On March 1, Cooper Company borrows $80,000 from New National Bank by signing a

6-month, 6%, interest-bearing note.

Instructions

Prepare the necessary entries below associated with the note payable on the books of

Cooper Company.

(a)Prepare the entry on March 1 when the note was issued.

(b)Prepare any adjusting entries necessary on June 30 in order to prepare the

semiannual financial statements. Assume no other interest accrual entries have been

made.

(c)Prepare the entry to record payment of the note at maturity.

Operating expenses would include

a.interest expense.

b.income tax expense.

c.freight-out.

d.freight-out and interest.

With regard to accounting for a merchandising company versus a service company,

which of the following is true?

a.Additional accounts and entries are typically required for a service company.

b.Retailers and wholesalers can be either service companies or merchandising

companies.

c.The operating cycle of a merchandising company is longer than that of a service

company.

d.Because inventory is an asset, it is recognized on the balance sheet by both service

and merchandising companies.

Cochran Corporation, Inc. has the following income statement (in millions):

COCHRAN CORPORATION, INC.

Income Statement

For the Year Ended December 31, 2014

Using vertical analysis, what percentage is assigned to net income?

a.100%

b.60%

c.40%

d.33%

Benedict Company compiled the following financial information as of December 31,

2014:

Benedict’s stockholders’ equity on December 31, 2014 is

a.$420,000.

b.$440,000.

c.$320,000.

d.$480,000.

At December 31, 2014, before any year-end adjustments, Dallis Company’s Prepaid

Insurance account had a balance of $2,900. It was determined that $1,300 of the Prepaid

Insurance had expired. The adjusted balance for Insurance Expense for the year would

be:

a.$1,300.

b.$1,600.

c.$2,900.

d.$1,400.

Using the following balance sheet and income statement data, what is the debt to assets

ratio?

Average common shares outstanding was 10,000.

