All changes in estimate are accounted for retrospectively.

If the estimate of a transaction price is revised, the price change is allocated entirely to

the remaining performance obligations that are yet to be satisfied.

Earnings quality refers to the ability of reported earnings (income) to predict future

earnings.

Net purchases are reduced for discounts taken whether the net method is used or the

gross method is used.

GAAP requires using intrinsic value accounting for employee stock options.

The funding of the standard-setting bodies that promulgate IFRS is as independent as

that underlying U.S. GAAP.

Sellers should recognize revenue over time for a long term contract in which the seller

is receiving periodic payments for progress to date but may need to refund those

payments in the event the contract is cancelled.

Gains or losses result, respectively, from the disposition of business assets for greater

than, or less than, their book values.

Accrued salaries and wages in a balance sheet represent salaries and wages that have

been earned by employees but not yet paid.

Hans Cars & Trucks sells various types of used vehicles with a one-year warranty that

covers any defects. When customers make a purchase, they also receive a coupon for 10

free engine oil changes and an option to change all of the tires for $50 after 30,000

miles. Typically, customers pay $25 for an oil change and $250 for a new set of tires.

Required:

(a) Given the information above, how many performance obligations exist in the

contract to purchase a vehicle?

(b) Assume the same contract but that it offers customers an option to change all of the

tires for $250 after 30,000 miles. How many performance obligations exist in the

contract to purchase a vehicle?

A statement of comprehensive income does not include:

a. Net income.

b. Losses from the return on assets exceeding expectations.

c. Losses from changes in estimates regarding the PBO.

d. Prior service cost.

