1) An auditor needs to determine whether all customers of an electric utility company

are being billed. The auditor should test from the:

A) sales register to the accounts receivable ledger

B) sales register to the meter department records

C) accounts receivable ledger to the sales register

D) meter department records to the sales register

2) Required sample size increases as the auditor’s tolerable misstatement for an account

balance or class of transactions decreases.

A) True

B) False

3) In evaluating sample results for tests of details, auditors must evaluate exceptions

identified by the performance of audit procedures.

A) True

B) False

4) In performing a review of a client’s cash disbursements, an auditor uses systematic

sample selection with a random start. The primary disadvantage of this technique is

population items:

A) may occur twice in the sample

B) must be reordered in a systematic pattern before the sample can be drawn

C) may occur in a systematic pattern, thus negating the randomness of the sample

D) must be replaced in the population after sampling to permit valid statistical inference

5) Collectively, procedures performed to obtain an understanding of the entity and its

environment, including internal controls, represent the auditor’s:

A) audit strategy

B) tests of controls

C) risk assessment procedures

D) tests of transactions

6) The audit procedure “Account for unused tag numbers shown in the auditor’s

working papers to make sure no tags have been added” provides assurance mainly for

the existence objective for inventory pricing and compilation.

A) True

B) False

7) Audit standards require the auditor to consider materiality early in the audit. Which

statement(s) regarding preliminary materiality are true?

I.Preliminary materiality may change during the engagement.

II.Preliminary materiality is the maximum amount the auditor by which the auditor

believes the financials could be misstated and still not affect the decisions of reasonable

users.

A) I only

B) II only

C) both I and II

D) neither are true

8) Application controls vary across the IT system. To gain an understanding of internal

control for a private company, the auditor must evaluate the application controls for

every:

A) audit area

B) material audit area

C) audit area in which the client uses the computer

D) audit area where the auditor plans to reduce assessed control risk

9) The assessment against a defendant of that portion of the damage caused by the

defendant’s negligence is called:

A) separate and proportionate liability

B) joint and several liability

C) shared liability

D) unitary liability

10) Assume that the client’s valuation of an inventory item is $10 per unit for 1,000

units, using first-in, first-out (FIFO). If the most recent acquisition of inventory was for

600 units at $10 per unit and the immediately preceding acquisition was for 700 units at

$9 per unit, the inventory item is in error and it is:

A) understated $400

B) understated $300

C) overstated $400

D) overstated $700

11) An independent review must be performed of all audits.

