1) LIFO liquidations can occur frequently when using a specific-goods LIFO approach.

2) Under IFRS, there is no specific standard related to pledging receivables.

3) In all cases when FIFO is used, the cost of goods sold would be the same whether a

perpetual or periodic system is used.

4) The IASB is considering a proposal to provide expanded guidance on estimating fair

values.

5) An accelerated depreciation method is appropriate when the assets economic

usefulness is the same each year.

6) If a long-term note payable has a stated interest rate, that rate should be considered to

be the effective rate.

7) Benefits under a pension plan can include the retiree, the retiree’s spouse, and other

dependents.

8) Taxable income is a tax accounting term and is also referred to as income before

taxes.

9) Impaired assets held for disposal should be reported at the lower of cost or net

realizable value.

10) Neither U.S. GAAP nor IFRS requires interim reports.

11) Cash payments for operating expenses are computed by subtracting an increase in

prepaid expenses and a decrease in accrued expenses payable from operating expenses.

12) Hogan Farms produced 1,600,000 pounds of cotton during the 2015 season. Hogan

sells all of its cotton to Ott Co., which has agreed to purchase Hogan’s entire production

at the prevailing market price. Recent legislation assures that the market price will not

fall below $.70 per pound during the next two years. Hogan’s costs of selling and

distributing the cotton are immaterial and can be reasonably estimated. Hogan reports

its inventory at expected exit value. During 2015, Hogan sold and delivered to Ott

1,200,000 pounds at the market price of $.70. Hogan sold the remaining 400,000

pounds during 2016 at the market price of $.72. What amount of revenue should Hogan

recognize in 2015?

a.$840,000

b.$864,000

c.$1,120,000

d.$1,152,000

13) The information provided by financial reporting pertains to

a.individual business enterprises, rather than to industries or an economy as a whole or

to members of society as consumers

b.business industries, rather than to individual enterprises or an economy as a whole or

to members of society as consumers

c.individual business enterprises, industries, and an economy as a whole, rather than to

members of society as consumers

d.an economy as a whole and to members of society as consumers, rather than to

individual enterprises or industries

14) If the LIFO inventory method was used last period, it should be used for the current

and following periods because of

a.comparability

b.materiality

c.timeliness

d.verifiability

15) Which of the following statements about the recognition of a prior service cost

related to a postretirement obligation is correct?

a.The prior service amount is recognized in the income statement in the current period

b.The prior service cost is recognized in the income statement net of tax

c.Restatement of previously issued annual financial statements is required

d.The prior service cost amount affects comprehensive income in the current period

16) Miles Company, a wholesaler, budgeted the following sales for the indicated

months:

June July August

Sales on account$2,700,000$2,760,000$2,850,000

Cash sales 270,000 300,000 390,000

Total sales$2,970,000$3,060,000$3,240,000

All merchandise is marked up to sell at its invoice cost plus 25%. Merchandise

inventories at the beginning of each month are at 30% of that month’s projected cost of

goods sold.

The cost of goods sold for the month of June is anticipated to be

a.$2,025,000

b.$2,227,500

c.$2,079,000

d.$2,376,000

17) Which of the following intangible assets should be shown as a separate item on the

balance sheet?

a.Goodwill

b.Franchise

c.Patent

d.Trademark

18) Which of the following accounts is credited in the loss method of writing-down of

inventory to its market value?

a.Inventory

b.Loss Due to Decline of Inventory to market

c.Cost of Goods Sold

d.Allowance to Reduce Inventory to Market

19) Garwood Company has the following items: write-down of inventories, $360,000;

loss on disposal of Sports Division, $555,000; and loss due to an expropriation,

$359,000. Ignoring income taxes, what amount should Garwood Company report as

extraordinary losses?

a.$359,000

b.$555,000

c.$719,000

d.$914,000

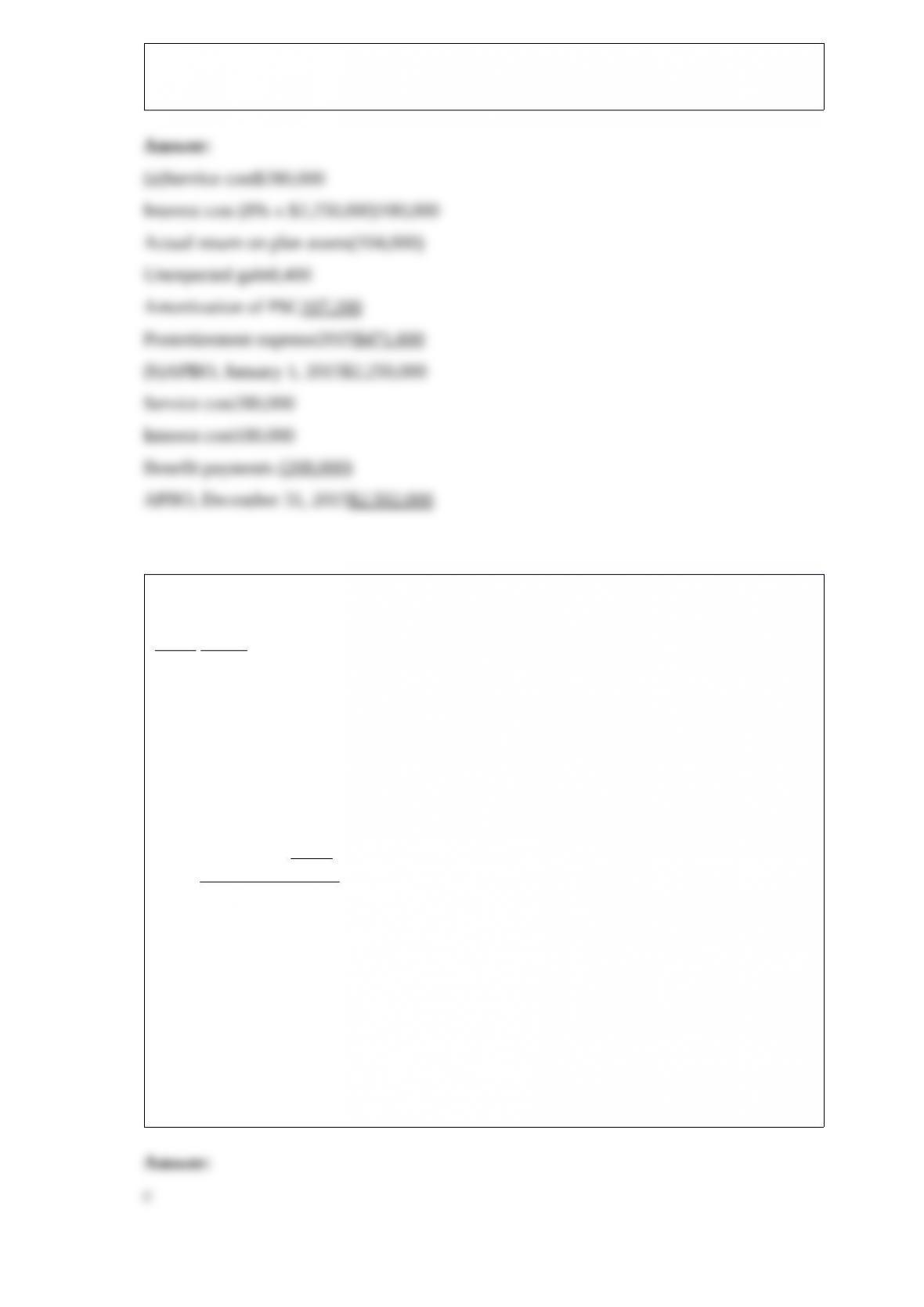

20) The following information is related to the postretirement benefits plan of Heerey,

Inc. for 2015:

Service cost$ 280,000

Discount rate8%

APBO, January 1, 20152,250,000

EPBO, January 1, 20152,400,000

Actual return on plan assets in 2015104,000

Expected return on plan assets in 201595,600

Amortization of PSC, due to benefit increase107,200

Contributions (funding)400,000

Benefit payments208,000

Instructions

(a)Compute the amount of postretirement expense for 2015 . (Show computations.)

(b)Compute the amount of the APBO at December 31, 2015 .

21) Logan Corp.’s trial balance of income statement accounts for the year ended

December 31, 2014 included the following:

Debit Credit

Sales revenue$280,000

Cost of goods sold$150,000

Administrative expenses40,000

Loss on disposal of equipment18,000

Sales commission expense16,000

Interest revenue10,000

Freight-out6,000

Loss due to earthquake damage24,000

Bad debt expense 6,000

Totals$260,000$290,000

Other information:

Logan’s income tax rate is 30%. Finished goods inventory:

January 1, 2014$160,000

December 31, 2014140,000

On Logan’s multiple-step income statement for 2014,

Income before extraordinary item is

a.$88,000

b.$54,000

c.$37,800

d.$21,000

22) During 2014, a textbook written by Mercer Co. personnel was sold to Roark

Publishing, Inc., for royalties of 10% on sales. Royalties are receivable semiannually on

March 31, for sales in July through December of the prior year, and on September 30,

for sales in January through June of the same year.

Royalty income of $162,000 was accrued at 12/31/14 for the period July-December

2014 .

Royalty income of $180,000 was received on 3/31/15, and $234,000 on 9/30/15.

Mercer learned from Roark that sales subject to royalty were estimated at $3,240,000

for the last half of 2015 .

In its income statement for 2015, Mercer should report royalty income at

a.$414,000

b.$432,000

c.$558,000

d.$576,000

23) Hopkins Co. at the end of 2014, its first year of operations, prepared a

reconciliation between pretax financial income and taxable income as follows:

Pretax financial income$1,500,000

Estimated litigation expense2,000,000

Extra depreciation for taxes (3,000,000)

Taxable income$ 500,000

The estimated litigation expense of $2,000,000 will be deductible in 2015 when it is

expected to be paid. Use of the depreciable assets will result in taxable amounts of

$1,000,000 in each of the next three years. The income tax rate is 30% for all years.

The deferred tax asset to be recognized is

a.$150,000 current

b.$300,000 current

c.$450,000 current

d.$600,000 current

24) Each of the following are included in both the current ratio and the acid-test ratio

except

a.cash

b.short-term investments

c.net receivables

d.inventory

25) At the beginning of 2015, Hamilton Company had retained earnings of $250,000.

During the year Hamilton reported net income of $75,000, sold treasury stock at a gain

of $27,000, declared a cash dividend of $45,000, and declared and issued a small stock

dividend of 1,500 shares ($10 par value) when the fair value of the stock was $30 per

share. The amount of retained earnings available for dividends at the end of 2015 was:

a.$284,500

b.$262,000

c.$257,500

d.$235,000

26) On January 1, 2012, Knapp Corporation acquired machinery at a cost of $750,000.

Knapp adopted the double-declining balance method of depreciation for this machinery

and had been recording depreciation over an estimated useful life of ten years, with no

residual value. At the beginning of 2015, a decision was made to change to the

straight-line method of depreciation for the machinery. The depreciation expense for

2015 would be

a.$38,400

b.$54,858

c.$75,000

d.$107,142

27) Operating losses incurred during the start-up years of a new business should be

a.accounted for and reported like the operating losses of any other business

b.written off directly against retained earnings

c.capitalized as a deferred charge and amortized over five years

d.capitalized as an intangible asset and amortized over a period not to exceed 20 years

28) One of the benefits of the statement of cash flows is that it helps users evaluate

financial flexibility. Which of the following explanations is a description of financial

flexibility?

a.The nearness to cash of assets and liabilities

b.The firm’s ability to respond and adapt to financial adversity and unexpected needs

and opportunities

c.The firm’s ability to pay its debts as they mature

d.The firm’s ability to invest in a number of projects with different objectives and costs