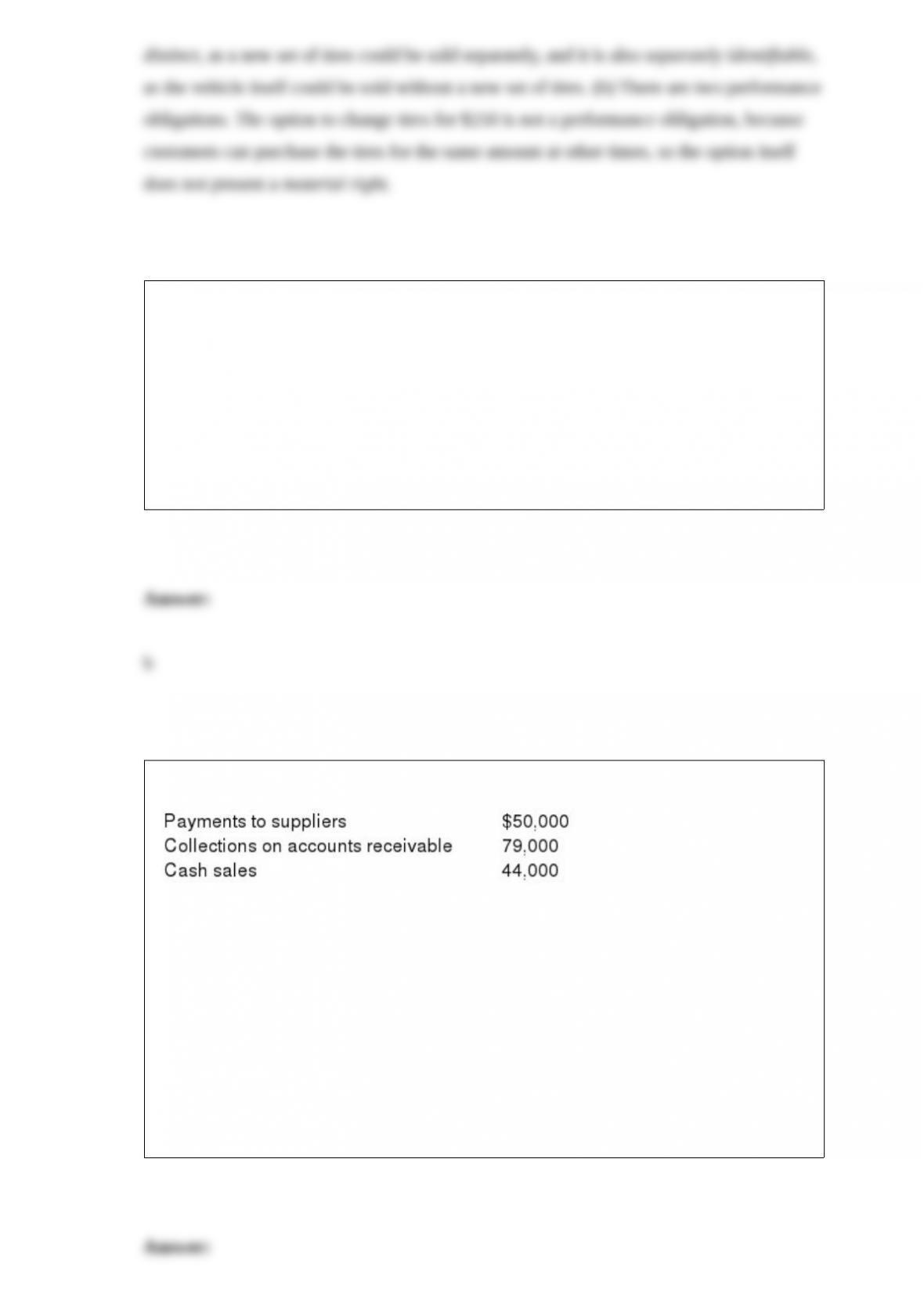

Lite Travel Company’s accounting records include the following information:

What is the amount of net cash provided by operating activities indicated by the

amounts provided?

a. $ 50,000.

b. $ 73,000.

c. $ 94,000.

d. $129,000.

Alamo Inc. had $300 million in taxable income for the current year. Alamo also had a

decrease in deferred tax assets of $30 million and an increase in deferred tax liabilities

of $60 million. The company is subject to a tax rate of 40%. The total income tax

expense for the year was:

a. $390 million.

b. $210 million.

c. $150 million.

d. $180 million.

For 2015, P Co. estimated its two-year equipment warranty costs based on $23 per unit

sold in 2015. Experience during 2016 indicated that the estimate should have been

based on $25 per unit. The effect of this $2 difference from the estimate is reported:

a. In 2016 income from continuing operations.

b. As an accounting change, net of tax, below 2016 income from continuing operations.

c. As an accounting change requiring 2015 financial statements to be restated.

d. As a correction of an error requiring 2015 financial statements to be restated.

Bond X and bond Y both are issued by the same company. Each of the bonds has a

maturity value of $100,000 and each matures in 10 years. Bond X pays 8% interest

while bond Y pays 9% interest. The current market rate of interest is 8%. Which of the

following is correct?

a. Both bonds sell for the same amount.

b. Bond X sells for more than bond Y.

c. Bond Y sells for more than bond X.

d. Both bonds sell at a discount.

