The list of names and reference numbers that the company will use when accounting for

transactions is called the Chart of Accounts.

Answer:

In general, the cash flow from operating activities is considered by many to be the most

important component of the statement of cash flows.

Answer:

Which of the following is notTRUE about the unadjusted trial balance?

A. An unadjusted trial balance may only include a preliminary amount for income tax

expense.

B. An unadjusted trial balance might balance even if there is a mistake.

C. An unadjusted trial balance does not yet include end-of-the-accounting period

adjustments.

D. An unadjusted trial balance is part of the financial statements issued to external

decision makers.

Answer:

The beginning credit balance in the allowance for doubtful accounts is $12,656 and the

ending credit balance is $14,348. If bad debt expense was $3,879, which of the

following statements isTRUE?

A. The allowance account was retroactively debited $2,187 for additional bad debts that

became apparent in a future time period.

B. The allowance account was debited $2,187 for write-offs of actual bad debts.

C. The allowance account was credited $2,187 for recoveries of bad debts.

D. The allowance account was credited $2,187 for the difference between the percent of

credit sales method and the aging of accounts receivable method.

Answer:

The Sarbanes-Oxley Act (SOX) grants legal protection to ‘whistle-blowers.’

Answer:

If a company failed to record depreciation expense on equipment for a period, the

financial statements would show total assets overstated and total stockholders’ equity

understated on the balance sheet.

Answer:

The Sarbanes-Oxley Act (SOX) requires the company’s board of directors to establish

an audit committee of independent directors to oversee the financial matters of the

company.

Answer:

A company has a current ratio of 2.0 and a quick ratio of 1.5. Assume the company then

paid previously declared dividends in the amount of $20,000. Which of the following

statements isTRUE?

A. The current ratio will decrease and the quick ratio will decrease.

B. The current ratio will decrease and the quick ratio will not change.

C. The current ratio and the quick ratio will not change.

D. The current ratio will increase and the quick ratio will increase.

Answer:

Goods on consignment are goods shipped by the owner to another company that holds

the goods and sells them for the owner.

Answer:

Which of the following statements isTRUE?

A. FIFO results in a lower net income than LIFO when costs are increasing.

B. LIFO results in a higher net income than FIFO when costs are increasing.

C. LIFO results in a higher net income than FIFO when costs are decreasing.

D. LIFO results in the same net income as FIFO when costs are increasing.

Answer:

Which of the following isTRUE about the format of financial statements?

A. A double underline is drawn below the subtotal for total liabilities on the balance

sheet.

B. Dollar signs are omitted if the heading states that amounts are reported in U.S.

dollars.

C. Dividends are reported in parentheses on the statement of retained earnings.

D. The heading of each financial statement indicates who, when, and what in that

particular order.

Answer:

On a bank statement, deposits are listed as debits and cleared checks are listed as

credits.

Answer:

Which of the following statements isTRUE?

A. Retained earnings is a permanent account, while income statement accounts are

temporary.

B. Retained earnings and income statement accounts are all temporary accounts.

C. Retained earnings and income statement accounts are all permanent accounts.

D. Retained earnings is a temporary account, while income statement accounts are

permanent accounts.

Answer:

Which of the following statements isTRUE?

A. Valuing inventory under LIFO may produce different results depending on whether a

perpetual or periodic inventory system is used.

B. Valuing inventory under the weighted average cost method always produces the

same results using either a perpetual or periodic inventory system.

C. Valuing inventory under FIFO may produce different results depending on whether a

perpetual or periodic inventory system is used.

D. Using the specific identification method will produce different results depending on

whether perpetual or periodic inventory system is used.

Answer:

In any given industry, companies are entirely consistent in the account titles they use on

financial statements.

Answer:

Revenue is reported on the income statement only if cash was received at the point of

sale.

Answer:

General Motors (GM) signs a new labor agreement that its workers will receive a 5%

wage increase next year. This is considered a transaction that affects GM’s financial

statements in the current year.

Answer:

If the receivables turnover ratio rises significantly, the increase may be a signal that the

company is extending credit to high-risk borrowers or allowing an overly generous

repayment schedule.

Answer:

A merchandising company’s operating cycle begins with the sale of merchandise and

ends with the cash collection from sales.

Answer:

Which of the following statements regarding debits and credits is alwaysTRUE?

A. Debits decrease accounts while credits increase them.

B. The total value of all debits recorded in the ledger must equal the total value of all

credits recorded in the ledger.

