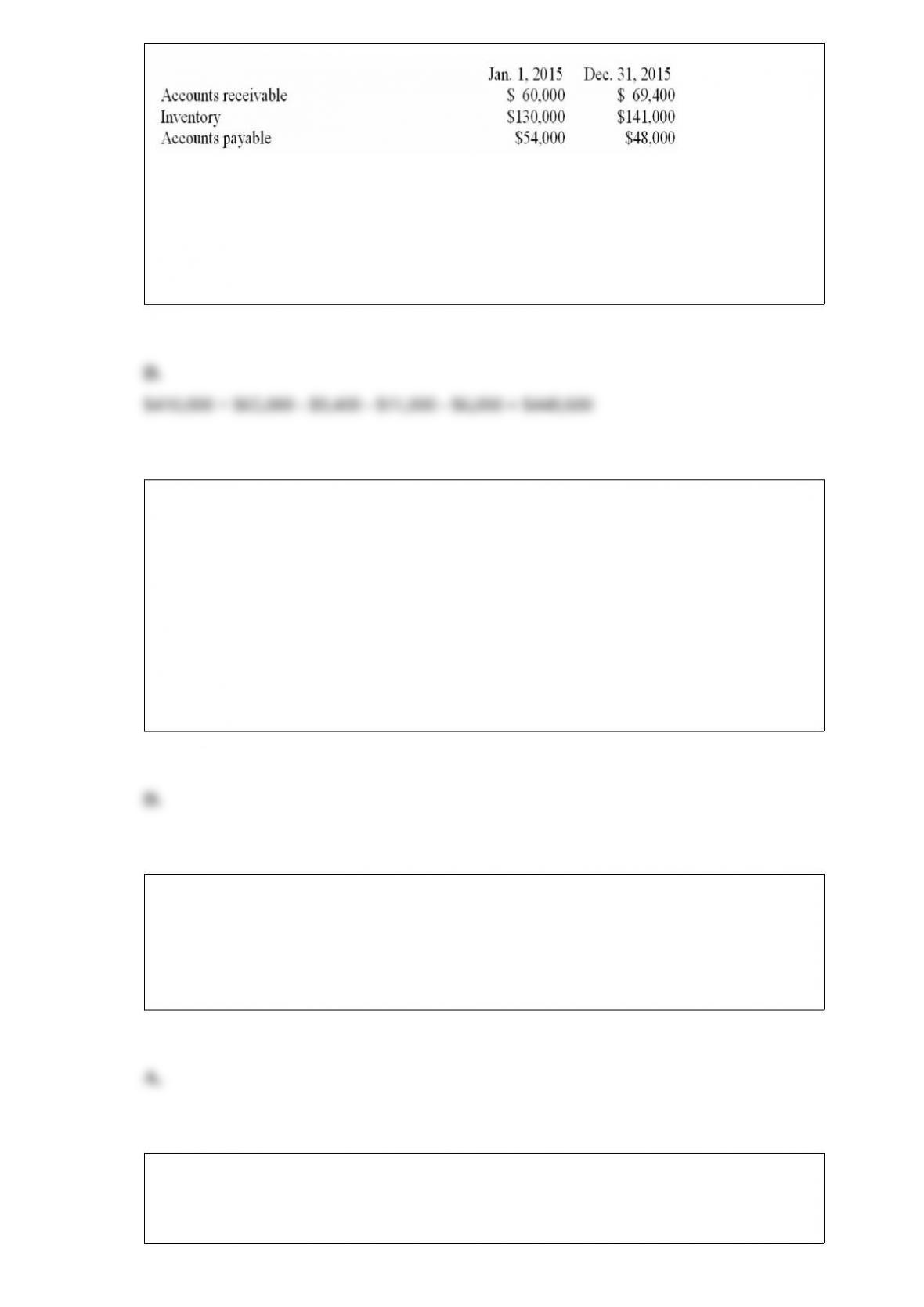

An analysis of changes in selected balance sheet accounts of Johnson Corporation

shows the following for the current year:

Johnson’s income statement for the current year includes a $14,000 loss on disposal of

plant assets. All payments and proceeds relating to purchase or sale of plant assets were

in cash.