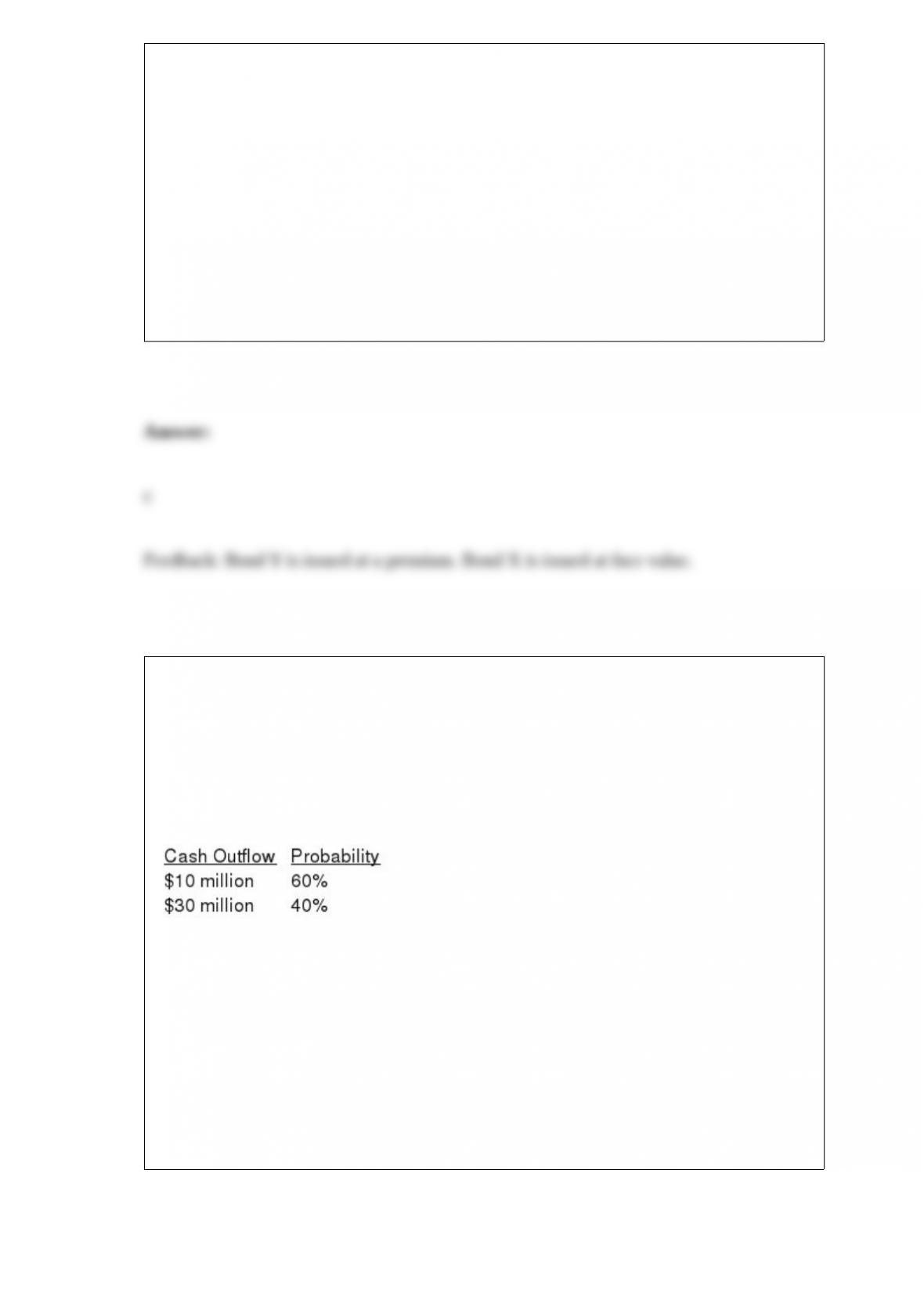

Montana Mining Co. (MMC) paid $200 million for the right to explore and extract rare

metals from land owned by the state of Montana. To obtain the rights, MMC agreed to

restore the land to a suitable condition for other uses after its exploration and extraction

activities. MMC incurred exploration and development costs of $60 million on the

project. MMC has a credit-adjusted risk free interest rate is 7%. It estimates the possible

cash flows for restoring the land, three years after its extraction activities begin, as

follows:

The asset retirement obligation (rounded) that should be recognized by MMC at the

beginning of the extraction activities is:

a. $ 8.2 million.

b. $14.7 million.

c. $ 18 million.

d. $ 30 million.

The possibility that the capital markets’ focus on periodic profits may tempt a

company’s management to bend or even break accounting rules to inflate reported net

income is an example of:

a. An ethical dilemma.

b. An accounting theory issue.

c. A technical accounting issue.

d. An auditor”s responsibility to inform the SEC.

You borrow $20,000 to buy a boat. The loan is to be paid off in monthly installments

over one year at 18% interest annually. The first payment is due one month from today.

What is the amount of each monthly payment?

a. $1,667.

b. $1,511.

c. $1,834.

d. None of the above.

Peterson Photoshop sold $1,000 in gift cards on a special promotion on October 15,

2016, and sold $1,500 in gift cards on another special promotion on November 15,

2016. Of the cards sold in October, $100 were redeemed in October, $250 in November,

and $300 in December. Of the cards sold in November, $150 were redeemed in

November and $350 were redeemed in December. Peterson views the probability of

redemption of a gift card as remote if the card has not been redeemed within two

months. At 12/31/2016, Peterson would show an deferred revenue account for the gift

cards with a balance of:

a. $0.

b. $1,000.

c. $1,350.

d. $1,500.

