In process cost accounting, direct labor includes only the labor that is applied directly to

the products.

Answer:

According to the cost principle, it is preferable for managers to report the most current

estimate of an asset’s value.

Answer:

Unearned revenues are classified as liabilities.

Answer:

Variable costing separates the variable costs from fixed costs and therefore makes it

easier to identify and assign control over costs.

Answer:

GAAP criteria for identifying a lease as a capital lease are more general than the criteria

under IFRS.

Answer:

In applying the lower of cost or market method to inventory valuation, market is

defined as the current selling price.

Answer:

The raw materials section of a job cost sheet shows the materials costs assigned to a

job, but the direct labor section shows only the total hours of labor exerted by

employees on the job.

Answer:

Departmental information is important and always disclosed to the public as part of the

company’s annual report and footnotes.

Answer:

Merchandising companies prepare the production budget after preparing the sales

budget.

Answer:

A lease is a contractual agreement between a lessor and a lessee that grants the lessee

the right to use the asset for a period of time in return for cash payment(s) to the lessor.

Answer:

An important assumption in the analysis of a multiproduct situation is that the sales mix

is known and remains constant.

Answer:

Under a traditional income statement format expenses are grouped according to cost

behavior.

Answer:

If a company’s activities include operations that are being discontinued, the income or

loss from the discontinued operations are included on the income statement as part of

income from continuing operations.

Answer:

The extent, or relative size, of fixed costs in the total cost structure is known as

operating leverage.

Answer:

The file of job cost sheets for completed but undelivered jobs equals the balance in the

Goods in Process Inventory account.

Answer:

In a double-entry accounting system, the total amount debited must always equal

the-total amount credited.

Answer:

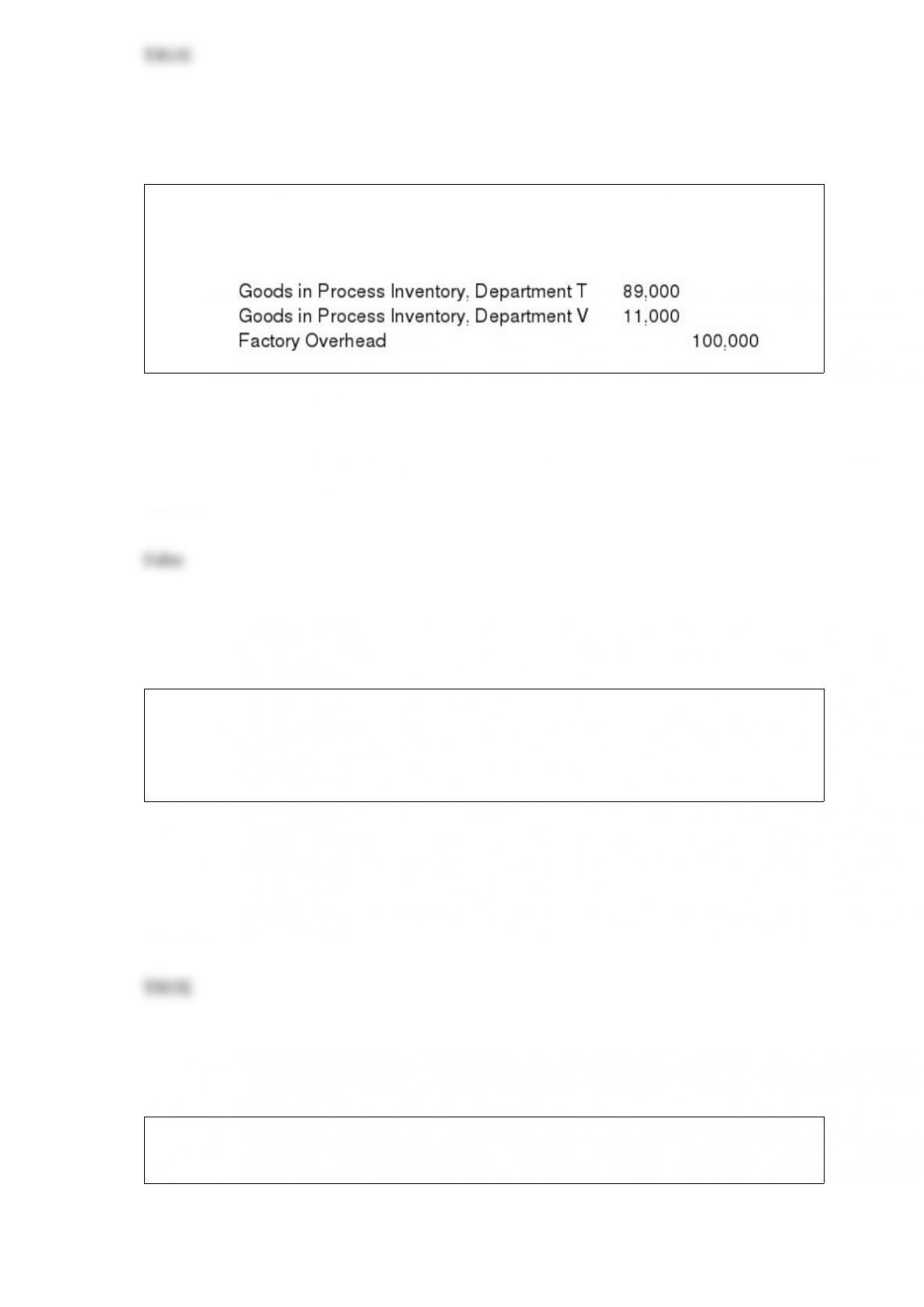

If Department T uses $89,000 of direct labor and Department V uses $11,000 of direct

labor, the following journal entry would be recorded by the process cost accounting

system:

Answer:

On May 1, Franke Co. purchases 2,000 shares of Computech stock for $25,000. This

investment is considered to be an available-for-sale investment. On July 31 (Franke’s

year-end), the stock had a market value of $28,000. Franke should record a credit to

Unrealized Gain-Equity for $3,000.

Answer:

Technology such as cash registers, check protectors, time clocks, and personal

identification scanners can increase the strength of internal controls.

Answer:

Current liabilities are obligations not due within one year or the company’s operating

cycle, whichever is longer.

Answer:

If a credit card sale is made, the seller will debit either Cash or Accounts Receivable

when the sale occurs depending on the sellers arrangements with the credit card

provider.

Answer:

If a long-term investment in an equity security gives the investor significant influence

over the investee, the investment is classified as available-for-sale.

Answer:

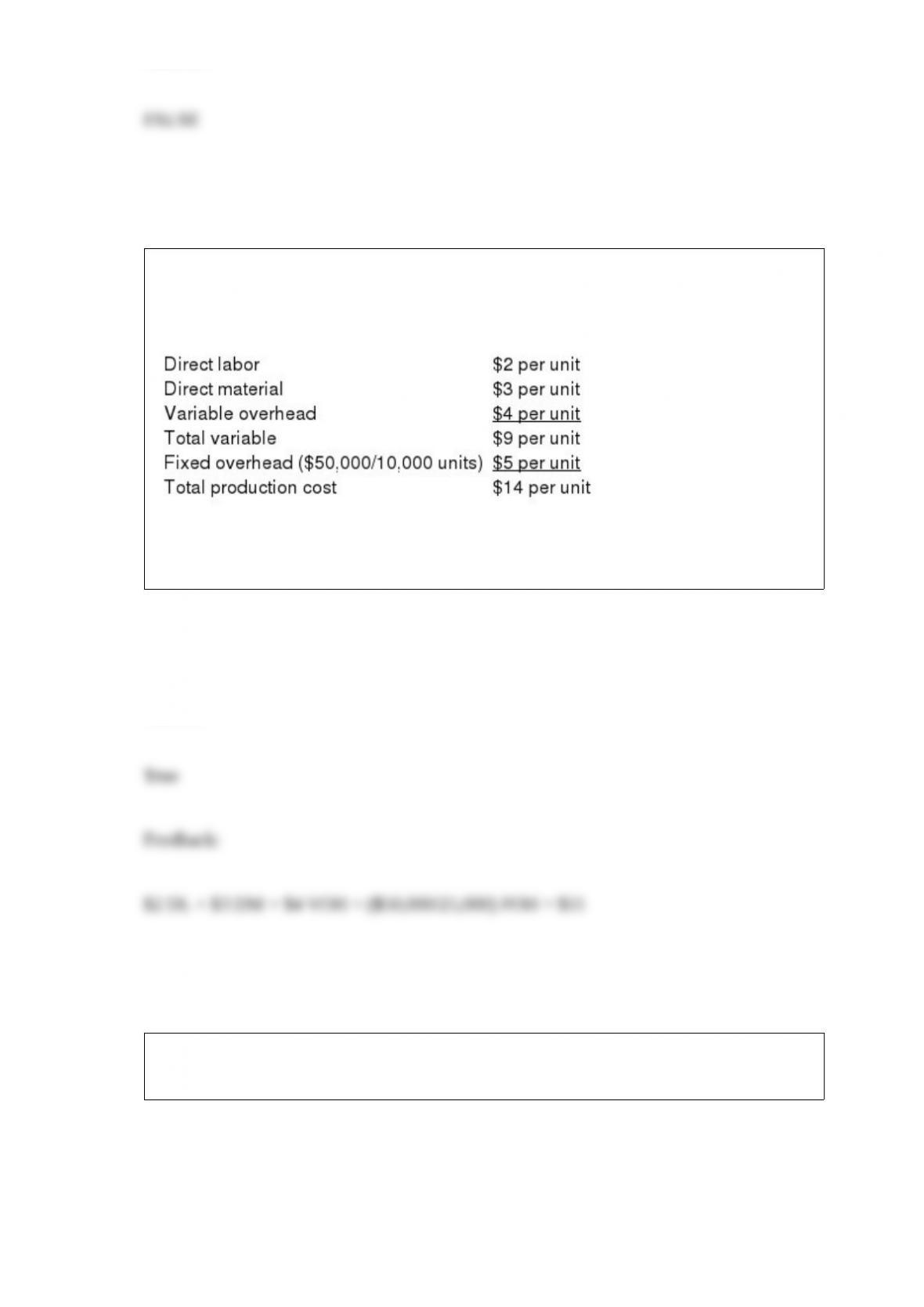

Under absorption costing, a company had the following unit costs when 10,000 units

were produced:

The total production cost per unit under absorption costing if 25,000 units had been

produced would be $11.

Answer:

The first step in using the departmental overhead rate method requires that overhead be

traced to each of the companys departments.

Answer:

Unearned revenue is another name for sales.

Answer:

A single liability can be divided between current and noncurrent liabilities.

Answer:

The adjusting entry to reflect inventory shrinkage is a debit to Income Summary and a

credit to Inventory Shrinkage Expense.

Answer:

The predetermined overhead allocation rate is used to apply overhead cost to products.

Answer:

Outstanding checks are checks the bank has paid and deducted from the customer’s

account during the month.

Answer:

In a periodic inventory system, cost of goods sold is recorded as each sale occurs.

Answer:

A company’s current ratio is 1.2 and its quick ratio is 25. This company is probably an

excellent credit risk because the ratios reveal no indication of liquidity problems.

Answer:

The last step in the four-step accounting procedure for process costing is the calculation

of equivalent units of production.

Answer:

Capital budgeting decisions are risky because the outcome is uncertain, large amounts

are usually involved, the investment involves a long-term commitment, and the decision

could be difficult or impossible to reverse.

Answer:

The time period assumption presumes that an organization’s activities can be divided

into specific time periods.

Answer:

The present value of an annuity can be computed as the sum of the individual future

values for each payment.

Answer:

If the seller is responsible for paying freight charges, then ownership of inventory

passes when goods arrive at their destination.

Answer:

Accounting is one way important financial information about businesses is reported to

decision makers.

Answer:

A cost variance equals the sum of the quantity variance and the price variance.

Answer:

Employers must pay FICA taxes that are equal to the amount being withheld from their

employees.

Answer:

Any unrealized gain or loss on available-for-sale securities is reported on the income

statement in the other gain or loss section.

Answer:

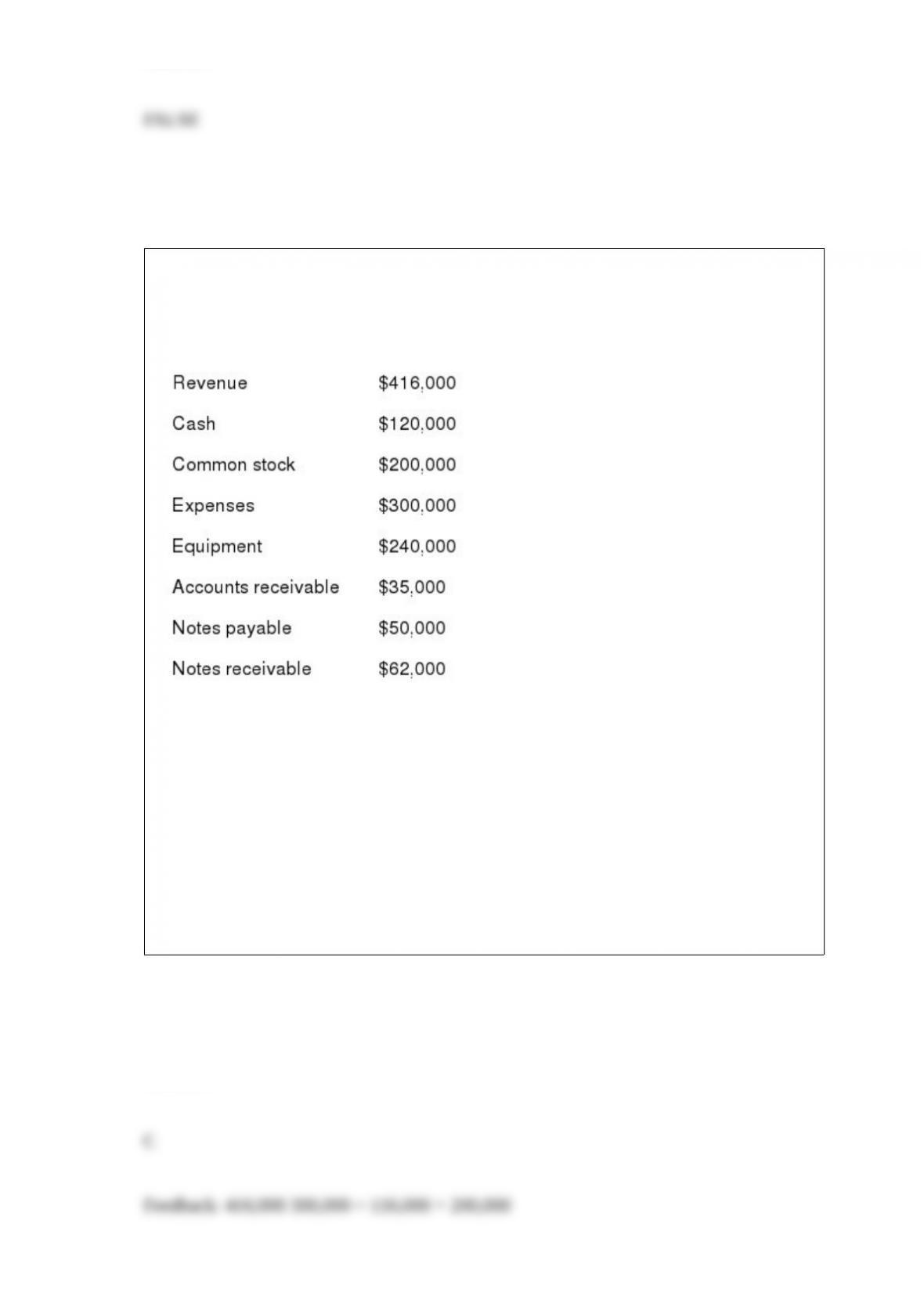

Below is accounting information for Cascade Company for 2013, its first year of

business

What was total equity at year end?

A. $320,000

B. $296,000

C. $316,000

D. $457,000

E. $116,000

Answer:

A department had 65 units which were 20% complete in beginning Goods in Process

Inventory. During the current period, 77 units were transferred out. Ending Goods in

Process Inventory was 30 units which were 20% complete. Using the FIFO method,

what are the equivalent units produced if all direct material and direct labor are added

uniformly throughout the process?

A. 83

B. 70

C. 100

D. 77

E. 107

Answer:

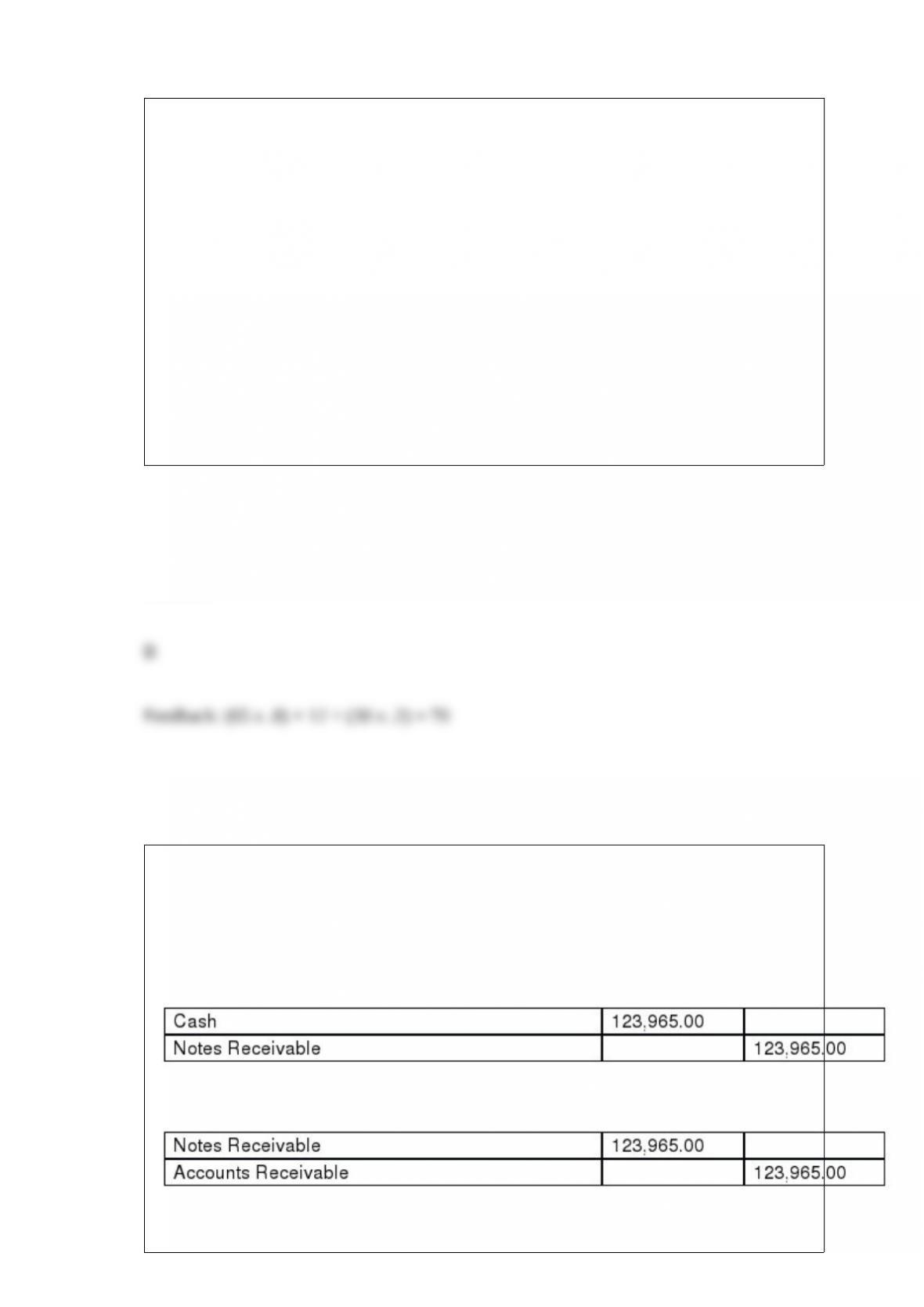

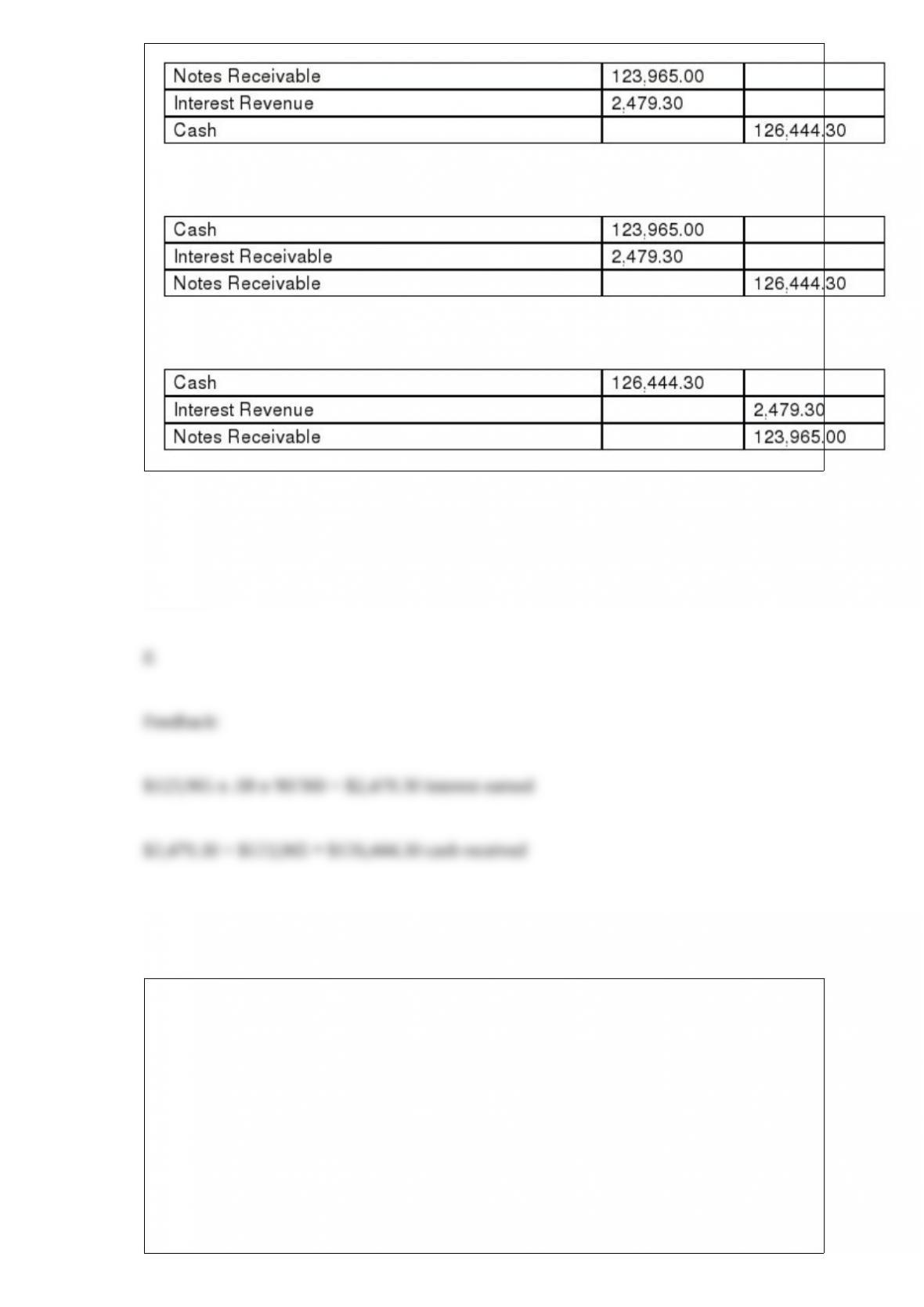

On August 1, 2013, Ace Corporation accepted a note receivable in place of an

outstanding accounts receivable in the amount of $123,965. The note is due in 90 days

and has an interest rate of 8%. What would be the appropriate journal entry to record

the receipt of cash at the maturity date?

A.

B.

C.

D.

E.

Answer:

A general journal is:

A. A ledger in which amounts are posted from a balance column account.

B. Not required if T-accounts are used.

C. A complete record of each transaction in the place from which transaction amounts

are posted to the ledger accounts.

D. Not necessary in electronic accounting systems.

E. A book of final entry because financial statements are prepared from it.

Answer:

K Company estimates that overhead costs for the next year will be $2,900,000 for

indirect labor and $800,000 for factory utilities. The company uses direct labor hours as

its overhead allocation base. If 80,000 direct labor hours are planned for this next year,

what is the companys plantwide overhead rate?

A. $.02 per direct labor hour.

B. $46.25 per direct labor hour.

C. $36.25 per direct labor hour.

D. $10 per direct labor hour.

E. $.10 per direct labor hour.

Answer:

Expenses that support the overall operations of a business and include the expenses

relating to accounting, human resource management, and financial management are

called:

A. Cost of goods sold.

B. Selling expenses.

C. Purchasing expenses.

D. General and administrative expenses.

E. Nonoperating activities.

Answer:

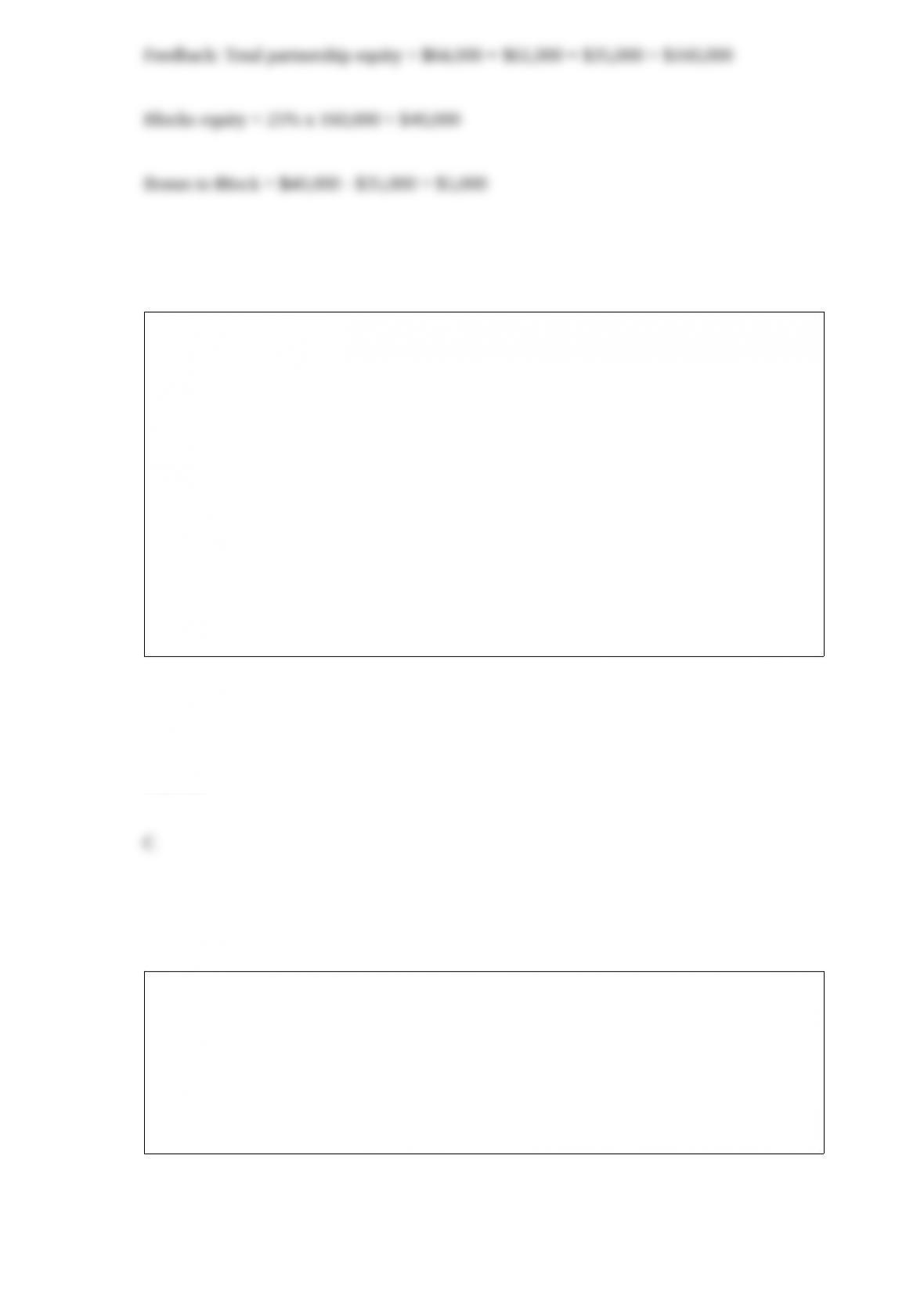

Groh and Jackson are partners. Groh’s capital balance in the partnership is $64,000 and

Jackson’s capital balance is $61,000. Groh and Jackson have agreed to share equally in

income or loss. Groh and Jackson agree to accept Block with a 25% interest. Block will

invest $35,000 in the partnership. The bonus that is granted to Block equals:

A. $5,000.

B. $2,500.

C. $6,667.

D. $3,333.

E. $0, because Block must actually grant a bonus to Groh and Jackson.

Answer:

A change in an accounting estimate is:

A. Reflected in past financial statements.

B. Reflected in future financial statements and also requires modification of past

statements.

C. A change in a calculated amount that is part of current and future financial

statements that results from new information or subsequent developments and from

better insight or improved judgment.

D. Not allowed under current accounting rules.

E. Considered an error in the financial statements.

Answer:

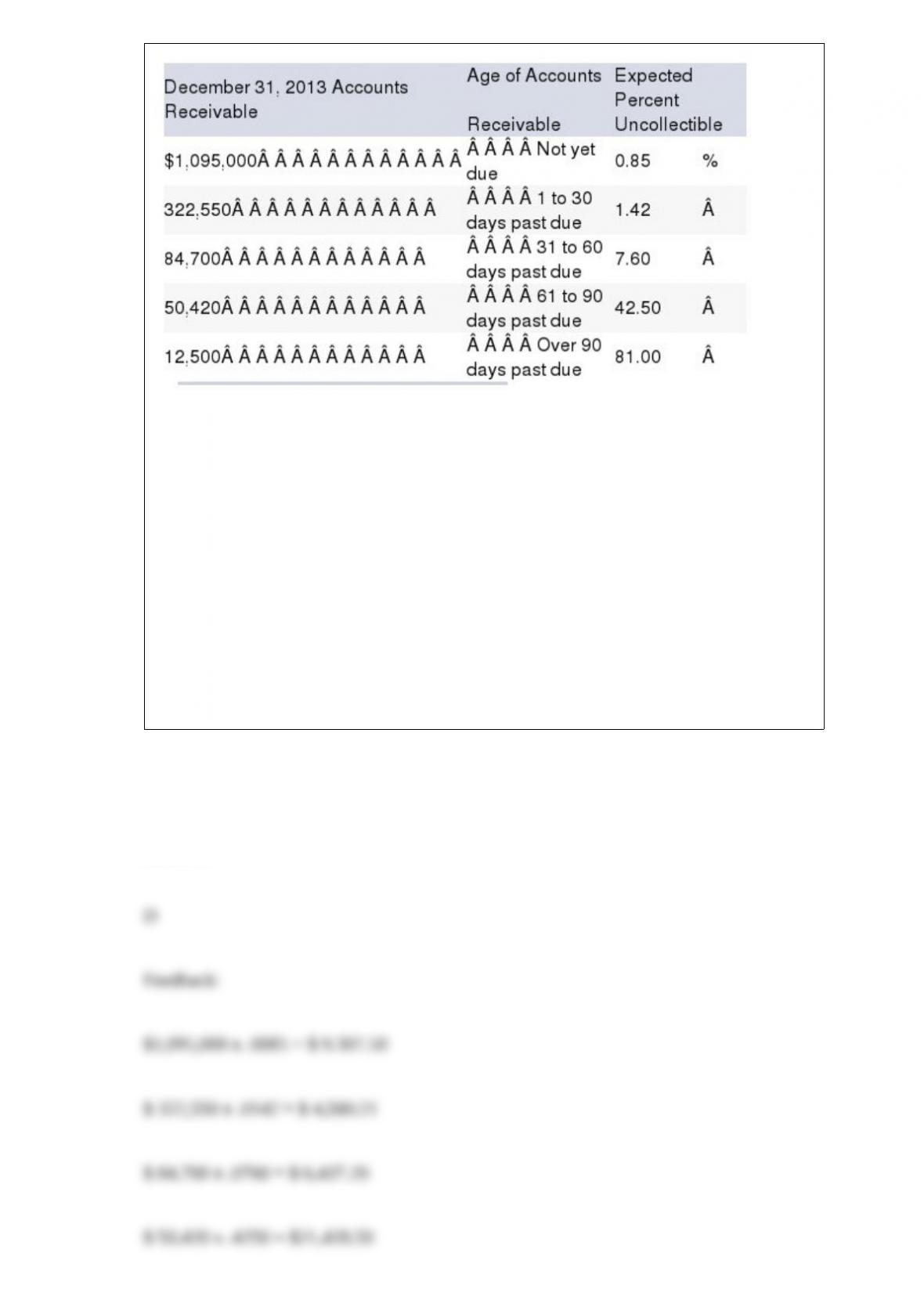

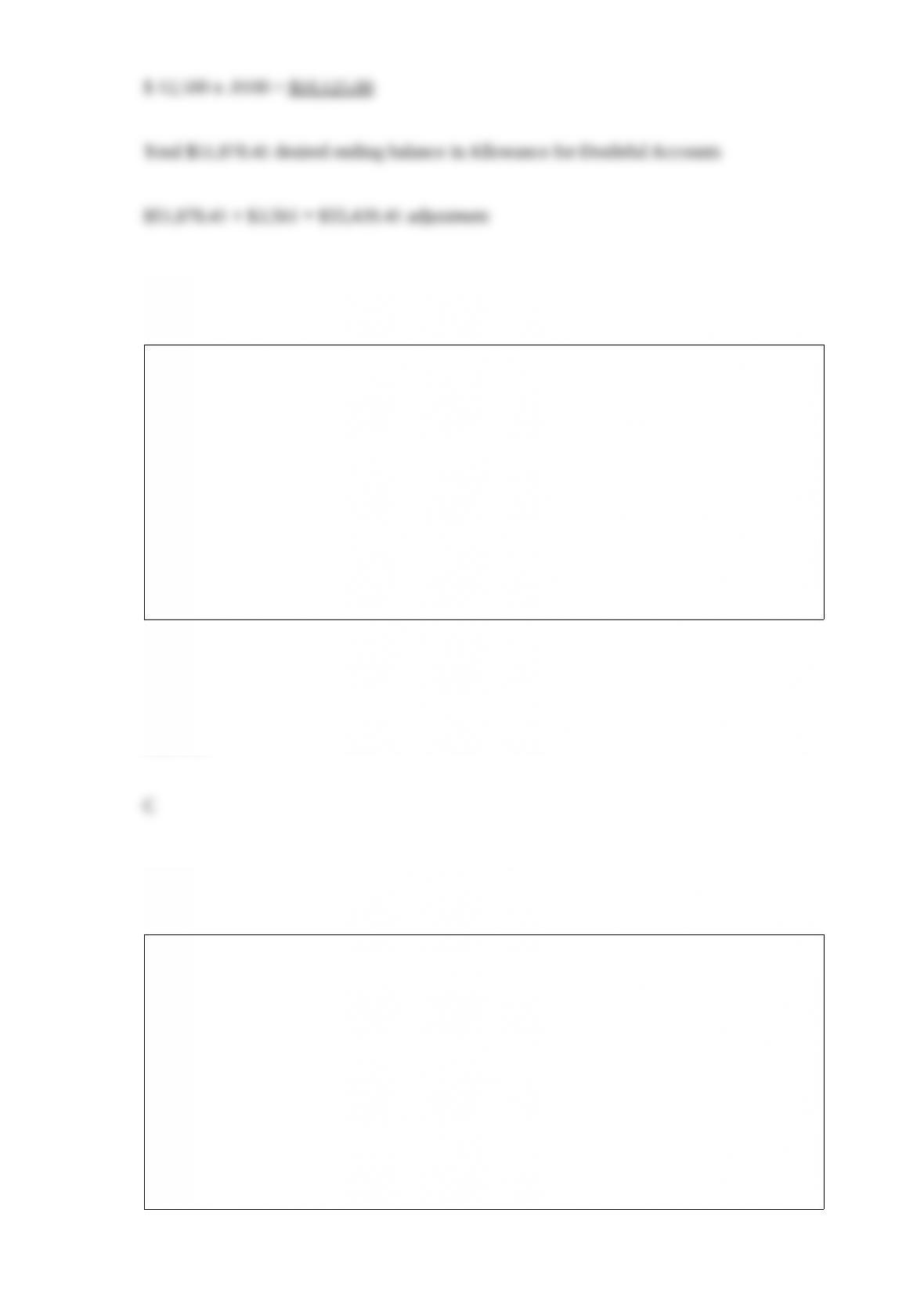

Chiller Company has credit sales of $5.60 million for year 2013. Chiller estimates that

1.32% of the credit sales will not be collected. Historically, 4% of outstanding accounts

receivable is uncollectible. On December 31, 2013, the companys Allowance for

Doubtful Accounts has an unadjusted debit balance of $3,561. Chiller prepares a

schedule of its December 31, 2010, accounts receivable by age. Based on past

experience, it estimates the percent of receivables in each age category that will become

uncollectible. This information is summarized here:

Assuming the company uses the aging of accounts receivable method, what is the

amount that Chiller will enter as the Bad Debt Expense in the December 31 adjusting

journal entry?

A. $59,045.80

B. $51,878.41

C. $48,317.41

D. $55,439.41

E. $66,167.80

Answer:

Which of the following does not require an adjusting entry at year-end?

A. Accrued interest on notes payable.

B. Supplies used during the period.

C. Cash investments by stockholders.

D. Accrued wages.

E. Expired portion of prepaid insurance.

Answer:

The main purpose of the wage bracket withholding table is to:

A. Compute social security withholding.

B. Compute Medicare withholding.

C. Compute federal income tax withholding.

D. Prepare the W-4.

E. Compute gross earnings.

Answer:

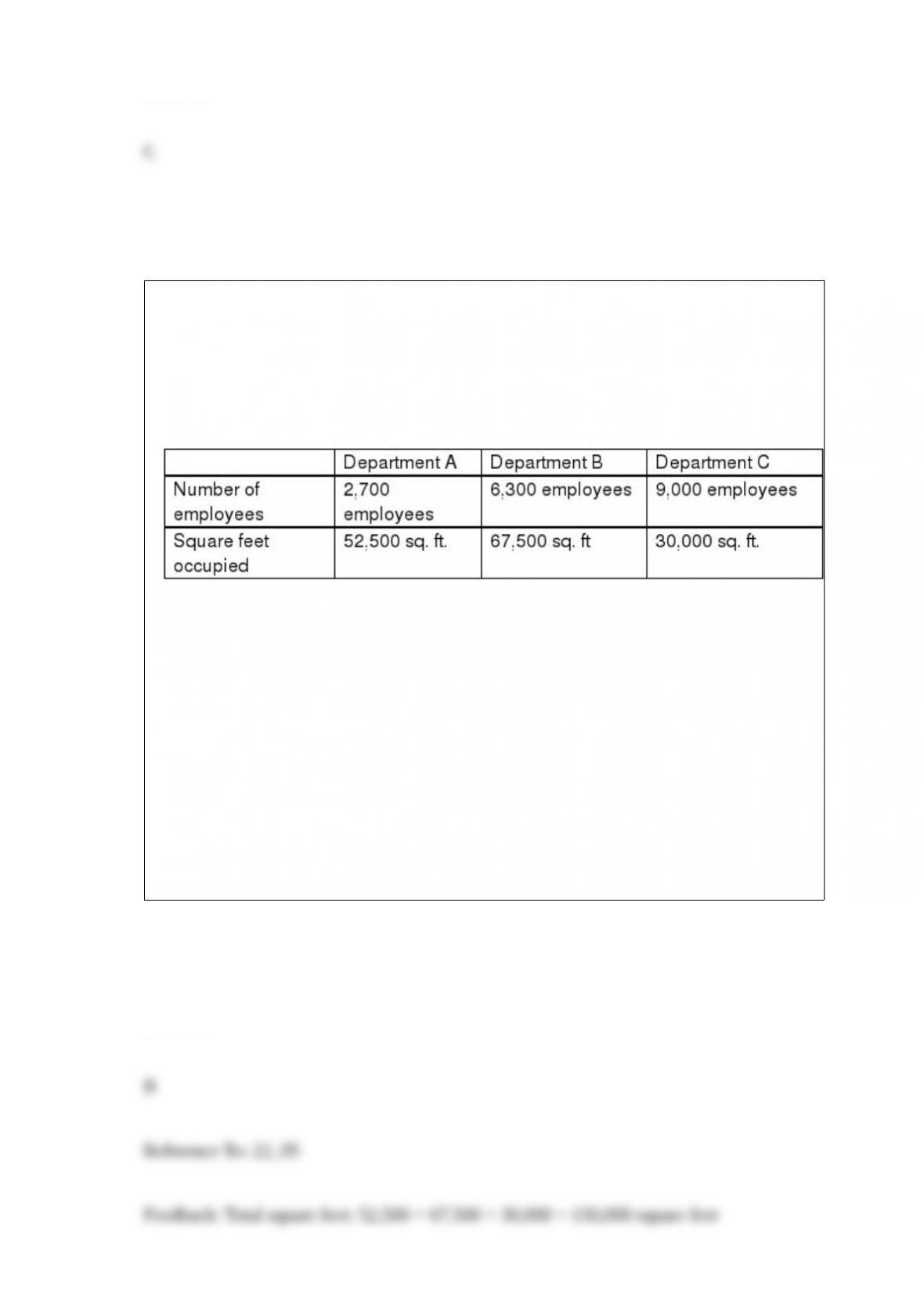

Reference: 22_05

Bookman Company has three operating departments: Department A, Department B, and

Department C. Administrative costs are allocated to operating departments based on the

number of workers and maintenance costs are allocated to operating departments based

on square footage occupied.

Assume that Bookman allocated $67,050 maintenance costs to Department B. Based on

the above data, determine the companys total maintenance costs.

A. $30,172

B. $149,000

C. $23,467

D. $191,571

E. $335,250

Answer:

Assume Moes Southwest Grill has a break-even point of 24,000 units. At this point,

total sales are $1,800,000 and total variable costs are $1,200,000. Compute total fixed

costs at the break-even point.

A. $1,800,000

B. $1,200,000

C. $3,000,000

D. $25

E. $ 600,000

Answer:

A company retires its bonds at 105. The carrying value of the bonds at the date of is

$103,745. The issuer’s journal entry to record the retirement will include a:

A. Debit to Premium on Bonds.

B. Credit to Premium on Bonds.

C. Debit to Discount on Bonds.

D. Credit to Gain on Bond Retirement.

E. Credit to Bonds Payable.

Answer:

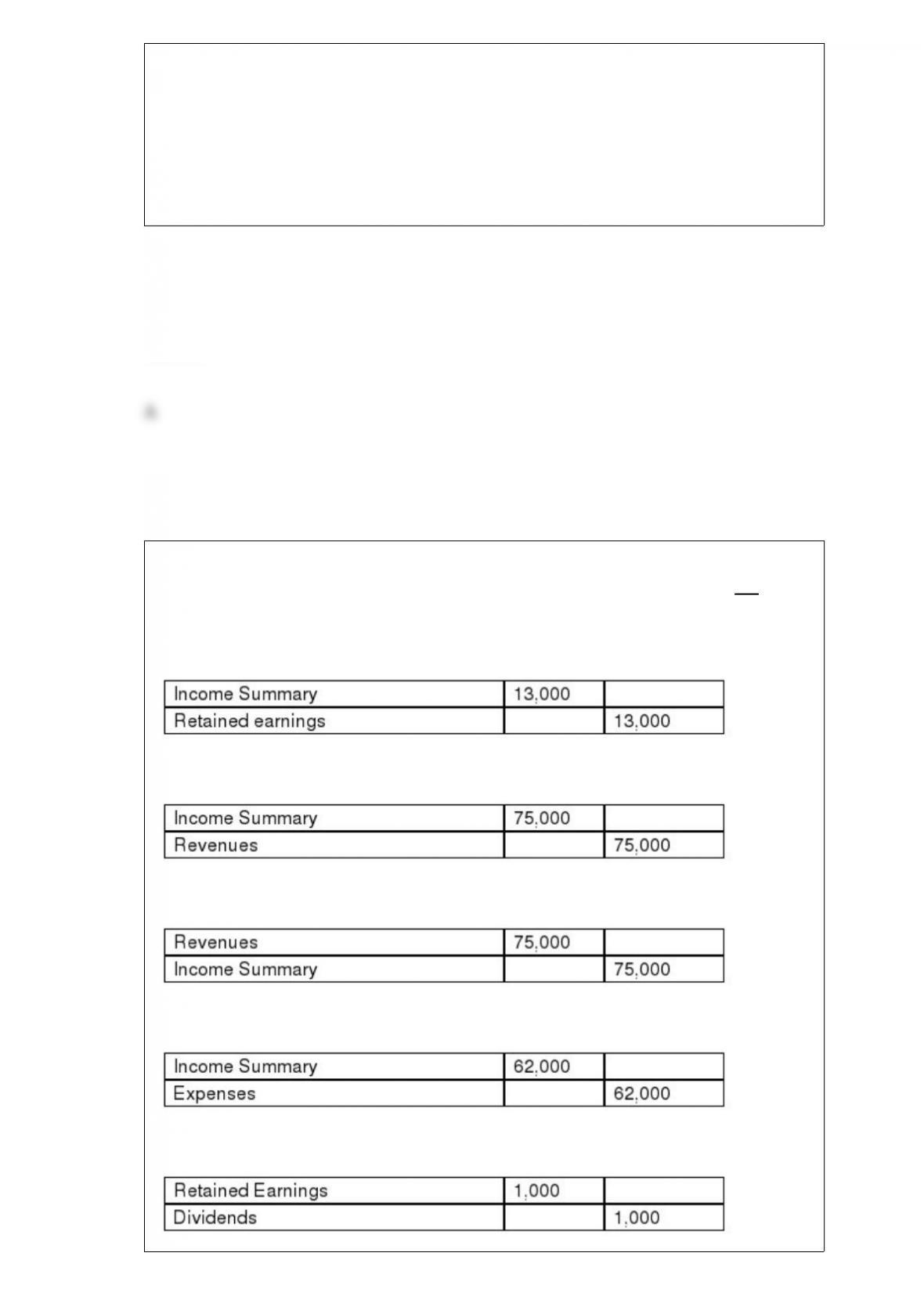

A company had revenues of $75,000 and expenses of $62,000 and paid $1,000

dividends during the accounting period. Which of the following entries could not be a

closing entry for this company?

A.

B.

C.

D.

E.

Answer:

RC Corp. uses a job order cost accounting system. During the month of April, the

following events occurred:

A. Purchased raw materials on credit, $32,000.

B. Raw materials requisitioned: $25,800 as direct materials (Job 1:$4,200, Job 2:

$7,500, Job 3: $3,600 and Job 4: $10,500) and $10,500 indirect materials.

C. Paid factory payroll for the month totaling $37,700 which includes $8,200 indirect

labor.

D. Assigned the factory payroll to jobs and overhead. (Job 1:$7,000, Job 2: $9,800, Job

3: $3,000 and Job 4: $9,700)

E. Overhead was assigned at a rate of 50% of direct labor cost.

Determine the total cost of each job.

Answer:

A comprehensive or overall formal plan for a business that includes specific plans for

expected sales, the units of product to be produced, the merchandise or materials to be

purchased, the expense to be incurred, the long-term assets to be purchased, and the

amounts of cash to be borrowed or loans to be repaid, as well as a budgeted income

statement and balance sheet, is called a:

A. Master budget.

B. Cash budget.

C. Capital expenditures budget.

D. Rolling budget.

E. Production budget.

Answer:

Marian Mosely is the owner of Mosely Accounting Services. Which accounting

assumption requires Marian to keep her personal financial information separate from

the financial information of Mosely Accounting Services?

A. Monetary unit assumption

B. Going-concern assumption

C. Cost assumption

D. Business entity assumption

E. Full disclosure assumption

Answer:

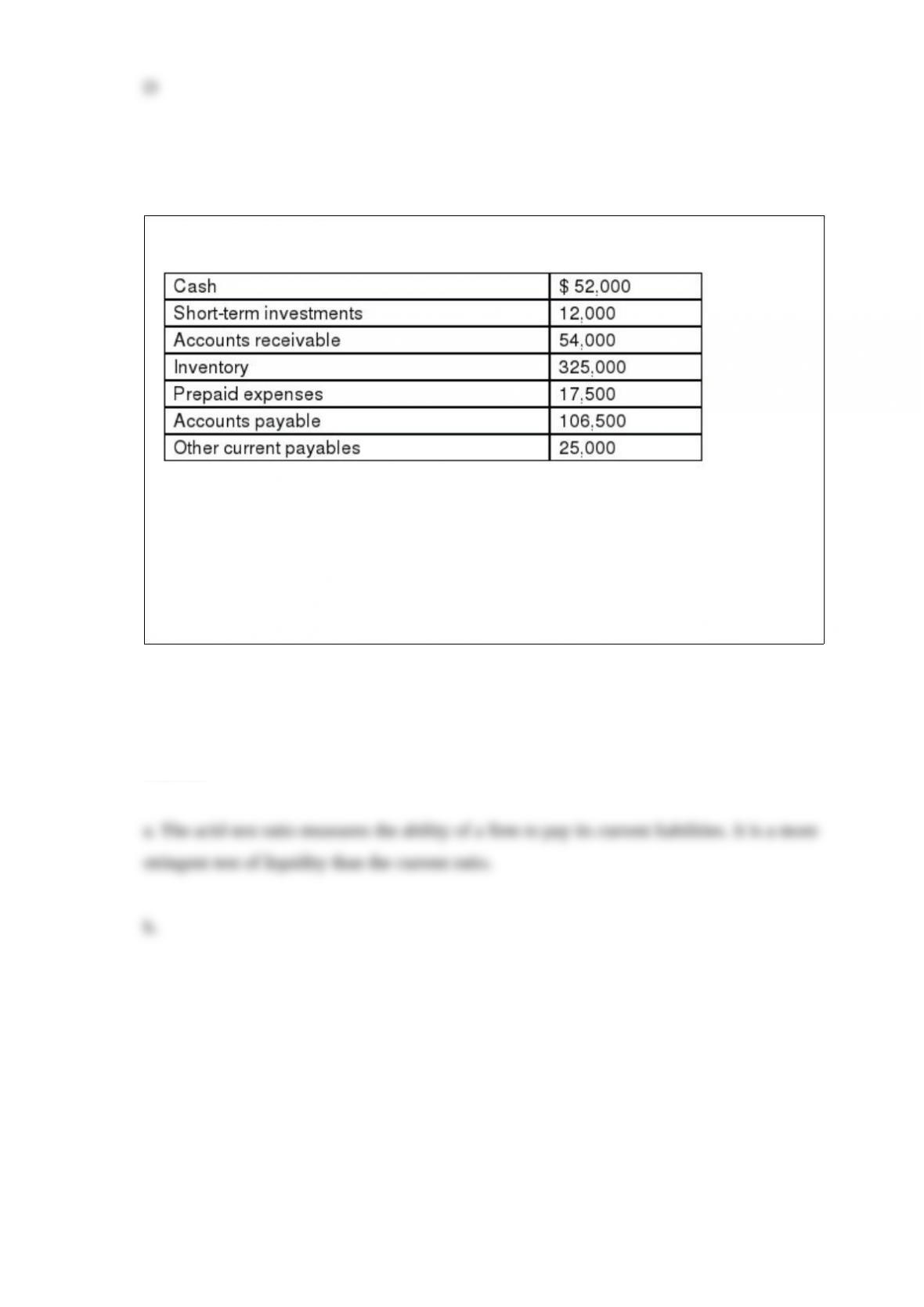

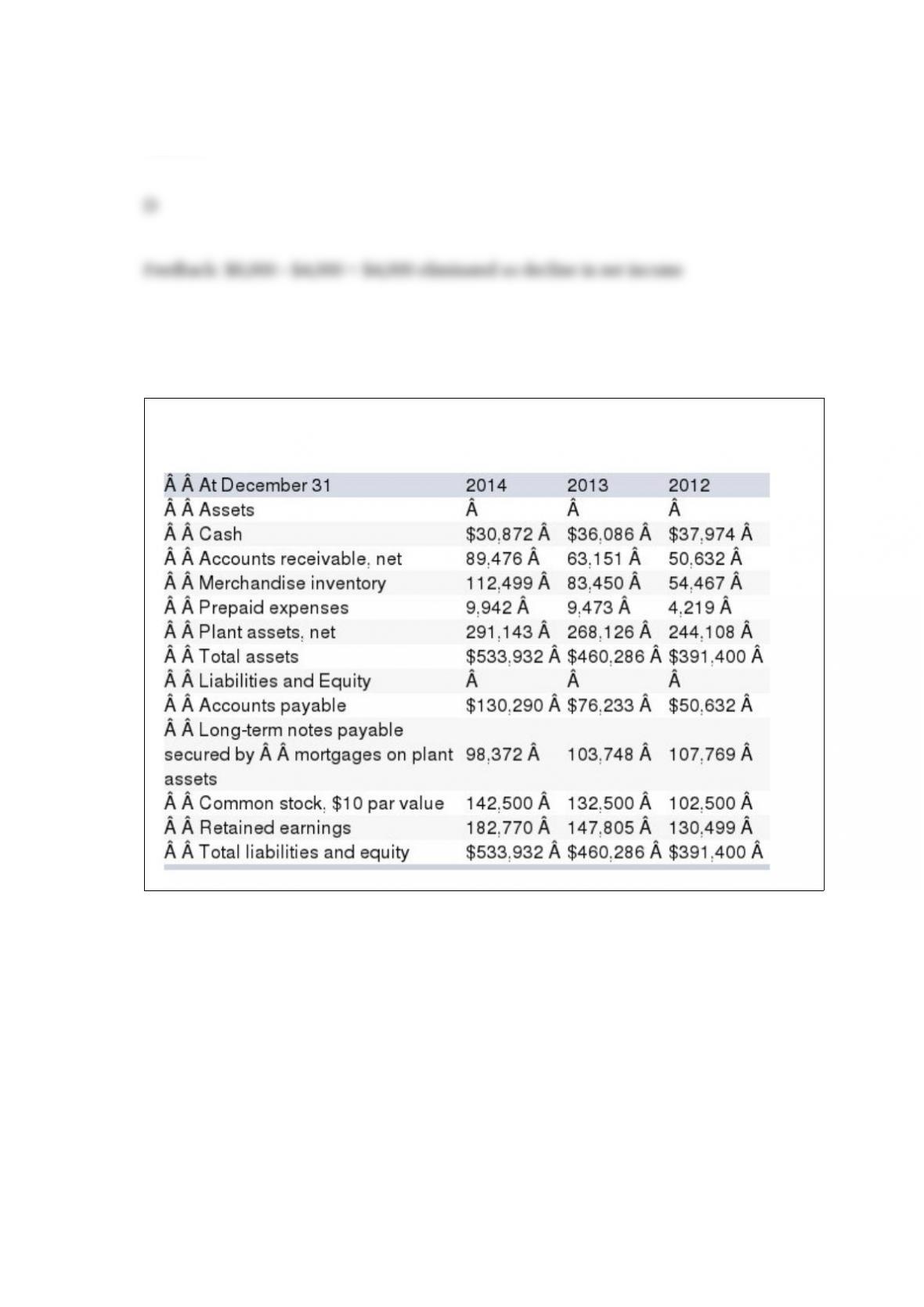

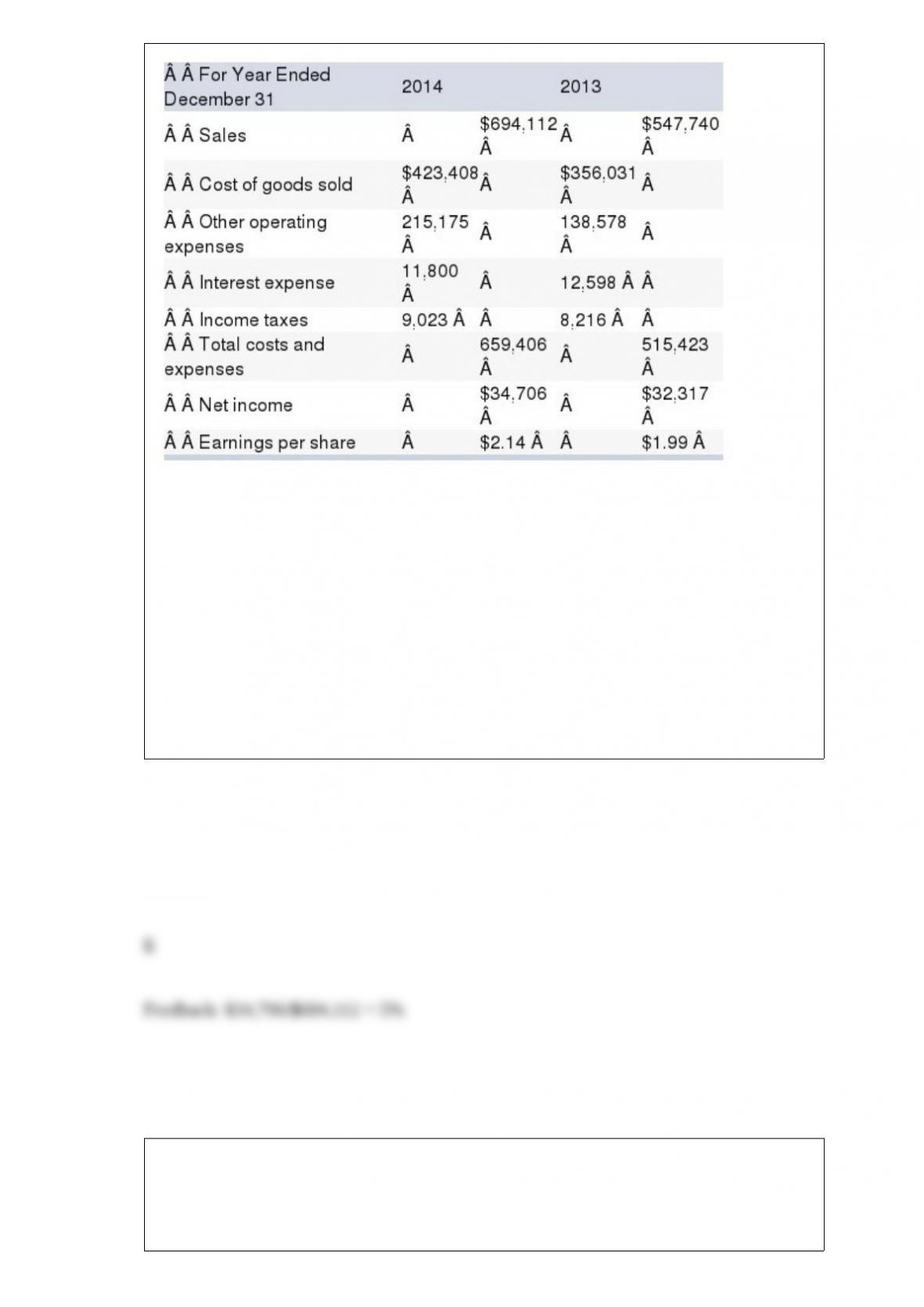

A company reported the following year-end information:

Required:

a. Explain the purpose of the acid-test ratio.

b. Calculate the acid-test ratio for this company.

c. What does the acid-test ratio reveal about this company?

Answer:

A method of assigning overhead costs to a product using a single overhead rate is:

A. Plantwide overhead rate method.

B. Cost pool overhead rate method.

C. Departmental overhead rate method.

D. Activity-based costing.

E. Overhead cost allocation method.

Answer:

Owners of preferred stock often do not have:

A. Ownership rights to assets of the corporation.

B. Voting rights.

C. Preference to dividends.

D. The right to sell their stock on the open market.

E. Preference to assets at liquidation.

Answer:

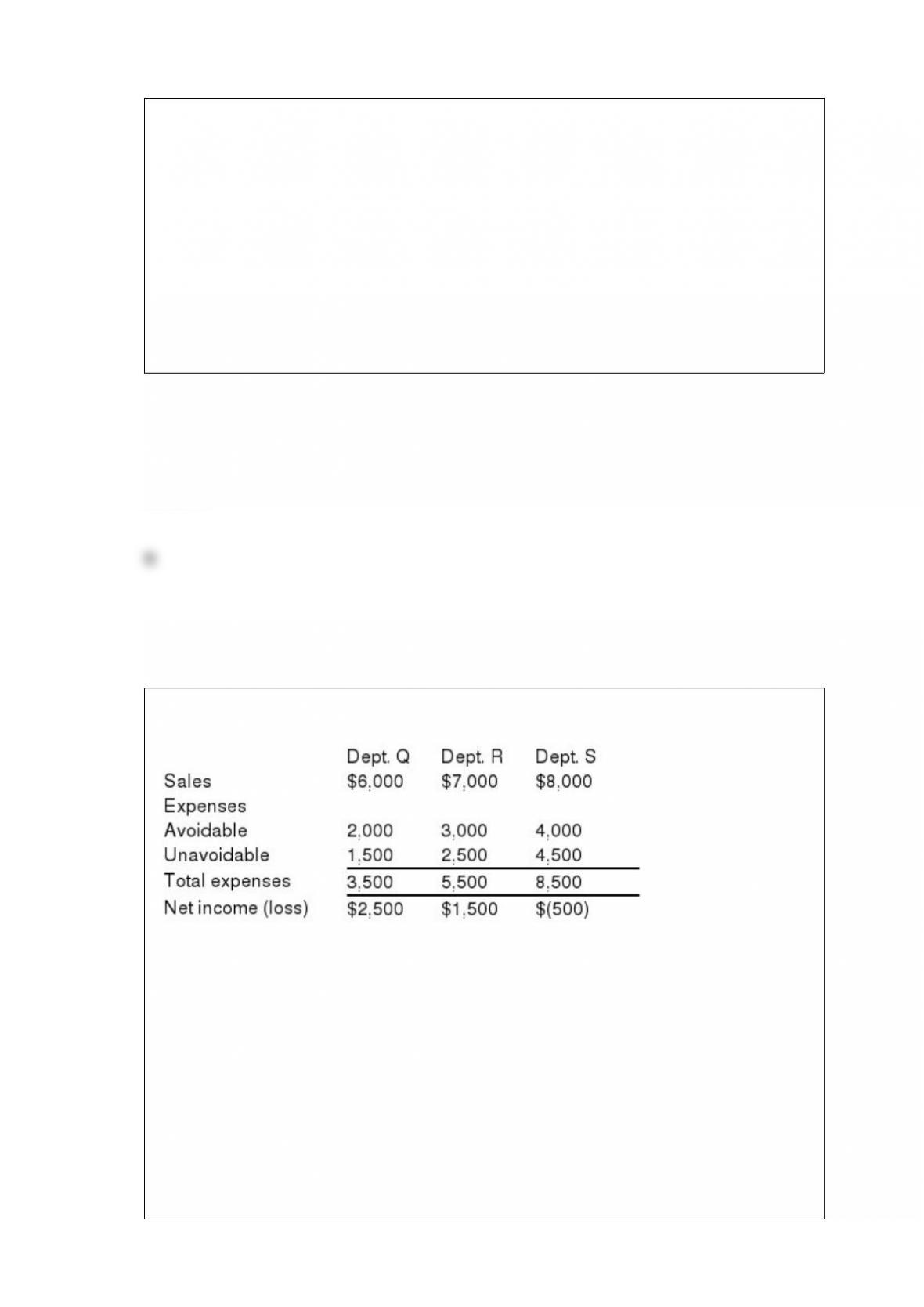

A company expects its three departments to yield the following income for next year:

Compute the change to the companys total net income if Dept. S is eliminated.

A. $500 increase

B. $500 decrease

C. $4,000 increase

D. $4,000 decrease

E. $3,500 decrease

Answer:

A companys balance sheet and income statement accounts follow:

What is the companys profit margin ratio for 2014?

A. 65%

B. 12%

C. 3.7%

D. 5.9%

E. 5.0%

Answer:

The time value of money concept:

A. Means that a dollar today is worth less than a dollar tomorrow.

B. Means that a dollar tomorrow is worth more than a dollar today.

C. Means that a dollar today is worth more than a dollar tomorrow.

D. Means that Time is money.

E. Does not involve the concept of compound interest.

Answer:

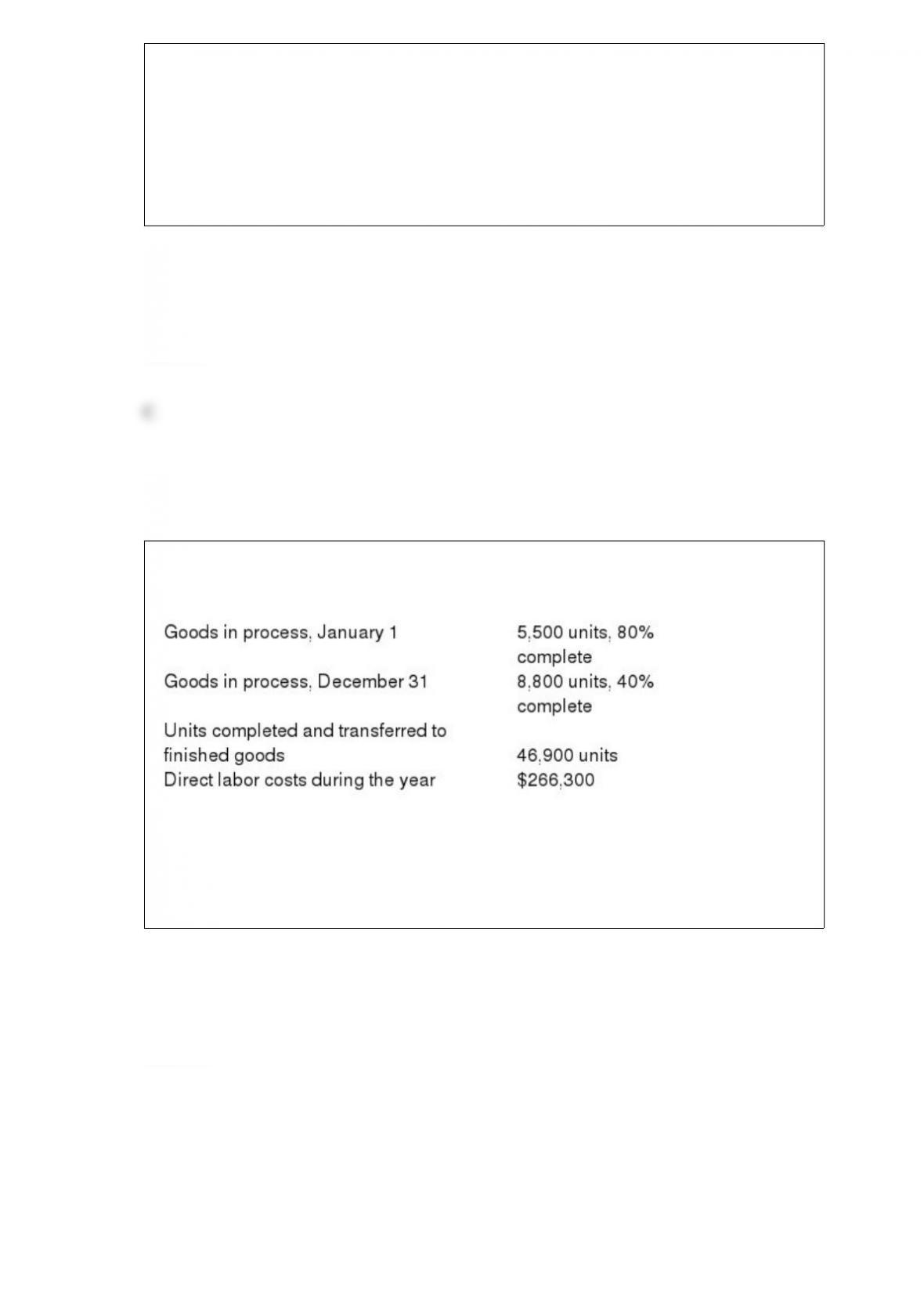

A company uses a process cost accounting system. The following information is

available regarding direct labor for the current year:

(a) Calculate the equivalent units of production for direct labor for the year using FIFO.

(b) Calculate the average cost per equivalent unit for direct labor (round to the nearest

cent).

Answer:

Which of the following accounting principles dictates when expenses are recognized?

A. Revenue recognition principle

B. Monetary unit principle

C. Business entity principle

D. Matching principle

E. Full disclosure principle

Answer:

The ability to generate future revenues and meet long-term obligations is referred to

as:

A. Liquidity and efficiency.

B. Solvency.

C. Profitability.

D. Market prospects.

E. Creditworthiness.

Answer:

Prior to June 1, a company has never had any treasury stock transactions. The company

repurchased 100 shares of its common stock on June 1 for $5,000. On July 1, it reissued

50 of these shares at $52 per share. On August 1, it reissued the remaining treasury

shares at $49 per share. What is the balance in the Contributed Capital, Treasury Stock,

account on August 2?

A. $5,050

B. $2,600

C. $100

D. $50

E. $0

Answer:

Ecology Co. sells a biodegradable product called Dissol and has predicted the following

sales for the first four months of the current year:

Ending inventory for each month should be 20% of the next month’s sales, and the

December 31 inventory is consistent with that policy. How many units should be

purchased in February?

A. 1,860

B. 1,900

C. 1,940

D. 1,980

E. 2,320

Answer:

A cost that cannot be avoided or changed because it arises from a past decision, and is

irrelevant to future decisions, is called a(n):

A. Uncontrollable cost

B. Incremental cost

C. Opportunity cost

D. Out-of-pocket cost

E. Sunk cost

Answer:

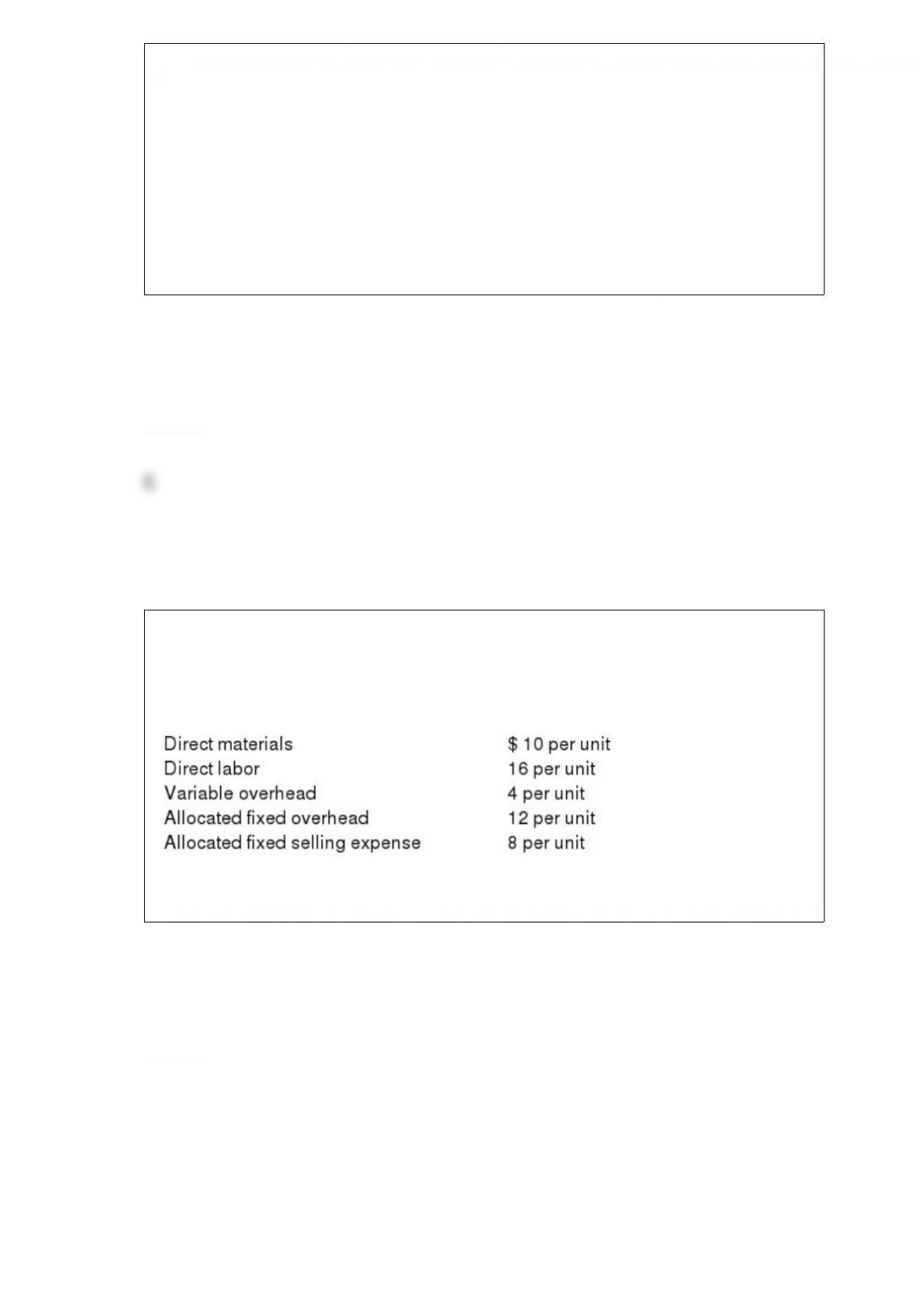

A company has just received a special, one-time order for 1,000 units. Producing the

order will have no effect on the production and sales of other units. The buyer’s name

will be stamped on each unit, at a total cost of $2,000. Normal cost data, excluding

stamping, follows:

What selling price per unit will this company require to earn $3,000 on the order?

Answer:

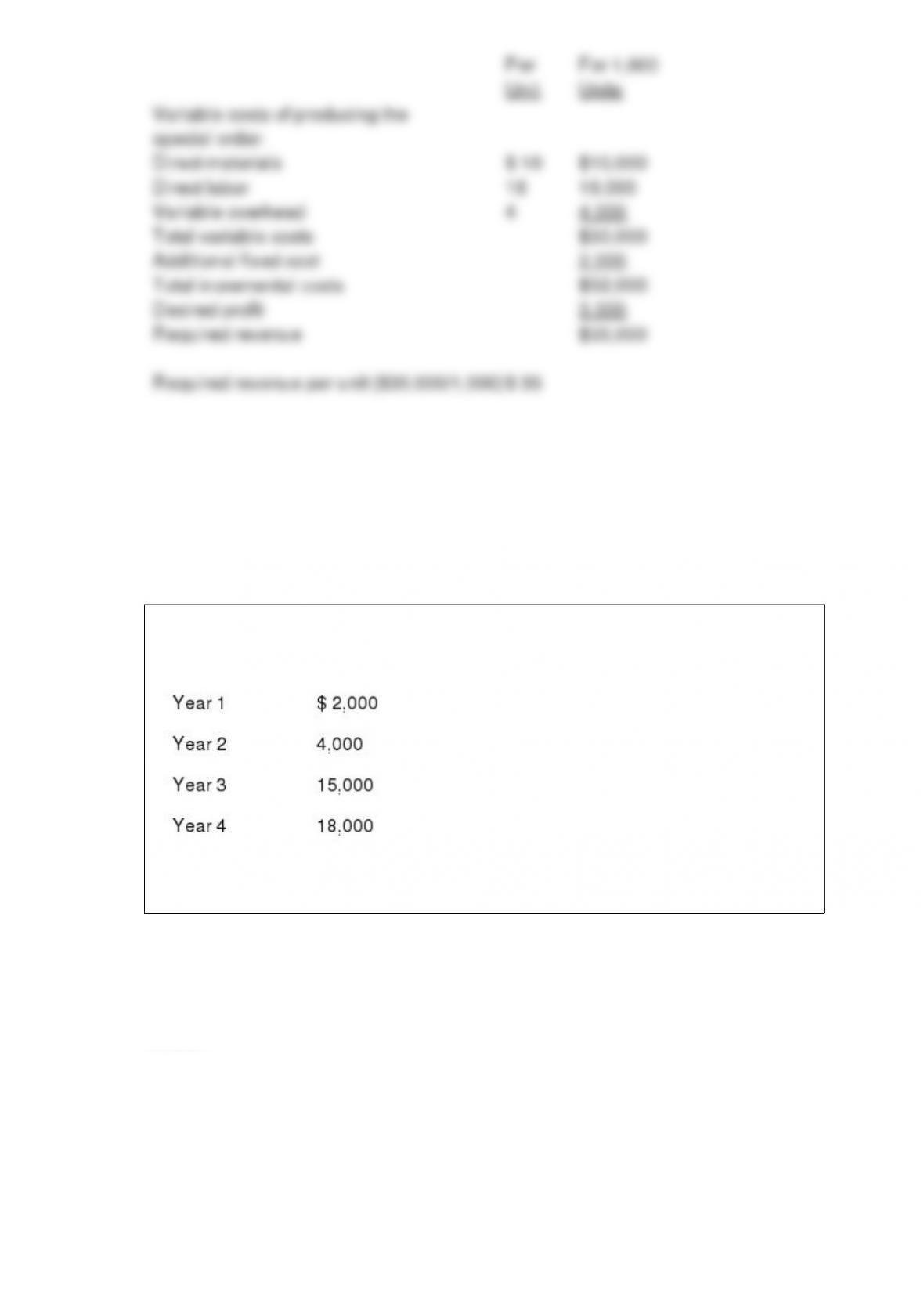

A company is considering a proposal to invest $22,000 in a project that would provide

the following net cash flows:

Compute the project’s payback period.

Answer:

Describe source documents and their purpose.

Answer:

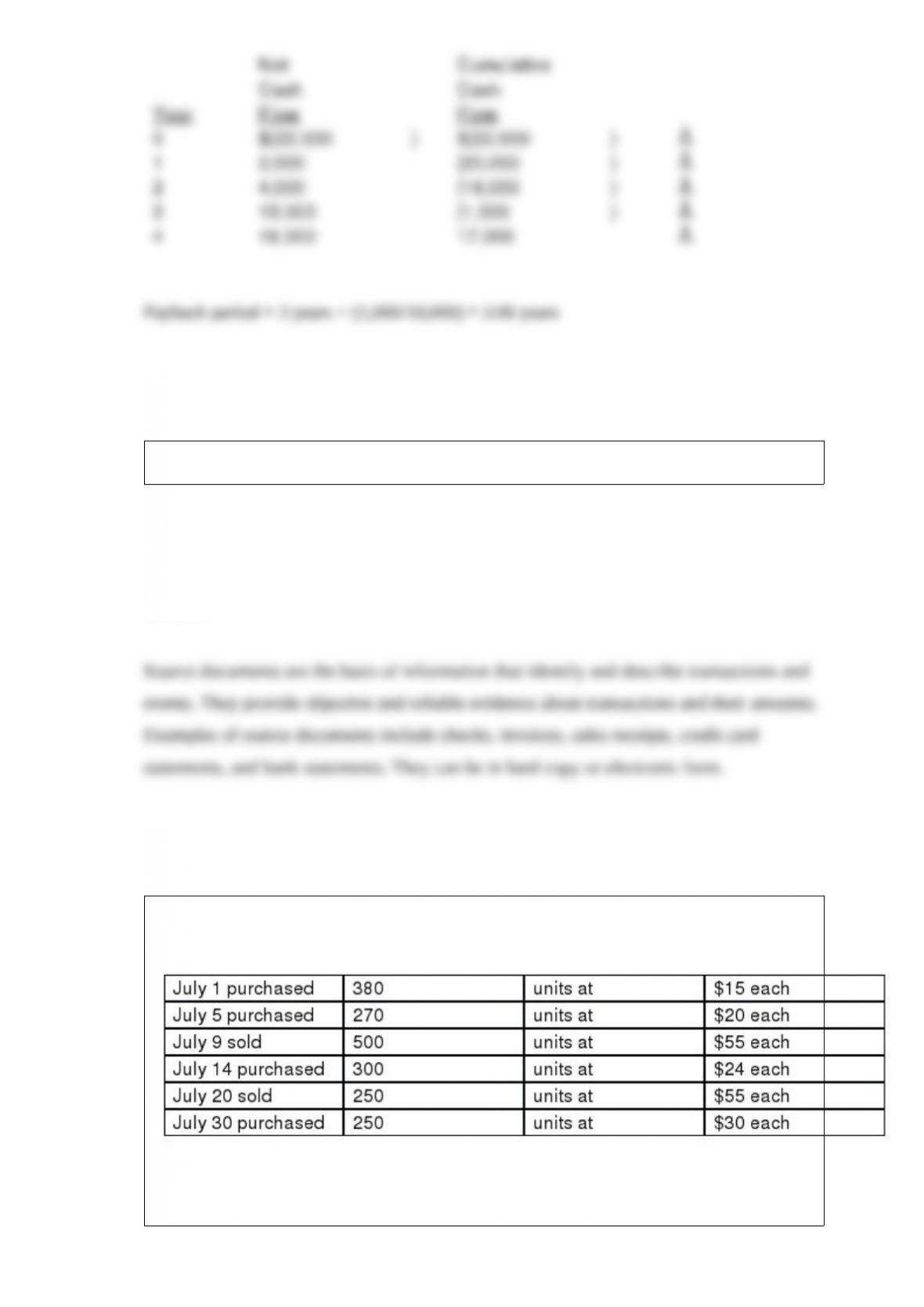

A company made the following merchandise purchases and sales during the month of

July:

There was no beginning inventory. If the company uses the first-in, first-out perpetual

inventory method, what would be the cost of the ending inventory?

Answer:

Answer:

Explain (in detail) how to compute each of the following depreciation methods:

straight-line, units-of-production, and double-declining-balance.

Answer:

A _____________________________ is a part of a company’s operations that serves a

particular line of business or class of customers.

Answer:

A capital budgeting method that considers how quickly a project recovers costs is

known as ______________________. An enhancement to this method that considers

the time value of money is called _________________.

Answer:

How are unfavorable variances recorded?

Answer:

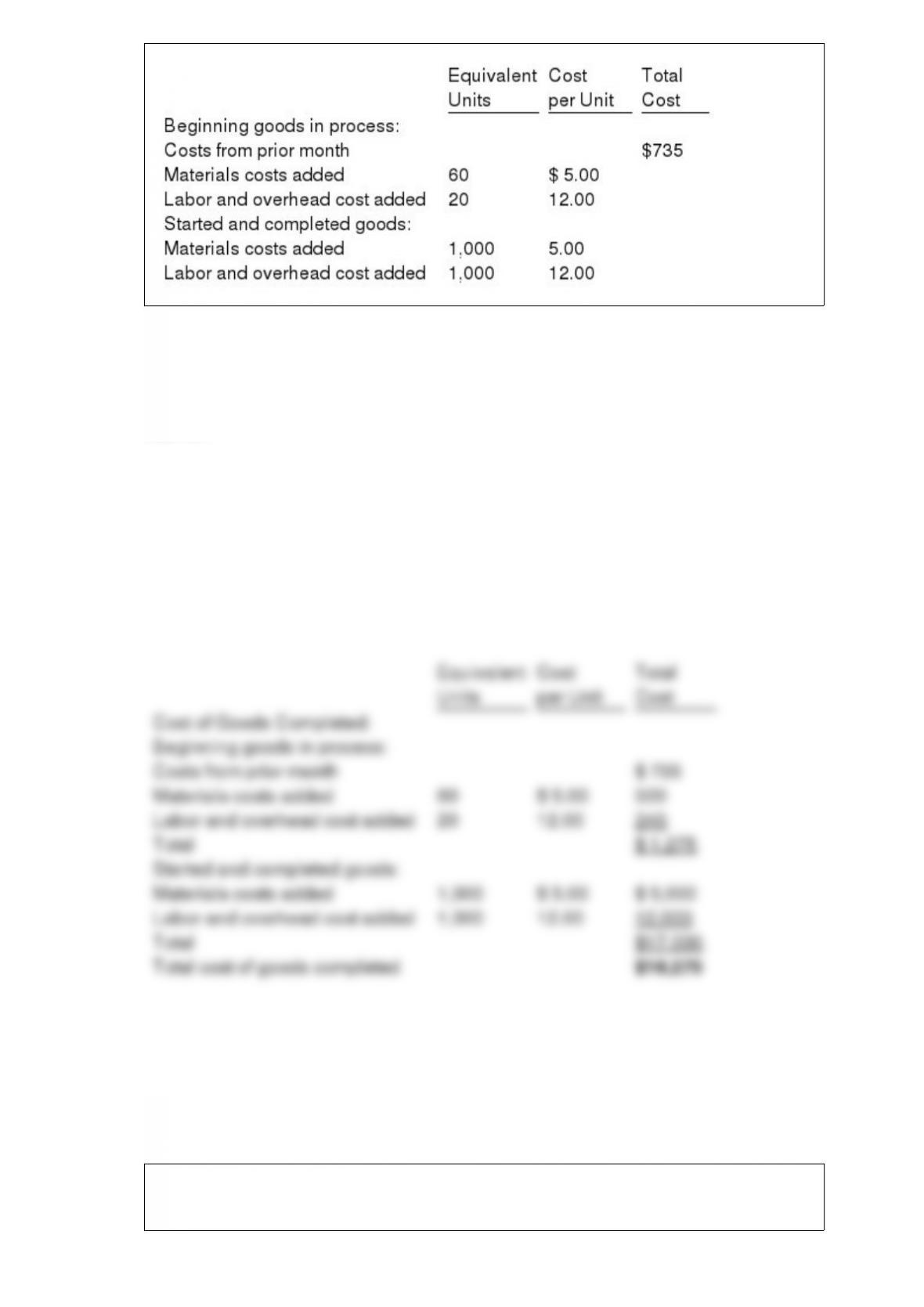

Assuming the FIFO inventory valuation method, use the following information to

determine the cost of the goods completed during the current reporting period:

Answer:

______________________ are required at the end of the accounting period because

certain internal transactions and events remain unrecorded.

Answer:

Given the following information, determine the cost of ending inventory at November

30 using the FIFO perpetual inventory method.

November 3: 15 units were purchased at $8 per unit.

November 11: 18 units were purchased at $9.50 per unit.

November 15: 15 units were sold at $45 per unit.

November 18: 30 units were purchased at $10.75 per unit.

November 30: 20 units were sold at $55 per unit.

Answer:

In a constrained resource situation, a company should maximize contribution margin

per _______________________________.

Answer:

There are three major subgroups of the master budget. These are

________________________, ___________________, and

_______________________.

Answer:

The following information refers to Annie’s Attic and its competitors in the antiques

business:

Required:

Comment on the relative liquidity positions of these companies.

Answer:

On January 10, a corporation purchased 5,000 shares of its own common stock at

$17.50 per share. On August 4, a total of 1,000 treasury shares were sold at $19.00 per

share. These are the only treasury stock transactions ever made by the corporation.

Prepare the journal entries required on January 10 and August 4.

Answer:

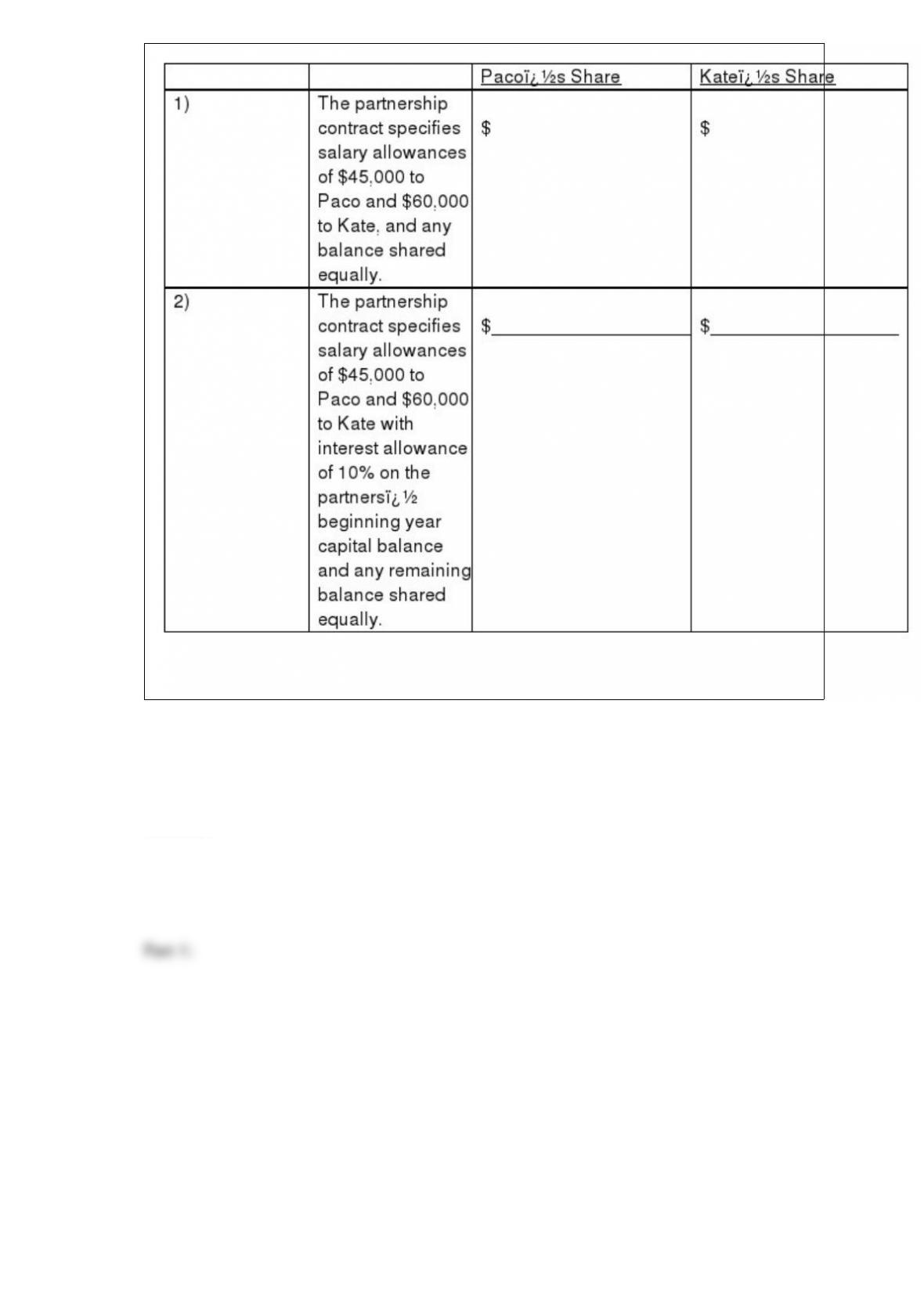

Paco and Kate invested $99,000 and $126,000, respectively, in a partnership they

began one year ago. Assuming the partnership earned $120,000 during the current year,

compute the share of the net income each partner should receive under each of these

independent assumptions.

Answer:

Vacation benefits are a type of _______________ liability.

Answer:

________________________ is the number of shares that a corporation’s charter

allows it to sell.

Answer: