1) Under IFRS, a deferred tax liability is classified as current or noncurrent based on

the classification of the asset or liability to which it relates.

2) A benefit of leasing to the lessor is the return of the leased property at the end of the

lease term.

3) In computing diluted earnings per share, stock options are considered dilutive when

their option price is greater than the market price.

4) When a buyer enters into a formal, noncancelable purchase contract, an asset and a

liability are recorded at the inception of the contract.

5) Land held for speculation is reported in the property, plant, and equipment section of

the balance sheet.

6) Companies have the option of disclosing information about the nature of their

operations and the use of estimates in preparing financial statements.

7) Depreciation is a means of cost allocation, not a matter of valuation.

8) IFRS permits an entity to reverse inventory write-downs in certain situations,

whereas U.S. GAAP does not.

9) A flood damaged a building and contents. Floods are unusual and infrequent in this

area. The receipts from insurance companies totaled $500,000, which was $150,000

less than the book values. The tax rate is 30%.

On the statement of cash flows (indirect method), the receipts from insurance

companies should

a.be shown as an addition to net income of $350,000

b.be shown as an inflow from investing activities of $350,000

c.be shown as an inflow from investing activities of $500,000

d.not be shown

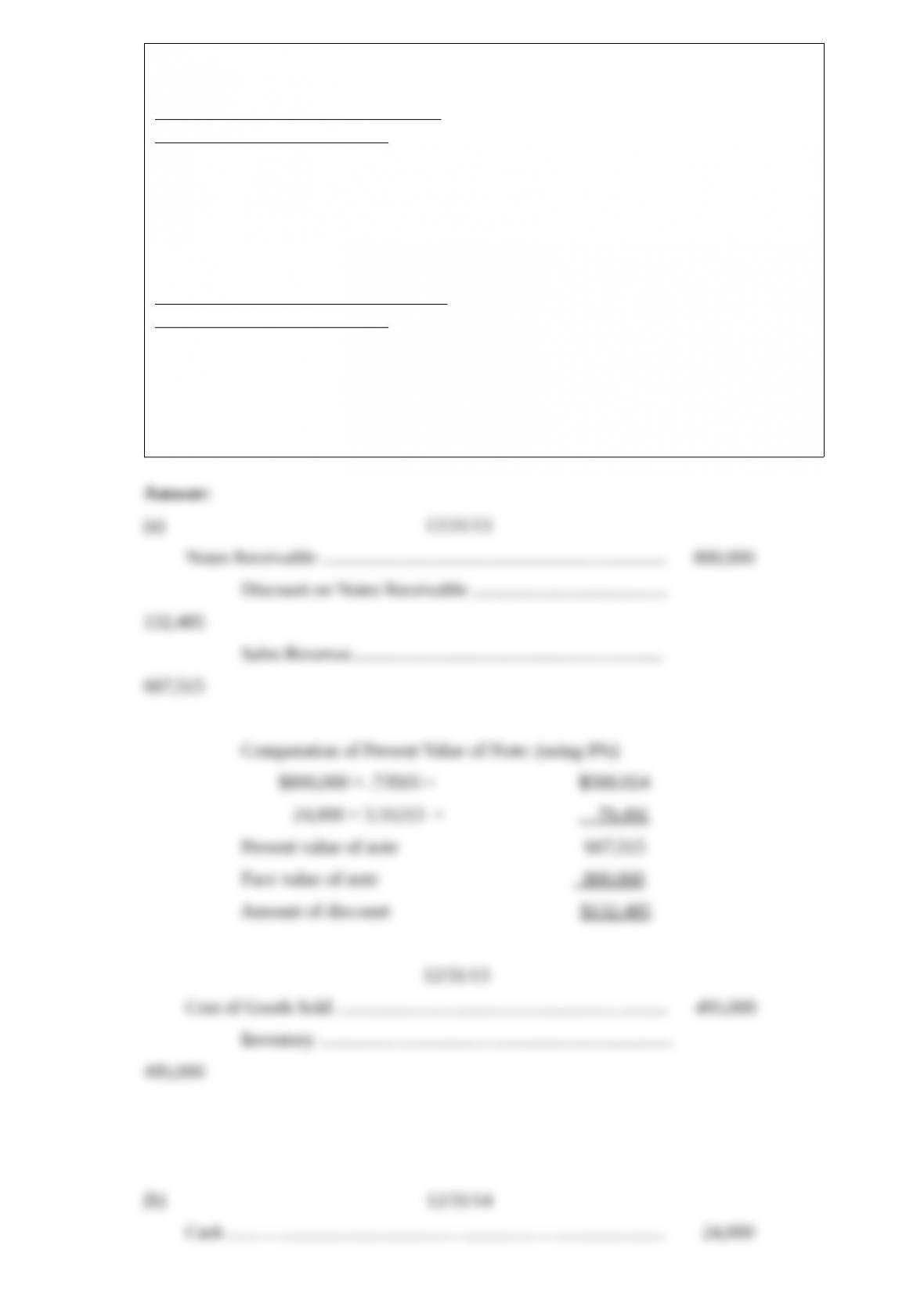

10) On December 31, 2013 Berry Corporation sold some of its product to Flynn

Company, accepting a 3%, four-year promissory note having a maturity value of

$800,000 (interest payable annually on December 31). Berry Corporation pays 6% for

its borrowed funds. Flynn Company, however, pays 8% for its borrowed funds. The

product sold is carried on the books of Berry at a manufactured cost of $495,000.

Assume Berry uses a perpetual inventory system.

Instructions

(a)Prepare the journal entries to record the transaction on the books of Berry

Corporation at December 31, 2013 . (Assume that the effective interest method is used.

Use the interest tables below and round to the nearest dollar.)

(b)Make all appropriate entries for 2014 on the books of Berry Corporation.

(c)Make all appropriate entries for 2015 on the books of Berry Corporation.

Table 1

Future Value of 1

Periods2%3%4%6%8%

11.020001.030001.040001.060001.08000

21.040401.060901.081601.123601.16640

31.061211.092731.124861.191021.25971

41.082431.125511.169861.262481.36049

51.104081.159271.216651.338231.46933

Table 2

Present Value of 1

Periods2%3%4%6%8%

10.980390.970870.961540.943400.92593

20.961170.942600.924560.890000.85734

30.942320.915140.889000.839620.79383

40.923850.888490.854800.792090.73503

50.905730.862610.821930.747260.68058

Table 3

Future Value of Ordinary Annuity of 1

Periodic Rents2%3%4%6%8%

11.000001.000001.000001.000001.00000

22.020002.030002.040002.060002.08000

33.060403.090903.121603.183603.24640

44.121614.183634.246464.374624.50611

55.204045.309145.416325.637095.86660

Table 4

Present Value of Ordinary Annuity of 1

Periodic Rents2%3%4%6%8%

10.980390.970870.961540.943400.92593

21.941561.913471.886091.833391.78326

32.883882.828612.775092.673012.57710

43.807733.717103.629903.465113.31213

54.713464.579714.451824.212363.99271

11) According to a Financial Accounting Standards Board Statement, how are research

and development costs accounted for?

a.They must be capitalized when incurred and then amortized over their estimated

useful lives

b.They must be expensed in the period incurred

c.They may be either capitalized or expensed when incurred, depending upon the

materiality of the amounts involved

d.They must be expensed in the period incurred unless it can be clearly demonstrated

that the expenditure will have alternative future uses or unless contractually

reimbursable

12) Metro Company, a dealer in machinery and equipment, leased equipment to Sands,

Inc., on

July 1, 2015 . The lease is appropriately accounted for as a sales-type lease by Metro

and as a capital lease by Sands. The lease is for a 10-year period (the useful life of the

asset) expiring June 30, 2025 . The first of 10 equal annual payments of $552,000 was

made on July 1, 2015 . Metro had purchased the equipment for $3,500,000 on January

1, 2015, and established a list selling price of $4,800,000 on the equipment. Assume

that the present value at July 1, 2015, of the rent payments over the lease term

discounted at 8% (the appropriate interest rate) was $4,000,000.

What is the amount of profit on the sale and the amount of interest revenue that Metro

should record for the year ended December 31, 2015?

a.$0 and $137,920

b.$500,000 and $137,920

c.$500,000 and $160,000

d.$800,000 and $320,000

13) The assumption that a company will not be sold or liquidated in the near future is

known as the

a.economic entity assumption

b.monetary unit assumption

c.periodicity assumption

d.None of these answer choices are correct

14) The following information is available for Barkley Companys patents:

Cost$3,440,000

Carrying amount1,720,000

Expected future net cash flows1,600,000

Fair value1,300,000

Barkley would record a loss on impairment of

a.$ 120,000

b.$ 420,000

c.$1,720,000

d.$1,840,000

15) On January 1, 2015, Parks Co. has the following balances:

Projected benefit obligation$4,200,000

Fair value of plan assets3,750,000

The settlement rate is 10%. Other data related to the pension plan for 2015 are:

Service cost$240,000

Amortization of prior service costs54,000

Contributions270,000

Benefits paid250,000

Actual return on plan assets264,000

Amortization of net gain18,000

The fair value of plan assets at December 31, 2015 is

a.$3,506,000

b.$3,764,000

c.$4,034,000

d.$4,284,000

16) Present Value ofFuture Value of

Ordinary AnnuityOrdinary Annuity

7 periods5.20648.92280

8 periods5.746610.63663

9 periods6.246912.48756

(8% interest)

Korman Company wishes to accumulate $500,000 by May 1, 2022 by making 8 equal

annual deposits beginning May 1, 2014 to a fund paying 8% interest compounded

annually. What is the required amount of each deposit?

a.$87,008

b.$47,008

c.$43,525

d.$50,390

17) The accounting exchanges of nonmonetary assets has recently converged between

IFRS and U.S. GAAP, per SFAS No. 153, now requires

a.that gains on exchanges of nonmonetary assets be recognized if the exchange has

commercial substance

b.that gains on exchanges of nonmonetary assets be recognized if the exchange does not

have commercial substance

c.that gains on exchanges of nonmonetary assets be recognized if the exchange does not

have commercial substance, and has never been impaired

d.All of the above

18) Lease A does not contain a bargain purchase option, but the lease term is equal to 90

percent of the estimated economic life of the leased property. Lease B does not transfer

ownership of the property to the lessee by the end of the lease term, but the lease term is

equal to 75 percent of the estimated economic life of the leased property. How should

the lessee classify these leases?

Lease A Lease B

a.Operating leaseCapital lease

b.Operating leaseOperating lease

c.Capital leaseCapital lease

d.Capital leaseOperating lease

19) On August 31, Latty Co. partially refunded $450,000 of its outstanding 10% note

payable made one year ago to Dugan State Bank by paying $450,000 plus $45,000

interest, having obtained the $495,000 by using $131,000 cash and signing a new

one-year $400,000 note discounted at 9% by the bank.

Instructions

(1)Make the entry to record the partial refunding. Assume Latty Co. makes reversing

entries when appropriate.

(2)Prepare the adjusting entry at December 31, assuming straight-line amortization of

the discount.

20) Determine the proper unit inventory price in the following independent cases by

applying the lower of cost or market rule. Circle your choice.

1 2 3 4 5

Cost$8.00$10.50$12.00$6.00$7.20

Net realizable value8.8510.0012.204.256.90

Net realizable value less normal profit8.159.0011.403.756.00

Market replacement cost7.9010.1012.504.005.40

21) With regard to recognition of deferred tax assets, IFRS requires

22) Define temporary differences, future taxable amounts, and future deductible

amounts.

23) Hurst, Incorporated sold its 8% bonds with a maturity value of $6,000,000 on

August 1, 2013 for $5,892,000. At the time of the sale the bonds had 5 years until they

reached maturity. Interest on the bonds is payable semiannually on August 1 and

February 1 . The bonds are callable at 104 at any time after August 1, 2015 . By

October 1, 2015, the market rate of interest has declined and the market price of Hurst’s

bonds has risen to a price of 101 . The firm decides to refund the bonds by selling a new

6% bond issue to mature in 5 years. Hurst begins to reacquire its 8% bonds in the

market and is able to purchase $1,000,000 worth at 101 . The remainder of the

outstanding bonds is reacquired by exercising the bonds’ call feature. In the final

analysis, how much was the gain or loss experienced by Hurst in reacquiring its 8%

bonds? (Assume the firm used straight-line amortization.) Show calculations.

24) Briefly describe some of the similarities and differences between U.S. GAAP and

IFRS with respect to income tax accounting.