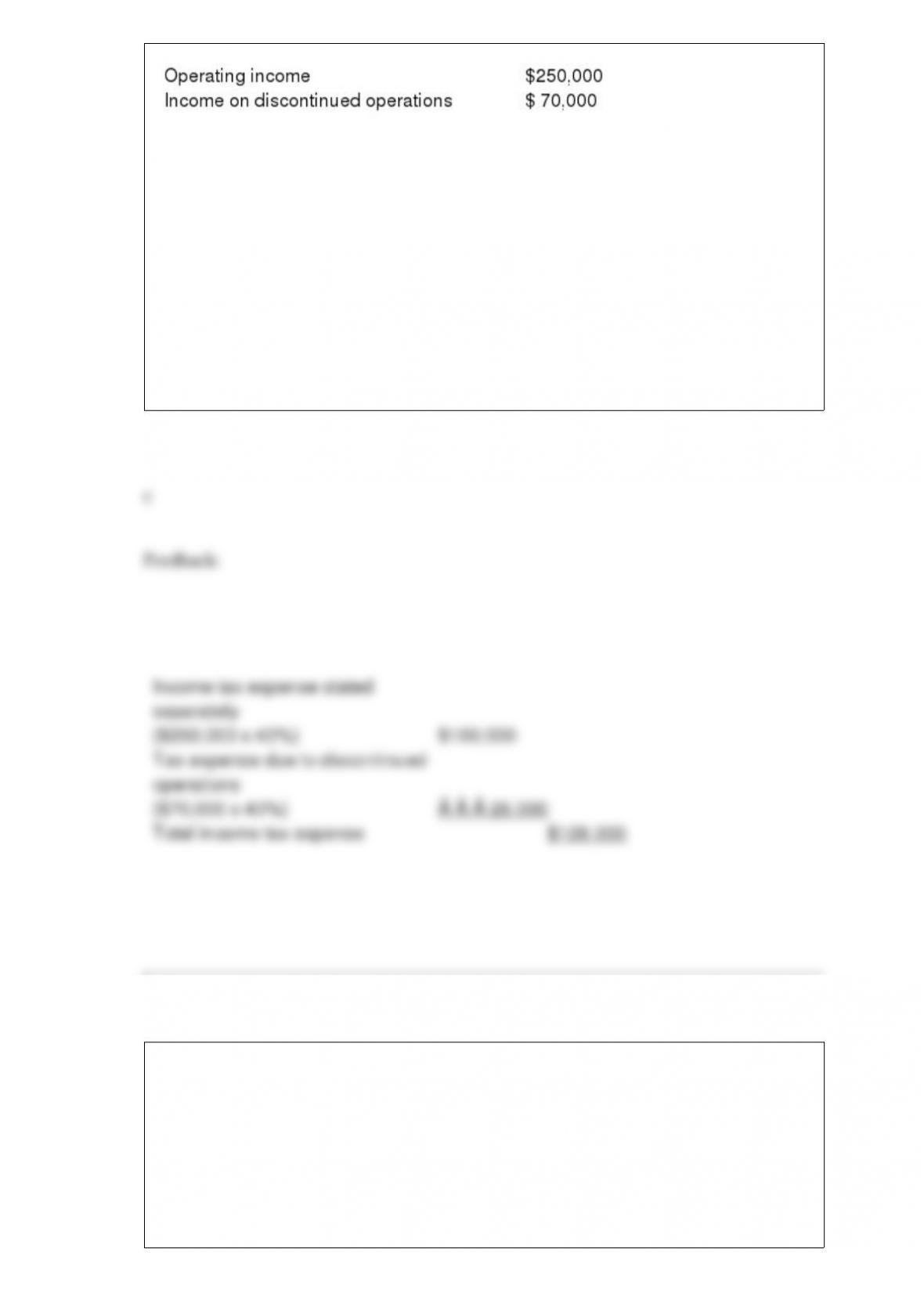

Freda’s Florist reported the following before-tax income statement items for the year

ended December 31, 2016:

All income statement items are subject to a 40% income tax rate. In its 2016 income

statement, Freda’s separately stated income tax expense and total income tax expense

would be:

a. $128,000 and $128,000, respectively.

b. $128,000 and $100,000, respectively.

c. $100,000 and $128,000, respectively.

d. $100,000 and $100,000, respectively.

The inventory method that will always produce the same amount for cost of goods sold

in a periodic inventory system as in a perpetual inventory system would be:

a. FIFO.

b. LIFO.

c. Weighted average.

d. None of these answer choices is correct.

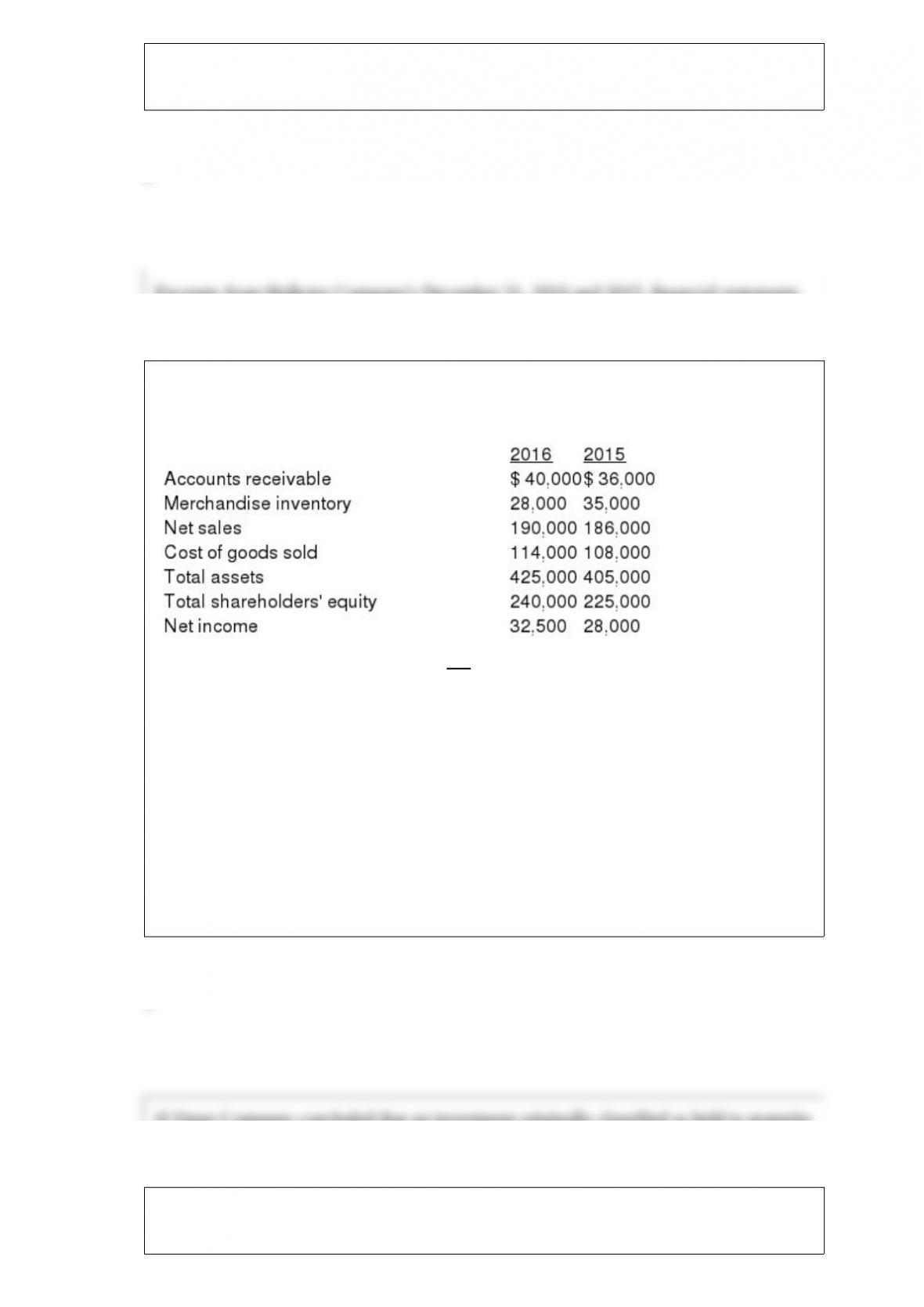

Excerpts from Hulkster Company’s December 31, 2016 and 2015, financial statements

are presented below:

