1) Eberley Corporation’s cost formula for its manufacturing overhead is $25,700 per

month plus $10 per machine-hour. For the month of July, the company planned for

activity of 5,900 machine-hours, but the actual level of activity was 5,920

machine-hours. The actual manufacturing overhead for the month was $86,800.

The manufacturing overhead in the planning budget for July would be closest to:

A.$84,900

B.$86,800

C.$84,700

D.$86,507

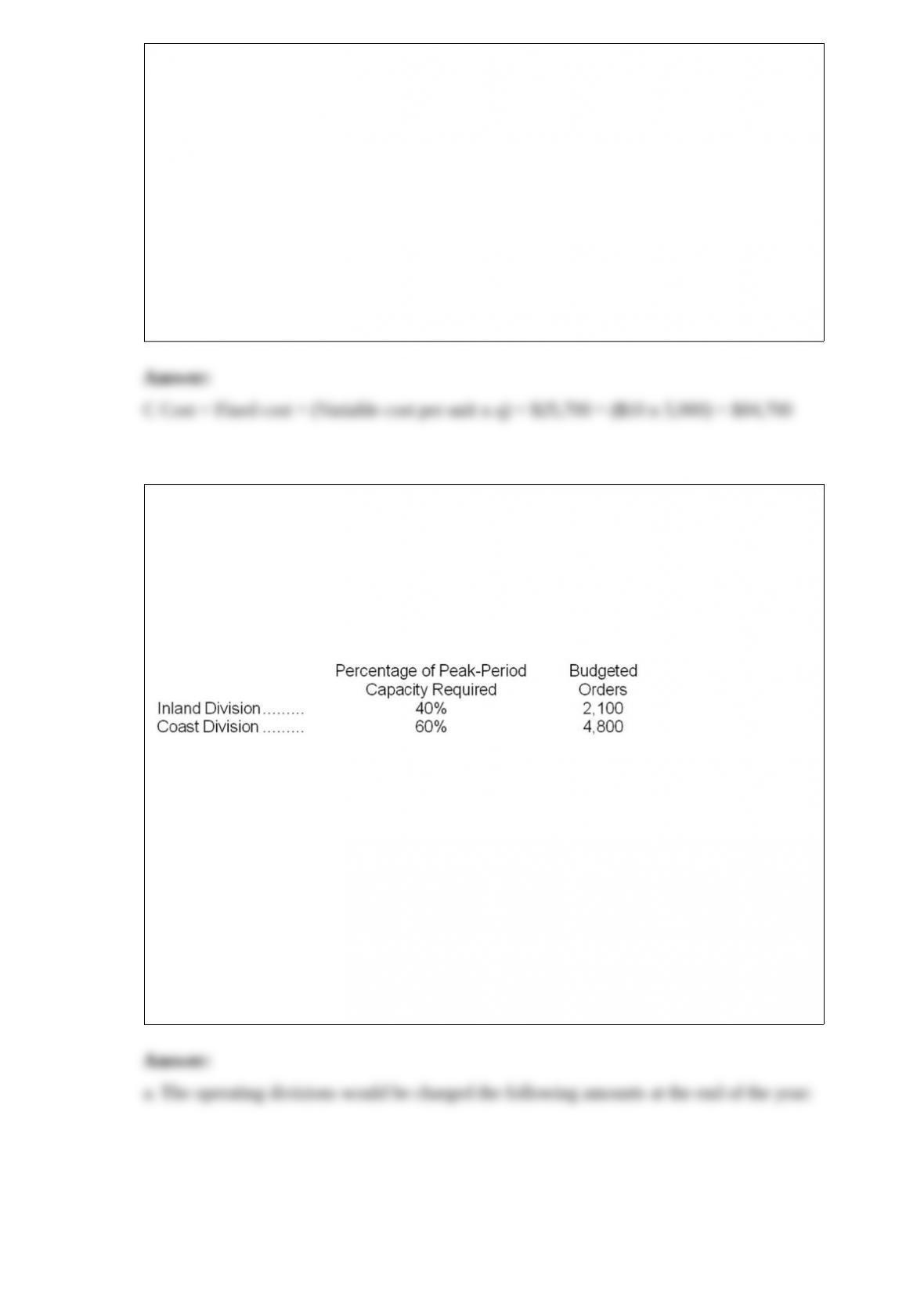

2) Larubbio Corporation has two operating divisions–an Inland Division and a Coast

Division. The company’s Customer Service Department provides services to both

divisions. The variable costs of the Customer Service Department are budgeted at $23

per order. The Customer Service Department’s fixed costs are budgeted at $407,100 for

the year. The fixed costs of the Customer Service Department are determined based on

the peak-period orders.

At the end of the year, actual Customer Service Department variable costs totaled

$168,560 and fixed costs totaled $426,700. The Inland Division had a total of 2,110

orders and the Coast Division had a total of 4,770 orders for the year.

Required:

a. Prepare a report showing how much of the Customer Service Department’s costs

should be charged to each of the operating divisions at the end of the year.

b. How much of the actual Customer Service Department costs should not be charged to

the operating divisions at the end of the year? Who should be held responsible for these

uncharged costs?

3) ( Peter wants to buy a computer which he expects to save him $4,000 each year in

bookkeeping costs. The computer will last for five years, and at the end of five years it

will have no salvage value. If Peter’s required rate of return is 12%, what is the

maximum price Peter should be willing to pay for the computer now?

A.$20,000

B.$14,420

C.$11,340

D.$10,830

4) Lartey Corporation’s cost formula for its selling and administrative expense is

$22,200 per month plus $27 per unit. For the month of December, the company planned

for activity of 5,300 units, but the actual level of activity was 5,270 units. The actual

selling and administrative expense for the month was $168,150.

The activity variance for selling and administrative expense in December would be

closest to:

A.$810 U

B.$2,850 F

C.$2,850 U

D.$810 F

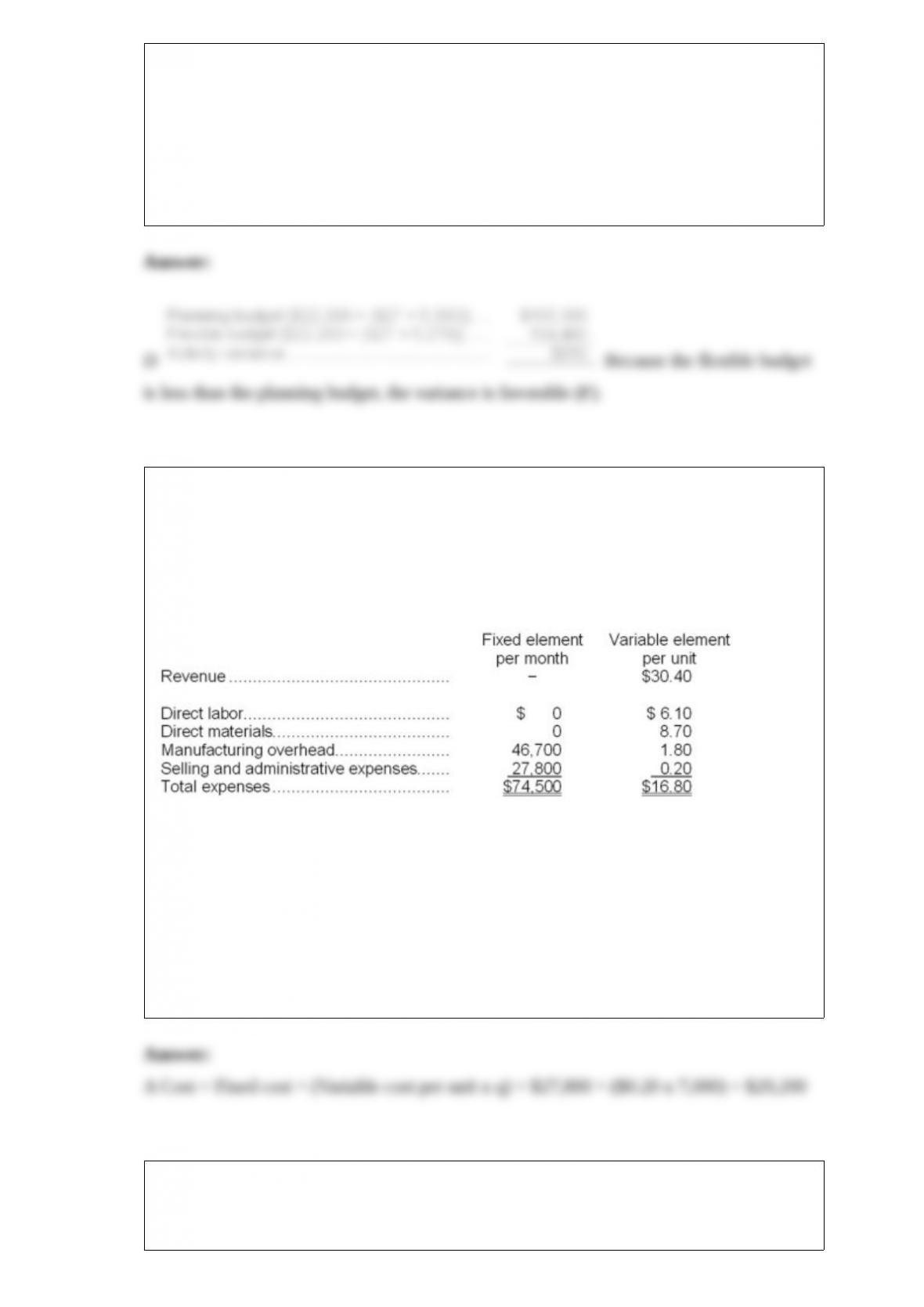

5) Letts Corporation manufactures and sells a single product. The company uses units

as the measure of activity in its budgets and performance reports. During January, the

company budgeted for 7,000 units, but its actual level of activity was 6,970 units. The

company has provided the following data concerning the formulas to be used in its

budgeting:

The selling and administrative expenses in the planning budget for January would be

closest to:

A.$29,200

B.$29,884

C.$29,194

D.$30,013

6) Rollison Corporation has two divisions: Retail Division and Wholesale Division. The

following data are for the most recent operating period:

The common fixed expenses of the company are $76,300.

The Retail Division’s break-even sales in dollars is closest to:

A.$469,884

B.$200,000

C.$251,211

D.$300,395

7) The debits to the Manufacturing Overhead account as a consequence of the raw

materials transactions in August total:

A.$6,000

B.$69,000

C.$0

D.$63,000

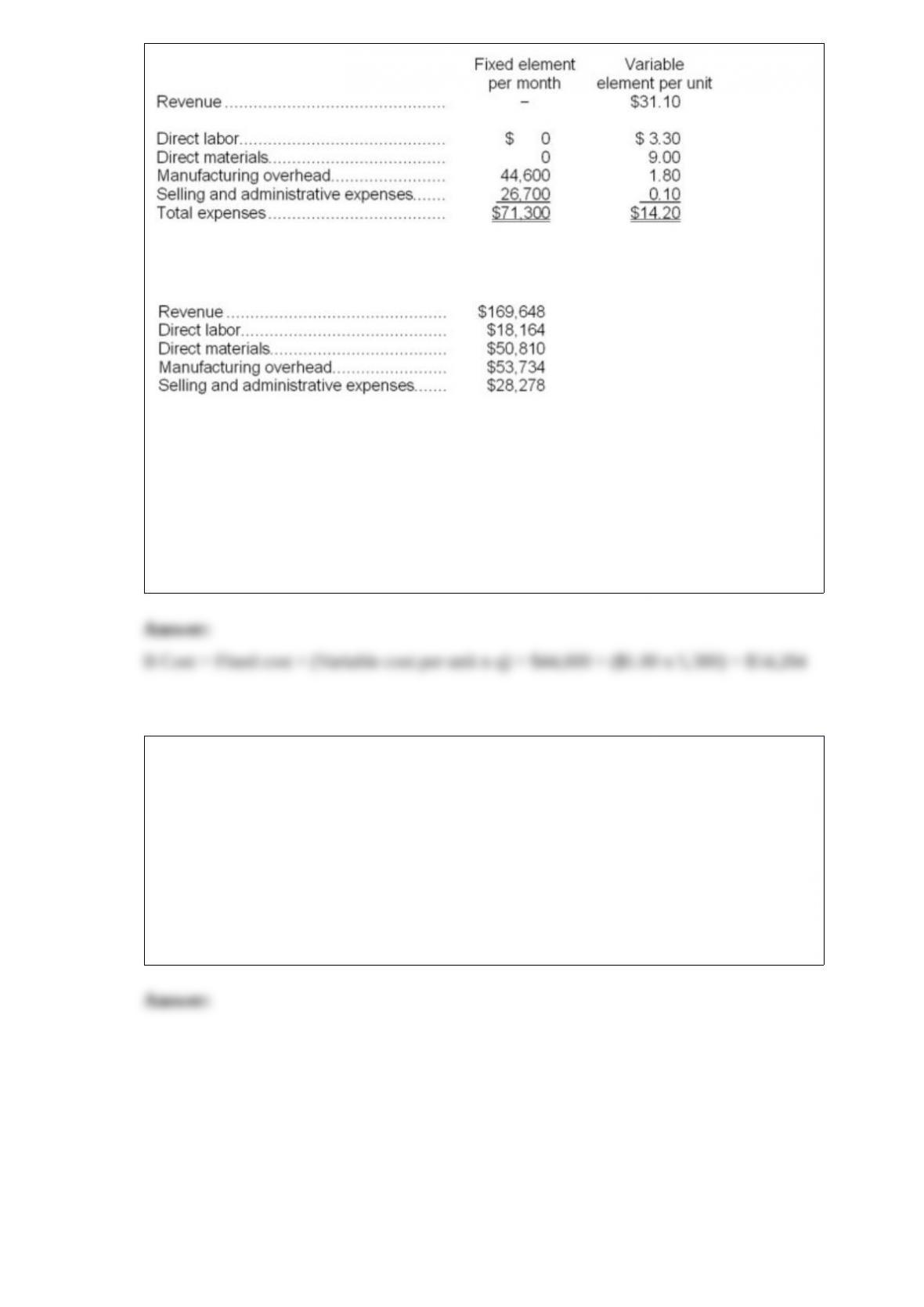

8) Prater Corporation manufactures and sells a single product. The company uses units

as the measure of activity in its budgets and performance reports. During February, the

company budgeted for 5,400 units, but its actual level of activity was 5,380 units. The

company has provided the following data concerning the formulas used in its budgeting

and its actual results for February:

Data used in budgeting:

Actual results for February:

The manufacturing overhead in the flexible budget for February would be closest to:

A.$53,934

B.$54,284

C.$54,320

D.$53,535

9) ( Beaver Corporation is investigating the purchase of a new threading machine that

costs $18,000. The machine would save about $4,000 per year over the present method

of threading component parts, and would have a salvage value of about $3,000 in 6

years when the machine would be replaced. The company’s required rate of return is

12%. The machine’s net present value is closest to:

A.$1,556

B.$(35)

C.$11,000

D.$8,000

10) Assume that Melrose expects to sell 60,000 units of Product C to regular customers

next year. At what selling price for the 7,000 units would Melrose be economically

indifferent between accepting and rejecting the special order from Moore?

A) $53.00

B) $54.50

C) $75.00

D) $76.50

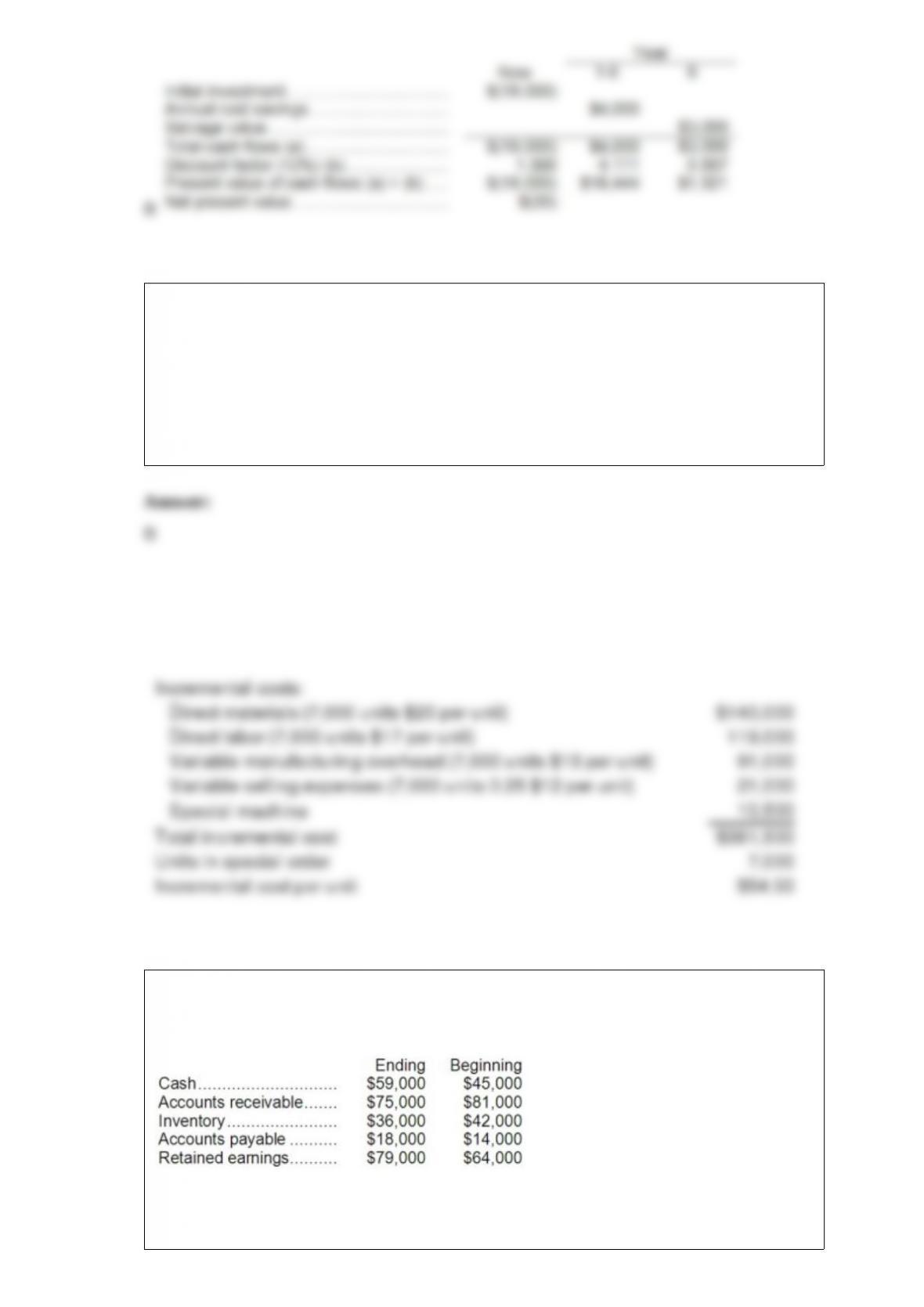

11) Kuma, Inc. had cost of goods sold of $106,000 for the just completed year. Shown

below are the beginning and ending balances of various Kuma accounts:

Kuma prepares its statement of cash flows using the direct method. On its statement of

cash flows, what amount should Kuma show for its cost of goods sold adjusted to a

cash basis (i.e., cash paid to suppliers)?

A.$100,000

B.$96,000

C.$102,000

D.$116,000

12) Based on the information above, what will be Jebb’s increase or decrease in profit

for the year if he chooses to start slicing up the lettuce instead of selling it whole?

A.$3,000 increase

B.$3,000 decrease

C.$12,000 decrease

D.$30,000 increase