1) As a consequence of his failure to adhere to generally accepted auditing standards in

the course of his examination of the Lamp Corp., Harrison, CPA, did not detect the

embezzlement of a material amount of funds by the company’s controller. As a matter of

common law, to what extent would Harrison be liable to the Lamp Corp. for losses

attributable to the theft?

A) He would have no liability, since the ordinary examination cannot be relied upon to

detect thefts of assets by employees

B) He would have no liability because privity of contract is lacking

C) He would be liable for losses attributable to his negligence

D) He would be liable only if it could be proven that he was grossly negligent

2) If an auditor concludes there are contingent liabilities, then he or she must evaluate

the:

A)

B)

C)

D)

3) Which of the following statements best describes the primary purpose of Statements

on Auditing Standards?

A) They are guides intended to set forth auditing procedures that are applicable to a

variety of situations

B) They are procedural outlines that are intended to narrow the areas of inconsistency

and divergence of auditor opinion

C) They are authoritative statements, enforced through the Code of Professional

Conduct, and are intended to limit the degree of auditor judgment

D) They are interpretations that are intended to clarify the meaning of “generally

accepted auditing standards”

4) Which of the following is not likely a factor in the increase in the number of lawsuits

and sizes of awards to plaintiffs related to auditor behavior?

A) Increased awareness of auditor responsibilities by users of financial statements

B) CPA firms are more willing to settle lawsuits

C) Difficulty judges and jurors have in understanding legal matters

D) Increased consciousness on the part of the SEC for its responsibility to protect

investors

5) Which of the following tests are typically not necessary when auditing a client’s

schedule of recorded disposals?

A) Footing the schedule

B) Tracing schedule totals to the general ledger

C) Tracing cost and accumulated depreciation of the disposals to the property master

file

D) All of the above are necessary

6) The King Surety Company wrote a general fidelity bond covering thefts of assets by

the employees of Wilson, Inc. Thereafter, Cooney, an employee of Wilson, embezzled

$17,200 of company funds. When the activities were discovered, King paid Wilson the

full amount in accordance with the terms of the fidelity bond, and then sought recovery

against Wilson’s auditors, Lynch & Merritt, CPAs. Which of the following would be

Lynch & Merritt’s best defense?

A) King is not in privity of contract

B) The shortages were the result of clever forgeries and collusive fraud which would

not be detected by an examination made in accordance with generally accepted auditing

standards

C) Lynch & Merritt were not guilty either of gross negligence or fraud

D) Lynch & Merritt were not aware of the King-Wilson surety relationship

7) The auditor’s first course of action when an illegal act is uncovered should be to

immediately notify the appropriate authorities, including but not limited to the police,

and for publicly held companies, the Securities and Exchange Commission.

A) True

B) False

8) An auditor has accessed client business risk and the risk to material misstatements to

the clients financial statements. These are done in order to:

A) apply the audit risk model in determining the appropriate audit procedures to

perform

B) determine the reliance on the company’s internal control systems for financial

reporting

C) determine the test of balances to be performed by the audit team

D) assure the CPA firm that they can perform the audit effectively and efficiently

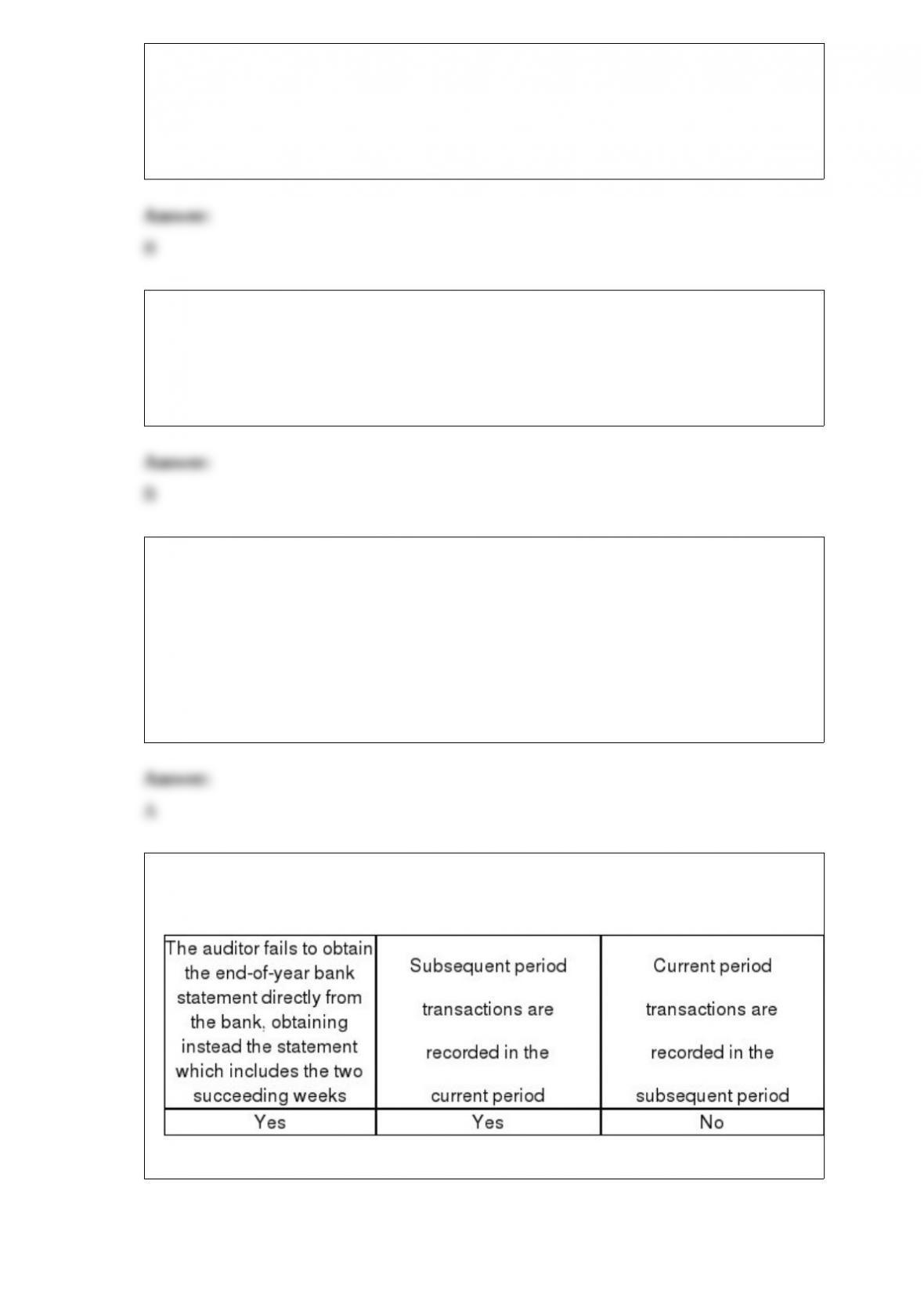

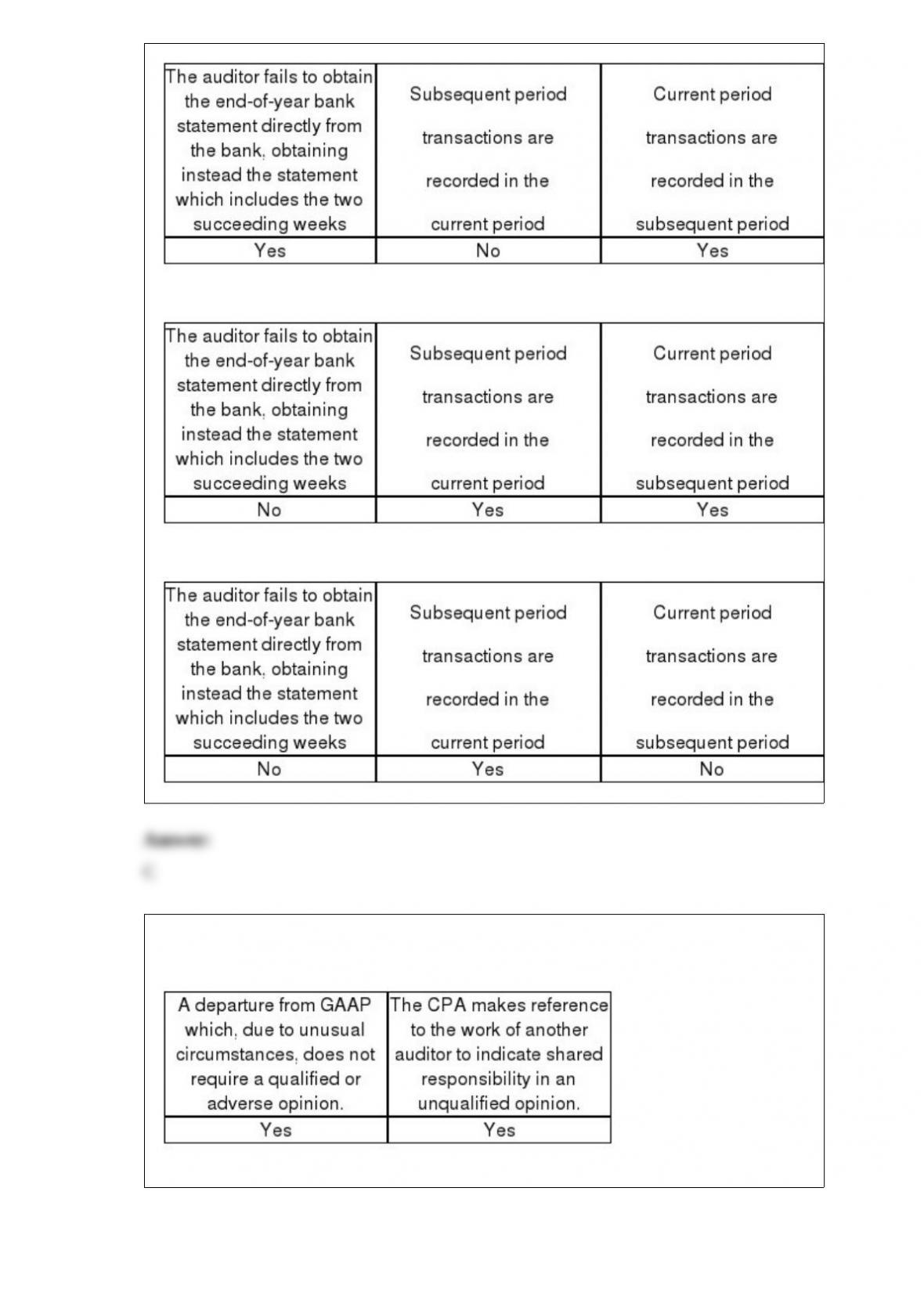

9) Cutoff misstatements occur when:

A)

B)

C)

D)

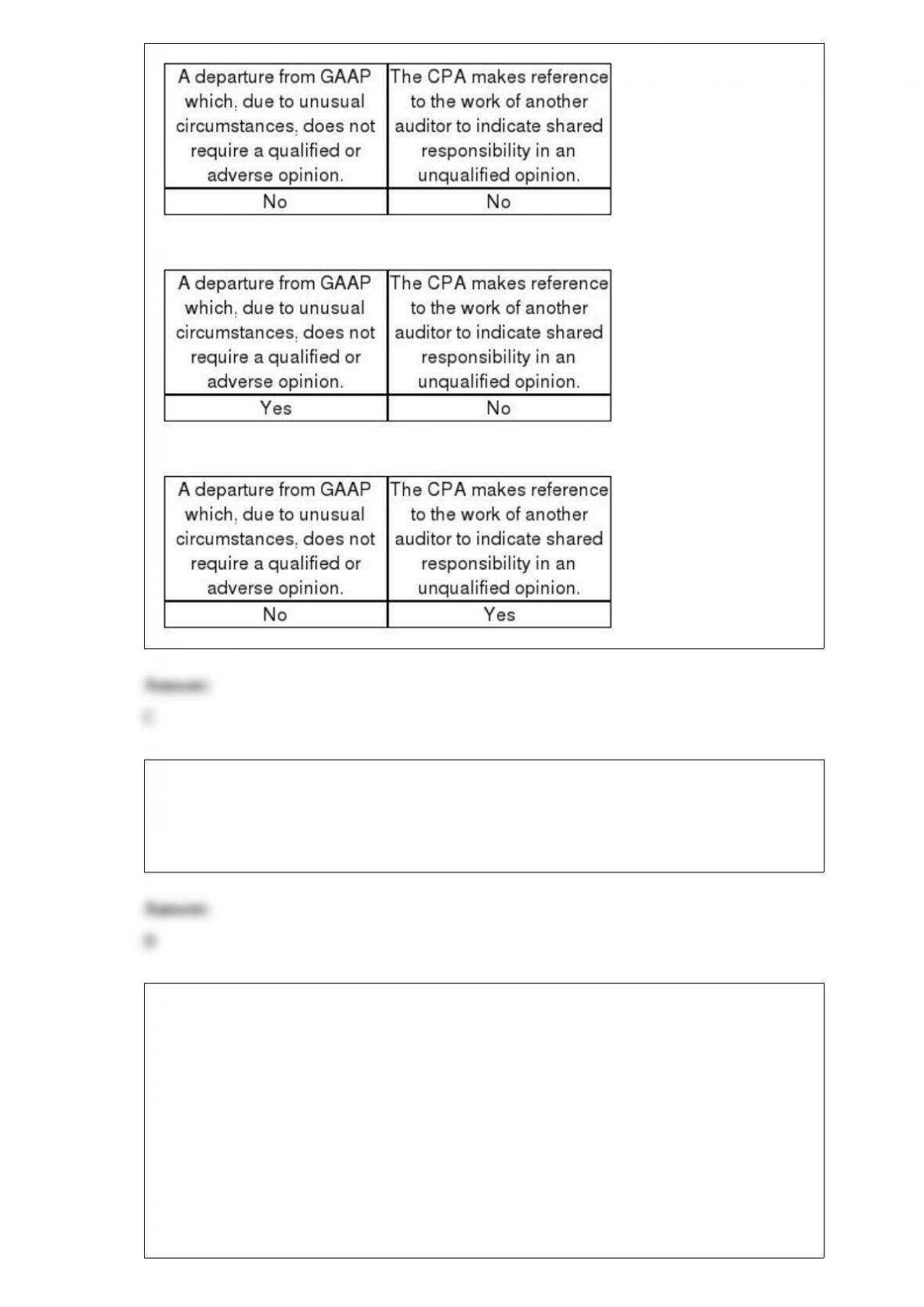

10) Indicate which changes would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

11) Users of the financial statements rely on the auditor’s report because it provides

absolute assurance the report provides.

A) True

B) False

12) William Gregory, CPA, is the principal auditor for a multi-national corporation.

Another CPA has examined and reported on the financial statements of a significant

subsidiary of the corporation. Gregory is satisfied with the independence and

professional reputation of the other auditor, as well as the quality of the other auditor’s

examination. With respect to his report on the consolidated financial statements, taken

as a whole, Gregory:

A) must not refer to the examination of the other auditor

B) must refer to the examination of the other auditor

C) may refer to the examination of the other auditor

D) must refer to the examination of the other auditors along with the percentage off

consolidated assets and revenue that they audited

13) To be capitalized as part of property, plant and equipment, assets must:

A) have expected useful lives of more than one year

B) not be acquired for resale

C) be useful in multiple productive capacities within the organization

D) A and B, but not C

14) The audit procedure that requires an auditor to “foot the acquisition schedule”

relates to which balance-related audit objective?

A) Classification

B) Detail tie-in

C) Existence

D) Cut-off

15) While performing their audit, the audit team uncovers fraud that is likely to have an

immaterial affect on the financial statements taken as whole. In this case the auditors

should:

A) plan on additional audit procedures to determine the exact amount of the fraud

B) communicate with legal authorities as to the identity of the fraudsters

C) disclose the fraud to the appropriate level of management or to the audit committee

D) call the whistleblower hotline and name the suspected individuals

16) The provisions of the Sarbanes-Oxley Act of 2002 are most likely to allow which of

the following non-audit services for audit clients?

A) appraisal or valuation services (e.g., pension, post-employment benefit liabilities)

B) financial information systems design and implementation

C) internal audit outsourcing

D) tax consulting

17) When an auditor observes that personnel who are responsible for physically

counting inventory are not following the inventory instructions, the auditor should:

A) contact a client’s supervisor in an attempt to correct the problem

B) modify the client’s physical inventory instructions

C) not discuss the problem with client’s supervisor in order to maintain independence

D) assign audit staff to the inventory count

18) Both overstatements and understatements must be considered when allocating

materiality to balance sheet accounts.

A) True

B) False

19) When performing a review (SSARS review) of financial statements, the accountant

is required to obtain a letter of representation from management.

A) True

B) False

20) What is the best reason that standards prohibit accepting an engagement on a

projection for general use?

A) The CPA’s procedures would violate SSARS

B) Reports on projections are not well understood by the general public

C) Underlying hypothetical assumptions are difficult to interpret without obtaining

additional information

D) The CPA is not qualified to report on the use of GAAP in the projected financial

statement

21) If a company employs a capital stock registrar and/or transfer agent, the registrar or

agent, or both, should be requested to confirm directly to the auditor the number of

shares of each class of stock:

A) surrendered and canceled during the year

B) authorized at the balance sheet date

C) issued and outstanding at the balance sheet date

D) authorized, issued, and outstanding during the year

22) Which of the following parties is responsible for implementing internal controls to

minimize the likelihood of fraud?

A) External auditors

B) Audit committee members

C) Management

D) Committee of Sponsoring Organizations

23) Management assertions are:

A) directly related to the financial reporting framework used by the company, usually

U.S. GAAP or IFRS

B) stated in the footnotes to the financial statements

C) explicitly expressed representations about the financial statements

D) provided to the auditor in the assertions letter, but are not disclosed on the financial

statements

24) The relevance of audit evidence depends on the audit objective being tested.

A) True

B) False

25) The audit team has identified and documented fraud risk. Their next step should be

to:

A) evaluate factors that should reduce risk

B) develop programs to test for fraud

C) proceed with performing tests of controls

D) proceed with performing substantive tests of balances

26) When the auditor knows that an illegal act has occurred, the auditor must:

A) report it to the proper governmental authorities

B) consider the effects on the financial statements, including the adequacy of disclosure

C) withdraw from the engagement

D) issue an adverse opinion

27) Which of the following is least likely to be used in obtaining an understanding of

client general controls?

A) examination of system documentation

B) inquiry of client personnel (e.g., key users)

C) walk through of a sales transaction

D) reviews of questionnaires completed by client IT personnel

28) Under Rule 505, Form of Organization and Name, a CPA firm may not designate

itself as “Members of the American Institute of Certified Public Accountants” unless a

majority of its owners are members of the Institute.

A) True

B) False

29) Output controls focus on preventing errors during processing.

A) True

B) False

30) An engagement letter sent to a publicly held audit client usually would not include

a:

A) reference to the auditor’s responsibility for the detection of errors or irregularities

B) estimation of the time to be spent on the audit work by audit staff and management

C) statement that management advisory services would be made available upon request

D) reference to management’s responsibility for the financial statements

31) Which of the following is most reliable for verifying the correct balance of accounts

payable?

A) Vendors’ invoices

B) Vendors’ statements

C) Confirmations

D) Bills of lading

32) Inquiries of the client are usually sufficient to provide appropriate evidence to

satisfy an audit objective.

A) True

B) False

33) The preliminary judgment on materiality is compared to an estimated total

misstatements to determine if an account balance is materially misstated.

A) True

B) False

34) In certifying their annual financial statements, the CEO and CFO of a public

company certify that the financial statements comply with the requirements of:

A) GAAP

B) the Sarbanes-Oxley Act

C) the Securities Exchange Act of 1934

D) GAAS

35) A company frequently sells products at a price below inventory cost. Essential

controls in the risk assessment process would include:

A) adequate controls that address the risk of overstating inventory

B) adequate controls that address the risk of not including a purchased item in inventory

C) adequate controls that address the risk of understatement of inventory

D) adequate controls that address the risk of overstatement of cost of goods sold

36) The responsibility for adopting sound accounting policies and maintaining adequate

internal control rests with the:

A) board of directors

B) company management

C) financial statement auditor

D) company’s internal audit department