Under IFRS, which of the following is not a condition for recognizing revenue?

a) The amount of revenue and costs associated with the transaction can be measured

reliably.

b) It is reasonably possible that the economic benefits associated with the transaction

will flow to the seller.

c) For sales of goods, the seller has transferred to the buyer the risks and rewards of

ownership and doesn’t effectively manage or control the goods.

d) For sales of services, the stage of completion can be measured reliably.

If Ziggy Company concluded that an investment originally classified as held to maturity

would now more appropriately be classified as available for sale, Ziggy would:

a. Not reclassify the investment, as original classifications are irrevocable.

b. rReclassify the investment as available for sale and immediately recognize in net

income any unrealized gain or loss on the reclassification date.

c. Reclassify the investment as available for sale and immediately recognize in

accumulated other comprehensive income any unrealized gain or loss on the

reclassification date.

d. Need to restate earnings, as the original classification was in error.

() $3 x 15 shares = $45

On December 1, 2016, LCD Distributing Company (“LCD or “Company”) issued a

press release announcing its financial results for the fiscal year ended November 30,

2016. Included was the following information regarding a change in inventory method

(in part):

In the fourth quarter of fiscal 2016, the Company changed its inventory valuation

method from the Last-In First-Out (LIFO) method to the First-In First-Out (FIFO)

method. The change is preferable as it provides a more meaningful presentation of the

Company’s financial position as it values inventory in a manner which more closely

approximates current cost; better represents the underlying commercial substance of

selling the oldest products first; and more accurately reflects the Company’s realized

periodic income.

As required by U.S. generally accepted accounting principles, this change in accounting

principle has been reflected in the consolidated statements of financial position,

consolidated statements of operations, and consolidated statements of cash flows

through retroactive application of the FIFO method. Previously reported net income

(loss) available to common shareholders’ for the fiscal years 2016 and 2015 were

increased by $0.4 million and $2 million after income taxes, respectively.

Required:

1) Why does GAAP require LCD to retrospectively adjust prior years’ financial

statements for this type of accounting change?

2) Assuming that the quantity of inventory remained stable during 2015, did the cost of

LCD’s inventory move up or down during that period?

Which of the following is true about the initial journal entry used to record

quality-assurance warranties?

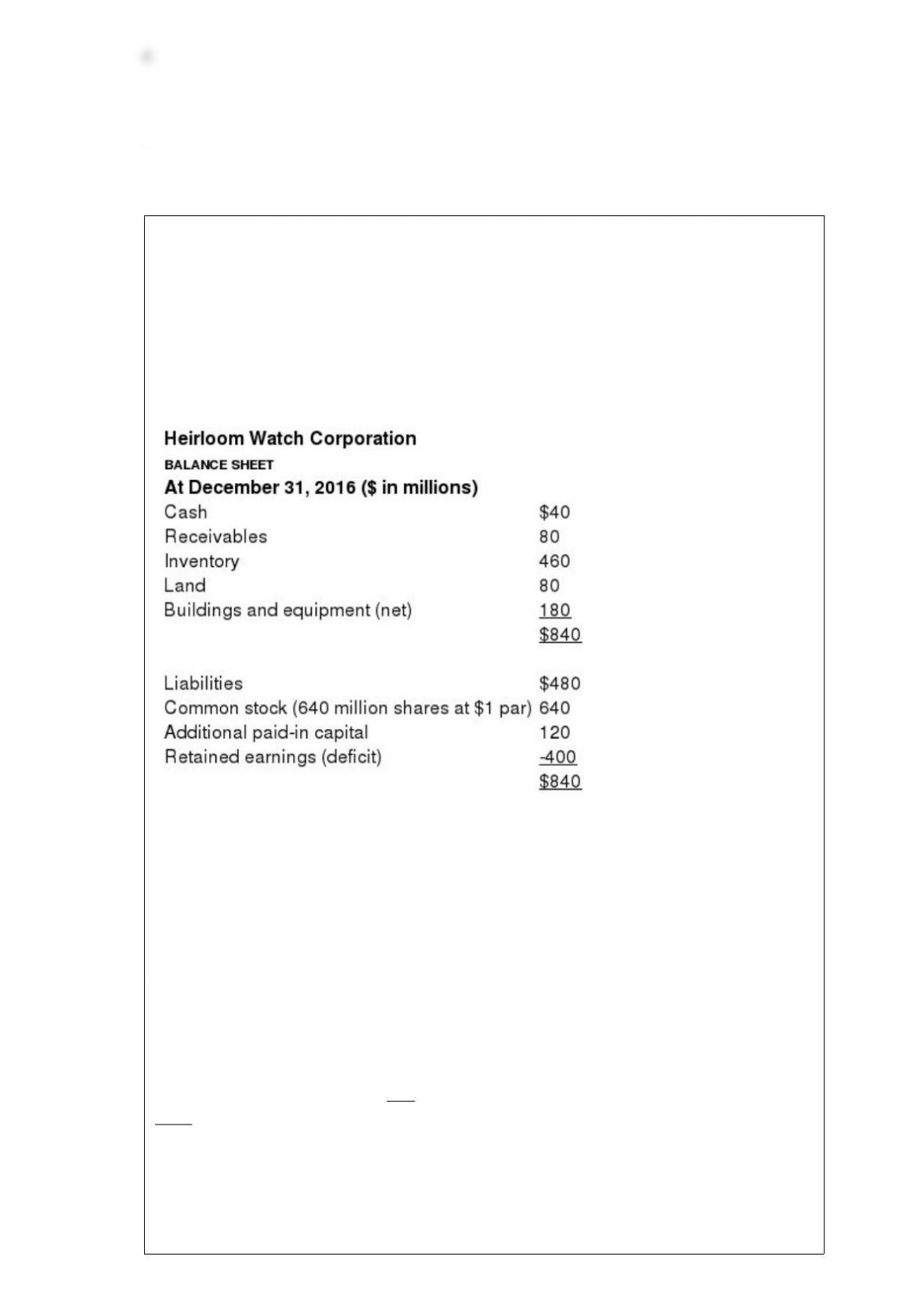

A new CEO was hired to revive the floundering Heirloom Watch Corporation. The

company had endured operating losses for several years, but confidence was emerging

that better times were ahead. The board of directors and shareholders approved a

quasi-reorganization for the corporation. The reorganization included devaluing

inventory for obsolescence by $210 million and increasing land by $10 million.

Immediately before the restatement, at December 31, 2016, Heirloom Watch

Corporation”s balance sheet appeared as follows (in condensed form):

Heirloom Watch Corporation

balance sheet

At December 31, 2016 ($ in millions)

Cash $ 40

Receivables 80

Inventory 460

Land 80

Buildings and equipment (net) 180

$840

Liabilities $480

Common stock (640 million shares at $1 par) 640

Additional paid-in capital 120

Retained earnings (deficit) (400)

$840

Identify the three common forms of business organization and the primary difference in

the way we account for them.

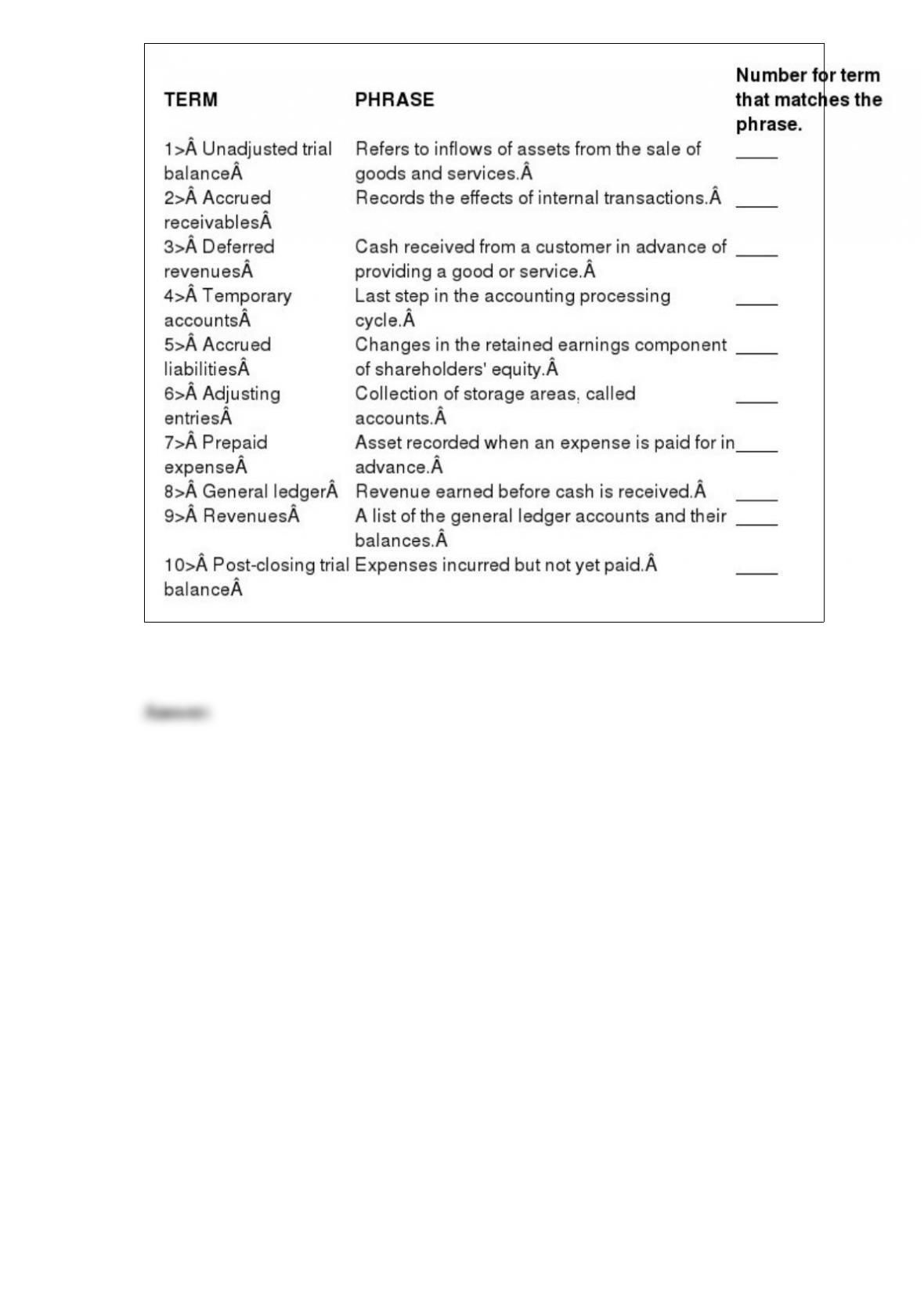

Listed below are 10 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the number for the correct term.

Define a loss contingency and give two examples that almost always are accrued.

Sunnyvale Computer Company sells a line of computers that carry a six-month

warranty. Customers are offered the opportunity to buy a two-year extended warranty

for an additional charge. During 2016, Sunnyvale received $320,000 from customers

for these extended warranties. All sales are on credit, and funds are received evenly

throughout the year and the warranties go into effect immediately after purchase.

Required:

Prepare a summary journal entry to record sales of the extended warranties. Also

prepare any other entries associated with the warranties that should be recorded during

2016.

Silicon Chip Company’s fiscal year-end is December 31. At the end of 2016, it owed

employees $22,000 in salaries and wages that will be paid on January 7, 2017.

Required:

1> Prepare an adjusting entry to record accrued salaries and wages, a reversing entry on

January 1, 2017, and an entry to record the payment of salaries and wages on January 7,

2017.

2> Prepare journal entries to record the accrued salaries and wages on December 31 and

the payment of salaries and wages on January 7, assuming a reversing entry is not

recorded.

DON Corp. is contemplating the purchase of a machine that will produce net after-tax

cash savings of $20,000 per year for five years. At the end of five years, the machine

can be sold to realize after-tax cash flows of $5,000. Interest is 12%. Assume the cash

flows occur at the end of each year.

Required: Calculate the total present value of the cash savings.