The present value of a given amount decreases as the number of years over which it is

to be discounted also decreases.

Answer:

When a company issues common stock in exchange for cash, the cash inflow is

recorded in the investing activities section of the statement of cash flows.

Answer:

In the selling and administrative budget, the non-cash charges (such as depreciation) are

added to the total budgeted selling and administrative expenses to determine the

expected cash disbursements for selling and administrative expenses.

Answer:

The traditional format income statement is used as an internal planning and

decision-making tool. Its emphasis on cost behavior aids cost-volume-profit analysis,

management performance appraisals, and budgeting.

Answer:

A newly formed company with enormous growth prospects would be expected to have

negative free cash flow during its start-up phase.

Answer:

The process of assigning overhead cost to jobs is known as overhead application.

Answer:

Generally, a product line should be dropped when the fixed costs that can be avoided by

dropping the product line are less than the contribution margin that will be lost.

Answer:

A favorable spending variance occurs when the actual cost exceeds the amount of that

cost in the flexible budget.

Answer:

When assigning costs to partially completed units in the ending work in process

inventory, it is not necessary to consider the percentage completion of the units under

the weighted-average method.

Answer:

A revenue variance is favorable if the revenue in the static planning budget exceeds the

revenue in the flexible budget.

Answer:

The following would typically be considered indirect costs of manufacturing a

particular Boeing 747 to be delivered to Singapore Airlines: electricity to run

production equipment, the factory manager’s salary, and the cost of the General Electric

jet engines installed on the aircraft.

Answer:

A sunk cost is a cost that has already been incurred and that cannot be avoided

regardless of what action is chosen.

Answer:

The contribution margin is viewed as a better gauge of the long run profitability of a

segment than the segment margin.

Answer:

A company has a standard cost system in which fixed and variable manufacturing

overhead costs are applied to products on the basis of direct labor-hours. The company’s

choice of the denominator level of activity affects the Fixed component of the

predetermined overhead rate.

Answer:

The salary of the treasurer of a corporation is an example of a common cost which

normally cannot be traced to product segments.

Answer:

A gain on the sale of equipment would be included as part of a company’s financing

activities on the statement of cash flows.

Answer:

Free cash flow is net cash provided by operating activities less dividends.

Answer:

A company can increase its net cash flow by increasing the depreciation expense it

records during the period.

Answer:

In order for a cost to be variable it must vary with either units produced or units sold.

Answer:

The cost of a resource that has no alternative use in a make or buy decision problem has

an opportunity cost of zero.

Answer:

Vandagriff Corporation has provided data concerning the company’s Manufacturing

Overhead account for the month of June. Prior to the closing of the overapplied or

underapplied balance to Cost of Goods Sold, the total of the debits to the Manufacturing

Overhead account was $77,000 and the total of the credits to the account was $64,000.

Which of the following statements is TRUE?

A. Manufacturing overhead transferred from Finished Goods to Cost of Goods Sold

during the month was $77,000.

B. Manufacturing overhead applied to Work in Process for the month was $64,000.

C. Manufacturing overhead for the month was overapplied by $13,000.

D. Actual manufacturing overhead incurred during the month was $64,000.

Answer:

Financial leverage is positive if the interest rate on debt is lower than the return on total

assets.

Answer:

Future costs that do not differ among the alternatives are not relevant in a decision.

Answer:

The standard cost per unit is computed by multiplying the standard quantity or hours by

the standard price or rate.

Answer:

Residual income equals average operating assets multiplied by the difference between

the return on investment and the minimum required rate of return.

Answer:

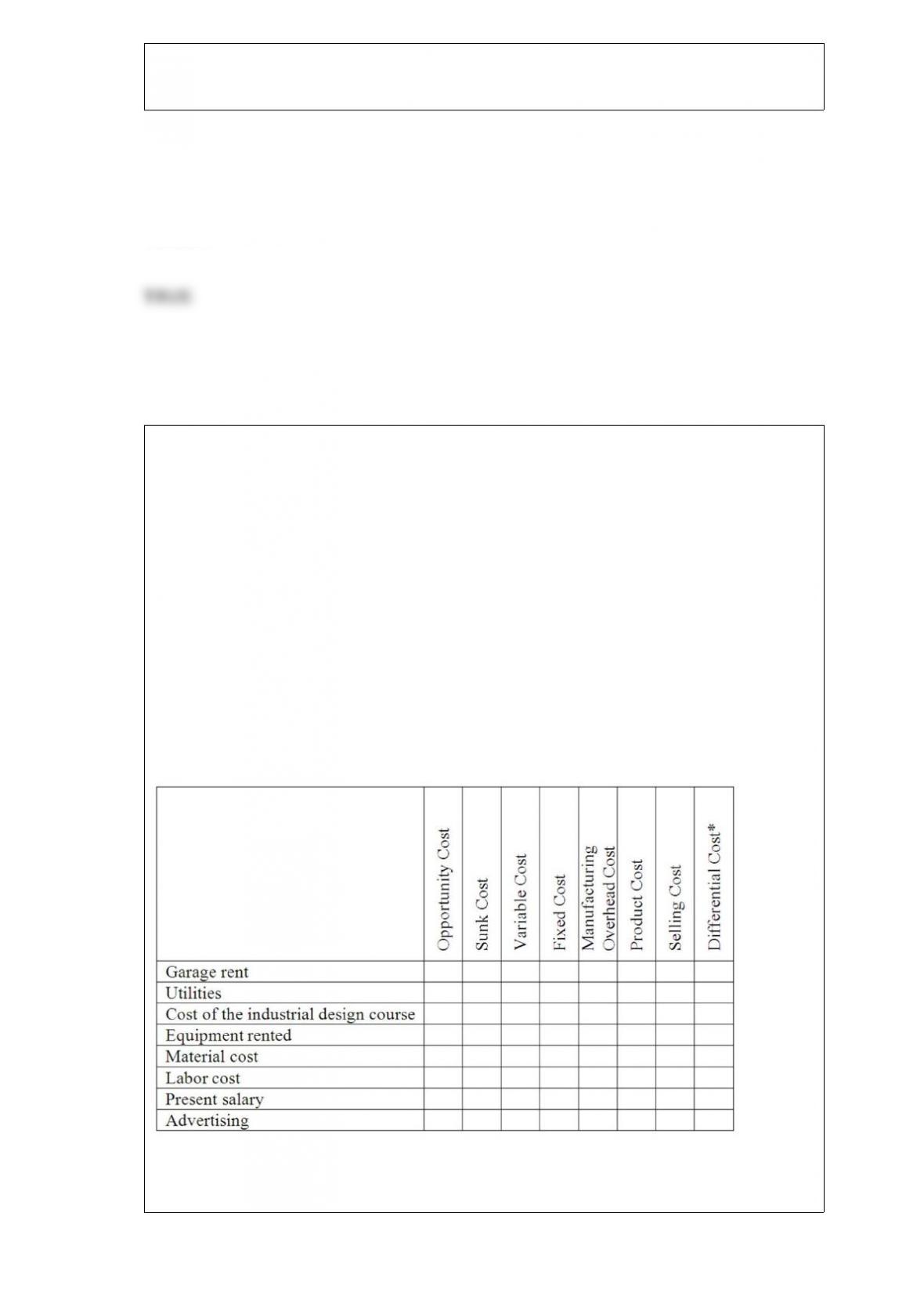

Bill Pope has developed a new device that is so exciting he is considering quitting his

job in order to produce and market it on a large-scale basis. Bill will rent a garage for

$300 per month for production purposes. Utilities will cost $40 per month. Bill has

already taken an industrial design course at the local community college to help prepare

for this venture. The course cost $300. Bill will rent production equipment at a monthly

cost of $800. He estimates the material cost per unit will be $5, and the labor cost will

be $3. He will hire workers and spend his time promoting the product. To do this he

will quit his job which pays $3,000 per month. Advertising and promotion will cost

$900 per month.

Complete the chart below by placing an “X” under each heading that helps to identify

the cost involved. There can be “Xs” placed under more than one heading for a single

cost, e.g., a cost might be a sunk cost, an overhead cost and a product cost; there would

be an “X” placed under each of these headings opposite the cost.

* Between the alternatives of going into business to make the device or not going into

business to make the device.

Answer:

Under the direct method of determining the net cash provided by operating activities on

the statement of cash flows, an increase in accounts payable would be added to cost of

goods sold to convert cost of goods sold to a cash basis.

Answer:

Under a job-order cost system the Work in Process account is debited with the cost of

materials purchased.

Answer:

If the fixed manufacturing overhead volume variance is unfavorable, too much has been

spent on fixed manufacturing overhead items.

Answer:

Joint production costs are relevant costs in decisions about what to do with a product

from the split-off point onward in the production process.

Answer:

Hults Corporation has provided data concerning the company’s Manufacturing

Overhead account for the month of November. Prior to the closing of the overapplied or

underapplied balance to Cost of Goods Sold, the total of the debits to the Manufacturing

Overhead account was $75,000 and the total of the credits to the account was $57,000.

Which of the following statements is TRUE?

A. Manufacturing overhead transferred from Finished Goods to Cost of Goods Sold

during the month was $75,000.

B. Actual manufacturing overhead incurred during the month was $57,000.

C. Manufacturing overhead applied to Work in Process for the month was $75,000.

D. Manufacturing overhead for the month was underapplied by $18,000.

Answer:

Under the direct method of determining net cash provided by operating activities on the

statement of cash flows, the net income figure is adjusted for changes in current assets

and liabilities.

Answer:

Assuming that a segment has both variable expenses and traceable fixed expenses, an

increase in sales should increase profits by an amount equal to the sales times the

segment margin ratio.

Answer:

In a process costing system, overhead costs are traced to units of product as they are

incurred.

Answer:

Vanstee Corporation manufactures a variety of products. Variable costing net operating

income last year was $60,000 and this year was $67,000. Last year, $37,000 in fixed

manufacturing overhead costs were deferred in inventory under absorption costing. This

year, $8,000 in fixed manufacturing overhead costs were released from inventory under

absorption costing.

What was the absorption costing net operating income last year?

A. $60,000

B. $23,000

C. $97,000

D. $89,000

Answer:

Fussner Medical Clinic measures its activity in terms of patient-visits. Last month, the

budgeted level of activity was 1,610 patient-visits and the actual level of activity was

1,670 patient-visits. The cost formula for administrative expenses is $3.30 per

patient-visit plus $17,900 per month. The actual administrative expense was $24,600.

Last month, the spending variance for administrative expenses was:

A) $1,287 U

B) $198 U

C) $69 U

D) $1,189 U

Answer:

Smotherman Corporation produces and sells a single product. Data concerning that

product appear below:

The break-even in monthly unit sales is closest to:

A. 2,194 units

B. 3,676 units

C. 1,176 units

D. 1,730 units

Answer:

Reference: 8-24

Rushton Hospital bases its budgets on patient-visits. The hospitals static planning

budget for May appears below:

Actual results for the month were:

The spending variance for laundry costs for the month is:

A) $960 F

B) $1,660 F

C) $960 U

D) $1,660 U

Answer:

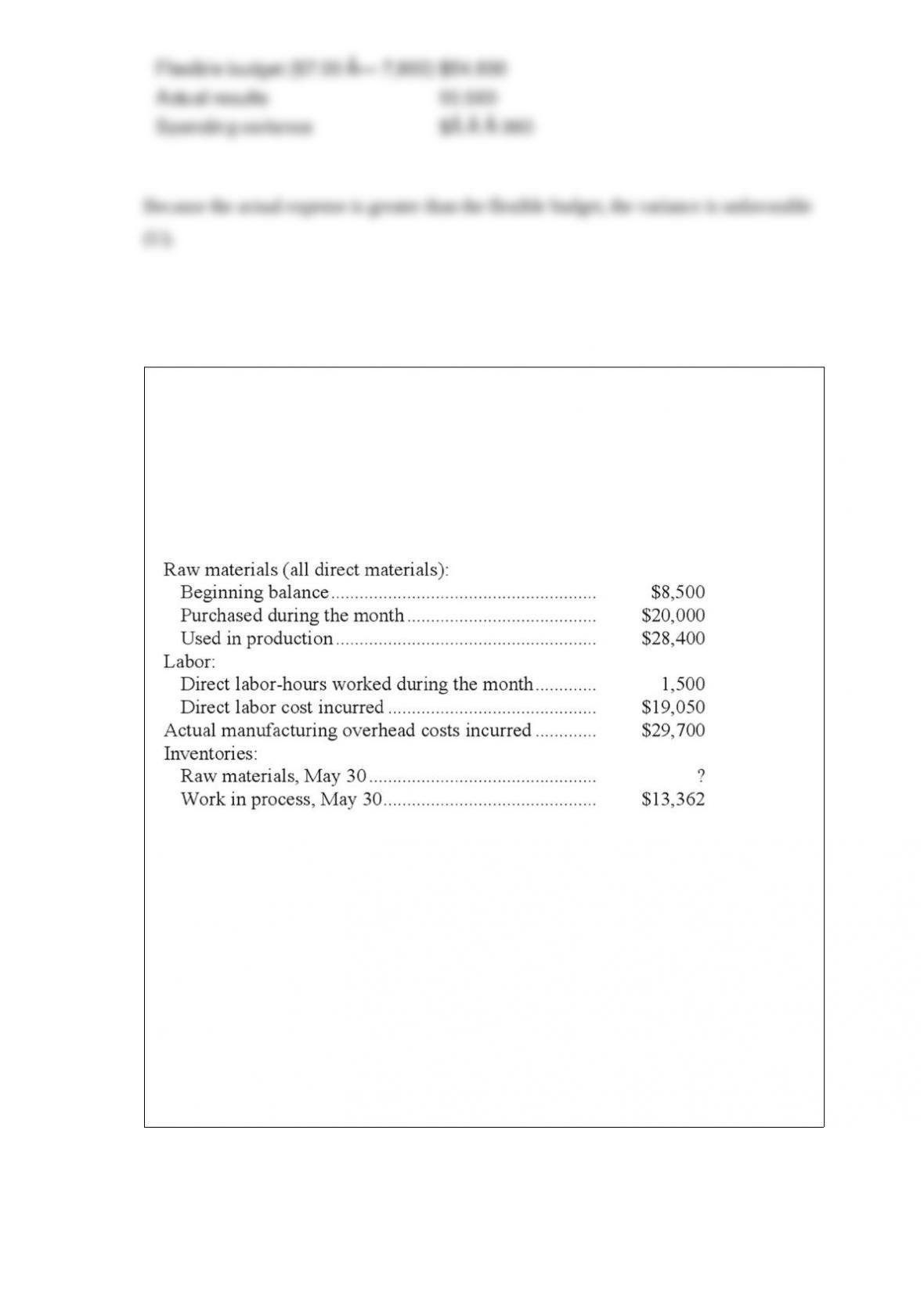

Daane Company had only one job in process on May 1. The job had been charged with

$1,000 of direct materials, $3,302 of direct labor, and $5,382 of manufacturing

overhead cost. The company assigns overhead cost to jobs using the predetermined

overhead rate of $20.70 per direct labor-hour.