C. The total value of all debits to a particular account must equal the total value of all

credits to that account.

D. A debit balance of $500 in the cash account means that cash receipts exceeded cash

payments by $500.

Answer:

Which of the following is aTRUE statement?

A. Revenue accounts are a subset of assets, and expense accounts are a subset of

liabilities.

B. Both revenue accounts and expense accounts are subsets of contributed capital.

C. Both revenue accounts and expense accounts are subsets of retained earnings.

D. Revenue accounts are a subset of cash, and expense accounts are a subset of

accounts payable.

Answer:

There are no differences between GAAP and IFRS rules of accounting for tangible and

intangible assets.

Answer:

The direct write-off method for uncollectible accounts is not allowed by either GAAP

or IFRS, but is required by the IRS.

Answer:

The normal balance of an account is on the same side that increases the account.

Answer:

Preferred stock is generally classified as stockholders’ equity under both GAAP and

IFRS.

Answer:

A company failed to make an accrual adjustment for interest owed on a short-term bank

loan. Which of the following statements isTRUE about how this will affect the financial

ratios?

A. Net profit margin ratio will be understated and debt-to-assets ratio will be overstated.

B. Net profit margin ratio and debt-to-assets ratios will be unaffected.

C. Net profit margin ratio will be overstated and debt-to-assets ratio will be understated.

D. Net profit margin ratio will be unaffected and debt-to-assets ratio will be overstated.

Answer:

Which of the following statements isTRUE?

A. The debt-to-assets ratio requires only information found on the balance sheet.

B. The net profit margin ratio requires only information found on the balance sheet.

C. The asset turnover ratio requires only information found on the income statement.

D. The debt-to-assets ratio and the asset turnover ratio are used to evaluate profitability

of the company.

Answer:

B. Darin Company issued stock to investors and received $50,000. Choose theTRUE

statement.

A. This is an example of a cash inflow from an investing activity.

B. The journal entry to record this transaction will include a credit to cash.

C. This is an example of a cash outflow from a financing activity.

D. The journal entry to record this transaction will include a credit to contributed

capital.

Answer:

The receivables turnover ratio is calculated using the total net receivables.

Answer:

A retail chain sells 100 designer sheet sets for $199.99 a set; these sheet sets cost the

company $69.95 a set to buy. The company also sells 1,000 basic sheet sets for $49.99 a

set; these sheet sets cost the company $24.99 to buy. Other operating expenses total

$10,000. Which of the following statements isTRUE?

A. The company’s net income is $38,004.

B. Rounded to the nearest whole number, the gross profit percentage is 65% on the

designer sheets and 50% on the basic sheets.

C. The company’s total gross profit is $28,004.

D. The total sales for the period are $48,004.

Answer:

If a company uses the direct method of calculating cash flows from operating activities,

it must adjust net income for gains or losses when selling property, plant, and

equipment.

Answer:

Dividing up the continuing life of a company into shorter periods is called the time

period assumption.

Answer:

The Buddy Burger Corporation has $3.5 million in long-lived assets and has an

accumulated depreciation account of $1.1 million. Which of the following statements

isTRUE?

A. The book value of long-lived assets is $2.4 million.

B. The market value of long-lived assets is $3.5 million.

C. The carrying value of long-lived assets is $3.5 million.

D. The resale value of long-lived assets is $2.4 million.

Answer:

Specific identification is the best inventory costing method because it is least subject to

manipulation by unscrupulous managers.

Answer:

If a company is to succeed over the long-term, a positive cash flow from operating

activities is necessary.

Answer:

A company has earnings per share of $1.20, it paid a dividend of $.50 per share, and the

market price of the company’s stock is $45 per share. The price/earnings ratio is closest

to:

A. 37.50.

B. 64.29.

C. 2.40.

D. 2.0.

Answer:

Which of the following would not be reported on the Income Statement?

A. Utilities expense in the amount of a bill received for utilities used during the current

period but unpaid as of the end of the period.

B. Rent expense in the amount of rent paid during the period for use of a storage facility

in the current period.

C. Revenue in the amount of services provided to customers who promise to pay in the

next period.

D. Cost of land, paid in cash, and purchased for future use.

Answer:

In the interest formula, the interest rate is on a(n) _____ basis; therefore, the time

variable must reflect how many _____ out of _____ in the interest period.

A. monthly, months, 6

B. annual, years, 1

C. monthly, months, 12

D. annual, months, 12

Answer:

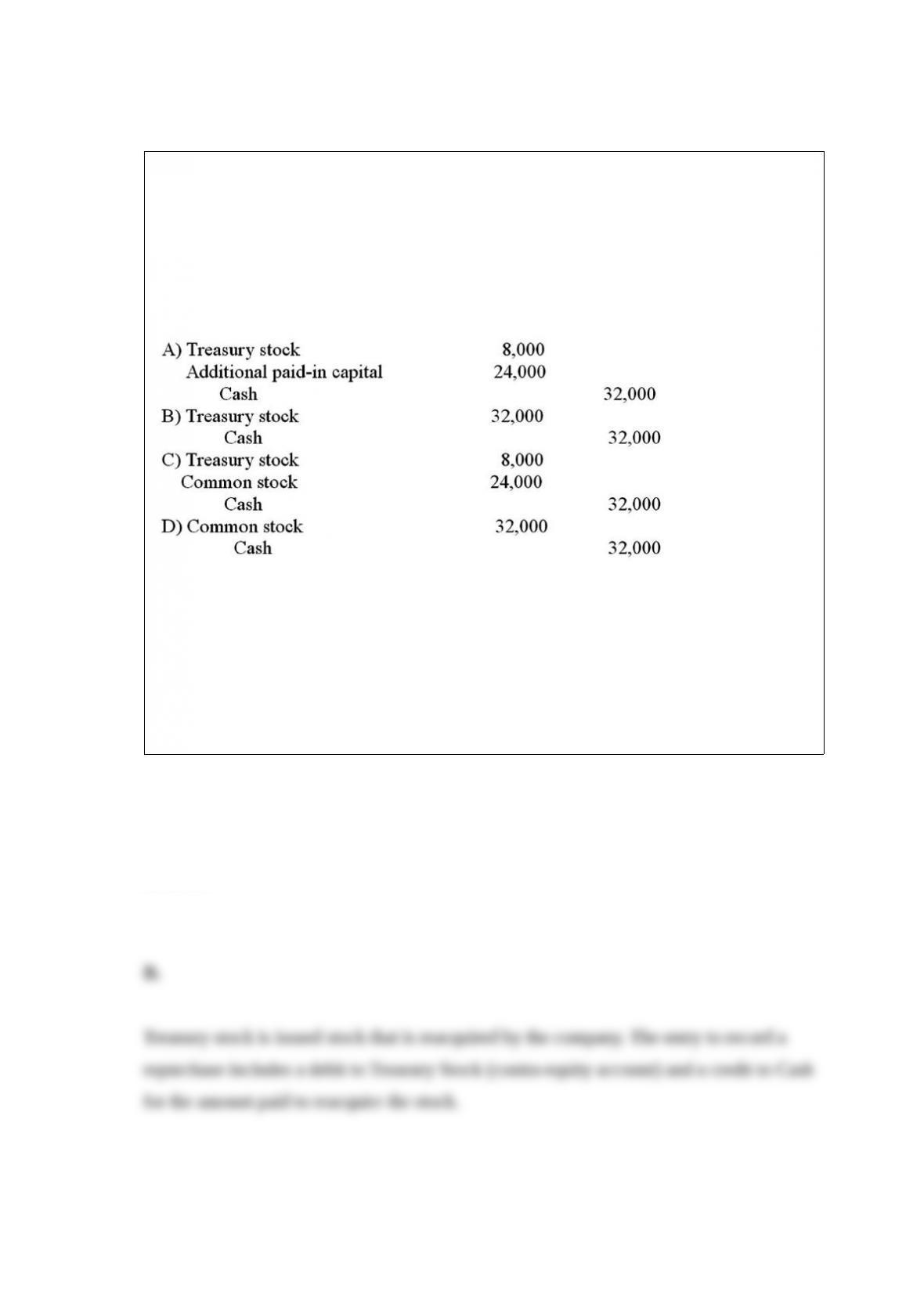

JC Corporation had 20,000 shares of $4 par value common stock outstanding on

January 1, 2014. On January 20, 2014, the company purchased 2,000 of the outstanding

shares for $16 per share. On July 3, 2014, the company reissued 1,000 of the shares at

$20 per share.

Use the information above to answer the following question. What is the journal entry

to record the purchase of the stock on January 20?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

Accumulated depreciation is classified as a(an)

A. expense.

B. contra-asset.

C. liability.

D. stockholders’ equity.

Answer:

Which of the following is generally the most useful in analyzing companies of different

size?

A. Comparative financial statements.

B. Horizontal analysis.

C. Common size financial statements.

D. Trend analysis.

Answer:

BetterBuy sells $50,000 of TVs to a customer. The credit terms state a 2% discount if

paid in 7 days and a 1% discount if paid in 8-14 days. The customer pays in 12 days.

How would BetterBuy record the customer’s payment?

A. Debit Cash for $50,000 and credit Accounts Receivable for $50,000.

B. Debit Accounts Receivable for $50,000, credit Cash for $49,500, and credit

Inventory for $500.

C. Debit Cash for $49,500, credit Accounts Receivable for $50,000, and debit Sales

Discounts for $500.

D. Debit Cash for $49,500, credit Accounts Receivable for $49,000, and credit Sales

Returns & Allowances for $500.

Answer:

If cost of goods sold is $145,000 and the beginning and ending inventory balances are

$18,000 and $13,000, respectively, the net purchases of inventory are:

A. $145,000

B. $140,000

C. $150,000

D. $132,000

Answer:

Company X has net sales revenue of $780,000, cost of goods sold of $343,200, and all

other expenses of $327,600. The net profit margin is closest to:

A. 0.32.

B. 0.56.

C. 0.86.

D. 0.14.

Answer:

The periodic allocation of the cost of equipment to the periods in which it is used is

called

A. Accumulated allocation.

B. Unearned revenue.

C. Depreciation.

D. Prepaid expense.

Answer:

A company reported that its bonds with a face value of $50,000 and a carrying value of

$53,000 are retired for $56,000 cash. The amount to be reported under cash flows from

financing activities is:

A. ($53,000).

B. ($3,000).

C. ($56,000)

D. $0. This is an operating activity.

Answer:

If the market rate of interest is 6%, a $10,000, 10-year bond with a stated annual

interest rate of 8% would be issued at an amount:

A. less than face value.

B. equal to the face value.

C. greater than face value.

D. equal to the face value minus a discount.

Answer:

Which of the following could indicate bad news?

A. An increase in asset turnover ratio.

B. A decrease in days to sell.

C. A decrease in EPS.

D. A decrease in the debt to assets ratio.

Answer:

The advantages of the direct method include all of the following except:

A. It allows for more detailed analysis of operating cash flows.

B. It provides more information than the indirect method to relate cash inflows and

outflows.

C. It allows for more reliable prediction of future cash flows.

D. Comparisons between companies are facilitated since most U.S. companies use the

direct method.

Answer:

During 2014, a company provided services for cash of $21,000 and services on credit of

$15,000. The company collected accounts receivable of $8,000 and incurred operating

expenses of $22,700, $14,000 of which were paid during the year. The amount of net

income (loss) for the year is:

A. $13,300.

B. ($1,700).

C. $22,700.

D. $6,300.

Answer:

Which of the following would not be affected by the choice of an inventory costing

method (that is between FIFO, LIFO, weighted average, and specific identification)?

A. Net sales

B. Cost of goods sold

C. Gross profit

D. Net income

Answer:

Your company pays $620,000 for a patent that has 10 years remaining. Each year, your

company should:

A. debit amortization expense for $62,000 and credit accumulated depreciation for

$62,000.

B. debit intangible assets and credit accumulated amortization for an amount equal to

20% of book value.

C. debit amortization expense for $62,000 and credit patent for $62,000.

D. report no amortization expense because patents are not subject to amortization.

Answer:

Expenses are shown

A. on the income statement in the time period in which they are paid.

B. on the income statement in the time period in which they are incurred.

C. on the balance sheet in the time period in which they are paid.

D. on the balance sheet in the time period in which they are incurred.

Answer:

When S. Dee Company bought B. Darin Company, the purchase price included a patent

valued at $15,000. The patent has 10 years remaining of its legal life, but its estimated

useful life to S. Dee Company was only 8 years. The journal entry to record the annual

patent amortization would include a

A. debit to Patent, $1,875.

B. debit to Amortization expense, $1,875.

C. credit to Patent, $1,500.

D. credit to Amortization expense, $1,500.

Answer:

On January 31, 2014, Purrfect Pets receives a $4,680 interest payment on a note

receivable representing two months of accumulated interest. One month of this interest

was accrued and recorded during the year ended December 31, 2013. Upon receiving

the payment, the company would:

A. debit Interest Receivable for $2,340, debit Cash $2,340, and credit Interest Revenue

for $4,680.

B. debit Cash for $4,680, credit Interest Revenue for $2,340, and credit Interest

Receivable for $2,340.

C. debit Cash for $4,680, and credit Interest Receivable for $4,680.

D. debit Cash for $4,680 and credit Interest Revenue for $4,680.

Answer:

The purpose of internal controls includes all of the following except:

A. to improve efficiency.

B. to reduce waste.

C. to minimize errors.

D. to eliminate fraud.

Answer:

One of the major advantages of making adjustments in order to improve the quality of

financial statements is that they:

A. ensure that revenues and expenses are recognized during the period they are earned

and incurred.

B. ensure that all estimates of future activities are eliminated from consideration.

C. ensure that revenues and expenses are recognized conservatively during the period

hey are paid.

D. provide an opportunity to manipulate the numbers to the best effect.

Answer:

In the T-account above:

A. (a) and (b) are credits.

B. (c) through (g) are debits.

C. if the sum of (a) and (b) is less than the sum of (c) through (g), the total cash will

increase.

D. (a) and (b) are increases.

Answer:

Which of the following is calculated by dividing net income by net sales?

A. Gross profit margin.

B. Current ratio.

C. Net profit margin.

D. Asset turnover.

Answer:

A corporate charter specifies that the company may sell up to 20 million shares of

stock. The company sells 12 million shares to investors and later buys back 3 million

shares. The current number of shares of treasury stock after these transactions have

been accounted for is:

A. 3 million shares.

B. 8 million shares.

C. 9 million shares.

D. 17 million shares.

Answer:

When a company uses excess cash to buy back some of its outstanding common stock,

which of the following ratios will be affected directly in the manner described below?

A. Return on equity (ROE) will decrease.

B. Earnings per share (EPS) will increase.

C. The Price Earnings (PE) ratio will increase.

D. The receivables turnover ratio will increase.

Answer:

When an adjusting entry is made in anticipation of some receivables being

uncollectible, the adjustment:

A. reduces both net income and net accounts receivable.

B. reduces net income and increases liabilities.

C. reduces net accounts receivable and increases liabilities.

D. reduces net income and selling expenses.

Answer:

Internal controls are concerned with:

A. only manual systems of accounting.

B. the extent of government regulations.

C. protecting against theft of assets and enhancing the reliability of accounting

information.

D. preparing income tax returns.

Answer:

Net income divided by Net sales is the calculation for which of the following ratios?

A. Return on equity ratio.

B. Net profit margin ratio.

C. Current ratio.

D. Asset turnover ratio.

Answer:

Company Z has 8 million shares of common stock authorized with a par value of $1

and a market price of $72. There are 4 million outstanding shares and 1 million shares

held in treasury stock.

a.

1) Prepare the journal entry if the company declares and distributes a 10% stock

dividend.

2) Show the effect of the 10% stock dividend on assets, liabilities, and stockholders’

equity.

b.

1) Prepare the journal entry if the company declares and distributes a 100% stock

dividend.

2) Show the effect of the 100% stock dividend on assets, liabilities, and stockholders’

equity.

c. Compare the two stock dividends in parts a and b above. Explain why the 100%

stock dividend is not 10 times larger than a 10% stock dividend.

Answer:

A company provided the following information:

There was no change in contributed capital this year and there were no dividends

declared in the current year. The return on equity ratio for the current year is closest to:

A. 20.7%.

B. 75%.

C. 3.8%.

D. 1.33%.

Answer:

Investors are often interested in the amount of net income distributed as dividends. In

which section of the financial statements would investors look to find this amount?

A. Statement of retained earnings.

B. Balance sheet.

C. Notes to the financial statements.

D. Income statement.

Answer:

Which of the following statements accurately explains why the board of directors of a

company whose financial future contains some uncertainties might issue a 2-for-1 stock

split rather than declare a 100% stock dividend?

A. A stock split would not reduce the market price per share, whereas a stock dividend

would.

B. A stock split would reduce the market price per share, whereas a stock dividend

would not.

C. A stock split would increase total stockholders’ equity, whereas a stock dividend

would not.

D. A stock split would not reduce retained earnings, whereas a stock dividend would.

Answer: