Effective internal control over accounts receivable ensures:

A. That credit is only extended to customers that meet the company’s credit standards.

B. That an approved factor is used when the company sells its accounts receivable.

C. There is an accurate accounting for cash receipts, cash disbursements, and cash

balances.

D. The availability of adequate cash for conducting business operations.

The cost of the employee who installs the leather on the seats of a new automobile

would be considered:

A. Manufacturing overhead.

B. Indirect labor.

C. Direct material.

D. Direct labor.

Craig Corporation’s reported net income for 2015 is less than its net cash flow from

operating activities. One reason for this could be:

A. The sale of machinery at a loss in 2015.

B. An increase in inventory levels during 2015.

C. The sale of investments at a gain in 2015.

D. An error in the preparation of the statement of cash flows; net income should be

greater than or equal to net cash flow from operating activities.

Rochester, Inc. purchased cameras from a Japanese company at a price of 4 million yen.

On the purchase date, the exchange rate was $0.0100 per Japanese yen, but when

Rochester, Inc., paid the liability, the exchange rate was $0.0103 per yen. When this

foreign account payable was paid, Rochester, Inc., recorded a:

A. Debit to Inventory of $1,200.

B. Loss of $1,200.

C. Credit to Accounts Payable of $41,200.

D. Gain of $1,200.

Which of the following is not a basic means of achieving internal control over cash

receipts?

A. Separate the functions of cash handling and maintenance of accounting records.

B. Prepare a daily listing of cash received through the mail.

C. Deposit all cash receipts daily in the petty cash fund.

D. Promptly reconcile bank statements with the accounting records.

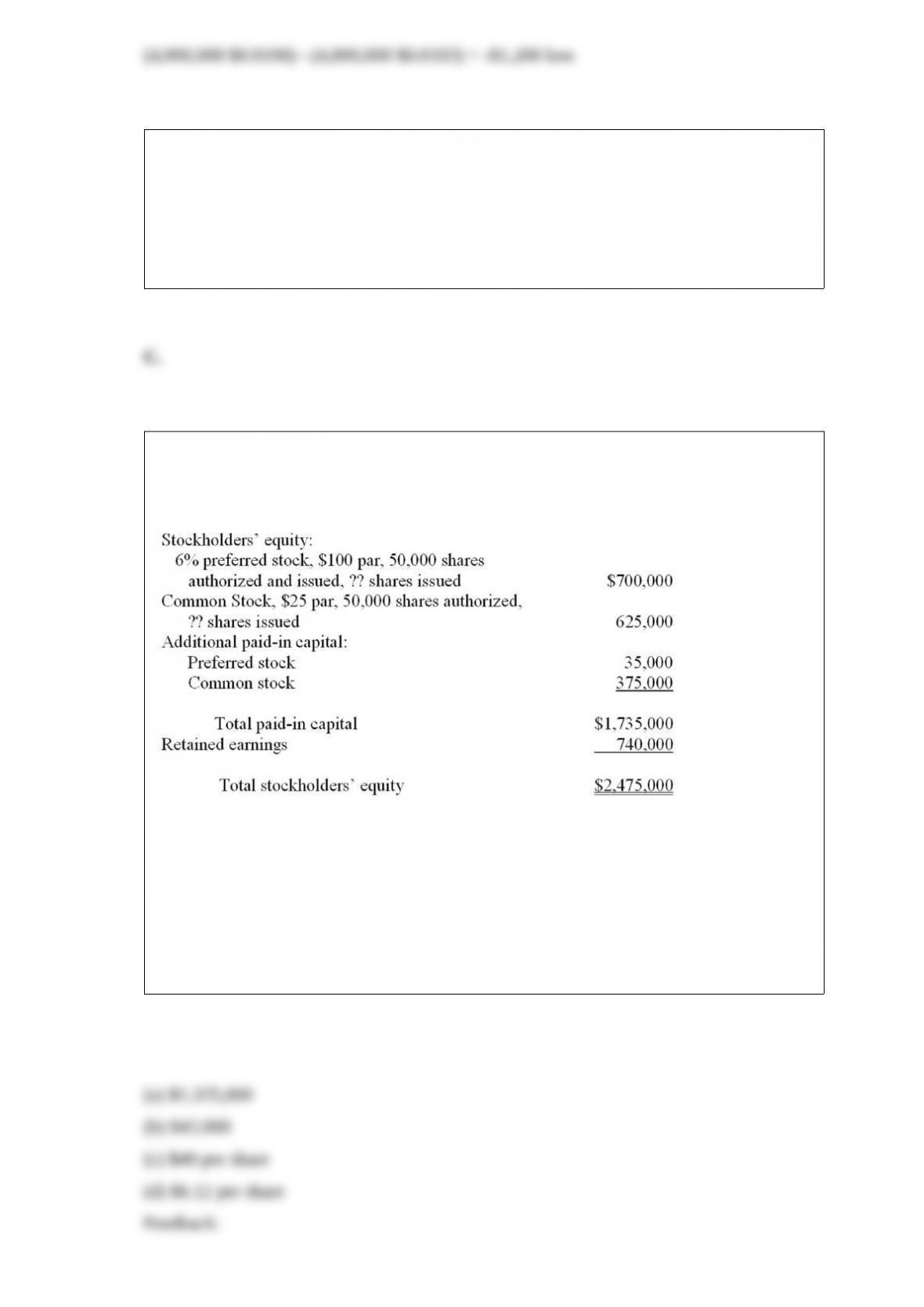

Interpreting the stockholders’ equity section

The stockholders’ equity section of the balance sheet of Benson Corporation (with

certain details omitted) appears below:

Answer the following questions based on the stockholders’ equity section given above.

(a) What is the total amount of legal capital?

(b) What is the total amount of dividends paid annually to the preferred stockholders?

(c) What is the average issue price of a share of common stock?

(d) The balance in retained earnings at the beginning of the current year was $575,000,

and there were no dividends in arrears. Net income for the current year was $360,000.

What is the amount of the dividends declared on each share of common stock during

the current year?

If the unit sales price is $7 and variable costs are $3, how many units have to be sold to

earn a profit of $3,600 if fixed costs equal $5,000?

A. 900 units.

B. 1,250 units.

C. 1,500 units.

D. 2,150 units.

The following entry appears in Galloway Paints general journal on April 23, 2015:

Refer to the information above. Before the journal entry above, Galloway had assets of

$450,000; liabilities of $230,000; and owners’ equity of $220,000. Total assets

immediately after the above transaction has been recorded amount to:

A. $430,000.

B. $450,000.

C. $470,000.

D. $476,000.

A job order cost system would be appropriate in the manufacturing of:

A. Paints.

B. Custom-made furniture.

C. Breakfast cereal.

D. Standard-grade plywood.

Which of the following is considered a return “on” investment?

A. Dividends.

B. Repayment of a loan.

C. Purchase of an asset.

D. Securing a loan.

Which of the following is a characteristic of a corporation?

A. Declaration of a dividend by the stockholders.

B. Appointment of officers by the stockholders.

C. Transferability of shares of stock.

D. Unlimited liability.

Cardinal Company’s bank statement showed a balance at May 31 of $180,974. The only

reconciling items consisted of a large number of outstanding checks totaling $51,847.

At May 31, what balance should Cardinal’s Cash account show?

A. $232,821.

B. $129,127.

C. $77,280.

D. $180,794.

All of the following statements are true of an income statement except:

A. The period of time covered by an income statement is the company’s accounting

period.

B. A fiscal year is any accounting period less than 12 months in length.

C. The length of a company’s accounting period may vary.

D. Every business prepares an annual income statement.

On September 1, 2015, Select Company borrowed $600,000 from a bank and signed a

12%, six-month note payable, with interest on the note due at maturity.

Refer to the information above. The total amount of the current liability (including

interest payable) for this loan that appears in Select Company’s balance sheet at

December 31, 2015, is:

A. $600,000.

B. $624,000.

C. $636,000.

D. $672,000.

The amount of owners’ equity in a business is not affected by:

A. The percentage of total assets held in cash.

B. The investments made in the business by the owner.

C. The profitability of the business.

D. The amount of dividends paid to stockholders.

On April 1, Year 1, Greenway Corporation issues $20 million of 10%, 20-year bonds

payable at par. Interest on the bonds is payable semiannually each April 1 and October

1.

Refer to the information above. The adjusting entry (if any) required on December 31,

Year 1, related to this bond issue involves:

A. Recognition of interest expense of $1,000,000.

B. Recognition of interest expense of $500,000.

C. A credit to Interest Payable of $2,000,000.

D. A credit to Cash of $500,000.

Which of the following statements is considered a “snapshot” of the business in

financial or dollar terms?

A. Statement of financial position.

B. Statement of cash flows.

C. Income statement.

D. The federal income tax return.

The ownership of common stock in a corporation usually carries the following rights:

A. To vote for directors.

B. To declare dividends.

C. To share in a distribution of assets if the corporation is to be liquidated.

D. Both to vote for directors and share in a distribution of assets if the corporation is to

be liquidated.

When the maker of a note defaults:

A. An account receivable is recorded for the principal amount of the note only.

B. An account receivable is recorded in the amount of the principal plus interest through

the maturity date.

C. Any interest earned for the current period is not recorded, since the maker has

defaulted.

D. Any interest earned in a previous period that has already been recorded as interest

receivable is written off as a loss due to the maker’s default.

Refer to the information above. In a trial balance prepared at December 31, 2014 the

total of the debit column is:

A. $1,540,000.

B. $780,000.

C. $1,020,000.

D. $700,000.

If an asset is determined to be impaired, it should be:

A. Depreciated only using the straight-line method.

B. Written up to its historical cost.

C. Reclassified as a liability.

D. Written down to its fair market value.

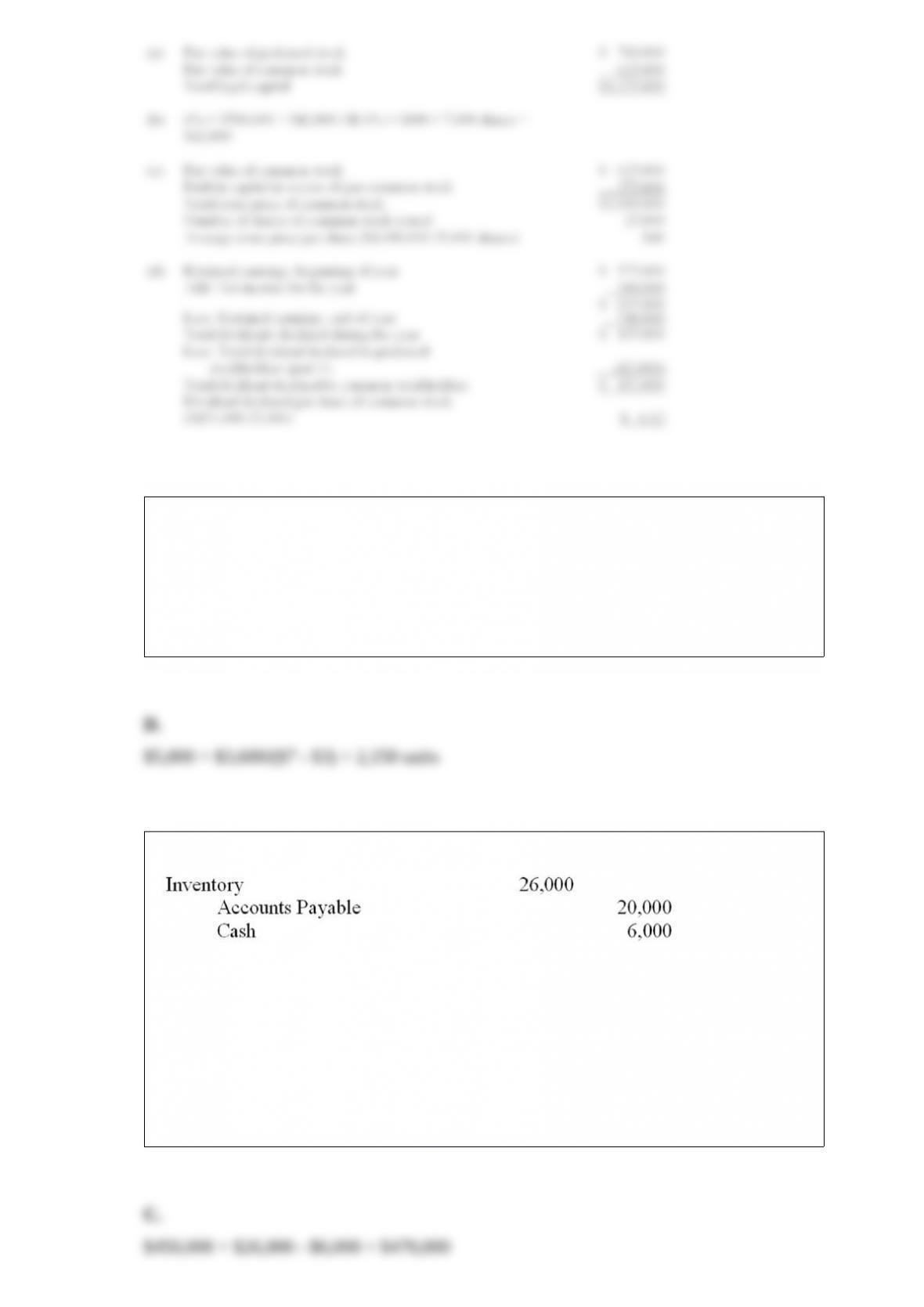

Job order cost system-journal entries

Paxton Products, which uses a job order cost system, completed the following

transactions during the current month:

(A) Materials costing $75,000 were used on various jobs.

(B) Time cards of direct workers indicate direct labor costs of $125,000 for the month.

(C) Overhead is applied to jobs at a rate of 75% of direct labor cost.

(D) Jobs with total accumulated costs of $165,000 were finished during the month.

(E) Units costing $210,000 were sold during the month at sales prices totaling

$390,000. All sales were on account.

In the space provided, prepare a general journal entry for the month summarizing each

of the above categories of transactions. Explanations may be omitted.

Bank reconciliation–computation and journal entry

The Cash account in the ledger of Arnaz Company showed a balance of $13,307 at

March 31. The bank statement, however, showed a balance of $9,936 at the same date.

The only reconciling items consisted of a $4,902 deposit in transit, a bank service

charge of $36, outstanding checks totaling $2,600, and an NSF check from L. Ball, one

of Arnaz’ customers.

(a) What is the amount of the adjusted cash balance on March 31?

(b) What is the amount of the NSF check?

(c) Record the journal entry necessary, if any, to adjust Arnaz Company’s accounting

records at March 31: (An explanation is not required; a single compound journal entry

is acceptable.)

Value-added activities include:

A. Setting up machinery.

B. Storing direct materials.

C. Employee idle time.

D. Product design.

When equipment is sold at a loss:

A. The net proceeds are shown in the investing section.

B. The book value of the asset is shown in the investing section.

C. The book value of the asset is shown in the investing section, and the loss is shown

in the operating section.

D. The net proceeds are shown in the financing section.

The basic purpose of the matching principle is to allocate the cost of an asset to expense

over the years in which the asset contributes to revenue. Current accounting practice

does not strictly apply this principle to expenditures for:

A. Natural resources.

B. Research and development.

C. Trademarks.

D. Equipment.

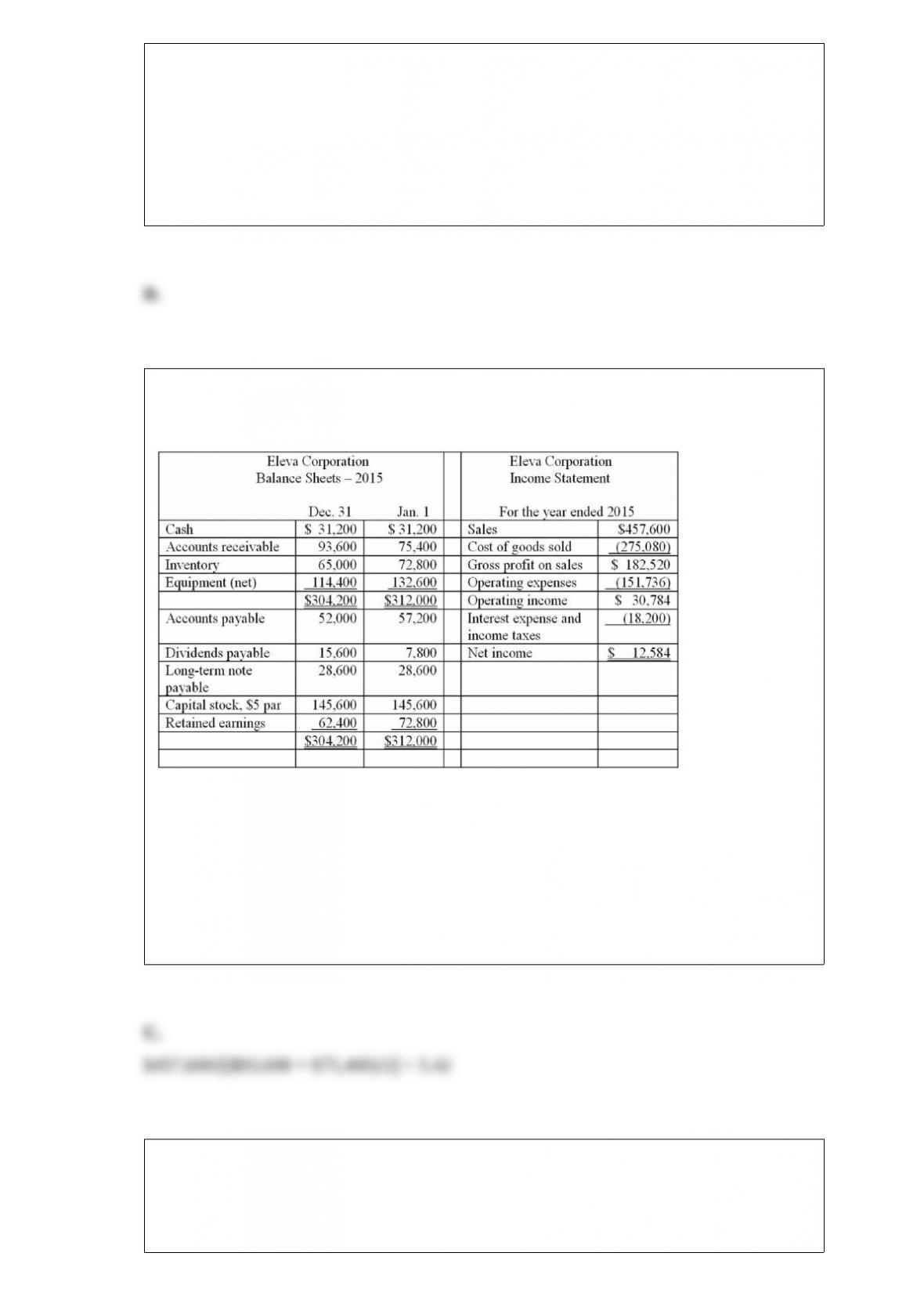

Given below are comparative balance sheets and an income statement for Eleva

Corporation.

All sales were made on account. Cash dividends declared during the year totaled

$22,984.

Refer to the information above. Eleva Corporation’s accounts receivable turnover for

2015 is closest to:

A. 4.63 times.

B. 2.91 times.

C. 5.42 times.

D. 68 days.

The legal life of most patents is:

A. 5 years.

B. 20 years.

C. 40 years.

D. 50 years.

In which of the following situations would an adjusting entry be made at the end of

January to record an accrued expense?

A. Ramona’s Nursery purchased playground equipment on January 1 with an estimated

useful life of six years.

B. On January 25, Ramona’s Nursery hired a college student to drive the minibus; the

new employee is to begin work in February.

C. January 31 falls on a Tuesday; salaries are paid on Friday of each week.

D. On January 31, Ramona’s Nursery paid the interest owed on a note payable for

January.

Which of the following is considered a financial budget?

A. The marketing budget.

B. The cost of goods sold budget.

C. The overhead budget.

D. The capital expenditures budget.

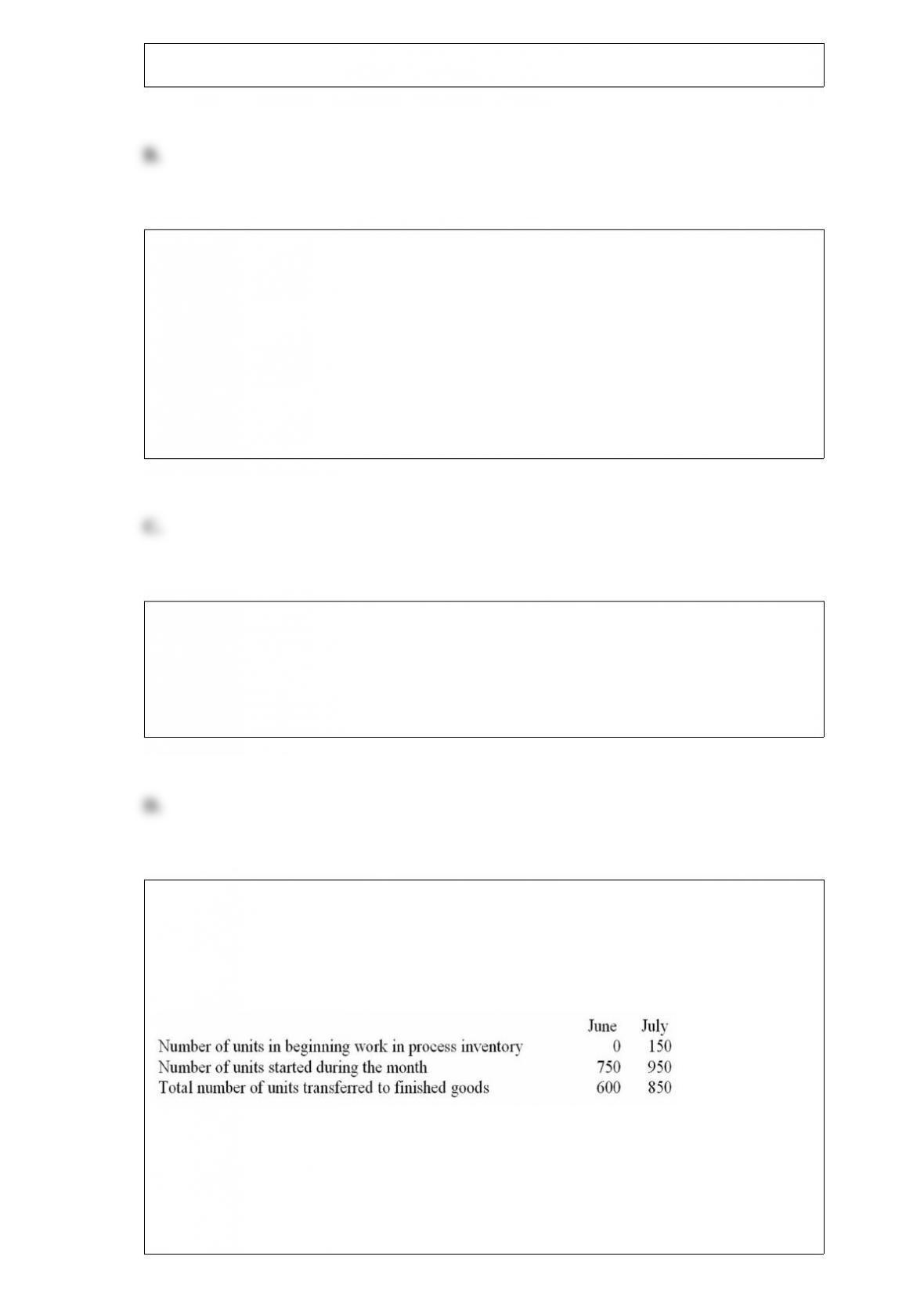

Aves Treats, Inc. produces bird seeds. All direct materials used in the production

process are added at the beginning of the manufacturing process. Labor and overhead

are added evenly thereafter, as each unit is mixed and packaged. Aves Treats uses

process costing and had the following unit production information available for the

months of June and July:

The units remaining in work in process at the end of June were 30% complete. During

the month of July, all of the beginning work in process units was completed and the

units remaining in work in process at the end of the month were 60% complete.

Refer to the information above. For the month of July, the number of equivalent units of

labor and overhead produced was:

A. 830.

B. 320.

C. 955.

D. Some other amount.

Omega Company adjusts its accounts at the end of each month. The following

information has been assembled in order to prepare the required adjusting entries at

December 31:

(1) A one-year bank loan of $720,000 at an annual interest rate of 12% had been

obtained on December 1.

(2) The company pays all employees up-to-date each Friday. Since December 31 fell on

Tuesday, there was a liability to employees at December 31 for two day’s pay

amounting to $6,800.

(3) On December 1, rent on the office building had been paid for four months. The

monthly rent is $6,000.

(4) Depreciation of office equipment is based on an estimated useful life of six years.

The balance in the Office Equipment account is $9,360; no change has occurred in the

account during the year.

(5) Fees of $9,800 were earned during the month for clients who had paid in advance.

Refer to the information above. The accrued interest should be:

A. Debited to Notes Payable.

B. Credited to Interest Payable.

C. Credited to Cash.

D. Credited to Interest Expense.