During May, the following activity was recorded:

Work in process inventory on May 30 contains $2,921 of direct labor cost. Raw

materials consist solely of items that are classified as direct materials.

The cost of goods manufactured for May was:

A. $78,500

B. $78,100

C. $77,150

D. $74,822

Answer:

Reference: 8-47

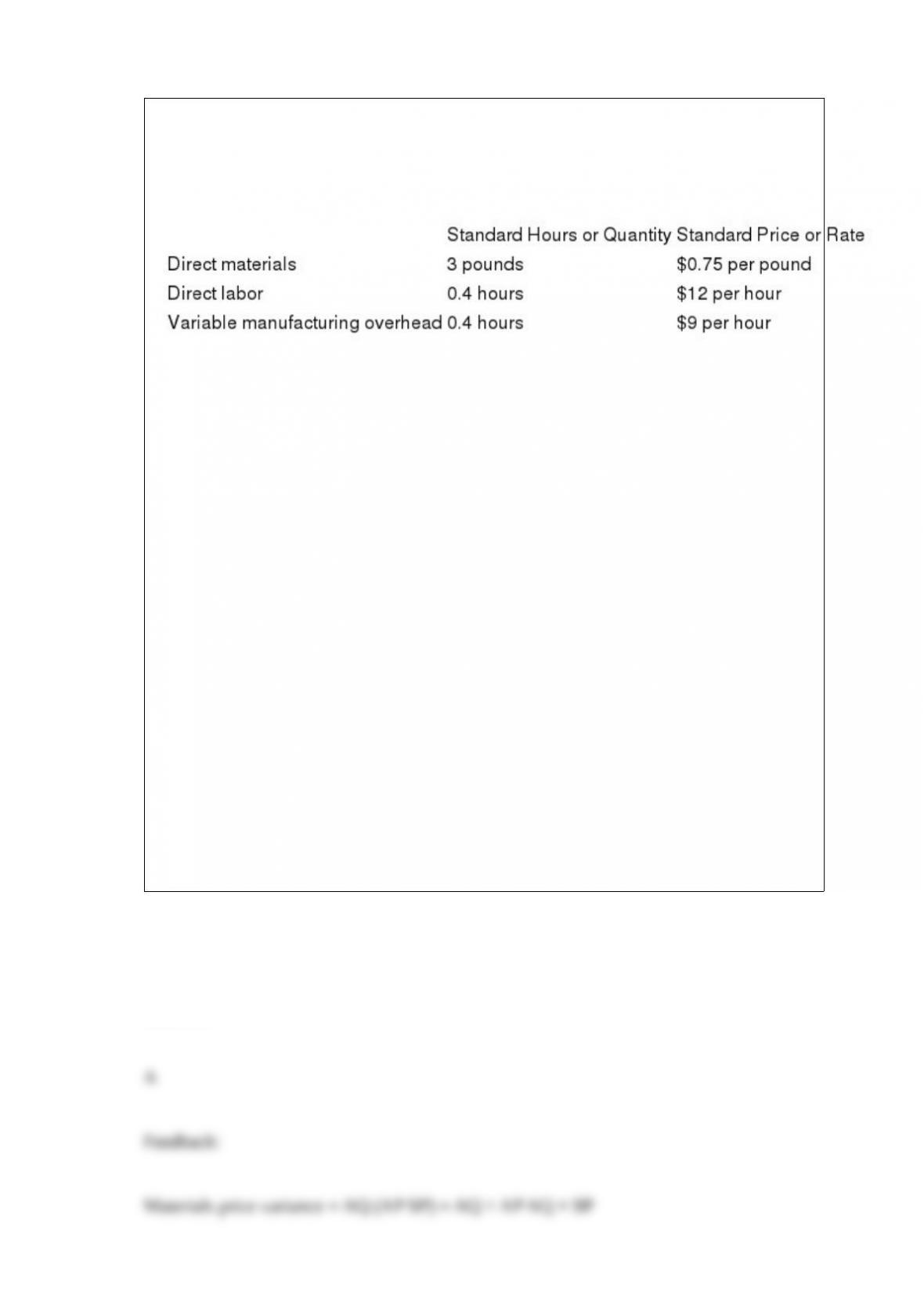

Bonnot Corporation makes a product that has the following direct labor standards:

The company budgeted for production of 2,100 units in October, but actual production

was 1,900 units. The company used 410 direct labor-hours to produce this output. The

actual direct labor rate was $20.60 per hour.

The labor rate variance for October is:

A) $164 F

B) $164 U

C) $152 U

D) $152 F

Answer:

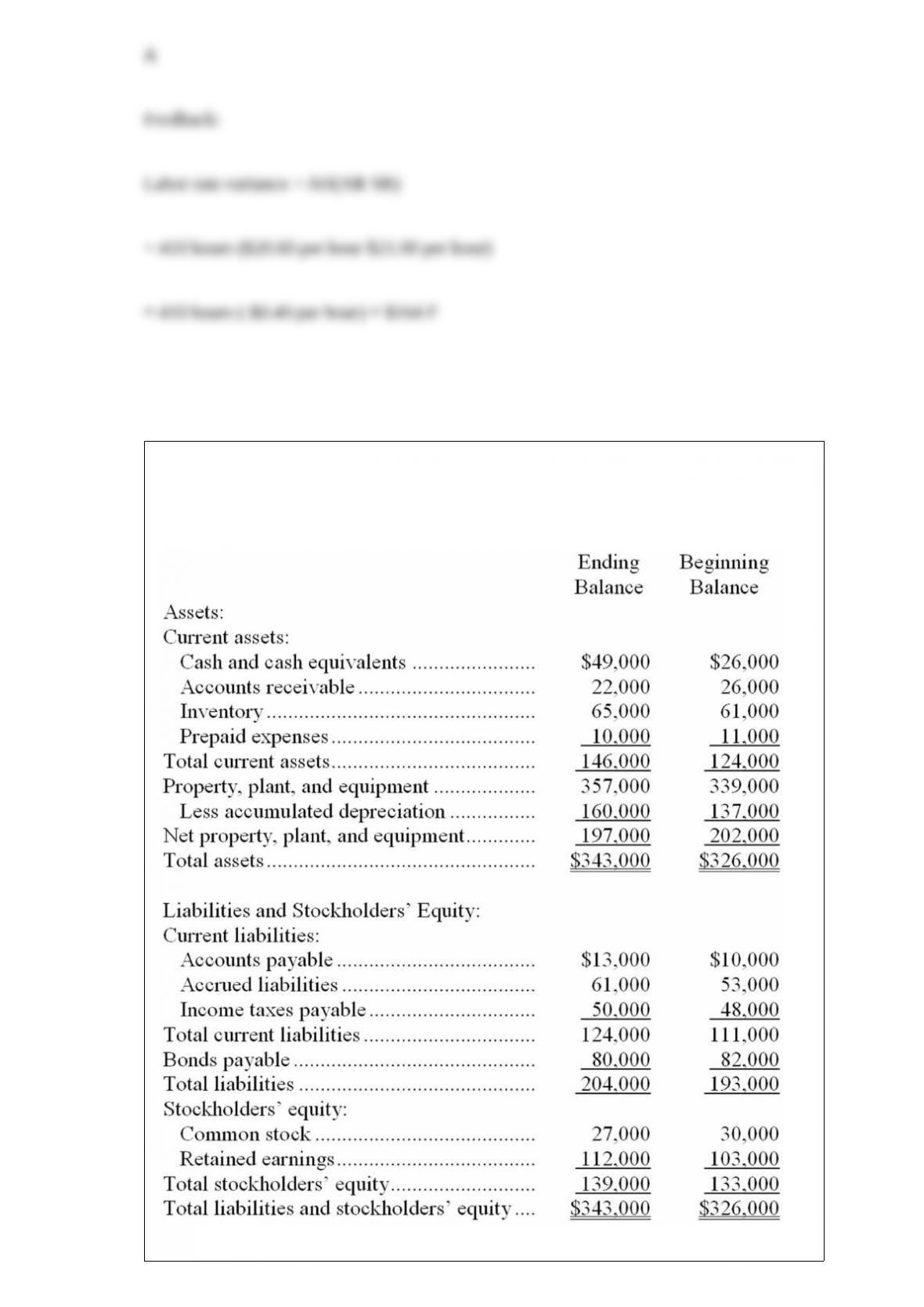

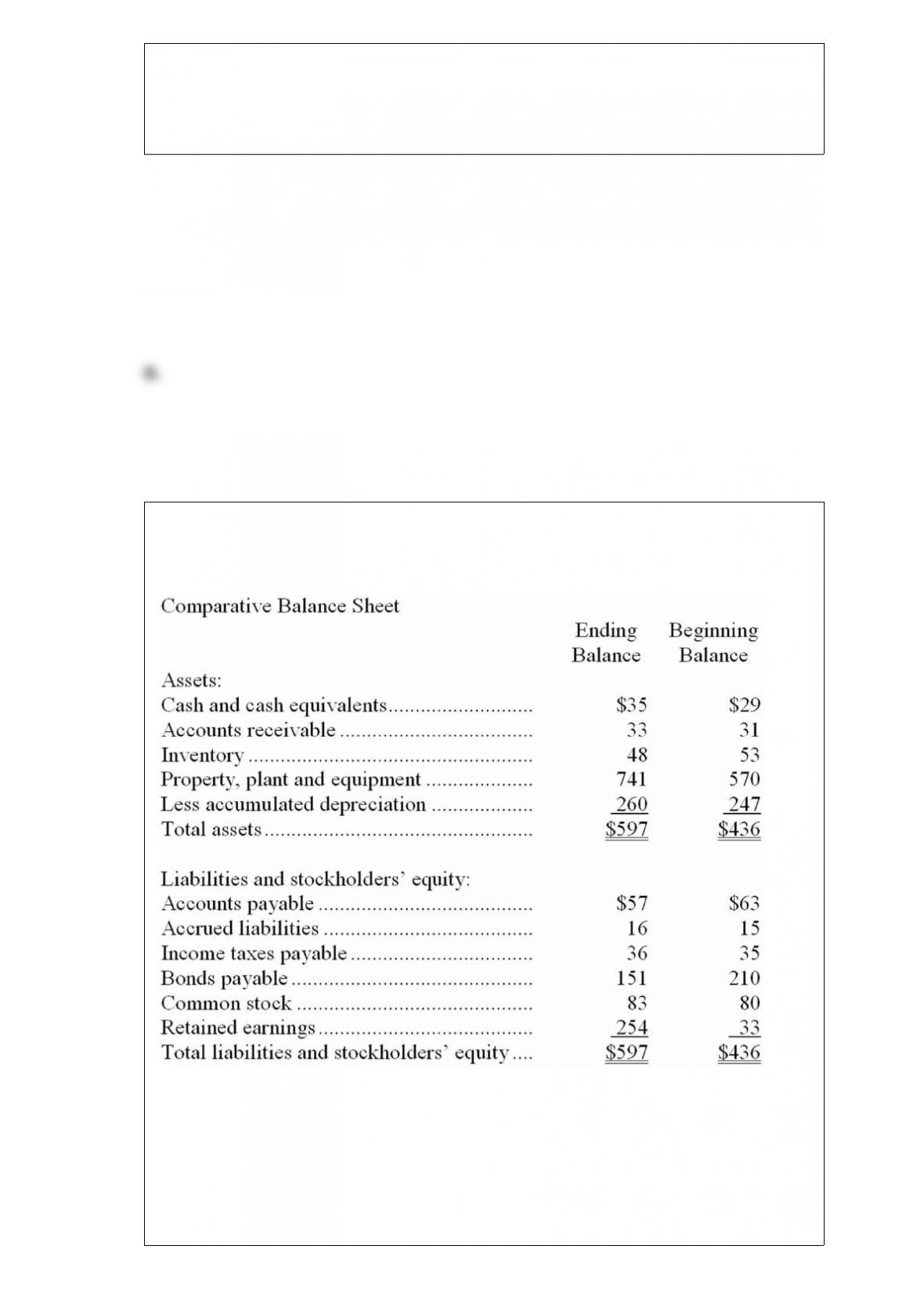

Hocking Corporation’s comparative balance sheet appears below:

The company’s net income (loss) for the year was $10,000 and its cash dividends were

$1,000. It did not sell or retire any property, plant, and equipment during the year. The

company uses the indirect method to determine the net cash provided by operating

activities.

Which of the following is correct regarding the operating activities section of the

statement of cash flows?

A. The change in Accounts Receivable will be subtracted from net income; The change

in Inventory will be added to net income

B. The change in Accounts Receivable will be added to net income; The change in

Inventory will be subtracted from net income

C. The change in Accounts Receivable will be added to net income; The change in

Inventory will be added to net income

D. The change in Accounts Receivable will be subtracted from net income; The change

in Inventory will be subtracted from net income

Answer:

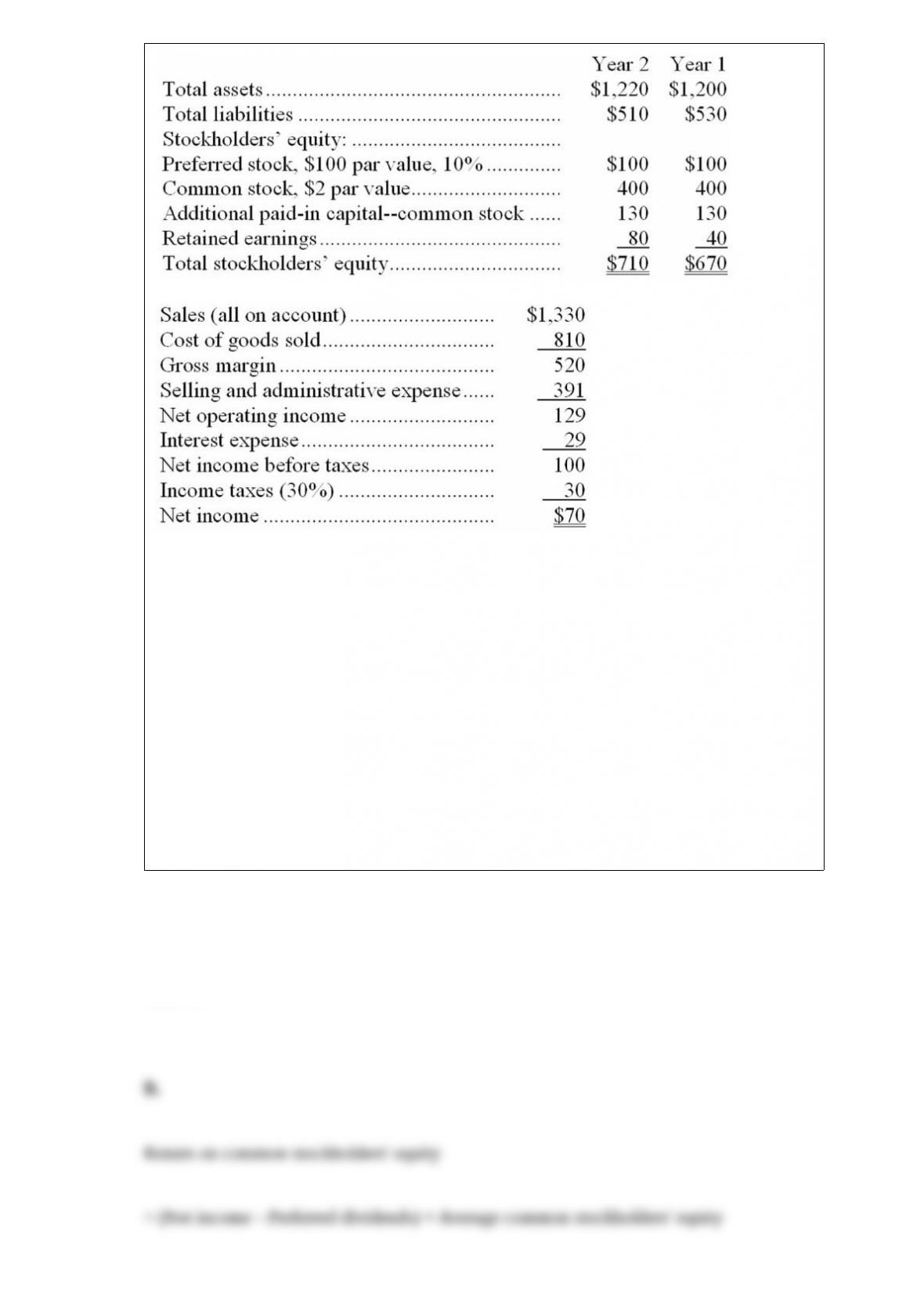

Excerpts from Goodrow Corporation’s most recent balance sheet and income statement

appear below:

Dividends on common stock during Year 2 totaled $20 thousand. Dividends on

preferred stock totaled $10 thousand. The market price of common stock at the end of

Year 2 was $5.34 per share.

The return on common stockholders’ equity for Year 2 is closest to:

A. 8.70%

B. 10.17%

C. 10.14%

D. 11.86%

Answer:

Salge Inc. bases its manufacturing overhead budget on budgeted direct labor-hours. The

variable overhead rate is $8.10 per direct labor-hour. The company’s budgeted fixed

manufacturing overhead is $74,730 per month, which includes depreciation of $20,670.

All other fixed manufacturing overhead costs represent current cash flows. The direct

labor budget indicates that 5,300 direct labor-hours will be required in September.

The September cash disbursements for manufacturing overhead on the manufacturing

overhead budget should be:

A. $42,930

B. $54,060

C. $96,990

D. $117,660

Answer:

The break-even point in unit sales is found by dividing total fixed expenses by:

A. the contribution margin ratio.

B. the variable expenses per unit.

C. the sales price per unit.

D. the contribution margin per unit.

Answer:

The Malcolm Company uses a standard cost system in which manufacturing overhead

costs are applied to products on the basis of standard direct labor-hours (DLHs). The

standards call for 3 hours of direct labor per unit produced. The following data pertain

to the company’s manufacturing overhead for the month of July:

The Fixed component of the predetermined overhead rate for June is:

A. $3.11

B. $3.39

C. $3.77

D. $3.00

Answer:

Carter Corporation applies manufacturing overhead on the basis of machine-hours. At

the beginning of the most recent year, the company based its predetermined overhead

rate on total estimated overhead of $135,850. Actual manufacturing overhead for the

year amounted to $145,000 and actual machine-hours were 5,660. The company’s

predetermined overhead rate for the year was $24.70 per machine-hour.

The predetermined overhead rate was based on how many estimated machine-hours?

A. 5,870

B. 5,500

C. 6,081

D. 5,660

Answer:

Rostad Corporation applies manufacturing overhead to products on the basis of

standard machine-hours. Budgeted and actual overhead costs for the most recent month

appear below:

The company based its original budget on 7,100 machine-hours. The company actually

worked 7,060 machine-hours during the month. The standard hours allowed for the

actual output of the month totaled 6,990 machine-hours. What was the overall fixed

manufacturing overhead volume variance for the month?

A. $512 favorable

B. $512 unfavorable

C. $1,408 favorable

D. $1,408 unfavorable

Answer:

During the last year, Snyder Co. produced 10,000 units of its only product. Costs

incurred by Snyder during the year were as follows:

The unit product cost under absorption costing was:

A. $5.43

B. $3.81

C. $4.71

D. $4.12

Answer:

The Rodgers Company makes 27,000 units of a certain component each year for use in

one of its products. The cost per unit for the component at this level of activity is as

follows:

Rodgers has received an offer from an outside supplier who is willing to provide 27,000

units of this component each year at a price of $25 per component. Assume that direct

labor is a variable cost. None of the fixed manufacturing overhead would be avoidable

if this component were purchased from the outside supplier.

Assume that if the component is purchased from the outside supplier, $35,100 of annual

fixed manufacturing overhead would be avoided and the facilities now being used to

make the component would be rented to another company for $64,800 per year. If

Rodgers chooses to buy the component from the outside supplier under these

circumstances, then the impact on annual net operating income due to accepting the

offer would be:

A. $18,900 decrease

B. $18,900 increase

C. $21,400 decrease

D. $21,400 increase

Answer:

Excerpts from Tigner Corporation’s most recent balance sheet appear below:

Sales on account in Year 2 amounted to $1,230 and the cost of goods sold was $820.

The current ratio at the end of Year 2 is closest to:

A. 1.12

B. 1.54

C. 0.35

D. 1.00

Answer:

Reference: 8-44

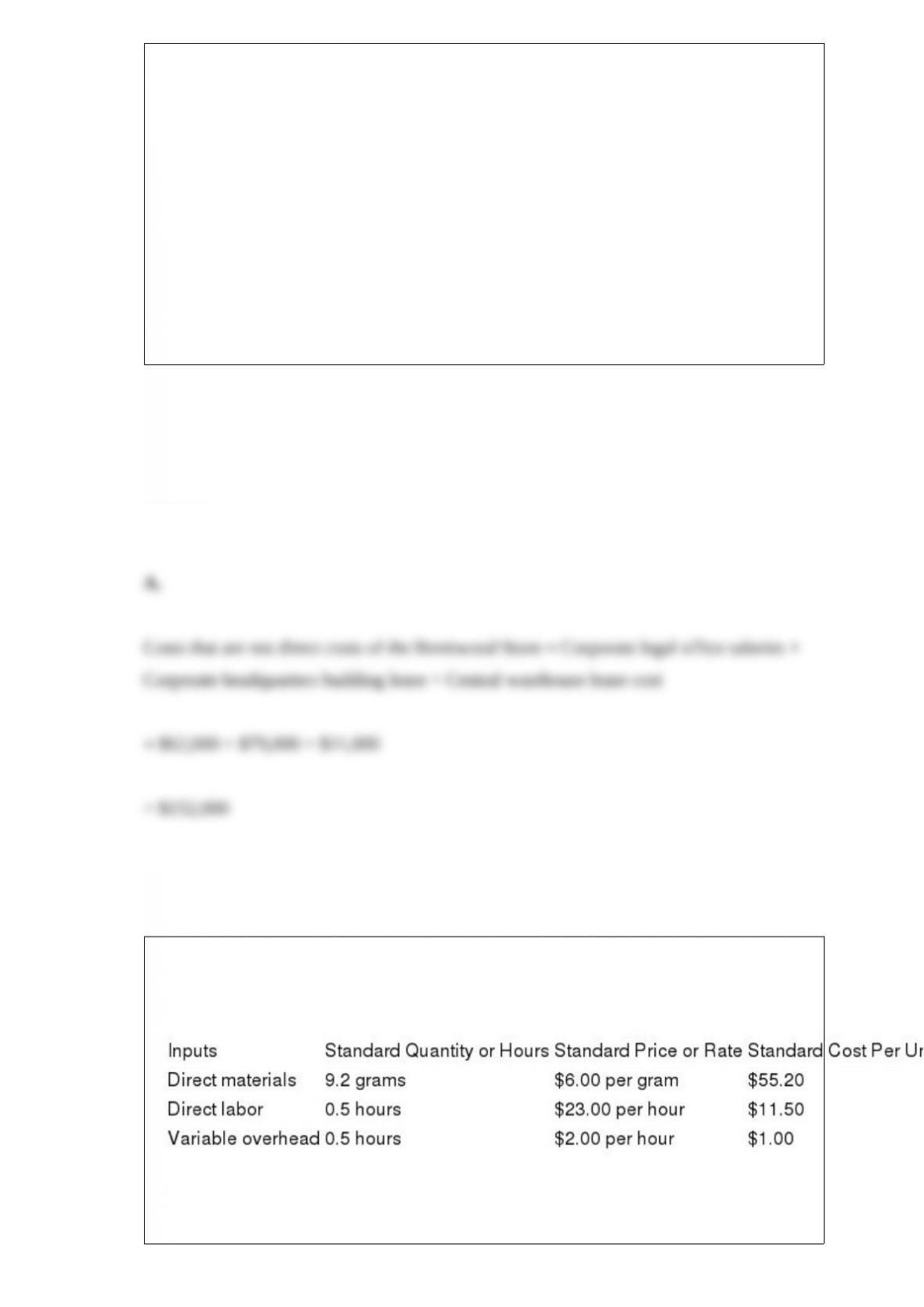

Carskadon Corporation makes a product that uses a material with the following direct

material standards:

The company produced 3,000 units in December using 6,270 pounds of the material.

During the month, the company purchased 7,100 pounds of the direct material at a total

cost of $13,490. The direct materials purchases variance is computed when the

materials are purchased.

The materials price variance for December is:

A) $710 F

B) $710 U

C) $660 F

D) $660 U

Answer:

Reference: 8-28

Cox Engineering performs cement core tests in its laboratory. The following standards

have been set for each core test performed:

During March, the laboratory performed 2,000 core tests. On March 1 no direct

materials (sand) were on hand. Variable manufacturing overhead is assigned to core

tests on the basis of standard direct labor-hours. The following events occurred during

March:

– 8,600 pounds of sand were purchased at a cost of $7,310.

– 7,200 pounds of sand were used for core tests.

– 840 actual direct labor-hours were worked at a cost of $8,610.

– Actual variable manufacturing overhead incurred was $3,200.

The materials price variance for March is:

A) $860 unfavorable

B) $860 favorable

C) $281 unfavorable

D) $281 favorable

Answer:

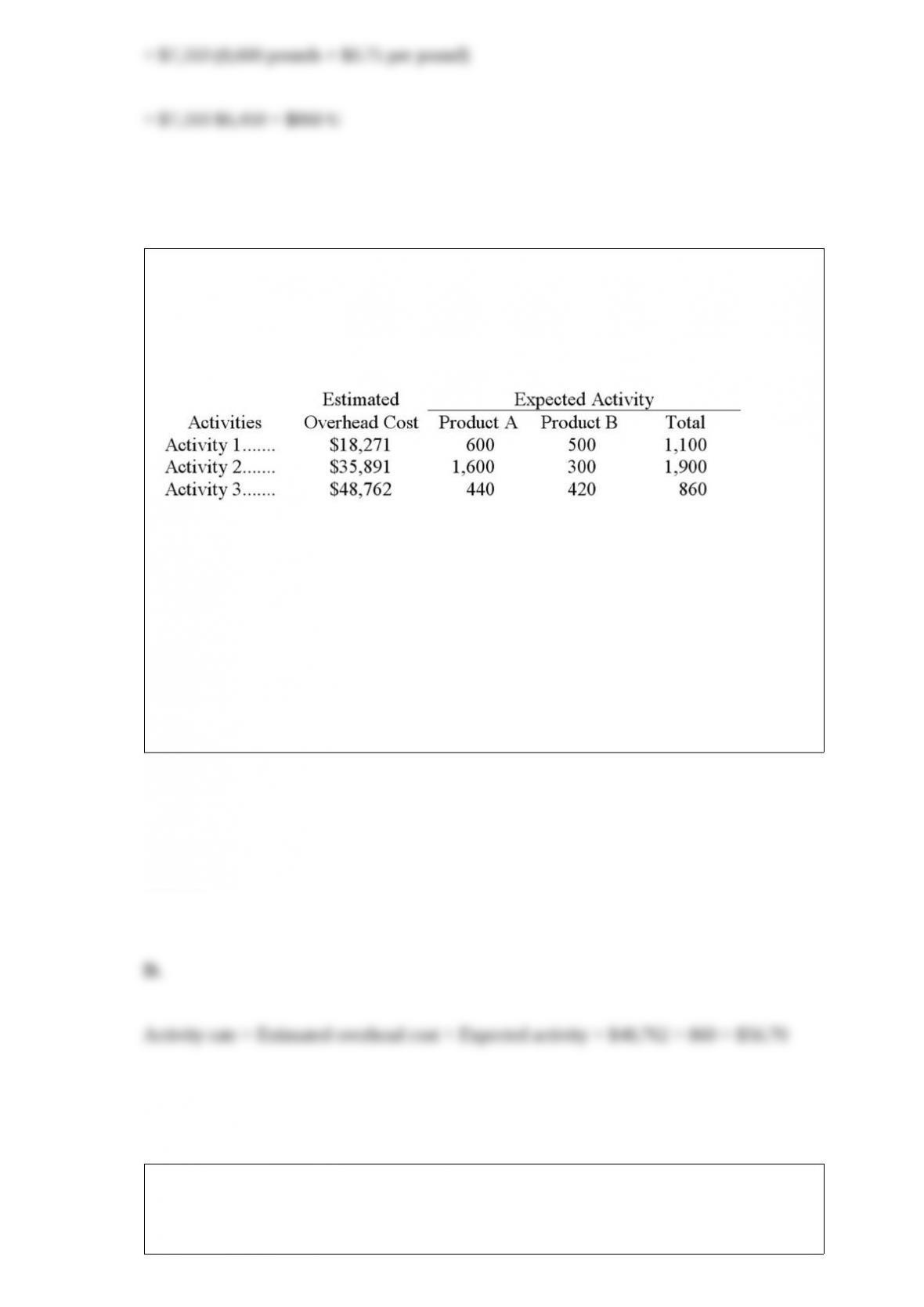

Accola Company uses activity-based costing. The company has two products: A and B.

The annual production and sales of Product A is 1,100 units and of Product B is 700

units. There are three activity cost pools, with estimated costs and expected activity as

follows:

The activity rate for Activity 3 is closest to:

A. $119.72

B. $116.18

C. $26.67

D. $56.70

Answer:

Hagos Corporation is working on its direct labor budget for the next two months. Each

unit of output requires 0.84 direct labor-hours. The direct labor rate is $9.40 per direct

labor-hour. The production budget calls for producing 2,100 units in June and 1,900

units in July. If the direct labor work force is fully adjusted to the total direct

labor-hours needed each month, what would be the total combined direct labor cost for

the two months?

A. $15,792.00

B. $15,002.40

C. $16,581.60

D. $31,584.00

Answer:

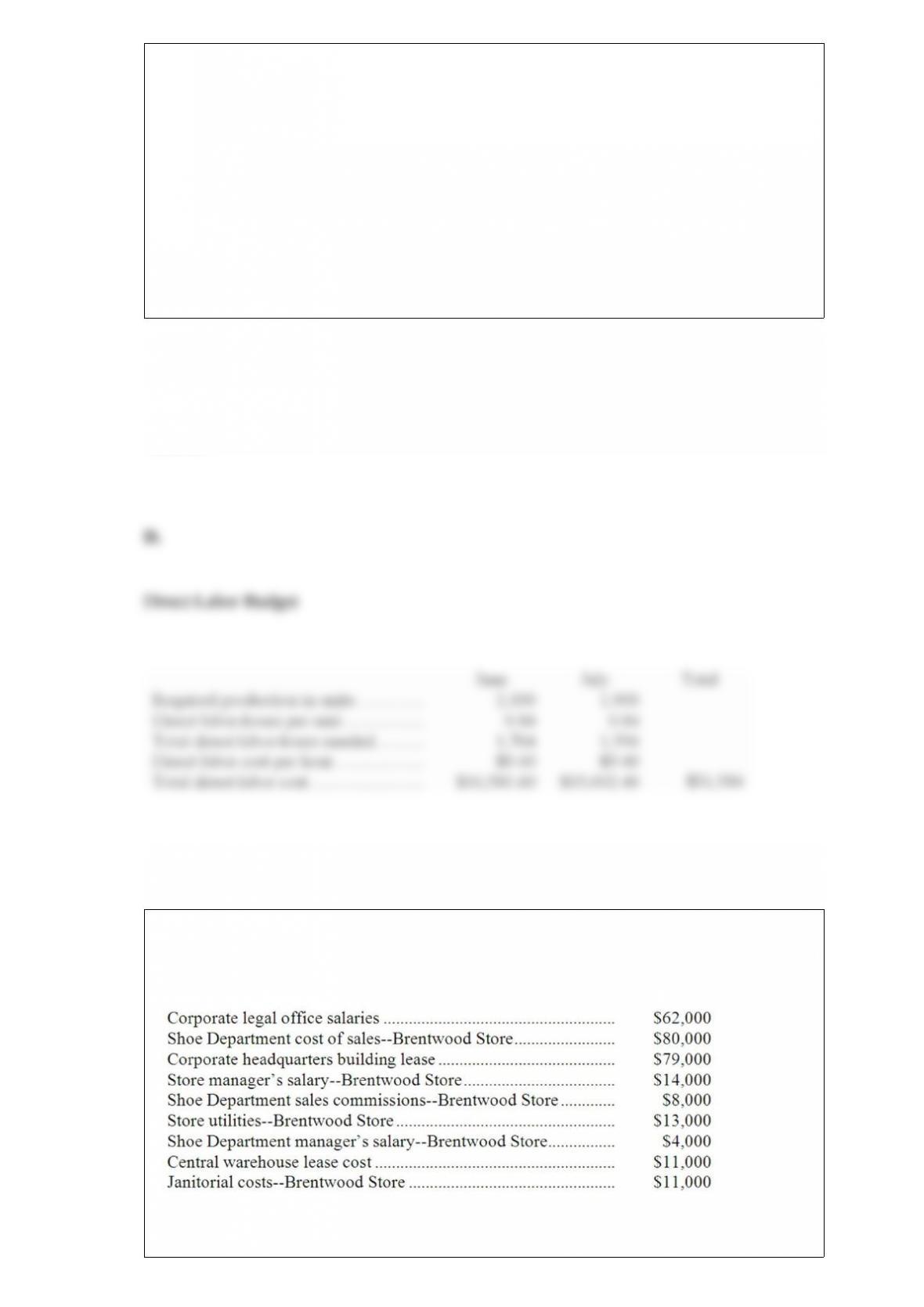

The following cost data pertain to the operations of Mancia Department Stores, Inc., for

the month of February.

The Brentwood Store is just one of many stores owned and operated by the company.

The Shoe Department is one of many departments at the Brentwood Store. The central

warehouse serves all of the company’s stores.

What is the total amount of the costs listed above that are NOT direct costs of the

Brentwood Store?

A. $152,000

B. $92,000

C. $79,000

D. $38,000

Answer:

Reference: 8-35

Sande Corporation makes a product with the following standard costs:

In November the companys budgeted production was 2,900 units but the actual

production was 3,000 units. The company used 27,670 grams of the direct material and

1,390 direct labor-hours to produce this output. During the month, the company

purchased 31,700 grams of the direct material at a cost of $196,540. The actual direct

labor cost was $29,607 and the actual variable overhead cost was $2,502.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The variable overhead rate variance for November is:

A) $300 U

B) $278 U

C) $300 F

D) $278 F

Answer:

In a process costing system, manufacturing overhead applied is usually recorded as a

debit to:

A. Finished goods.

B. Work in process.

C. Manufacturing overhead.

D. Cost of goods sold.

Answer:

Schleich Corporation’s most recent balance sheet appears below:

Net income for the year was $274. Cash dividends were $53. The company did not sell

or retire any property, plant, and equipment during the year. The net cash provided by

(used in) operating activities for the year was:

A. $286

B. $262

C. $391

D. $12

Answer:

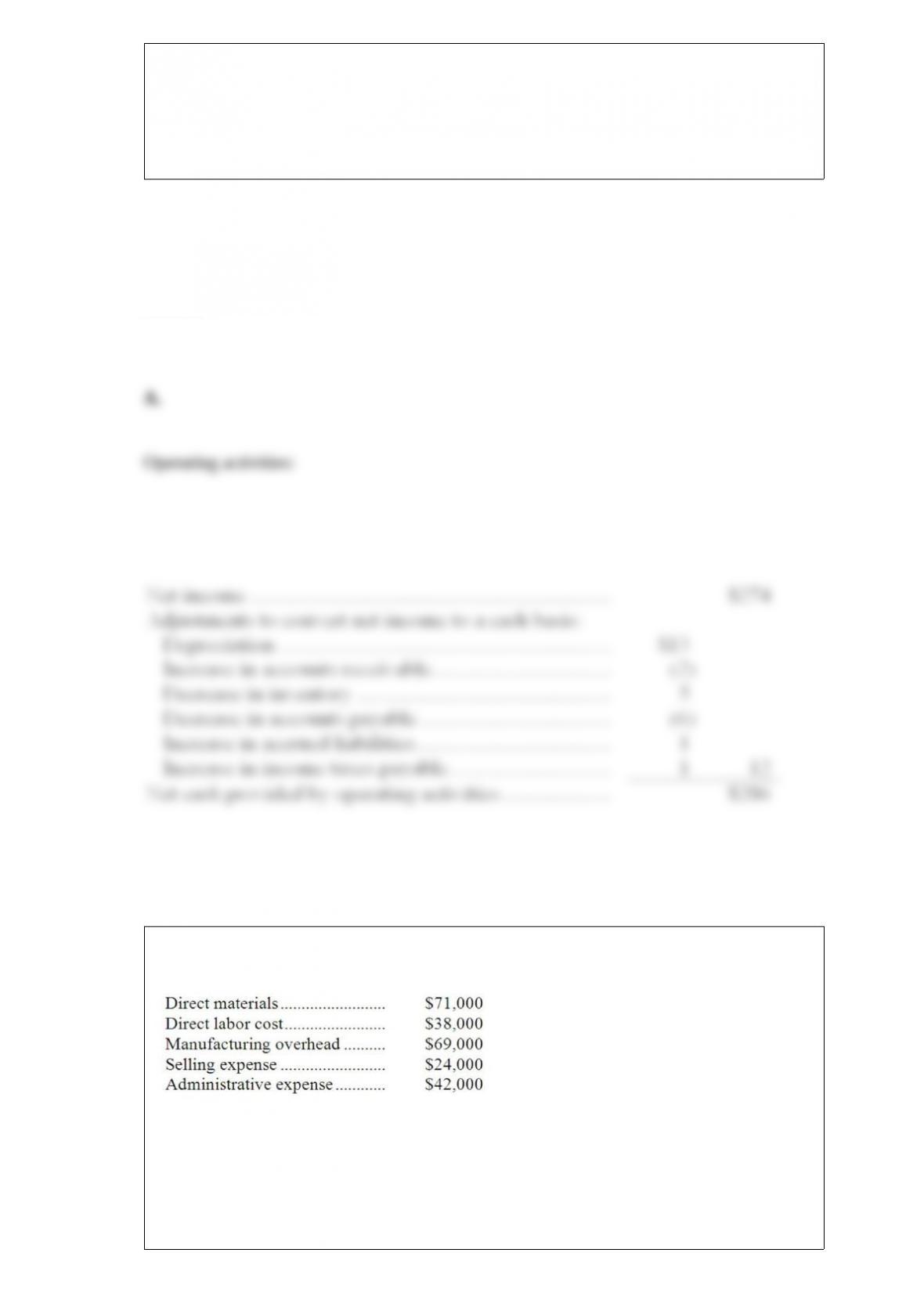

Dickison Corporation reported the following data for the month of December:

The prime cost for December was:

A. $109,000

B. $111,000

C. $107,000

D. $66,000

Answer:

Reference: 8-11

Doubleday Clinic uses client-visits as its measure of activity. During June, the clinic

budgeted for 3,200 client-visits, but its actual level of activity was 3,180 client-visits.

The clinic has provided the following data concerning the formulas to be used in its

budgeting for June:

The administrative expenses in the planning budget for June would be closest to:

A) $3,429

B) $3,408

C) $3,520

D) $3,518

Answer:

Davol Corporation is preparing its Manufacturing Overhead Budget for the fourth

quarter of the year. The budgeted variable manufacturing overhead rate is $6.80 per

direct labor-hour; the budgeted fixed manufacturing overhead is $72,000 per month, of

which $20,000 is factory depreciation.

If the budgeted direct labor time for October is 5,000 hours, then the total budgeted

manufacturing overhead for October is:

A. $52,000

B. $106,000

C. $54,000

D. $86,000

Answer:

Galino Company, which has only one product, has provided the following data

concerning its most recent month of operations:

The total gross margin for the month under the absorption costing approach is:

A. $49,400

B. $18,200

C. $73,400

D. $124,800

Answer:

The Gomez Company, a merchandising firm, has budgeted its activity for December

according to the following information:

– Sales at $500,000, all for cash.

– Merchandise Inventory on November 30 was $250,000.

– The cash balance at December 1 was $20,000.

– Selling and administrative expenses are budgeted at $50,000 for December and are

paid for in cash.

– Budgeted depreciation for December is $30,000.

– The planned merchandise inventory on December 31 is $260,000.

– The cost of goods sold represents 75% of the selling price.

– All purchases are paid for in cash.

The budgeted net income for December is:

A. $75,000

B. $45,000

C. $125,000

D. $65,000

Answer:

The Steff Company has the following flexible budget (in condensed form) for

manufacturing overhead:

The following data concerning production pertain to last year’s operations:

– The company used a denominator activity of 15,000 direct labor-hours to compute the

predetermined overhead rate.

– The company made 6,850 units of product and worked 14,200 actual hours during the

year.

– Actual variable manufacturing overhead was $15,904 and actual fixed manufacturing

overhead was $30, $850 for the year.

– The standard direct labor time is two hours per unit of product.

The variable element of the predetermined overhead rate was (per DLH):

A. $4.15

B. $3.00

C. $2.00

D. $1.15

Answer:

Excerpts from Goodrow Corporation’s most recent balance sheet and income statement

appear below:

Dividends on common stock during Year 2 totaled $20 thousand. Dividends on

preferred stock totaled $10 thousand. The market price of common stock at the end of

Year 2 was $5.34 per share.

The dividend yield ratio for Year 2 is closest to:

A. 2.81%

B. 66.67%

C. 1.87%

D. 0.94%

Answer:

Boole Corporation’s net cash provided by operating activities was $112; its capital

expenditures were $76; and its cash dividends were $31. The company’s free cash flow

was:

A. $36

B. $81

C. $219

D. $5

Answer:

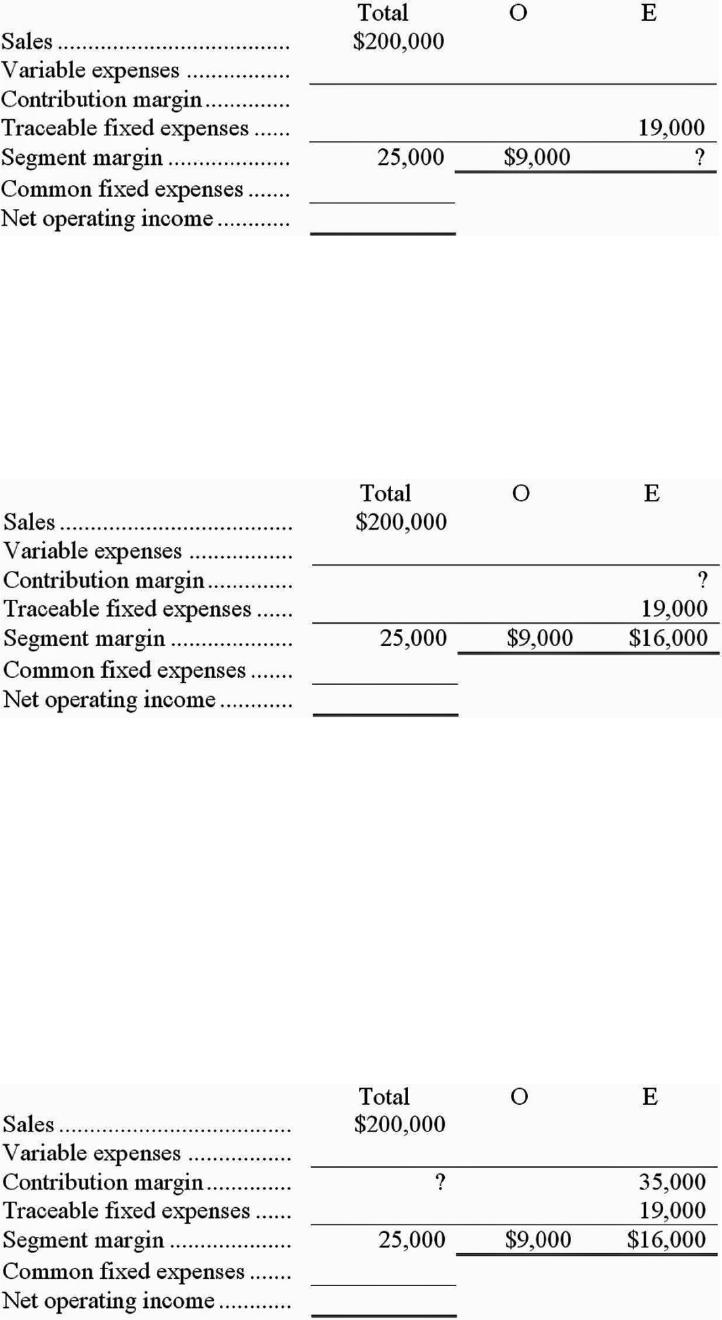

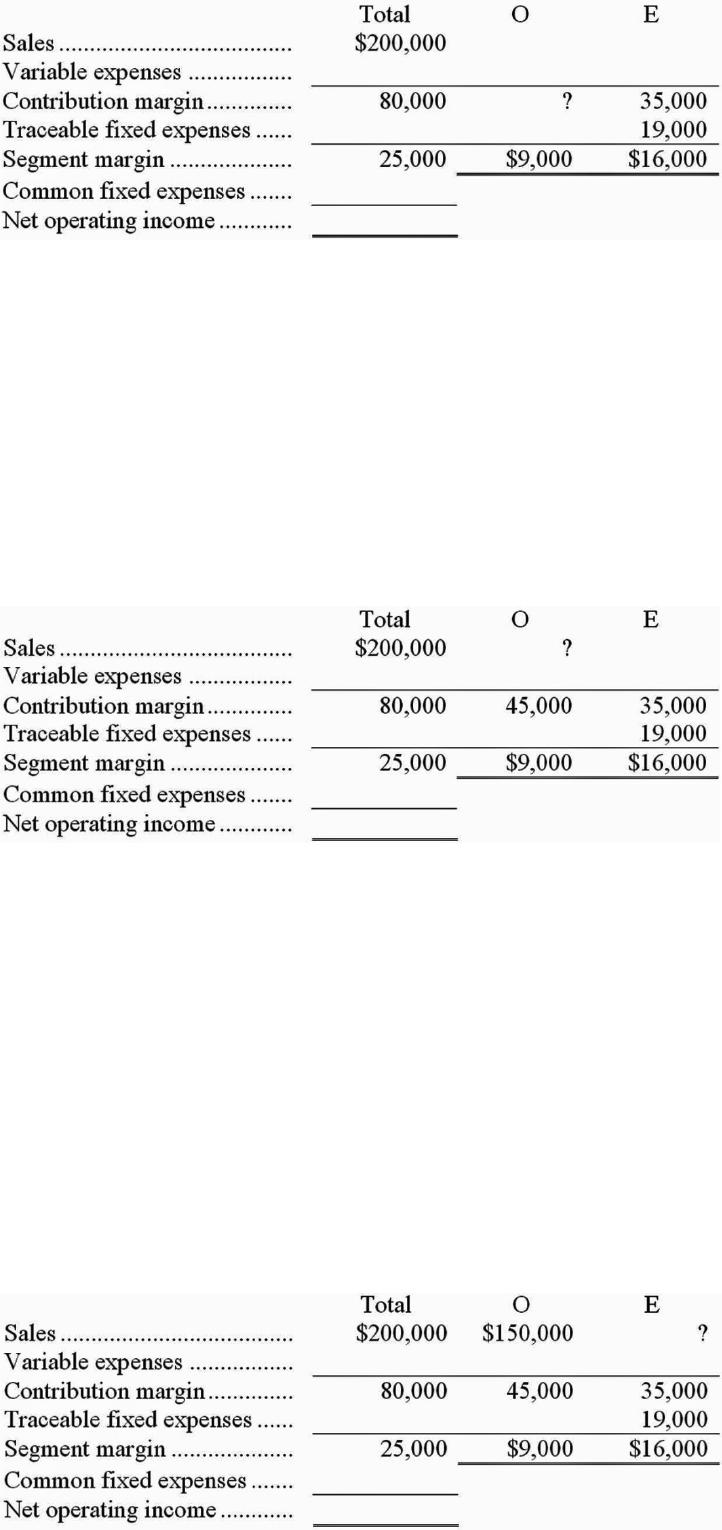

Hatch Company has two divisions, O and E. During the year just ended, Division O had

a segment margin of $9,000 and variable expenses equal to 70% of sales. Traceable

fixed expenses for Division E were $19,000. Hatch Company as a whole had a

contribution margin ratio of 40%, a segment margin of $25,000, and sales of $200,000.

Given this data, the sales for Division E for last year were:

A. $50,000

B. $150,000

C. $87,500

D. $116,667

Answer:

Which of the following formulas is used to calculate the contribution margin ratio?

A. (Sales – Fixed expenses) ÷ Sales

B. (Sales – Cost of goods sold) ÷ Sales

C. (Sales – Variable expenses) ÷ Sales

D. (Sales – Total expenses) ÷ Sales

Answer:

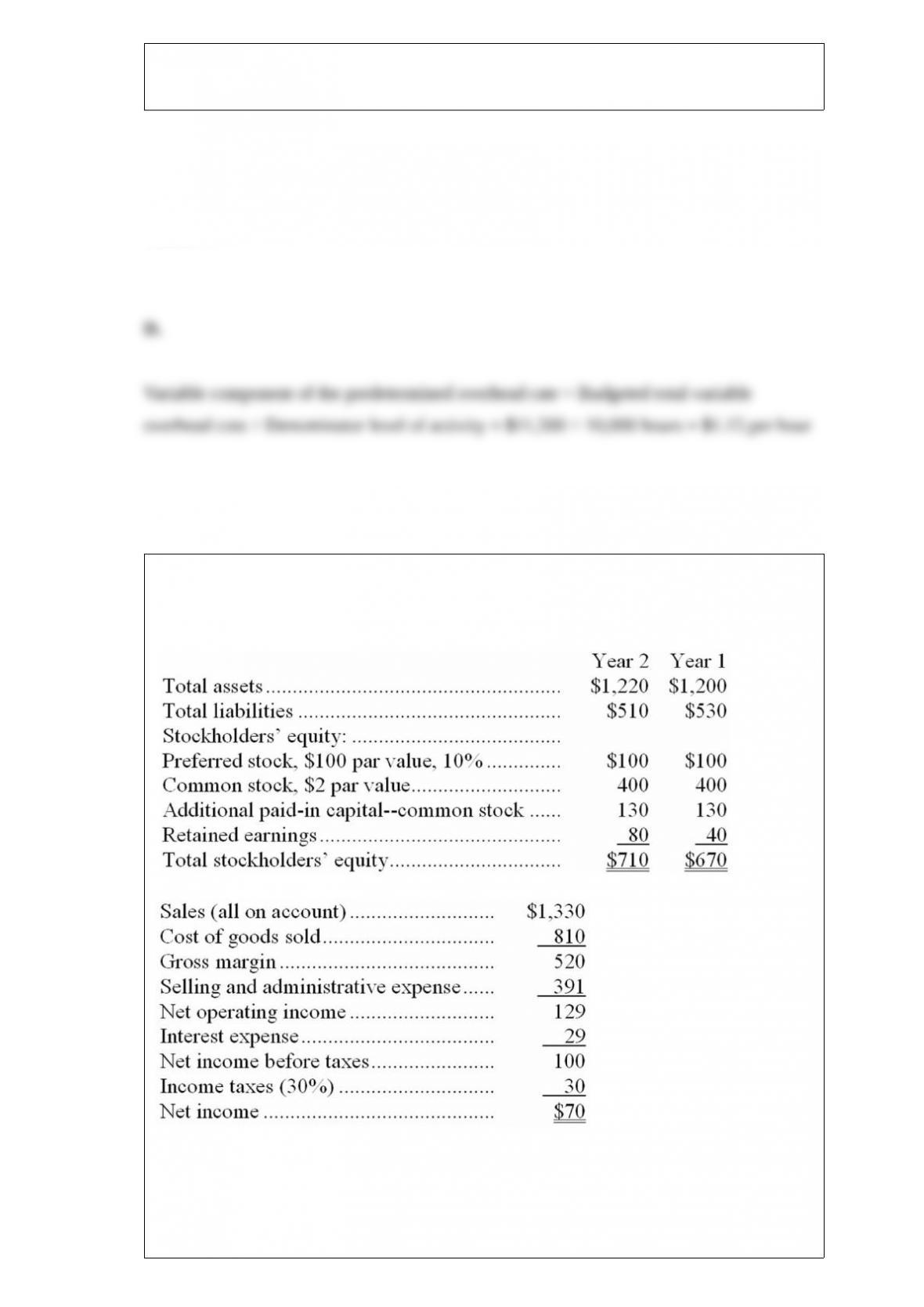

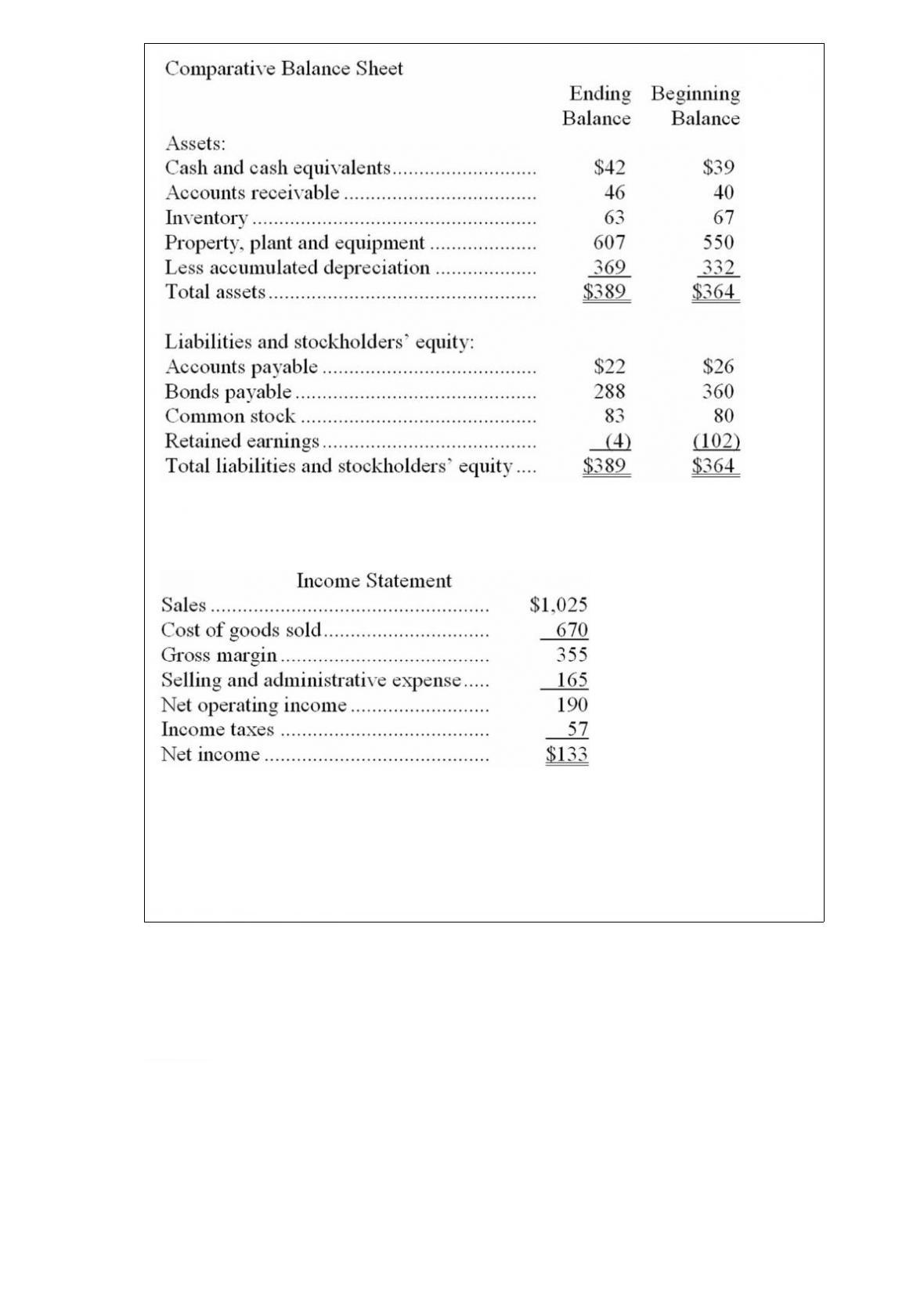

Kren Corporation’s balance sheet and income statement appear below:

Cash dividends were $35. The company did not dispose of any property, plant, and

equipment during the year.

Prepare the operating activities section of the statement of cash flows in good form

using the direct method.

Answer:

Answer:

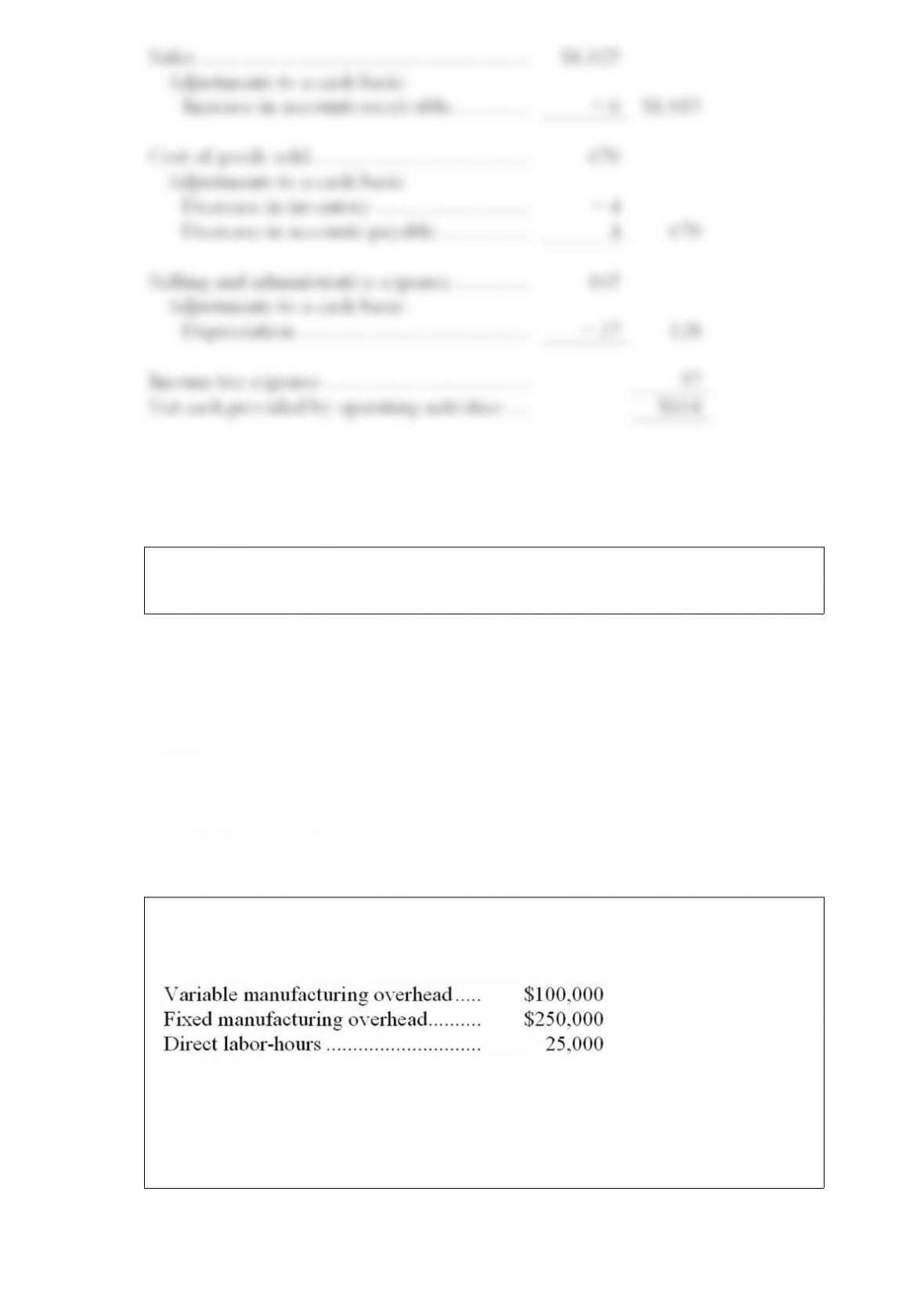

Bady Inc. makes a range of products. The company’s predetermined overhead rate is

$14 per direct labor-hour, which was calculated using the following budgeted data:

Component M3 is used in one of the company’s products. The unit cost of the

component according to the company’s cost accounting system is determined as

follows:

An outside supplier has offered to supply component M3 for $108 each. The outside

supplier is known for quality and reliability. Assume that direct labor is a variable cost,

variable manufacturing overhead is really driven by direct labor-hours, and total fixed

manufacturing overhead would not be affected by this decision. Bady chronically has

idle capacity.

Is the offer from the outside supplier financially attractive? Why?

Answer:

Candice Corporation has decided to introduce a new product. The product can be

manufactured using either a capital-intensive or labor-intensive method. The

manufacturing method will not affect the quality or sales of the product. The estimated

manufacturing costs of the two methods are as follows:

The company’s market research department has recommended an introductory selling

price of $30 per unit for the new product. The annual fixed selling and administrative

expenses of the new product are $500,000. The variable selling and administrative

expenses are $2 per unit regardless of how the new product is manufactured.

a. Calculate the break-even point in units if Candice Corporation uses the:

1/ capital-intensive manufacturing method.

2/ labor-intensive manufacturing method.

b. Determine the unit sales volume at which the net operating income is the same for

the two manufacturing methods.

c. Assuming sales of 250,000 units, what is the degree of operating leverage if the

company uses the:

1/ capital-intensive manufacturing method.

2/ labor-intensive manufacturing method.

d. What is your recommendation to management concerning which manufacturing

method should be used?

Answer:

Whitman Corporation, a merchandising company, reported sales of 7,400 units for May

at a selling price of $677 per unit. The cost of goods sold (all variable) was $441 per

unit and the variable selling expense was $54 per unit. The total fixed selling expense

was $155,600. The variable administrative expense was $24 per unit and the total fixed

administrative expense was $370,400.

a. Prepare a contribution format income statement for May.

b. Prepare a traditional format income statement for May.

Answer:

Job 434 was recently completed. The following data have been recorded on its job cost

sheet:

The company applies manufacturing overhead on the basis of machine-hours. The

predetermined overhead rate is $12 per machine-hour.

Compute the unit product cost that would appear on the job cost sheet for this job.

Answer:

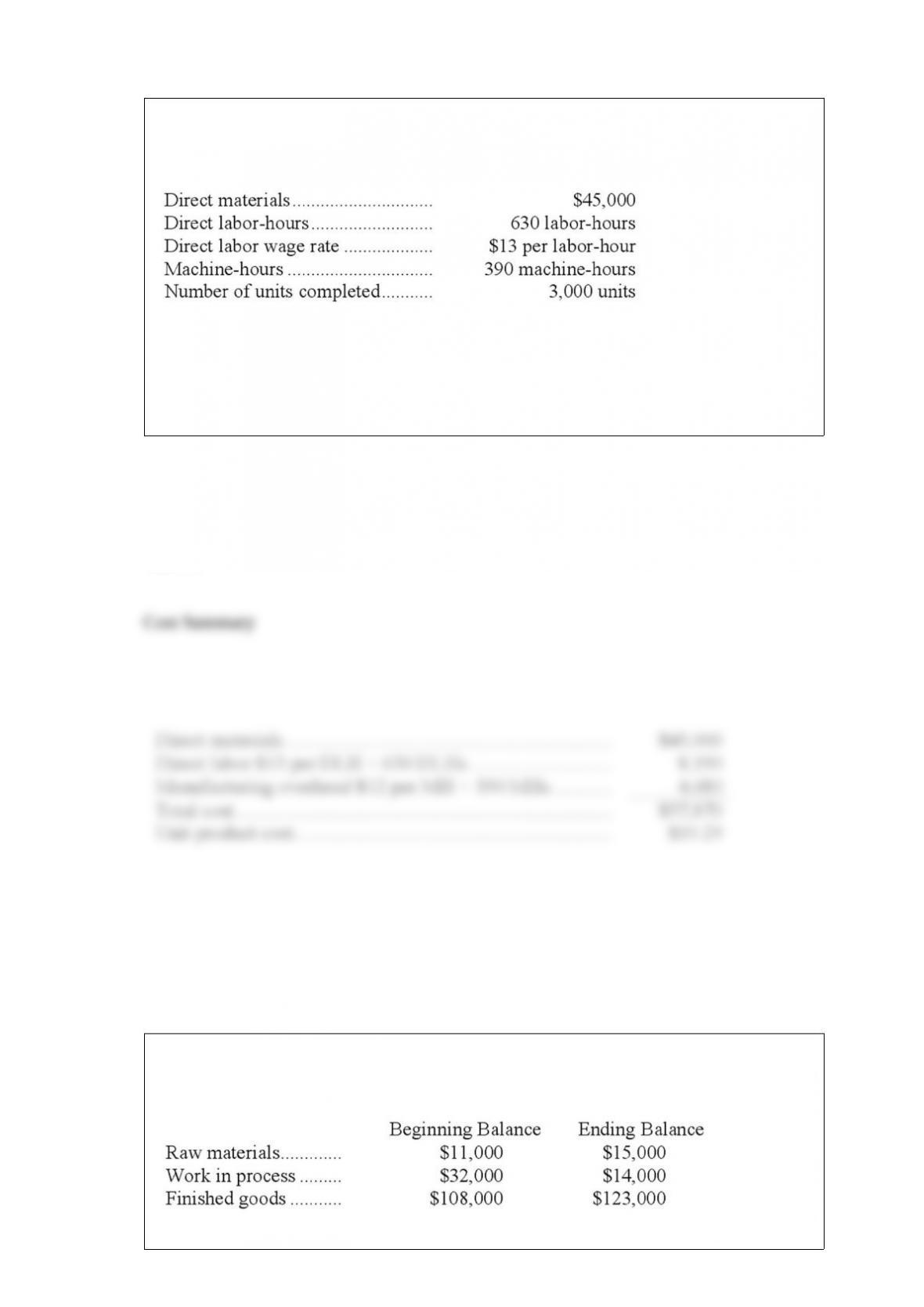

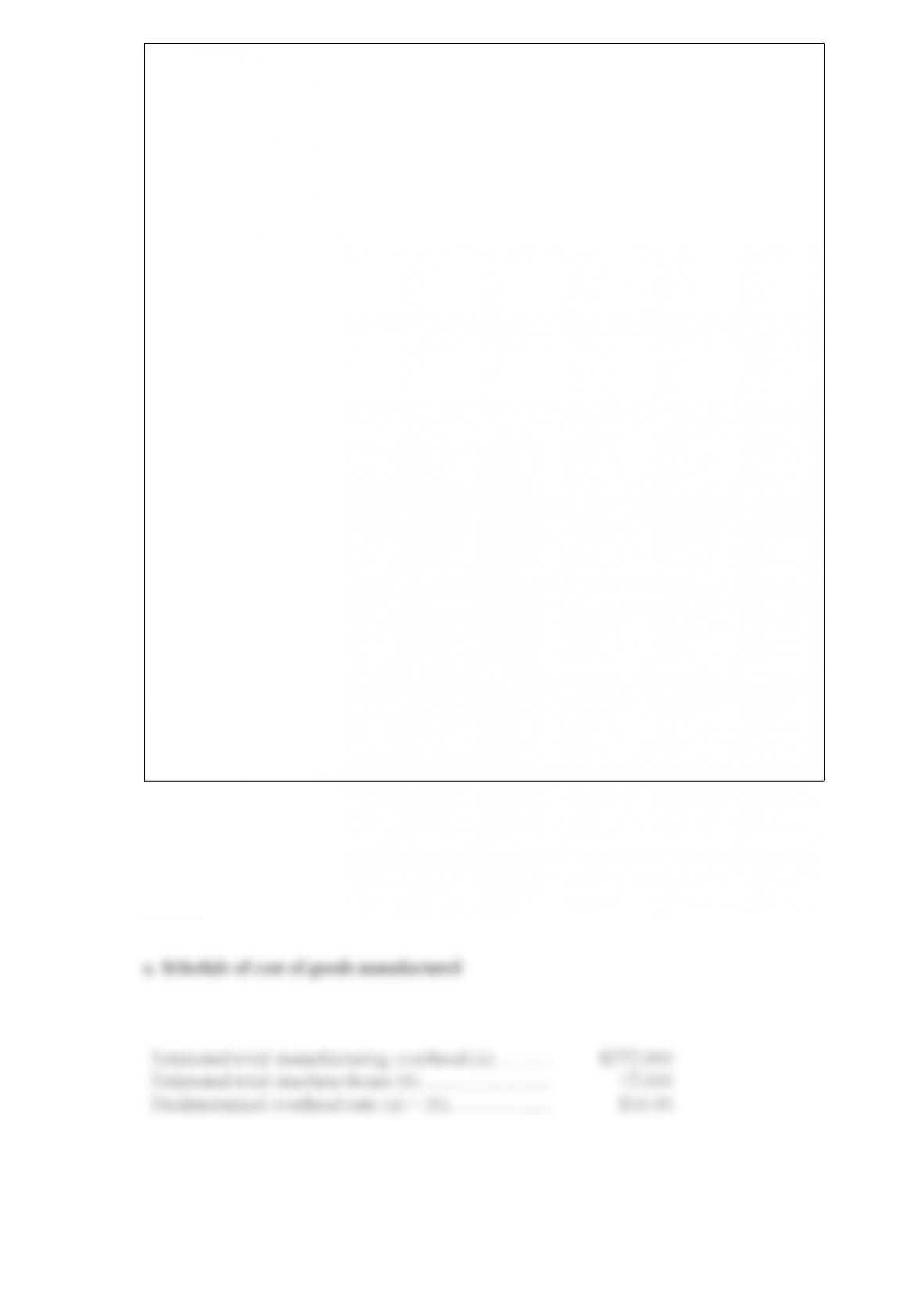

Babb Company is a manufacturing firm that uses job-order costing. The company’s

inventory balances were as follows at the beginning and end of the year:

The company applies overhead to jobs using a predetermined overhead rate based on

machine-hours. At the beginning of the year, the company estimated that it would work

17,000 machine-hours and incur $272,000 in manufacturing overhead cost. The

following transactions were recorded for the year:

– Raw materials were purchased, $416,000.

– Raw materials were requisitioned for use in production, $412,000 $(376,000 direct

and $36,000 indirect).

– The following employee costs were incurred: direct labor, $330,000; indirect labor,

$69,000; and administrative salaries, $157,000.

– Selling costs, $113,000.

– Factory utility costs, $29,000.

– Depreciation for the year was $121,000 of which $114,000 is related to factory

operations and $7,000 is related to selling, general, and administrative activities.

– Manufacturing overhead was applied to jobs. The actual level of activity for the year

was 15,000 machine-hours.

– Sales for the year totaled $1,282,000.

a. Prepare a schedule of cost of goods manufactured in good form.

b. Was the overhead underapplied or overapplied? By how much?

c. Prepare an income statement for the year in good form. The company closes any

underapplied or overapplied manufacturing overhead to Cost of Goods Sold.

Answer:

During October, Keliihoomalu Clinic budgeted for 2,700 patient-visits, but its actual

level of activity was 2,200 patient-visits. Revenue should be $27.30 per patient-visit.

Personnel expenses should be $21,100 per month plus $6.80 per patient-visit. Medical

supplies should be $500 per month plus $4.90 per patient-visit. Occupancy expenses

should be $5,700 per month plus $0.90 per patient-visit. Administrative expenses

should be $3,700 per month plus $0.40 per patient-visit.

Required:

Prepare the clinics flexible budget for October based on the actual level of activity for

the month.

Answer:

Qu Company, which has only one product, has provided the following data concerning

its most recent month of operations:

a. What is the unit product cost for the month under variable costing?

b. Prepare a contribution format income statement for the month using variable costing.

c. Without preparing an income statement, determine the absorption costing net

operating income for the month. (Hint: Use the reconciliation method.)

Answer:

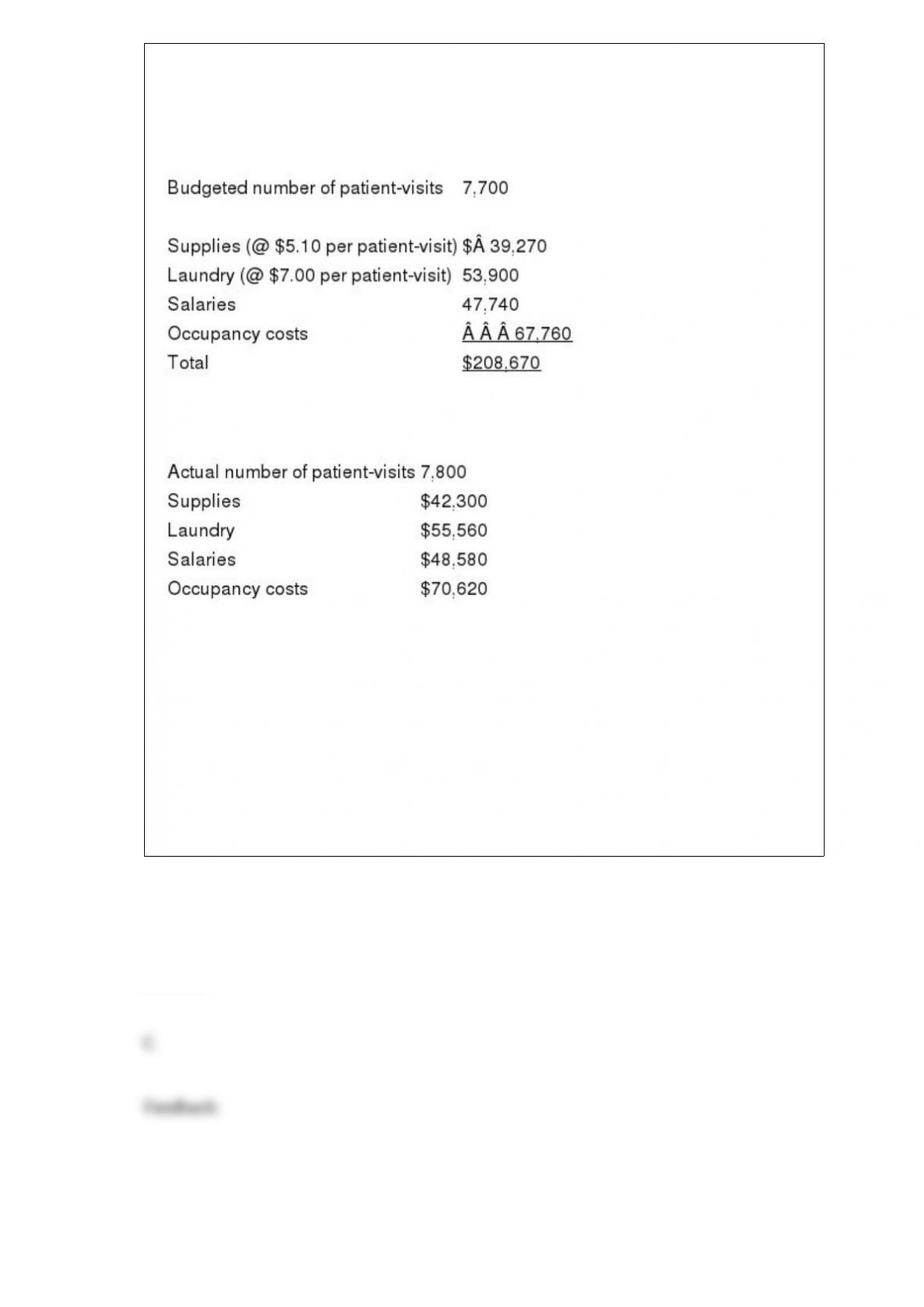

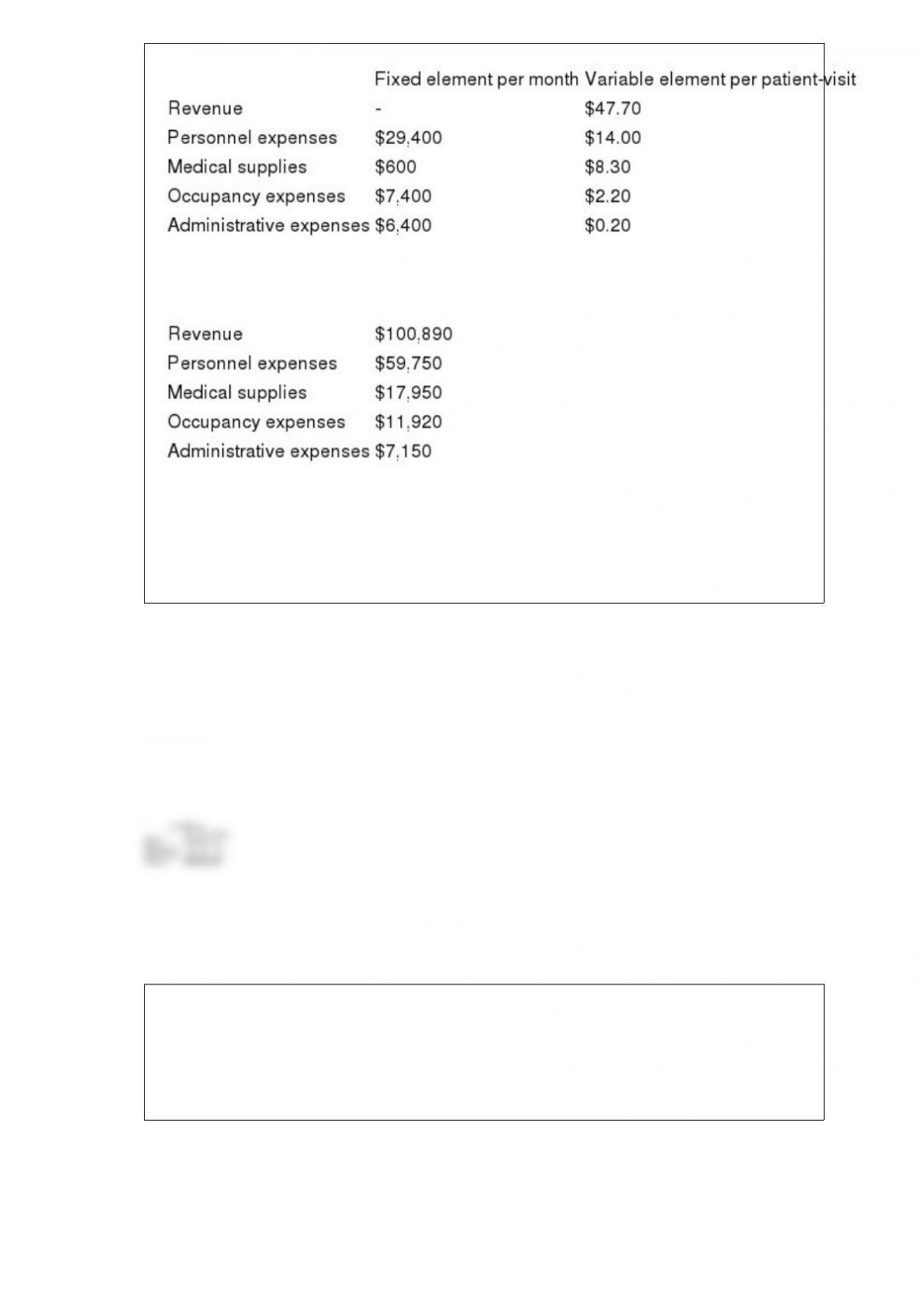

Carlisle Clinic uses patient-visits as its measure of activity. During December, the clinic

budgeted for 2,500 patient-visits, but its actual level of activity was 2,100 patient-visits.

The clinic has provided the following data concerning the formulas used in its

budgeting and its actual results for December:

Data used in budgeting:

Actual results for December:

Required:

Prepare a report showing the clinics revenue and spending variances for December.

Label each variance as favorable (F) or unfavorable (U).

Answer:

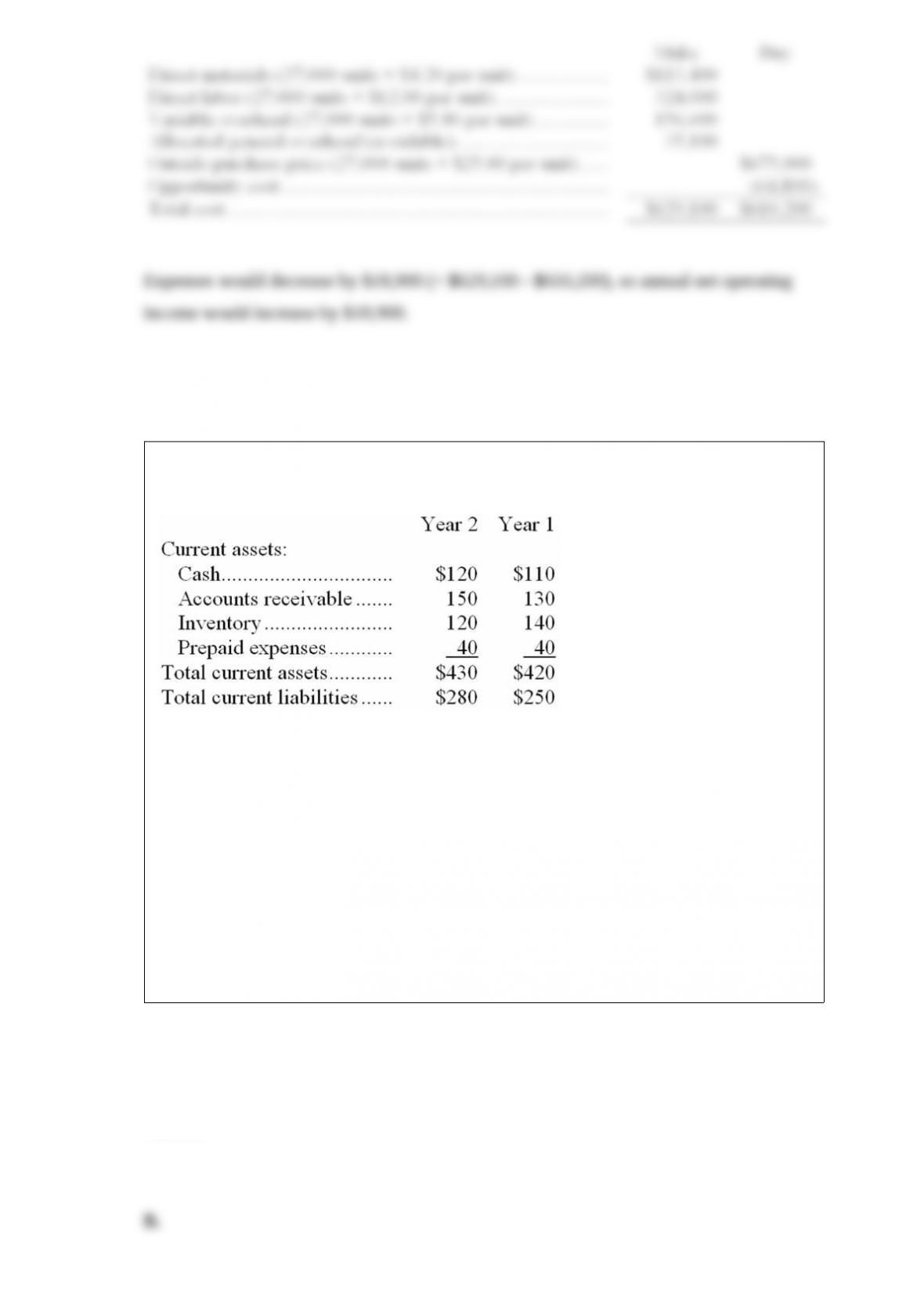

Heningburg Corporation’s total current assets are $230,000, its noncurrent assets are

$530,000, its total current liabilities are $140,000, its long-term liabilities are $370,000,

and its stockholders’ equity is $250,000.

Compute the company’s working capital. Show your work!

Answer:

Froment Inc. uses the FIFO method in its process costing system. The following data

concern the operations of the company’s first processing department for a recent month.

Using the FIFO method, determine the equivalent units of production for materials and

conversion costs.

Answer:

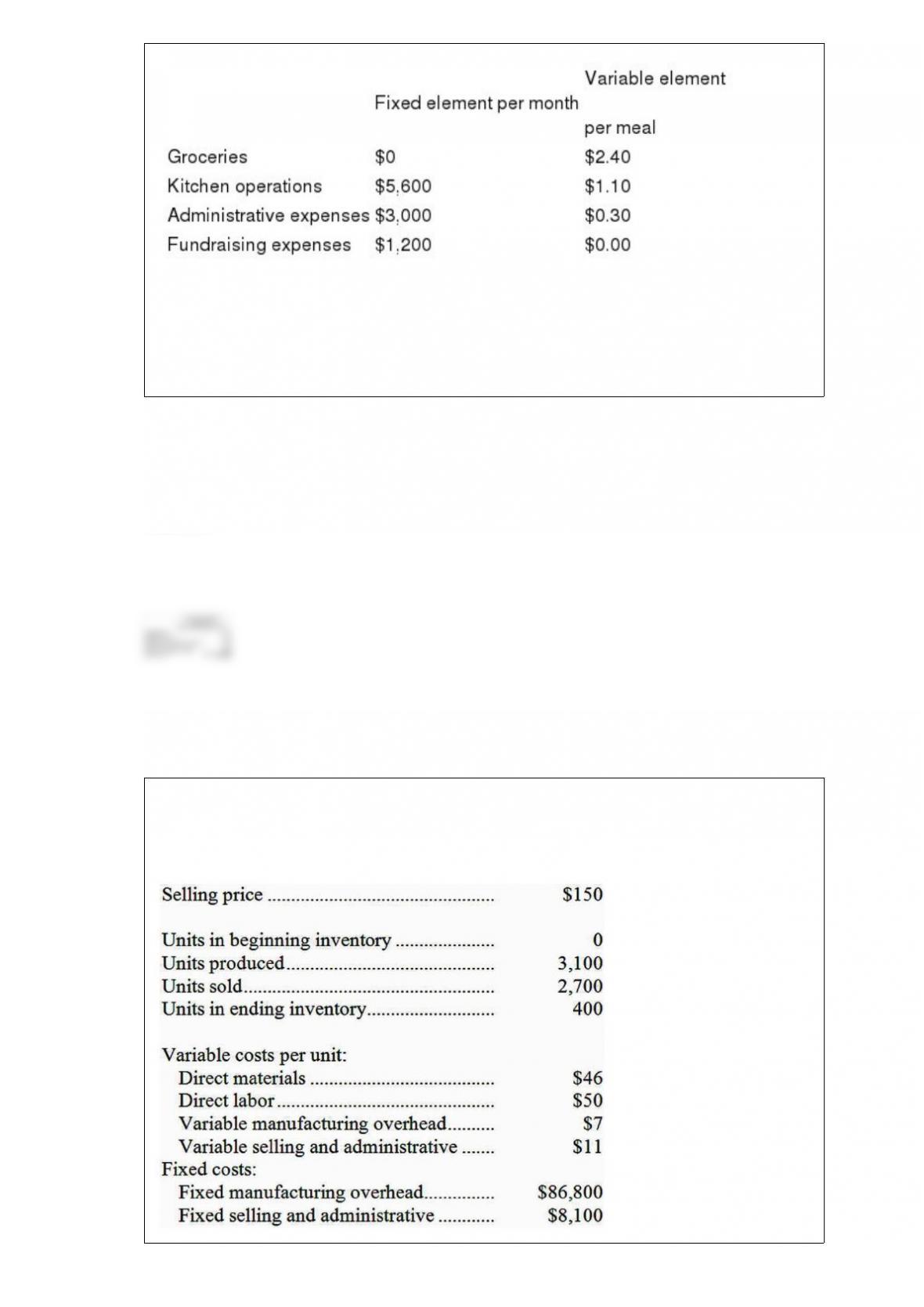

Barona Memorial Diner is a charity supported by donations that provides free meals to

the homeless. The diners budget for March was based on 2,900 meals, but the diner

actually served 3,000 meals. The diners director has provided the following cost

formulas to use in budgets:

Required:

Prepare the diners flexible budget for the actual number of meals served in March. The

budget will only contain the costs listed above; no revenues will be on the budget.

Answer:

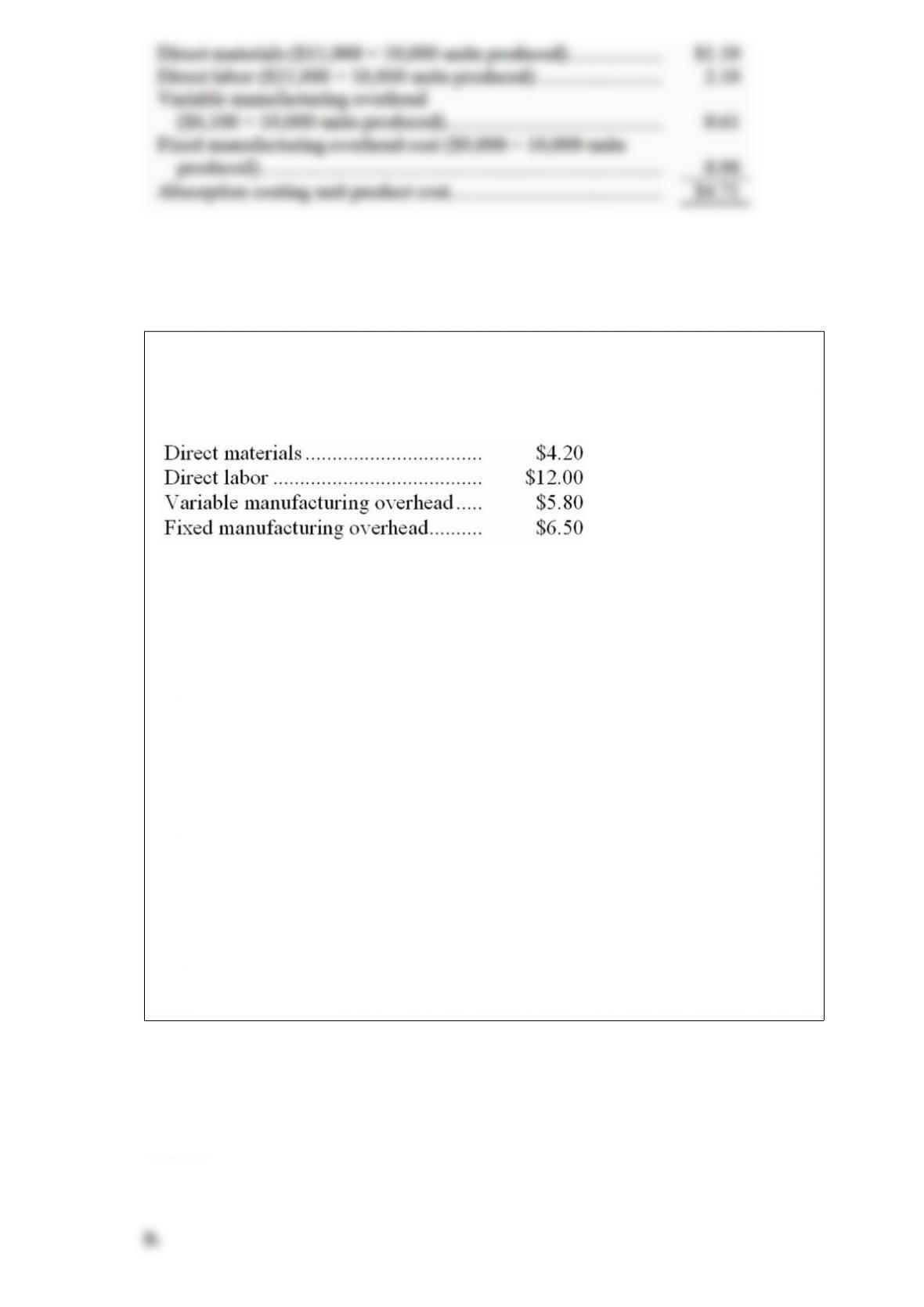

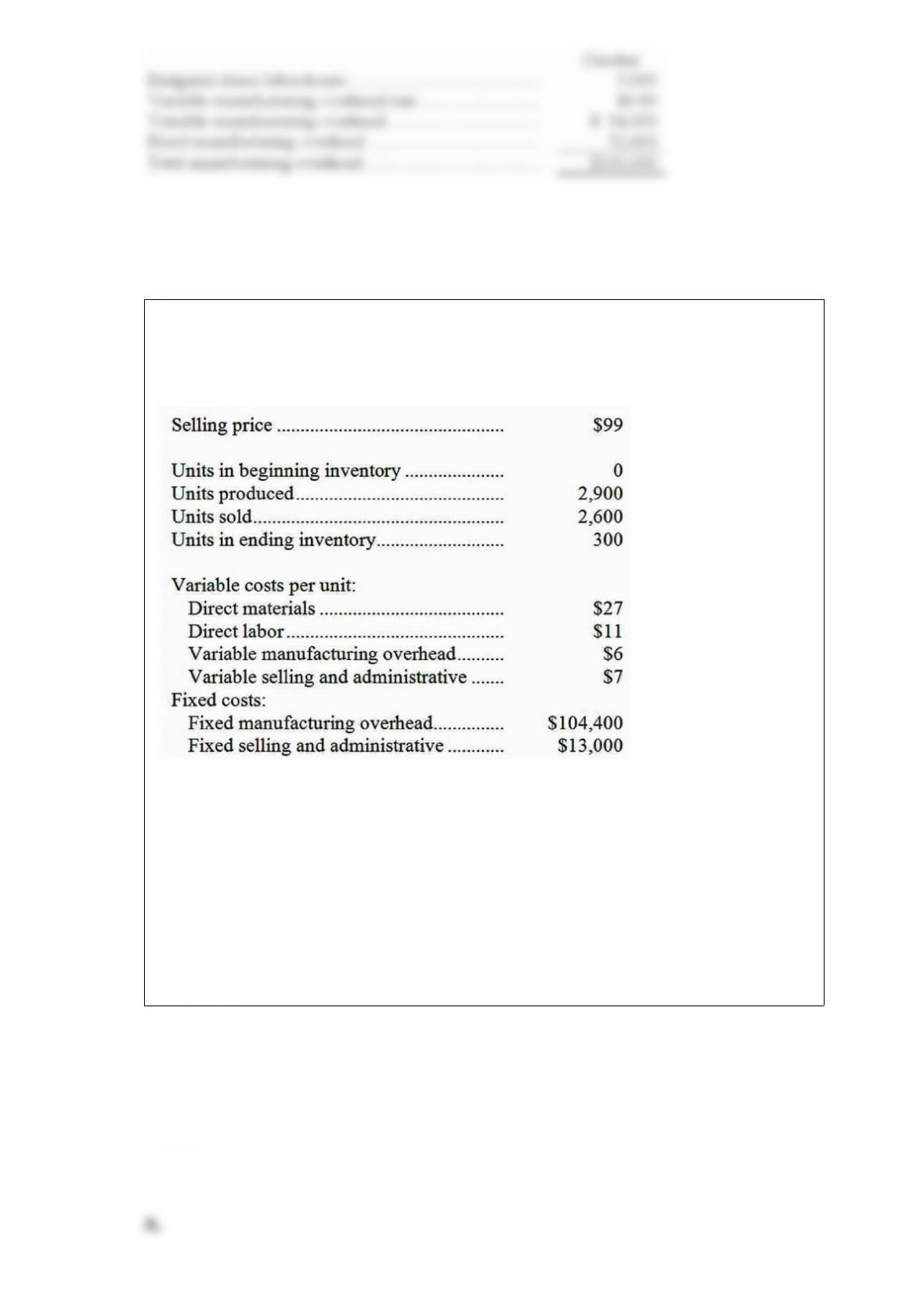

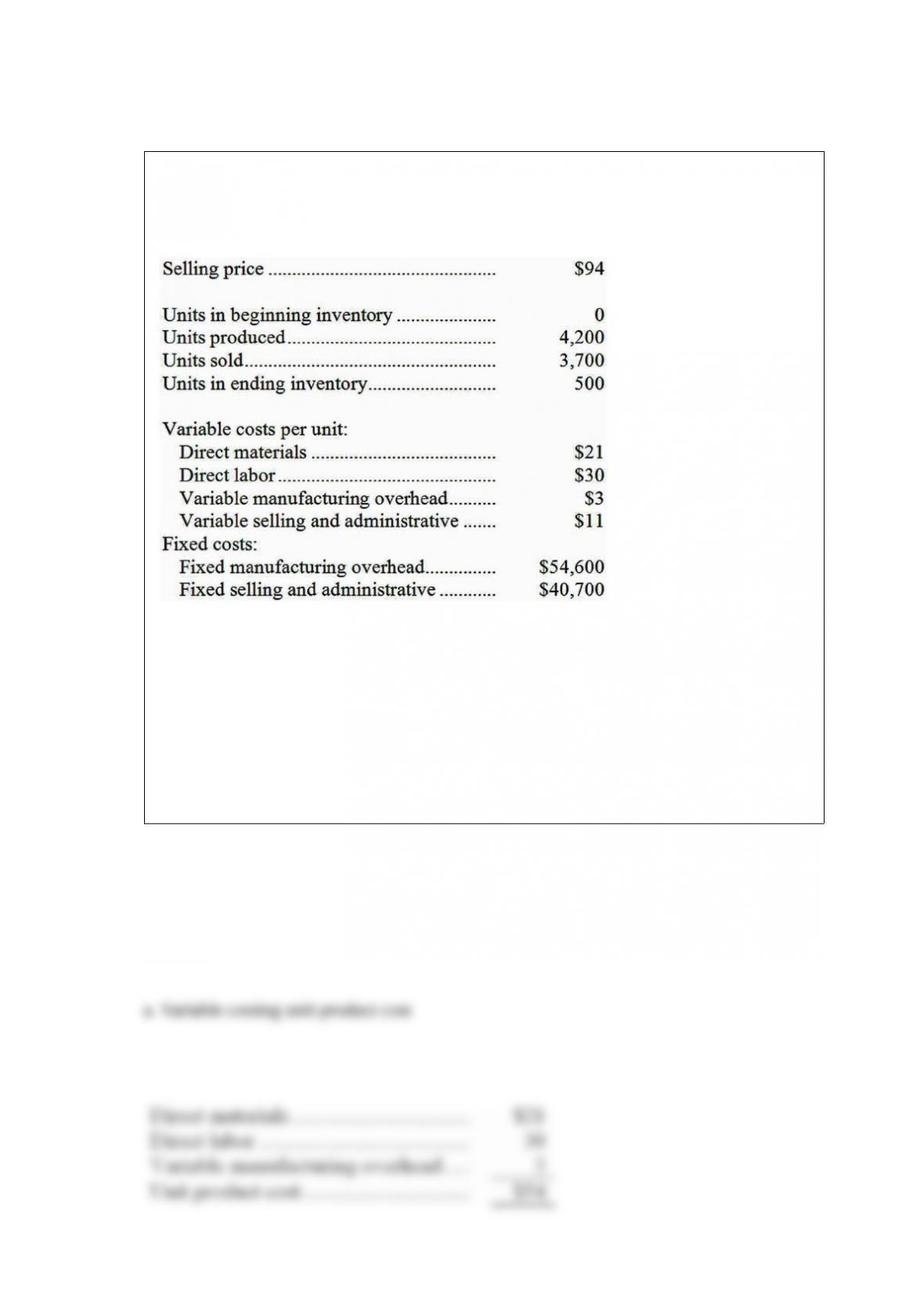

Maga Company, which has only one product, has provided the following data

concerning its most recent month of operations:

a. What is the unit product cost for the month under variable costing?

b. What is the unit product cost for the month under absorption costing?

c. Prepare a contribution format income statement for the month using variable costing.

d. Prepare an income statement for the month using absorption costing.

e. Reconcile the variable costing and absorption costing net operating incomes for the

month.

Answer:

Answer: