1) Governmental Auditing Standards recognize that because of public accountability

over governmental activities the acceptable tolerable misstatement as compared to

commercial businesses may be:

A) equal

B) lower

C) higher

D) indeterminable

2) The audit procedure “Test clerical accuracy by footing the journals and tracing

postings to general ledger and to accounts payable and inventory master files” is used to

test the posting and summarization objective for acquisitions.

A) True

B) False

3) Tracing outstanding checks to subsequent period bank statements tests the cutoff

audit objective.

A) True

B) False

4) Most illegal acts affect the financial statements:

A) directly

B) only indirectly

C) both directly and indirectly

D) materially if direct; immaterially if indirect

5) An auditor who accepts an audit engagement and does not possess the industry

expertise of the business entity should:

A) engage financial experts familiar with the nature of the business entity

B) obtain a knowledge of matters that relate to the nature of the entity’s business

C) refer a substantial portion of the audit to another CPA who will act as the principal

auditor

D) first inform management that an unqualified opinion cannot be issued

6) Which of the following statements about the Securities Act of 1933 is not true?

A) A third-party that purchased securities described in the registration statement may

sue the auditor for material misrepresentations or omissions in the audited financial

statements

B) A third-party user does not have the burden of proof that he/she relied on the

financial statements

C) A third-party user has the burden of proof that the auditor was either negligent or

fraudulent in doing the audit

D) A third-party user does not have the burden of proof that the loss was caused by the

misleading statements

7) Which of the following combinations is correct?

A) Existence relates to whether the amounts in accounts are understated

B) Occurrence relates to whether balances exist

C) Existence relates to whether amounts included exist

D) Occurrence relates to whether the amounts in accounts occurred in the proper year

8) Which of the following would the auditor be most concerned about regarding a

heightened risk of intentional misstatement?

A) senior management emphasizes that it is very important to beat analyst estimates of

earnings every reporting period

B) senior management emphasizes that budgeted amounts for expenses are to be

achieved for each reporting period or explained in the variance analysis report

C) senior management emphasizes that job rotation is a worthwhile corporate objective

D) senior management emphasizes that job evaluations are based on performance

9) A comparison of the current year’s inventory turnover ratio with previous years’ may

indicate the presence of obsolete inventory.

A) True

B) False

10) If an auditor concludes that internal controls are likely to be effective, the

preliminary assessment of control risk can be reduced, leading to which of the

following impacts on the acceptable risk of incorrect acceptance?

A) reduction in

B) increase in

C) elimination of

D) increase or decrease

11) In testing for cutoff, the objective is to determine:

A) whether all of the current period’s transactions are recorded

B) whether transactions are recorded in the correct accounting period

C) the proper cutoff between capitalizing and expensing expenditures

D) the proper cutoff between disclosing items in footnotes or in account balances

12) Audit evidence has two primary qualities for the auditor; relevance and reliability.

Given the choices below which provides the auditor with the most reliable audit

evidence?

A) general ledger account balances

B) confirmation of accounts receivable balance received from a customer

C) internal memo explaining the issuance of a credit memo

D) copy of month-end adjusting entries

13) Effectiveness is concerned with whether defined goals are achieved, whereas

efficiency is concerned with whether the goals are achieved with a minimum use of

resources.

A) True

B) False

14) The auditor generally decides whether the inventory count can be taken before

year-end primarily on the basis of:

A) audit efficiency

B) accuracy of the perpetual inventory master files

C) client convenience

D) audit staff availability

15) In an action against a CPA in a jurisdiction that follows the Ultramares doctrine,

lack of privity is a viable defense provided the plaintiff:

A) is the client’s creditor who sued the CPA for negligence

B) can prove gross negligence

C) violated the Securities Act of 1933

D) violated the Securities Act of 1934

16) Which of the following statements is false?

A) Either an overstatement of an asset account or an understatement of a liability

account would have the same effect on the income statement

B) A misclassification in the balance sheet will have no effect on operating income

C) Either an overstatement of an asset account or an overstatement of a liability account

would have the same effect on the income statement

D) Either an understatement of an asset account or an overstatement of a liability

account would have the same effect on the income statement

17) Auditors who test manual controls that rely on IT-generated reports must consider:

A) the benefits of relying on IT-generated reports

B) separation of duties related to the IT-generated reports

C) the controls related to the accuracy of the information in the report

D) whether the manual controls are approved by the audit committee

18) Which of the following audit procedure would normally be included in the audit

plan when auditing the allowance for doubtful accounts?

A) Send positive confirmations

B) Inquire of the client’s credit manager

C) Send negative confirmations

D) Examine sales invoices

19) Output controls are not designed to assure that data generated by the computer are:

A) accurate

B) distributed only to authorized people

C) complete

D) used appropriately by management

20) Match nine of the terms (a-k) with the definitions provided below (1-9):

a.Foot

b.Compute

c.Scan

d.Inquire

e.Count

f.Trace

g.Reperform

h.Read

i.Examine

j.Observe

k.Compare

________ 1> A calculation done by the auditor independent of the client.

________ 2> Addition of a column of numbers to determine if the total is the same as

the client’s.

________ 3> A comparison of information in two different locations.

________ 4> A use of the senses to assess certain activities.

________ 5> Following details of transactions from original documents to journals.

________ 6> A less detailed examination of a document or record to determine if there

is something unusual warranting further investigation.

________ 7> Obtaining information from the client in response to specific questions.

________ 8> A determination of assets on hand at a given time.

________ 9> An examination of written information to determine facts pertinent to the

audit.

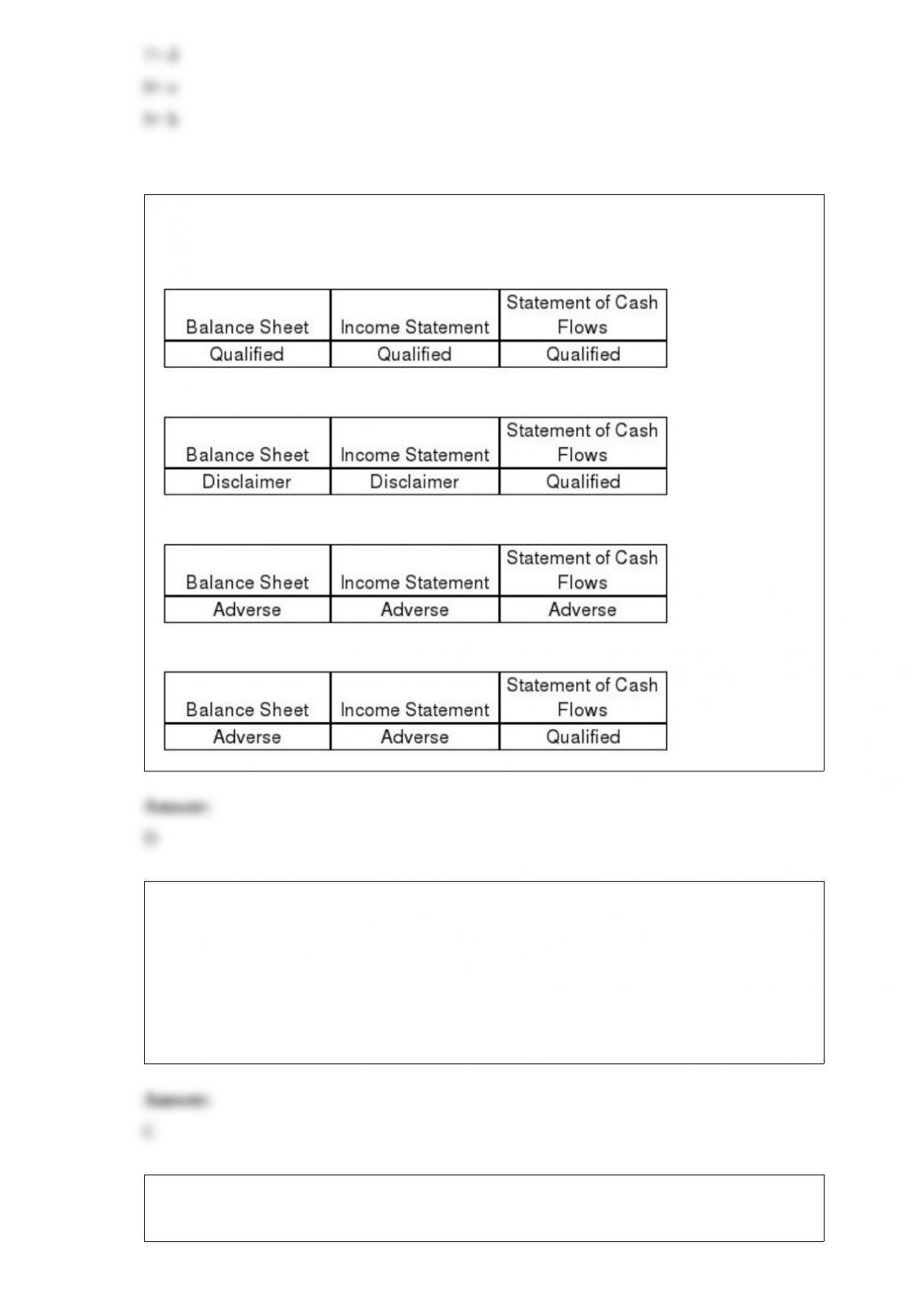

21) What type of audit opinion does the independent auditor issue when the following

financial statements are not presented?

A)

B)

C)

D)

22) A company is concerned with the theft of cash after the sale has been recorded. One

way in which fraudsters conceal the theft is by a process called “lapping”. Which of the

following best describes lapping?

A) reduce the customer’s account by recording a sales return

B) write off the customer’s account

C) apply the payment from another customer to the customer’s account

D) reduce the customer’s account by recording a sales allowance

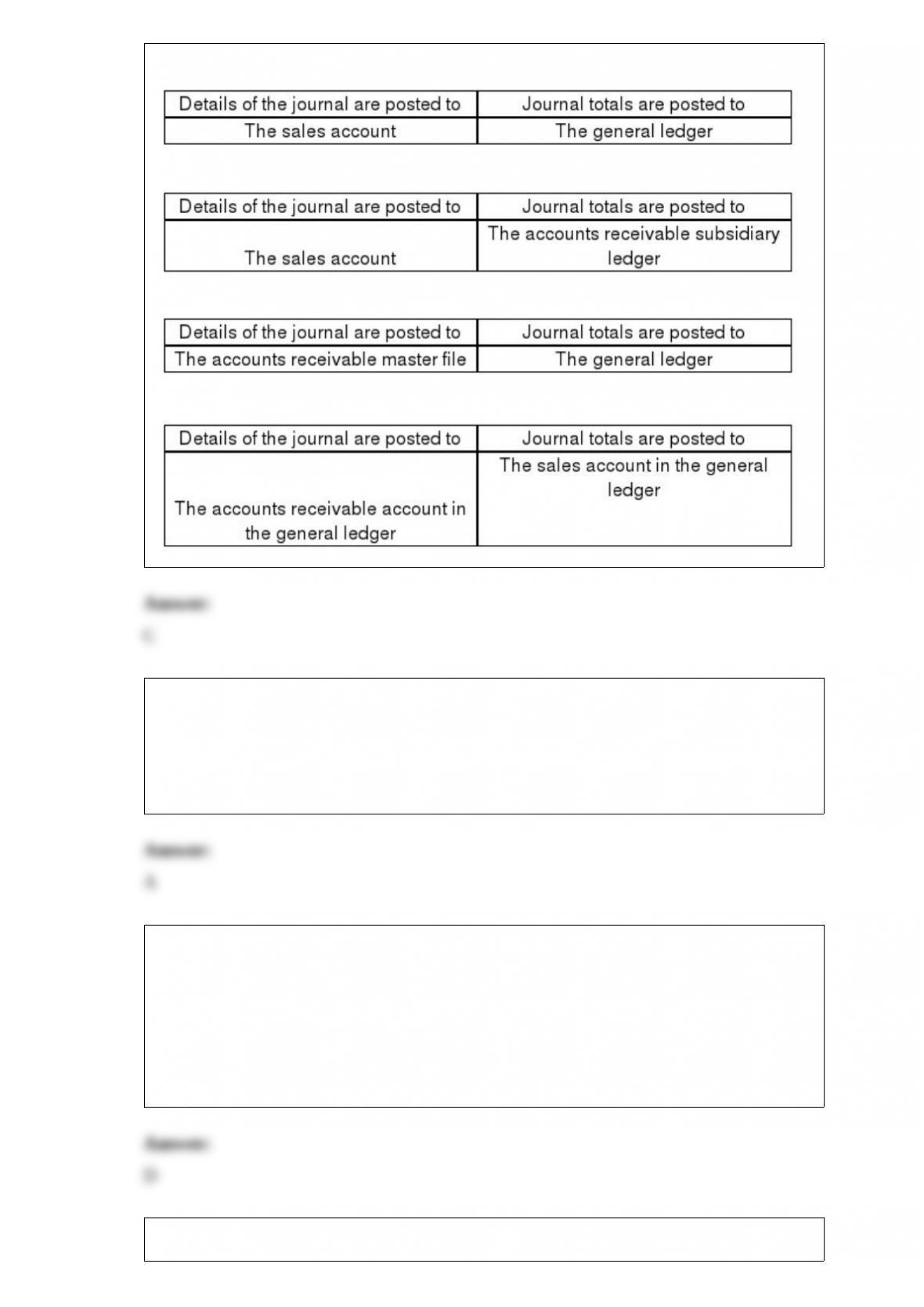

23) When posting items from the sales journal, details of the journal and journal totals

are posted to which items?

A)

B)

C)

D)

24) Auditing standards recognize that in instances where a significant amount of audit

evidence is in electronic form, it may not be possible to reduce detection risk to an

acceptable level by performing only substantive tests.

A) True

B) False

25) As a part of the auditor’s responsibility for ________, the auditor should review the

preparation of at least one of each type of payroll tax form the client is responsible for

filing.

A) doing tests of controls

B) doing tests of balances

C) doing tests of transactions

D) understanding the client’s internal controls

26) Which of the following services are allowed by the SEC whenever a CPA also

audits the company?

A) Internal audit outsourcing

B) Legal services unrelated to the audit

C) Appraisal or valuation services

D) Services related to assessing the effectiveness of internal control over financial

reporting

27) The Foreign Corrupt Practices Act of 1977 allows an injured party to seek treble

(triple) damages and recovery of legal fees in cases where it can be demonstrated that

the defendant was engaged in a pattern of fraudulent activity.

A) True

B) False

28) To help them remain independent of the operations they audit, internal auditors

should report directly to the controller.

A) True

B) False

29) At what point do most companies recognize liabilities in the acquisition and

payment cycle when the goods are shipped FOB Destination?

A) the issuance of a purchase order

B) receipt of acknowledgement of order by vendor

C) receipt of goods or services

D) the receipt of a vendor invoice