1) Adjusting entries are made after the preparation of financial statements.

2) The management concept of customer orientation causes a company to spend large

amounts on advertising to convince customers to buy the company’s standard products.

3) After posting the entries to close all revenue accounts and all expense accounts, the

Income Summary account of Waif Services has a $4,000 debit balance. This result

implies that Waif Services earned a net income of $4,000.

4) Owners of coupon bonds are not required to pay tax on the interest earned.

5) The heading on each financial statement lists the three W’s – Who (the name of the

organization), What (the name of the statement), and Where (the organization’s

address).

6) Unit costs can be significantly different when using activity-based costing compared

to traditional cost allocation methods.

7) The present value of an annuity table can be used to determine the series of equal

payments that are required by a loan agreement.

8) Overapplied or underapplied overhead should be removed from the Factory

Overhead account at the end of each accounting period.

9) Raw materials inventory includes only direct materials.

10) In the absence of a partnership agreement, the law says that income of a partnership

will be shared equally by the partners.

11) The effective interest method yields increasing amounts of bond interest expense

and decreasing amounts of premium amortization over the bond’s life for bonds issued

at a premium.

12) A corporation issued 6,000 shares of its $10 par value common stock in exchange

for land that has a market value of $84,000. The entry to record this transaction would

include:

A.A debit to Common Stock for $60,000

B.A debit to Land for $60,000

C.A credit to Land for $60,000

D.A credit to Paid-in Capital in Excess of Par Value, Common Stock for $24,000

E.A credit to Common Stock for $84,000

13) Stride Along has total assets of $385 million. Its total liabilities are $100 million

and its equity is $285 million. Calculate its debt ratio.

A.35.1%

B.26.0%

C.38.5%

D.28.5%

E.58.8%

14)

Identify the accounting information system principle below that applies to each of these

situations.

1>Cost-benefit A. Global Company has designed their accounting information system

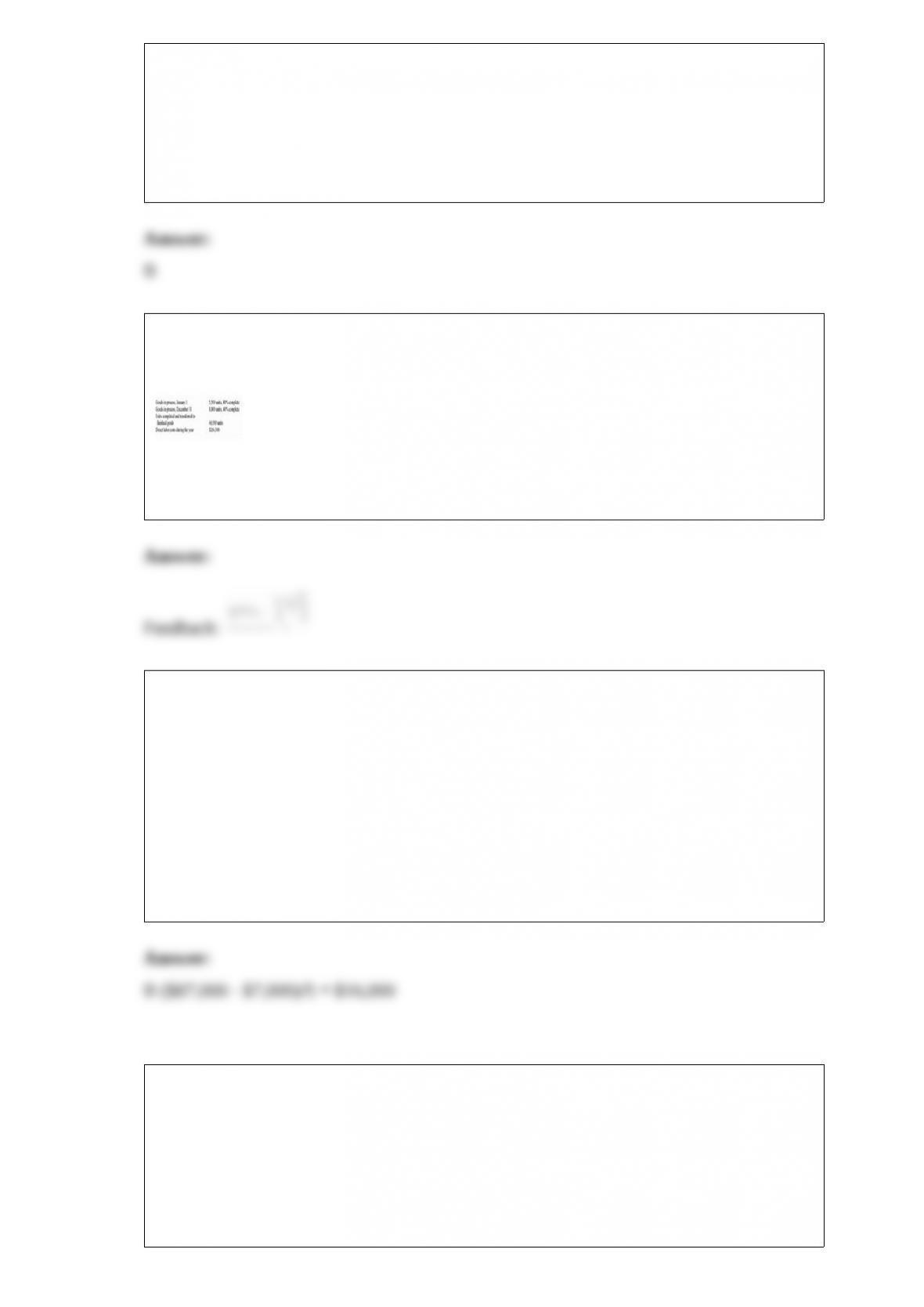

to be adaptable to changes in technology, the business environment, and the needs of

decision makers.

2>Control B. Global Company has world-wide operations that must handle several

thousand different products, so the accounting information system is fairly complex,

encompassing marketing and manufacturing.

3>Flexibility C. Global Company’s accounting information system has policies to

ensure that financial statements will be reliable, assets are protected, and relevant laws

and regulations are complied with.

4>Compatibility D. Global Company’s accounting information system can be improved

markedly for a cost of about $30,000,000. E. However, the incremental benefits from

such improvements are not expected to outweigh this cost.

5>Relevance F. Global Company has designed their accounting information system so

that key managers can obtain the information they need to make decisions relating to

new products, sales, and controlling costs.

15) Match the following terms with the appropriate definitions.

1>Consolidated financial statements A. Investments in equity and debt securities that

are not readily convertible to cash or are not intended to be converted to cash in the

short term.

2>Subsidiary B. A corporation controlled by another company when the parent owns

more than 50% of the subsidiary’s voting stock.

3>Equity method C. Change in market value that is not yet realized through an actual

sale.

4>Available-for-sale securities D. Financial statements that show the financial position,

results of operations, and cash flows of all entities under the parent’s control, including

those of any subsidiaries.

5>Unrealized gain (loss) E. A company that owns a more than 50% controlling interest

in a subsidiary.

6>Parent company F. Debt and equity securities not classified as trading or

held-to-maturity.

7>Trading securities G. Debt securities that a company intends and is able to hold until

maturity.

8>Held-to-maturity securities H. Debt and equity securities that a company intends to

actively manage and trade for profit.

9>Long-term investments I. A measure of operating efficiency, computed as net income

divided by average total assets.

10>Return on total assets J. An accounting method for long-term investments in equity

when the investor has significant influence over the investee.

16) Cash equivalents:

A.Are readily convertible to a known cash amount

B.Include short-term investments purchased within 3 months of their maturity dates

C.Have a market value that is not sensitive to interest rate changes

D.Include short-term U.S. treasury bills

E.All of these

17) The following data are available for a company’s manufacturing activities:

If materials are added when the production process begins and direct labor is applied

uniformly throughout the process, what are the equivalent units for direct materials and

for direct labor, respectively using the FIFO method of process costing?

A.16,250; 19,250

B.16,250; 21,750

C.21,000; 19,250

D.19,250; 18,750

E.21,000; 22,250

18) Which interest rate column would you use from a present value table or a future

value table for 8% compounded quarterly?

A.12%

B.6%

C.3%

D.2%

E.1%

19) An accounts receivable ledger is:

A.A subsidiary ledger that contains an account for each credit customer

B.A list of the balances of selected accounts in the accounts receivable ledger that is

added to show the total amount of the significant accounts receivable outstanding

C.A book of original entry that is designed and used for recording only a specified type

of transaction

D.The ledger that contains the financial statement accounts of a business

E.A subsidiary ledger that contains a separate account for each creditor (supplier) to the

company

20) At the current year-end, Hardly Company found that its overhead was underapplied

by $2,500, and this amount was not deemed to be a material amount. Based on this

information, Hardly should

A.Close the $2,500 to Cost of Goods Sold

B.Close the $2,500 to Finished Goods Inventory

C.Do nothing about the $2,500, since it is not material, and it is likely that overhead

will be overapplied by the same amount next year

D.Carry the $2,500 to the income statement as “Other Expense”

E.Carry the $2,500 to the next period

21) Plans that identify costs and expenses under each manager’s control prior to the

reporting period are called:

A.Cost accounting systems

B.Managerial accounting systems

C.Responsibility accounting systems

D.Responsibility accounting budgets

E.Activity-based accounting systems

22) An account used to record the owner’s investments in the business is called a(n):

A.Withdrawals account

B.Capital account

C.Revenue account

D.Expense account

E.Liability account

23) Grafton is preparing a cash budget for June. The company has $25,000 cash at the

beginning of June and anticipates $95,000 in cash receipts and $111,290 in cash

disbursements during June. Compute the amount the company must borrow, if any, to

maintain a $20,000 cash balance. The company has no loans outstanding on June 1.

A.$28,710

B.$12,290

C.$16,290

D.$11,290

E.$6,290

24) A company factored $45,000 of its accounts receivable and was charged a 3%

factoring fee. The journal entry to record this transaction would include a:

A.Debit to Cash of $45,000, a debit to Factoring Fee Expense of $1,350, and credit to

Accounts Receivable of $43,650

B.Debit to Cash of $45,000 and a credit to Accounts Receivable of $45,000

C.Debit to Cash of $43,650, a debit to Factoring Fee Expense of $1,350, and a credit to

Accounts Receivable of $45,000

D.Debit to Cash of $46,350 and a credit to Accounts Receivable of $46,350

E.Debit to Cash of $45,000 and a credit to Notes Payable of $45,000

25) Current assets minus current liabilities is:

A.Profit margin

B.Financial leverage

C.Current ratio

D.Working capital

E.Quick assets

26) The account receivable turnover measures:

A.How long it takes to sell accounts receivable to a factor

B.How often, on average, receivables are received and collected during the period

C.The relation of cash sales to credit sales

D.How long it takes to sell merchandise inventory

E.All of these

27) A plan that shows the expected cash inflows and cash outflows during the budget

period, including receipts from loans needed to maintain a minimum cash balance and

repayments of such loans, is called a(n):

A.Capital expenditures budget

B.Operating budget

C.Rolling budget

D.Cash budget

E.Income statement

28) When recording variances in a standard cost system:

A.Only unfavorable material variances are debited

B.Only unfavorable material variances are credited

C.Both unfavorable material and labor variances are credited

D.All unfavorable variances are debited

E.All unfavorable variances are credited

29) Information to prepare the statement of cash flows usually comes from (a)

comparative balance sheets, (b) current income statement, and (c) additional

information.

30) When raw materials are purchased on account for use in a process costing system,

the corresponding journal entry that should be recorded will include:

A.A debit to Goods in Process Inventory

B.A debit to Accounts Payable

C.A credit to Cash

D.A debit to Raw Materials Inventory

E.A credit to Raw Materials Inventory

31) The modified accelerated cost recovery system (MACRS):

A.Is included in the U.S. federal income tax rules for depreciating assets

B.Is an out-dated system that is no longer used by companies

C.Is required for financial reporting

D.Is identical to units of production depreciation

E.All of these

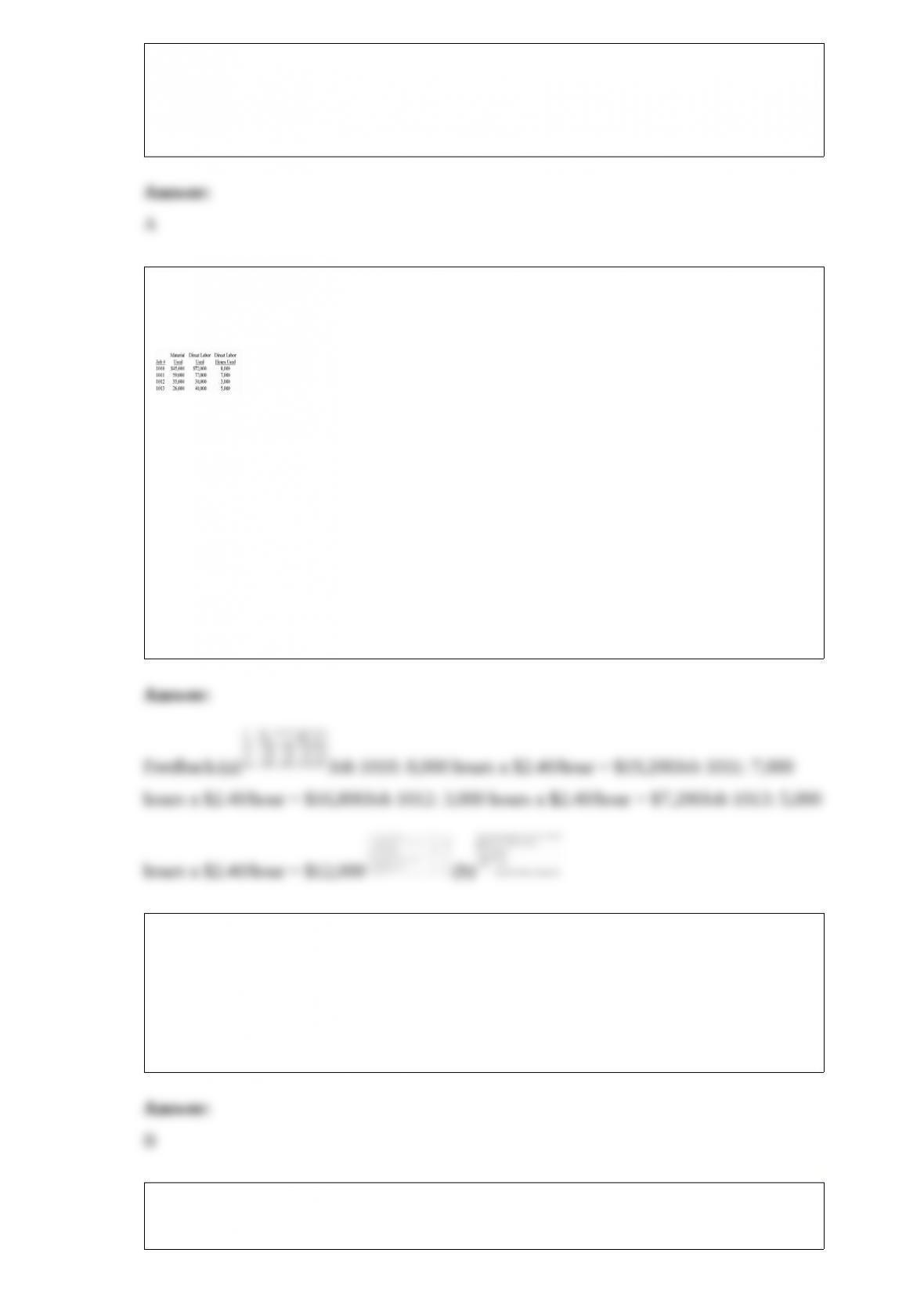

32) Dina Corp. uses a job order cost accounting system. Four jobs were started during

the current year. The following is a record of the costs incurred:

Actual overhead costs were $55,800. The predetermined overhead allocation rate is

$2.40 per direct labor hour. During the year, Jobs 1010, 1012, and 1013 were

completed. Also, Jobs 1010 and 1013 were sold for $387,000. Assuming that this is

Dina’s first year of operations:

(a) Make the necessary journal entries to charge the costs to the jobs started and to

record the completion and sale of finished jobs.

(b) Calculate the balance in the Goods in Process Inventory, Finished Goods Inventory,

and Factory Overhead accounts. Does the Factory Overhead account balance indicate

an over- or under applied overhead?

33) If the times interest ratio:

A.Increases, then risk increases

B.Increases, then risk decreases

C.Is greater than 1.5, then the company is in default

D.Is less than 1.5, the company is carrying too little debt

E.Is greater than 3.0, the company is likely carrying too much debt

34) A company reported that its bonds with a par value of $50,000 and a carrying value

of $57,000 are retired for $60,000 cash, resulting in a loss of $3,000. The amount to be

reported under cash flows from financing activities is:

A.$(3,000)

B.$(60,000)

C.$(57,000)

D.Zero. This is an operating activity

E.Zero. This is an investing activity

35) A company uses a process cost accounting system and the weighted average method

for inventory costs. The following information is available regarding direct labor for the

current year:

(a) Calculate the equivalent units of production for direct labor for the year.

(b) Calculate the average cost per equivalent unit for direct labor (round to the nearest

cent).

36) Salta Company installs a manufacturing machine in its factory at the beginning of

the year at a cost of $87,000. The machine’s useful life is estimated to be 5 years, or

400,000 units of product, with a $7,000 salvage value. During its second year, the

machine produces 84,500 units of product. Determine the machines’ second year

depreciation under the straight-line method.

A.$16,900

B.$16,000

C.$17,400

D.$18,379

E.$20,880

37) Adjusting entries made at the end of an accounting period accomplish all of the

following except:

A.Updating liability and asset accounts to their proper balances

B.Assigning revenues to the periods in which they are earned

C.Assigning expenses to the periods in which they are incurred

D.Assuring that financial statements reflect the revenues earned and the expenses

incurred

E.Assuring that external transaction amounts remain unchanged

38) All of the following statements regarding inventory shrinkage are true except:

A.Inventory shrinkage refers to the loss of inventory.

B.Inventory shrinkage is determined by comparing a physical count of inventory with

recorded inventory amounts.

C.Inventory shrinkage is recognized by debiting an operating expense.

D.Inventory shrinkage is recognized by debiting Cost of Goods Sold.

E.Inventory shrinkage can be caused by theft or deterioration.

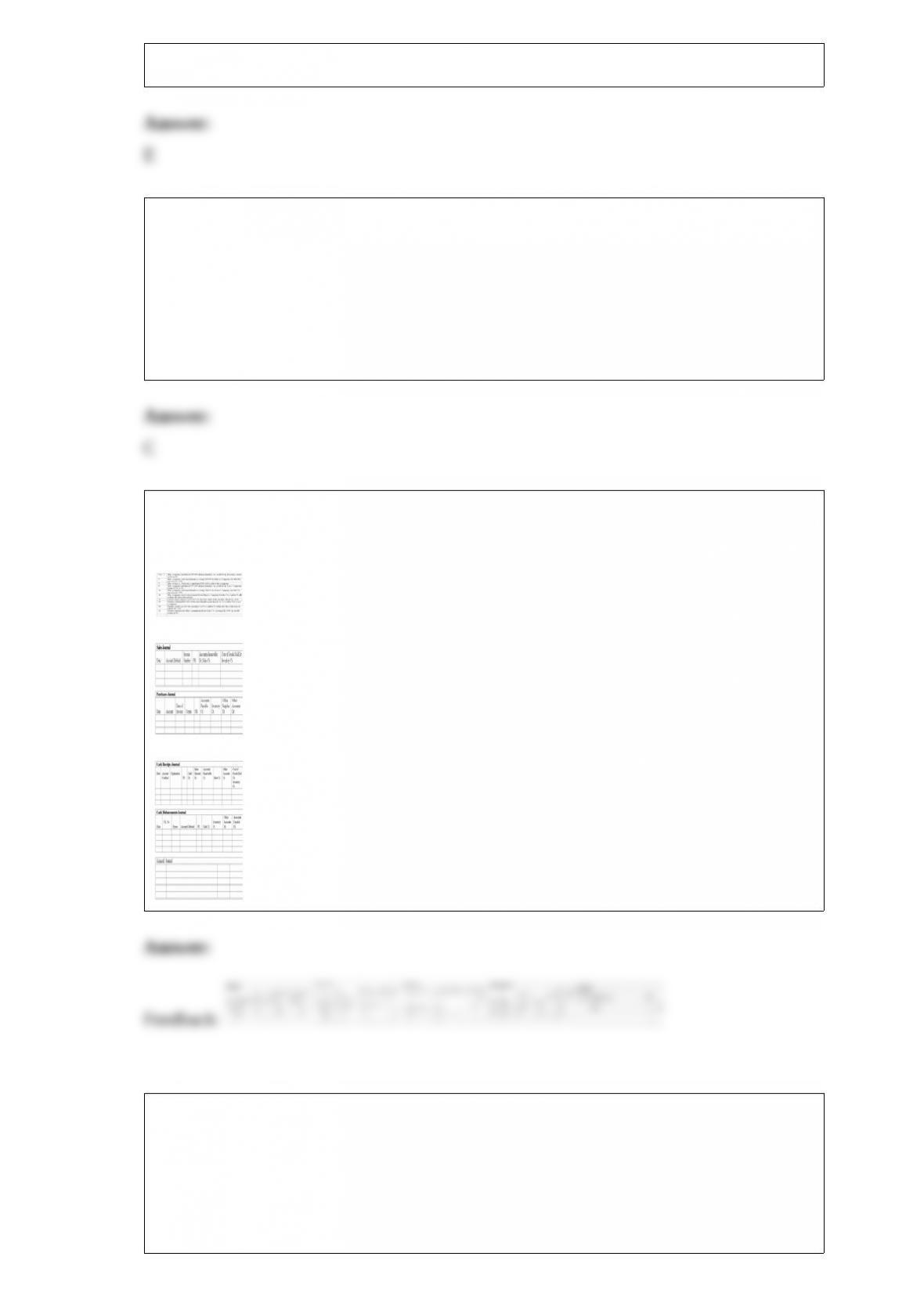

39) Medco Company uses special journals to record transactions. Medco uses the

perpetual inventory system. Journalize the following transactions in the appropriate

special journal. All credit sales have 2/10, n/30 terms.

40) A liability created by the receipt of cash from customers in payment for products or

services that have not yet been delivered to the customers is:

A.Recorded as a debit to an unearned revenue account

B.Recorded as a debit to a prepaid expense account

C.Recorded as a credit to an unearned revenue account

D.Recorded as a credit to a prepaid expense account

E.Not recorded in the accounting records until the earnings process is complete

41) Aniston Enterprises manufactures stylish hats for sophisticated women. All

materials are introduced at the beginning of the manufacturing process in the Cutting

Department. Conversion costs are incurred uniformly throughout the manufacturing

process. As the cutting of material is completed, the pieces are immediately transferred

to the Sewing Department. Information for the Cutting Department for the month of

May follows.

Goods in Process, May 1 (50,000 units, 100% complete for direct materials, 40%

complete with respect to direct labor and overhead; includes $70,500 of direct material

cost; $34,050 of conversion costs).

Goods in Process, May 31 (75,000 units, 100% complete for direct materials; 20%

complete for conversion costs).

If Aniston Enterprises uses the FIFO method of process costing, compute the equivalent

units for materials and conversion costs respectively for May.

A.225,000; 225,000

B.200,000; 195,000

C.275,000; 200,000

D.225,000; 195,000

E.200,000; 200,000

42) Financial budgets include all the following except the:

A.Sales budget

B.Budgeted balance sheet

C.Budgeted income statement

D.Cash budget

E.All of these are financial budgets

43) For which item does a bank NOT issue a debit memorandum?

A.To notify a depositor of all withdrawals through an ATM

B.To notify a depositor of a fee assessed to the depositor’s account

C.To notify a depositor of an uncollectible check

D.To notify a depositor of periodic payments arranged in advance, by a depositor

E.To notify a depositor of a deposit to their account

44) The times interest earned computation is:

A.(Net income + Interest expense + Income taxes)/Interest expense

B.(Net income + Interest expense – Income taxes)/Interest expense

C.(Net income – Interest expense – Income taxes)/Interest expense

D.(Net income – Interest expense + Income taxes)/Interest expense

E.Interest expense/(Net income + Interest expense + Income taxes expense)

45) The process of restating future cash flows in today’s dollars is known as:

A.Budgeting

B.Annualization

C.Discounting

D.Payback period

E.Capitalizing

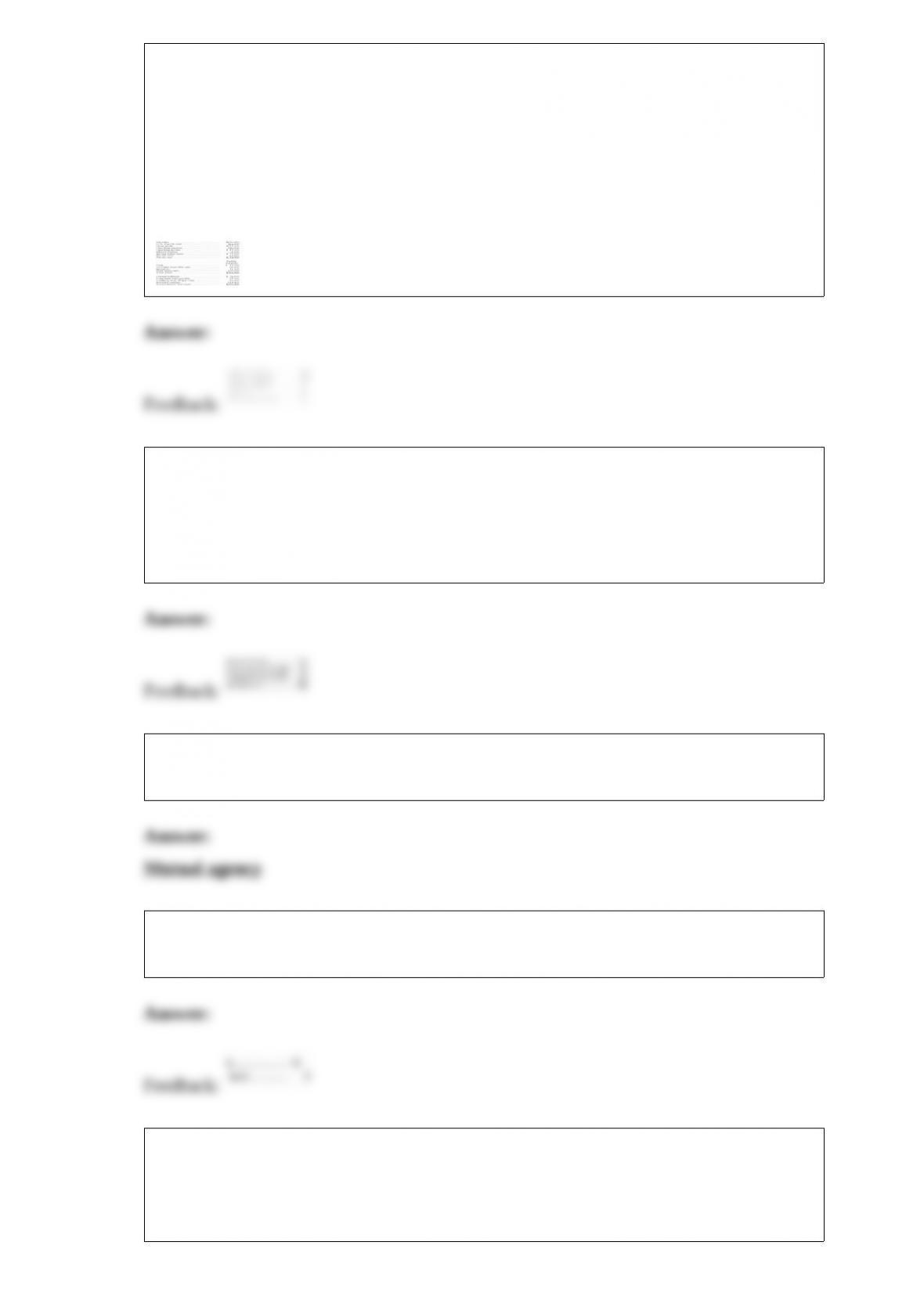

46) A company’s calendar-year financial data are shown below. The company had total

assets of $339,000 and total equity of $144,400 for the prior year. No additional shares

of common stock were issued during the year. The December 31 market price per share

is $49.50. Cash dividends of $19,500 were paid during the year. Calculate the following

ratios for the company:

(a) debt ratio

(b) equity ratio

(c) debt-to-equity ratio

(d) times interest earned

(e) total asset turnover

47) The Lamb Company budgeted sales for January, February, and March of $96,000,

$88,000, and $72,000, respectively. Seventy percent of sales are on credit. The

company collects 60% of its credit sales in the month following sale, 35% in the second

month following sale, and 5% is not collected. What are Lamb’s expected cash receipts

for March related to all current and past sales?

48) ___________________________ means that partners can commit or bind the

partnership to any contract within the scope of the partnership business.

49) Marquis and Bose agree to accept Sherman into their partnership. Sherman will

contribute $25,000 in cash. Prepare the journal entry to record this transaction.

50) A company paid $500,000 for 12% bonds with a par value of $500,000. The bonds

pay 6% interest semiannually on September 1 and March 1. The company intends to

hold the bonds until they mature. Prepare the journal entries for the following dates and

transactions related to this bond acquisition.

(1)Bonds purchased on September 1

(2) Year-end adjusting entry, December 31

(3) Receipt of semiannual interest March 1

(4) Redemption of the bonds at maturity on August 31

51) The job cost sheet for Job number 93-471 includes the following information:

DIRECT MATERIALS:

7/12 Requisition R93-566: 20 units @ $3.50 per unit

7/13 Requisition R93-576: 18 units @ $5.00 per unit

7/13 Requisition R93-578: 4 units @ $25.00 per unit

7/14 Requisition R93-591: 40 units @ $1.25 per unit

DIRECT LABOR:

7/12 Employee 19: 8 hours @ $9.00 per hour

7/13 Employee 19: 6 hours @ $9.00 per hour

7/13 Employee 37: 6 hours @ $7.00 per hour

7/14 Employee 19: 5 hours @ $9.00 per hour

7/14 Employee 92: 5 hours @ $11.00 per hour

FACTORY OVERHEAD:

Assigned at 150% of direct labor cost.

What is the total cost of Job number 93-471?

52) Prepare a December 31 balance sheet in proper form for Surety Insurance using the

following accounts and amounts:

53) ____________________ is the accounting system component that keeps data in a

form accessible to information processors.

54) Explain how to record the issuance and sale of a bond between interest payment

dates.

55) Madera Iron Sculpting is planning on replacing one of its robotic welders in five

years by making a one-time deposit of $20,000 today and four yearly contributions of

$5,000 beginning at the end of year 1. The deposits will earn 10% interest. How much

money will Sierra have accumulated at the end of five years to replace the welder?

56) What are the general accounting procedures for recording asset disposals?