Refer to the information above. Based solely on the data provided above, Johnson’s net

cash flow from investing activities for the current year is:

A. $160,000 net cash used by investing activities.

B. $147,000 net cash used by investing activities.

C. $13,000 net cash provided by investing activities.

D. $91,000 net cash used by investing activities.

Selecting an appropriate cost accounting system

Listed below are seven businesses. In the spaces provided, identify whether a job order

costing system or a process costing system would most likely be appropriate.

(a) _____ Nancy’s Paper Plate Company

(b) _____ Two Leg Pants Manufacturers, Inc.

(c) _____ Solid Residential Contractors

(d) _____ Float’s Boats

(e) _____ Big Heart Hospital

Equivalent units of production are:

A. A measure representing the percentage of a unit’s cost that has been completed.

B. Not computed separately for each input added during production.

C. Not assigned to beginning work-in-process or ending work-in-process.

D. The total units completed during the period.

During a period of steadily falling prices, which of the following methods of measuring

the cost of goods sold is likely to result in the lowest taxable income?

A. LIFO.

B. FIFO.

C. Average cost.

D. Specific identification.

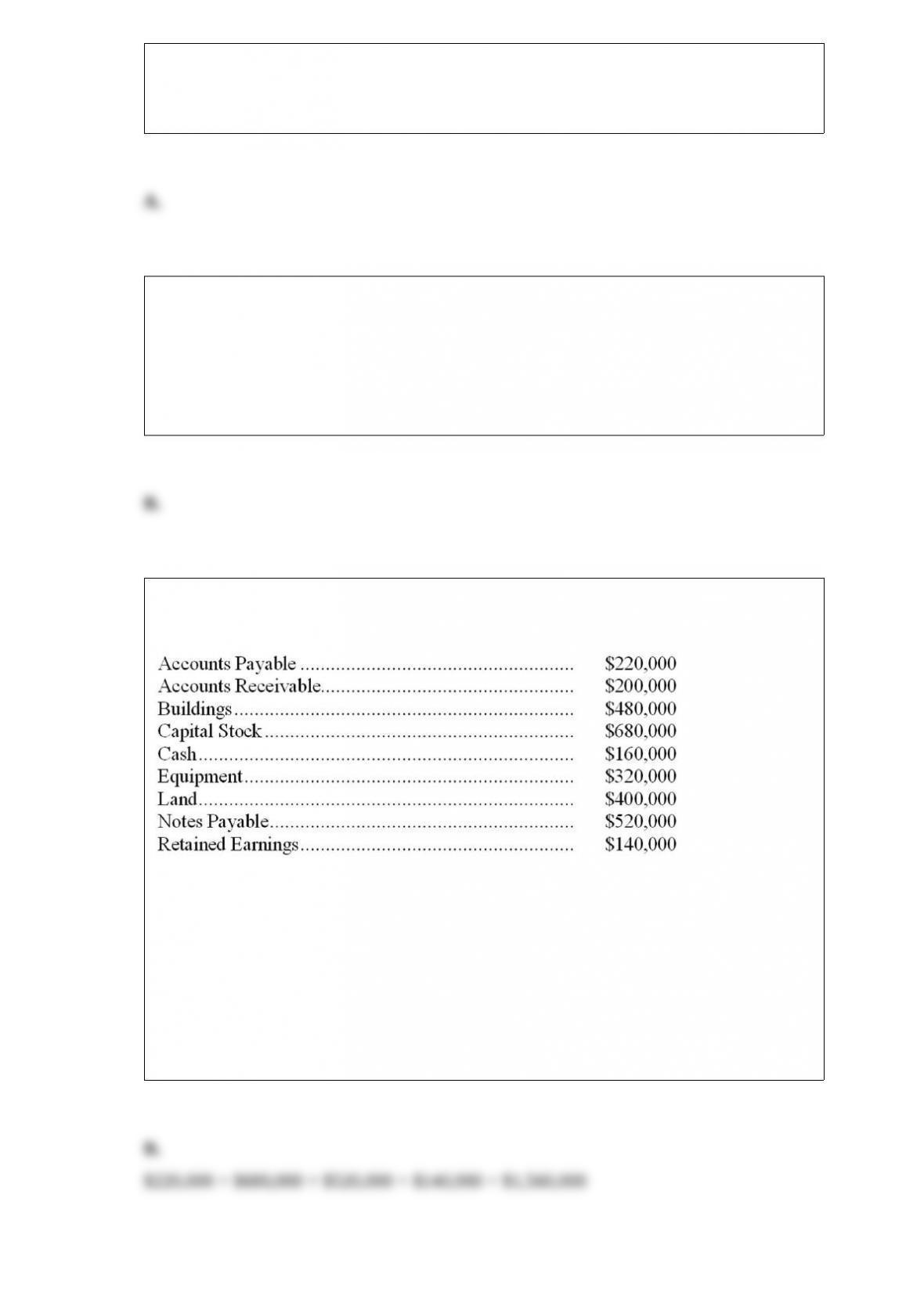

-Wilson Trucking, Inc. reports these account balances at January 1, 2015 (shown in

alphabetical order):

On January 5, Wilson Trucking collected $175,000 of its accounts receivable, paid

$150,000 on its accounts payable, and paid $11,000 on its note payable.

Refer to the information above. In a trial balance prepared for Wilson Trucking on

January 1, 2015, the total of the credit column is:

A. $1,580,000.

B. $1,560,000.

C. $1,620,000.

D. $3,120,000.

Most preferred stocks have one or more of the following characteristics, except:

A. To receive dividends on a preferred basis.

B. Cumulative dividends.

C. Voting rights.

D. Callable at the option of the corporation.

Retained earnings appears on:

A. The income statement.

B. The balance sheet.

C. The statement of cash flows.

D. All three of the financial statements.

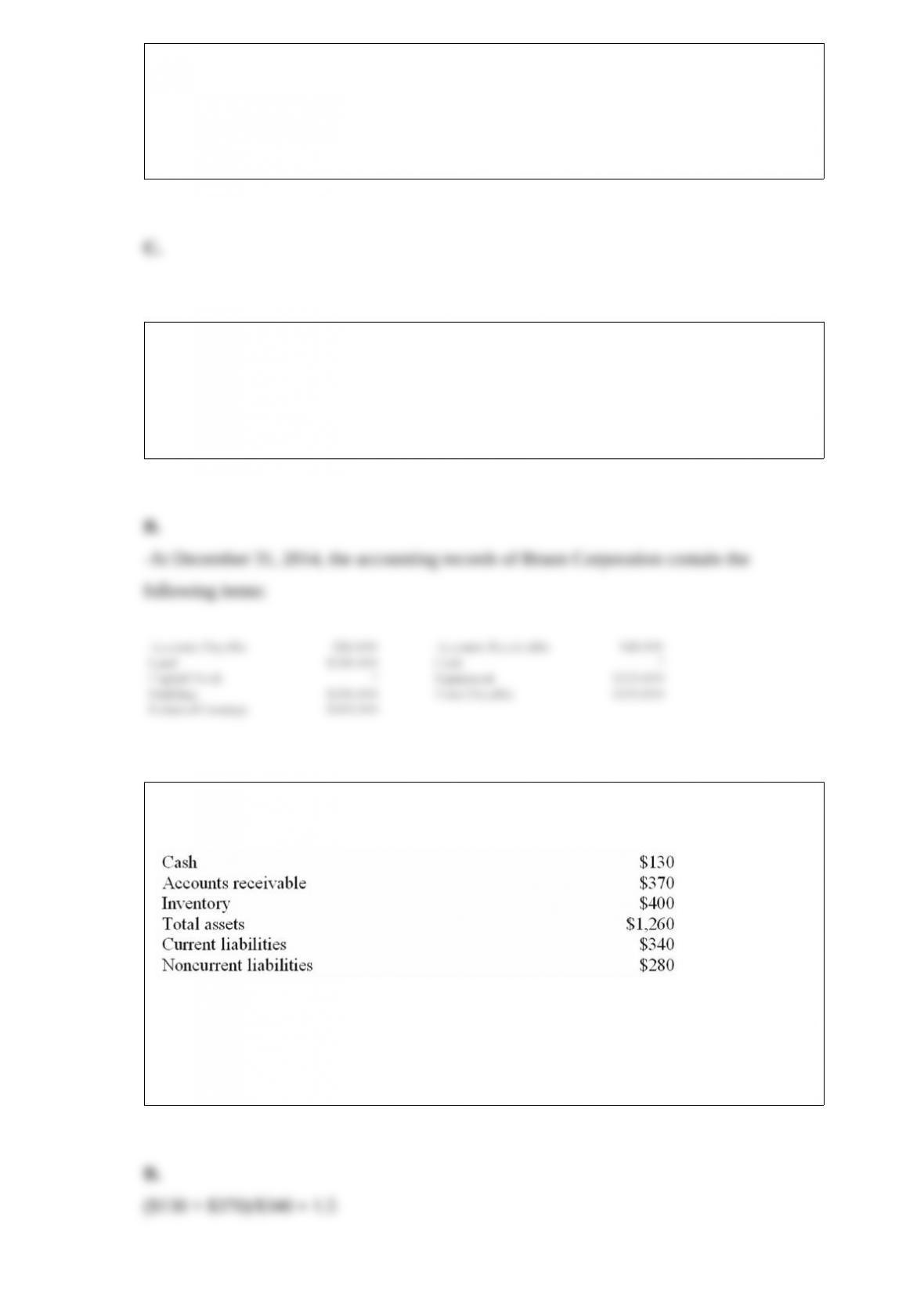

Shown below are selected data from the balance sheet of Bill’s Auto Parts, a retail store

(dollar amounts are in thousands):

Refer to the information above. What is the quick ratio?

A. 5%.

B. 1.5 to 1.

C. 20%.

D. 1.09 to 1.

-Indirect Oil Co. reports these account balances at December 31, 2014

On January 2, 2015, Indirect Oil collected $25,000 of its accounts receivable and paid

$20,000 of its accounts payable.

Refer to the information above. In a trial balance prepared at January 3, 2015, the total

of the debit column is:

A. $760,000.

B. $825,000.

C. $740,000.

D. $370,000.

Assuming a 365 day year, Gore Industries calculated an average of 53 days to collect its

accounts receivable in 2015. During 2015, Gore’s accounts receivable turnover rate:

A. Was approximately 6.89.

B. Was equal to 53 times its average accounts receivable.

C. Was approximately 0.15.

D. Can’t be determined from this information alone.

An organization that provides ratings of corporate governance services is:

A. SEC.

B. ISS.

C. IRS.

D. IBM.

Newman Labs is considering buying equipment which would enable the company to

obtain a five-year research contract. The specialized equipment costs $650,000 and will

have no salvage value when the five-year contract period is over. The estimated annual

operating results of the project are as follows:

All revenue from the contract and all expenses (except depreciation) will be received or

paid in cash in the same period as recognized for accounting purposes.

Refer to the information above. Compute the net present value of this investment, using

a discount rate of 12%. (An annuity table shows that the present value of $1 received

annually for five years, discounted at 12%, is 3.605.)

A. $468,650.

B. $179,150.

C. $289,500.

D. $829,150.

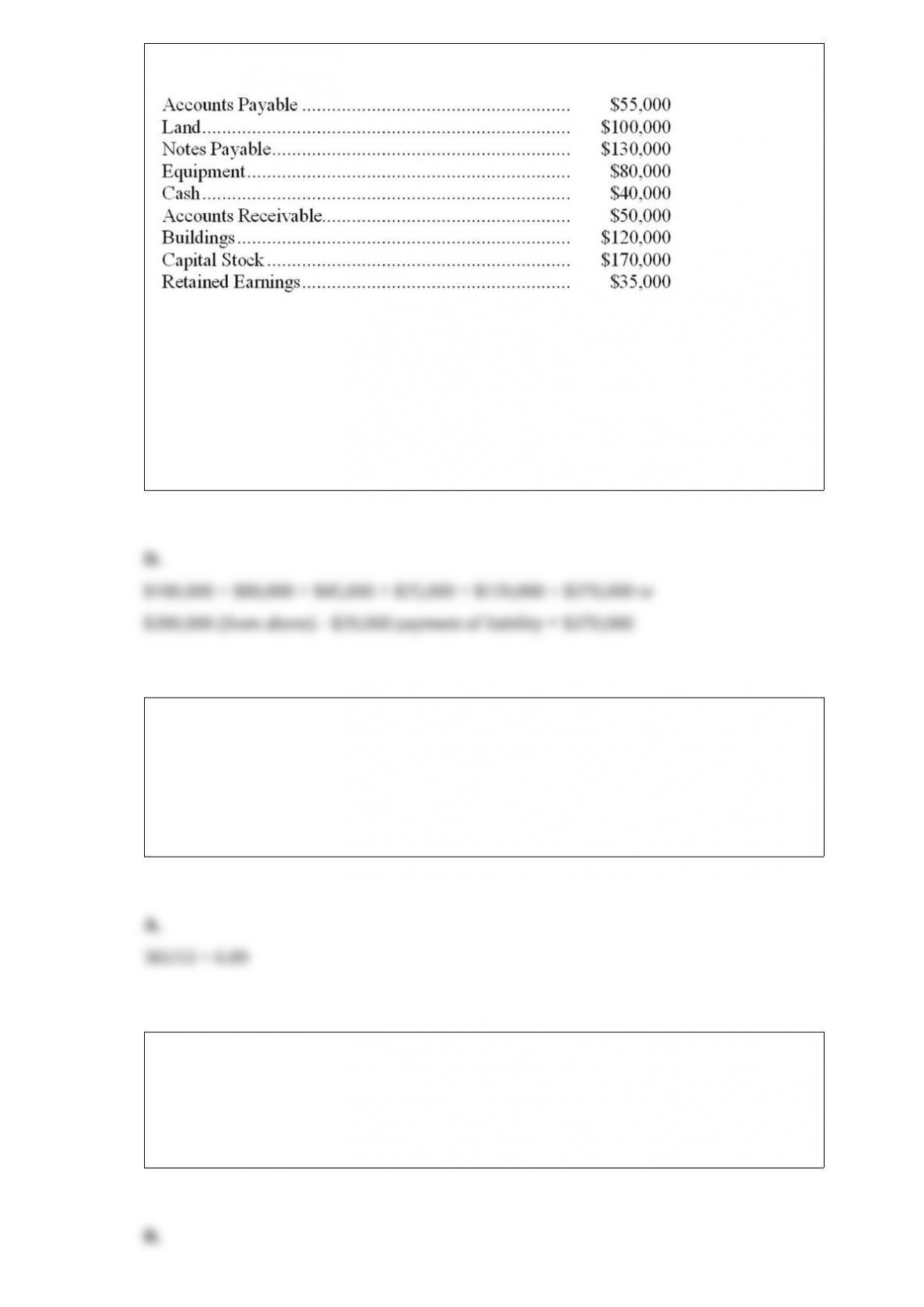

Refer to the information above. If the Notes Payable is $10,000, the December 31, 2014

cash balance is:

A. $60,000.

B. $160,000.

C. $30,000.

D. $20,000.

A/P ($2,500) + N/P ($10,000) + Capital Stock ($12,500) + R.E. ($125,000) = $150,000

Chapin Company reported net income of $410,000 for 2015. Balances of selected

current asset and current liability accounts are as shown on the indicated dates:

Depreciation expense for 2015 amounted to $65,000. Using only the above information,

compute Chapin’s net cash flow from operating activities (indirect method) for 2015:

A. $470,600.

B. $467,400.

C. $460,600.

D. $448,600.

Gannon Corporation uses the indirect method to prepare its statement of cash flows.

Following this approach, a gain on sale of equipment was deducted from net income in

computing net cash flow from operating activities. The most likely reason for this

adjustment is that:

A. The sale of equipment did not result in the receipt of any cash by Gannon

Corporation.

B. The sale resulted in a cash receipt in an accounting period different from the period

in which the gain was recognized.

C. The amount of the gain recognized was not equal to the cash received.

D. This type of transaction is not classified as an operating activity.

The book value of an asset in the plant and equipment category is:

A. The undepreciated cost of the asset.

B. The current replacement cost of the asset.

C. The original cost of the asset.

D. The accumulated depreciation on the asset to date.

Coca-Cola’s famous name printed in distinctive typeface is an example of:

A. A trademark.

B. A patent.

C. A copyright.

D. Goodwill.

Which of the following is not one of the three types of inventories of a manufacturing

company?

A. Raw materials inventory.

B. Work in process inventory.

C. Product inventory.

D. Finished goods inventory.

Cost centers are evaluated primarily on the basis of their ability to control costs and:

A. Their return on assets.

B. Residual income.

C. The quantity and quality of the services they provide.

D. Their contribution margin ratio.

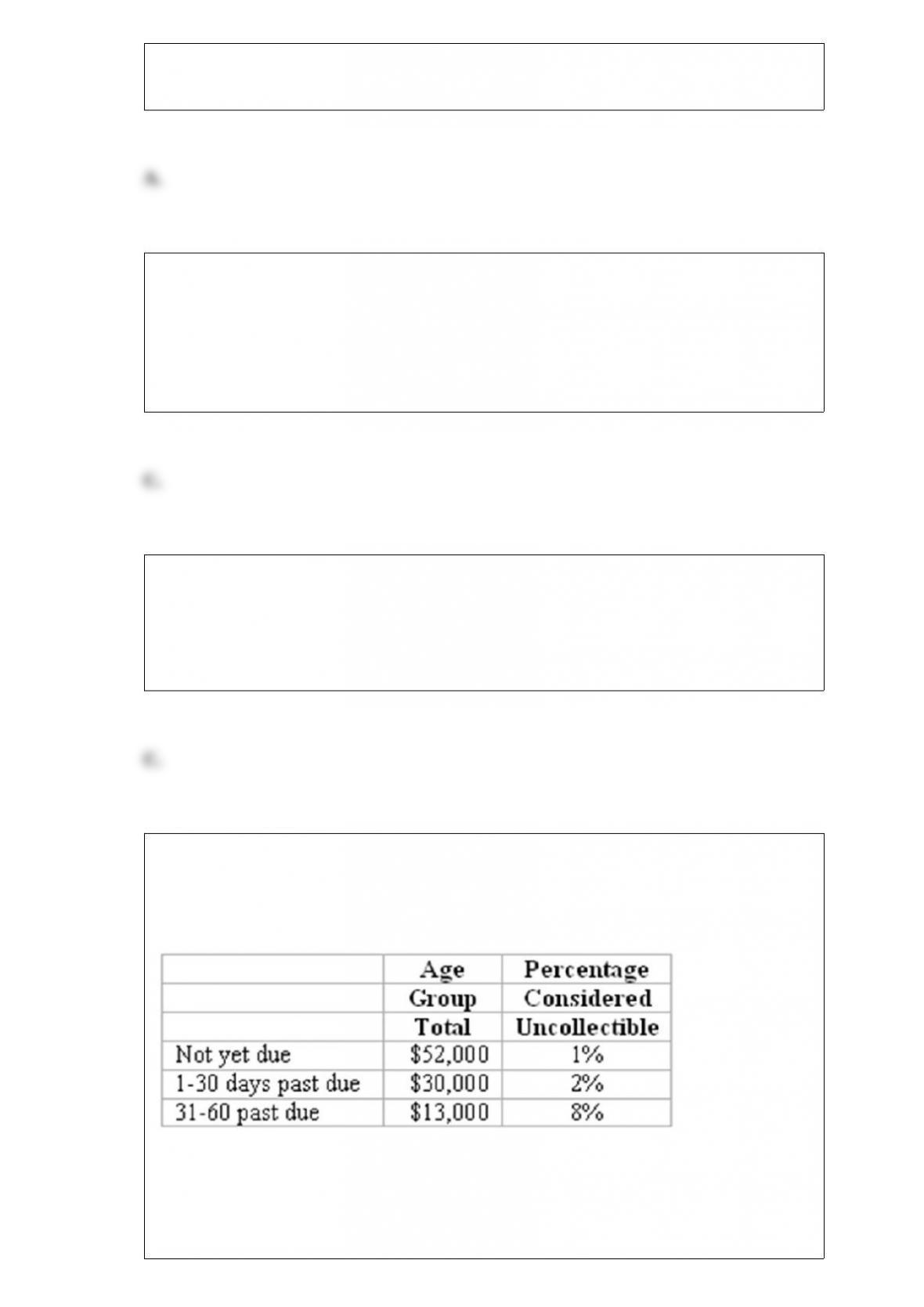

Oceanside Company uses the balance sheet approach in estimating uncollectible

accounts expense. Its Allowance for Doubtful Accounts has a $1,200 credit balance

prior to adjusting entries. It has just completed an aging analysis of accounts receivable

at December 31, 2015. This analysis disclosed the following information:

What is the appropriate balance for Oceanside’s Allowance for Doubtful Accounts at

December 31, 2015?

A. $95,000.

B. $960.

C. $3,360.

D. $2,160.

On April 1, 2015, Jetter Corporation reacquired 2,000 shares of its own $10 par stock

for $120,000 cash. On October 15, 2015, 600 of the treasury shares were reissued at a

price of $65 per share.

Refer to the information above. The reacquisition of the 2,000 shares on April 1, 2015,

causes:

A. No change in total assets of Jetter Corporation.

B. No change in the number of shares of Jetter Corporation stock outstanding.

C. A reduction in total assets and in total stockholders’ equity of Jetter Corporation.

D. Jetter Corporation to show a new asset, “Treasury Stock”, for $120,000.