A) True

B) False

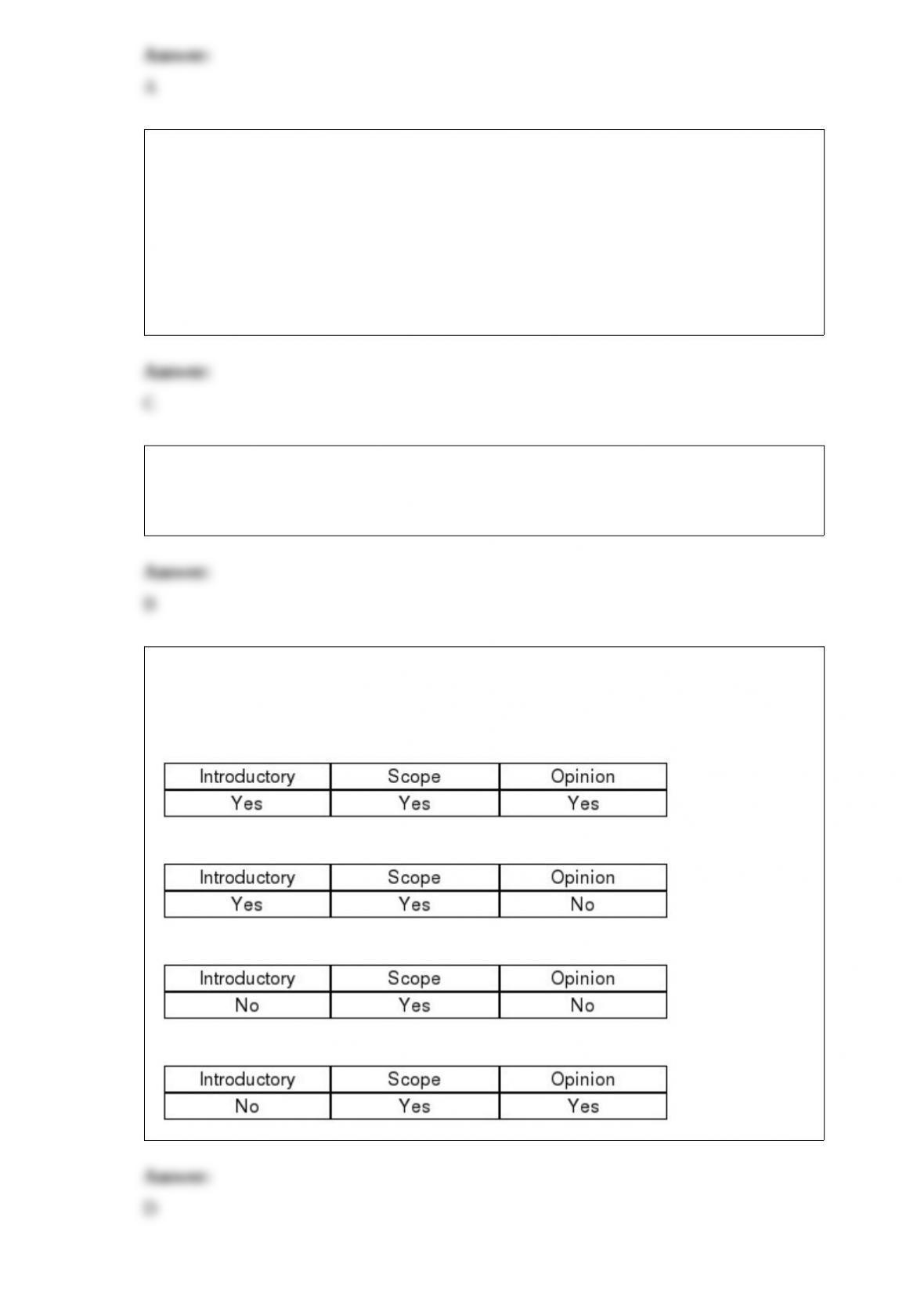

12) When an auditor issues a qualified report due to a scope limitation an explanatory

paragraph is normally added. Which, if any, of the following paragraphs are also

modified?

A)

B)

C)

D)

13) The balance-related audit objective realizable value is not applicable when auditing

Accounts payable.

A) True

B) False

14) A third-party beneficiary is one which:

A) has failed to establish legal standing before the court

B) does not have privity of contract and is unknown to the contracting parties

C) does not have privity of contract, but is known to the contracting parties and

intended to benefit under the contract

D) may establish legal standing before the court after a contract has been consummated

15) Recording, classifying, and summarizing economic events in a logical manner for

the purpose of providing financial information for decision making is commonly called:

A) finance

B) auditing

C) accounting

D) economics

16) Auditors will generally send a standard inquiry letter to:

A) only those attorneys who have devoted substantial time to client matters during the

year

B) every attorney that the client has been involved with in the current or preceding year,

plus any attorney the client engages on occasion

C) those attorneys whom the client relies on for advice related to substantial legal

matters

D) only the attorney who represents the client in proceeding where the client is

defendant

17) Handling the receipt of ordered goods is a part of the ________ cycle.

A) purchasing

B) acquisition and payment

C) inventory

D) inventory and warehousing

18) To be considered reliable evidence, confirmations must be controlled by:

A) a client employee responsible for accounts receivable

B) a financial statement auditor

C) a client’s internal audit department

D) a client’s controller or CFO

19) Risk assessment procedures are performed by auditors during an audit in order to:

A) determine the risk of material misstatement in the financial statements

B) determine the amount of testing of internal control

C) determine the extent of testing of details of balances

D) determine the extent of testing of transactions

20) The record of the outstanding shares at any given time is maintained in the:

A) corporate directory

B) stock certificate books

C) schedule of stock owners

D) shareholders’ capital stock master file

21) Rule 505, Form of Organization and Name, prohibits CPA firms from practicing as

limited liability partnerships.

A) True

B) False

22) Which of the following is not a reason why the auditor requests that the client

provide a letter of representation?

A) Professional auditing standards require the auditor to obtain a letter of representation

B) It impresses upon management its responsibility for the accuracy of the information

in the financial statements

C) It provides written documentation of the oral responses already received to inquiries

of management

D) It provides written documentation, which is a higher quality of evidence than

management’s oral responses to inquiries

23) Tolerable misstatement is often set at a(n) ________ level for notes payable.

A) high

B) moderate

C) low

D) unknown

24) Which of the following would you normally characterize as a difficult and complex

account to audit?

A) property, plant and equipment

B) cash

C) inventory

D) prepaid insurance

25) The primary emphasis by auditors when evaluating and testing internal control is on

controls over classes of transactions rather than controls over account balances.

A) True

B) False

26) If the auditor concludes that there are contingent liabilities, he or she must evaluate

the significance of the potential liability and the nature of the disclosure needed in the

financial statements. Which of the following statements is not true?

A) The potential liability is sufficiently well known in some instances to be included in

the financial statements as an actual liability

B) Disclosure may be unnecessary if the contingency is highly remote or immaterial

C) Frequently, the CPA firm obtains a separate evaluation of the potential liability from

its own legal counsel rather than relying on management or management’s attorneys

D) Answers B and C are correct, but answer A is not

27) For effective internal control, it is important that sales be recorded as soon after the

customer order is received as possible to prevent the unintentional omission of

transactions from the records and to make sure that sales are recorded in the proper

period.

A) True

B) False

28) Before the population can be considered acceptable based on the acceptable risk of

assessing control risk too low, the computed upper exception rate must be:

A) greater than or equal to the tolerable exception rate

B) greater than the tolerable exception rate

C) less than or equal to the tolerable exception rate

D) less than the tolerable exception rate

29) External auditors would consider internal auditors effective if they are:

A) independent of the operating units being evaluated

B) competent and well trained

C) have performed relevant audit tests of the internal controls and financial statements

D) all of the above

30) The purpose of an engagement letter is to:

A) document the CPA firm’s responsibility to external users of the audited financial

statements

B) document the terms of the engagement

C) notify the audit staff of an upcoming engagement so that personnel scheduling can

be facilitated

D) emphasize management’s responsibility for approving the audit program

31) Discuss the four characteristics of the capital acquisition and repayment cycle that

make it unique from other cycles.

32) Many auditors prove the subsequent period bank statement if a cutoff statement is

not received directly from the bank. Discuss the purpose of proving the subsequent

period statement, and explain the audit procedures performed during the proof.

33) There are several internal controls in the personnel and employment function that

are important from an audit perspective. For example, there should be an adequate

investigation of the competence and trustworthiness of new employees. Discuss other

internal controls in the personnel and employment function that are important from an

audit perspective.

34) State the four most important audit objectives for capital stock and describe how the

auditor typically verifies each of the four objectives.

35) The most important difference among tests of controls, substantive tests of

transactions, and tests of details of balances lies in what the auditor wants to measure.

Explain what each type of test attempts to measure.

36) How do the risk and materiality thresholds change in a government audit compared

to a financial statement audit of a public company?

37) The Institute of Internal Auditors has established Ethical Principles for its members.

List each of the principles.

38) Discuss each of the five steps in applying materiality in an audit, and identify the

audit phase(s) in which each step is performed. List these steps in the order in which

they occur.

39) Discuss the four areas of responsibility under the IT function that should be

segregated in large companies.

40) For each of the following potential misstatements, provide one potential audit test

that could be used to detect the misstatement.

Sales included in the journals for which there was no shipment

Sale recorded more than once

Shipments made to nonexistent customers and recorded as sales