a.20.5 percent

b.30 percent

c.33.3 percent

d.40.9 percent

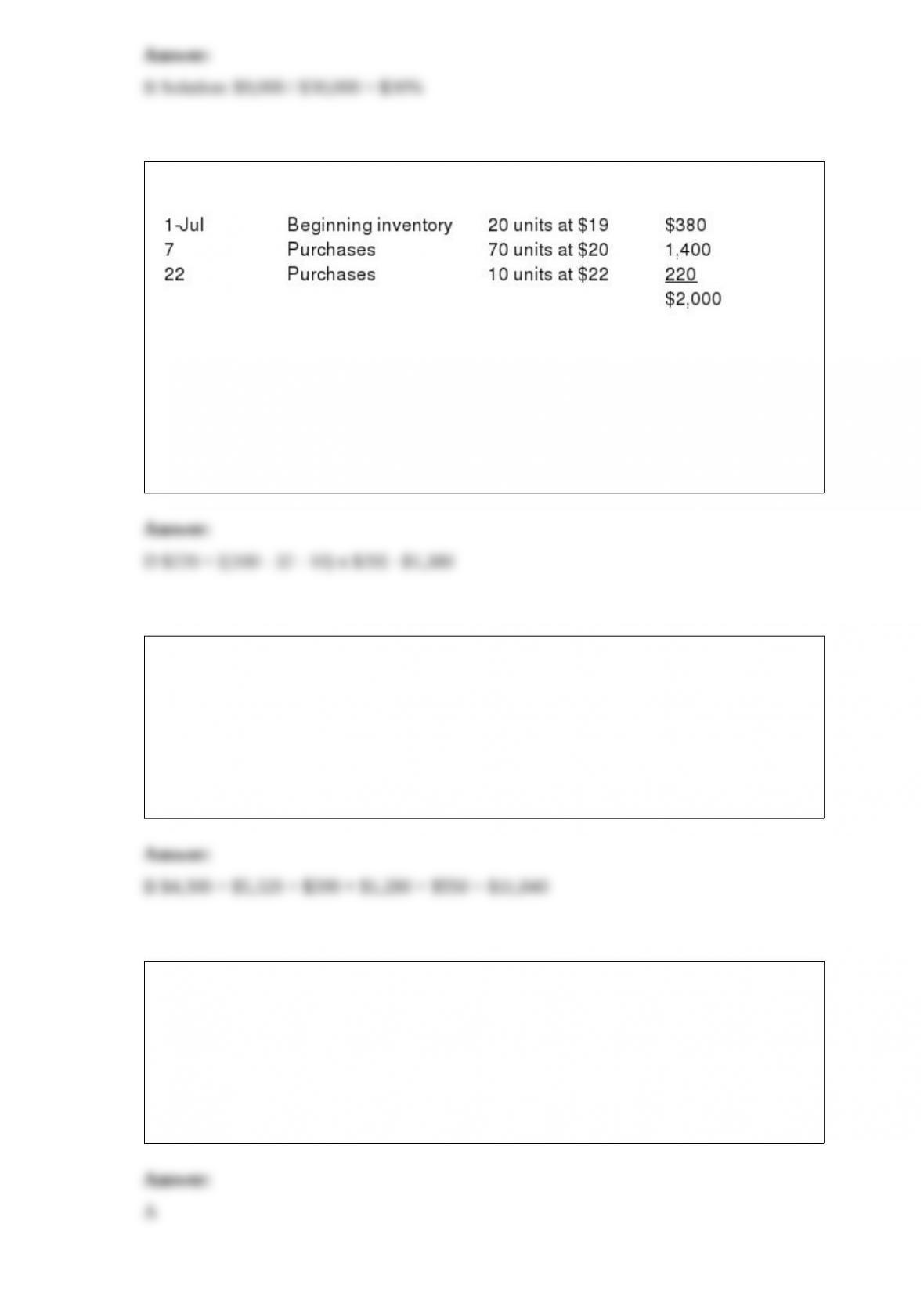

Quiet Phones Company has the following inventory data:

A physical count of merchandise inventory on July 30 reveals that there are 32 units on

hand. Using the LIFO inventory method, the amount allocated to cost of goods sold for

July is

a.$620.

b.$660.

c.$1,340.

d.$1,380.

Based on the account balances below, what is the total of the debit and credit columns

of the adjusted trial balance?

a.$10,150

b.$11,840

c.$10,560

d.$11,430

Reardon Inc. has an investment in trading securities of $120,000. This investment

experienced an unrealized loss of $6,000 during the current year. Assuming a 35% tax

rate, the effect of this loss on comprehensive income will be

a.no effect.

b.$120,000 increase.

c.$42,000 decrease.

d.$78,000 decrease.

Oliver Company issued $800,000 of 6%, 5-year bonds at 98. Assuming straight-line

amortization and annual interest payments, how much bond interest expense is recorded

on the next interest date?

a.$48,000

b.$24,000

c.$49,600

d.$51,200

If Jane Key invests $15,501.28 now and she will receive $40,000 at the end of 11 years,

what annual rate of interest will she be earning on her investment?

a.8%

b.8.5%

c.9%

d.10%

Prepare the journal entries to record the following transactions for Reese Company,

which has a calendar year end and uses the straight-line method of depreciation.

(a)On September 30, 2014, the company sold old equipment for $46,000. The

equipment was purchased on January 1, 2012, for $96,000 and was estimated to have a

$16,000 salvage value at the end of its 5-year life. Depreciation on the equipment has

been recorded through December 31, 2013.

(b)On June 30, 2014, the company sold old equipment for $24,000. The equipment

originally cost $36,000 and had accumulated depreciation to the date of disposal of

$15,000.

The following credit sales are budgeted by Gonzalez Company:

The company€s past experience indicates that 80% of the accounts receivable are

collected in the month of sale, 20% in the month following the sale. The anticipated

cash inflow for the month of March is

a.$198,000.

b.$168,000.

c.$210,000.

d.$204,000.

The entry to record a sale of $700 with terms of 2/10, n/30 will include a

a.credit to Sales Discounts for $14.

b.debit to Cash for $686.

c.credit to Accounts Receivable for $700.

d.credit to Sales Revenue for $700.

Somen to Park Corporation had net credit sales of $4,060,000 and cost of goods sold of

$3,000,000 for the year. The Accounts Receivable balances at the beginning and end of

the year were $650,000 and $750,000, respectively. The accounts receivable turnover

was

a.6.7 times.

b.6.2 times.

c.5.8 times.

d.6.4 times.

Bonds with a face value of $300,000 and a quoted price of 102¼ have a selling price of

a.$360,675.

b.$306,075.

c.$300,675.

d.$306,750.

How should the cost of intangible assets with indefinite lives be accounted for?

a.They should be amortized over the assets’ estimated useful lives, or their legal lives,

whichever is shorter.

b.They should be amortized over the assets’ estimated useful lives, or their legal lives,

whichever is longer.

c.They should be capitalized as an asset and checked for impairment periodically.

d.They should be expensed at acquisition.

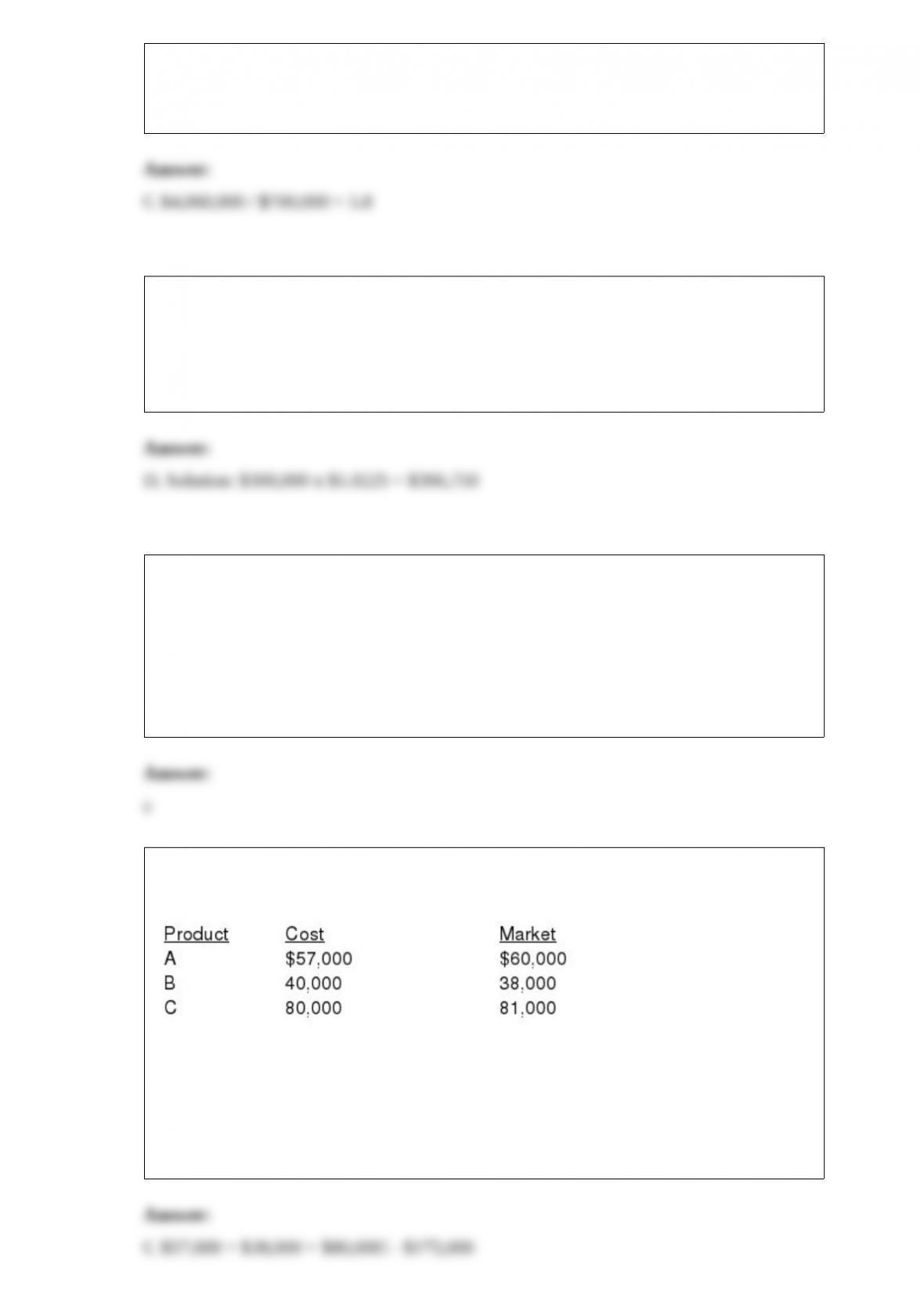

Jenks Company developed the following information about its inventories in applying

the lower of cost or market (LCM) basis in valuing inventories:

If Jenks applies the LCM basis, the value of the inventory reported on the balance sheet

would be

a.$177,000.

b.$179,000.

c.$175,000.

d.$181,000.