The asset/liability approach emphasizes:

a. Whether amounts on the balance sheet meet the definitions of assets and liabilities.

b. A close relation between the balance sheet and the statement of cash flows.

c. The distinction between net assets and gross assets.

d. All of the above are correct.

Bonds payable should be reported as a long-term liability in the balance sheet of the

issuing corporation at the:

a. Face amount price less any unamortized discount or plus any unamortized premium.

b. Current bond market price.

c. Face amount less any unamortized premium or plus any unamortized discount.

d. Face amount less accrued interest since the last interest payment date.

On January 1, 2016, Elite Advertising was contracted to run a marketing campaign for

Pharm King’s new dieting pills. In addition to getting a base fee of $150,000 for the

3-year campaign, Elite also may get an additional 5% of the base fee as a bonus if a

targeted sales level is reached at the end of three years. Elite currently lacks sufficient

information to make an estimate of the likelihood of the expected bonus, with the

marketing director indicating that “If you forced me to make an estimate, I’d say we

have a 50/50 chance. But don’t quote me on that – it’s really too early to tell.” Elite

concludes this contract qualifies for revenue recognition over time, and estimates

variable consideration using the most likely amount. How much revenue should Elite

recognize as of December 31, 2016?

a. $50,000

b. $51,250

c. $52,500

d. $57,500

Gains on the cash sales of fixed assets:

a. Are the excess of the book value over the cash proceeds.

b. Are part of cash flows from operations.

c. Are reported on a net-of-tax basis if material.

d. Are the excess of the cash proceeds over the book value of the assets sold.

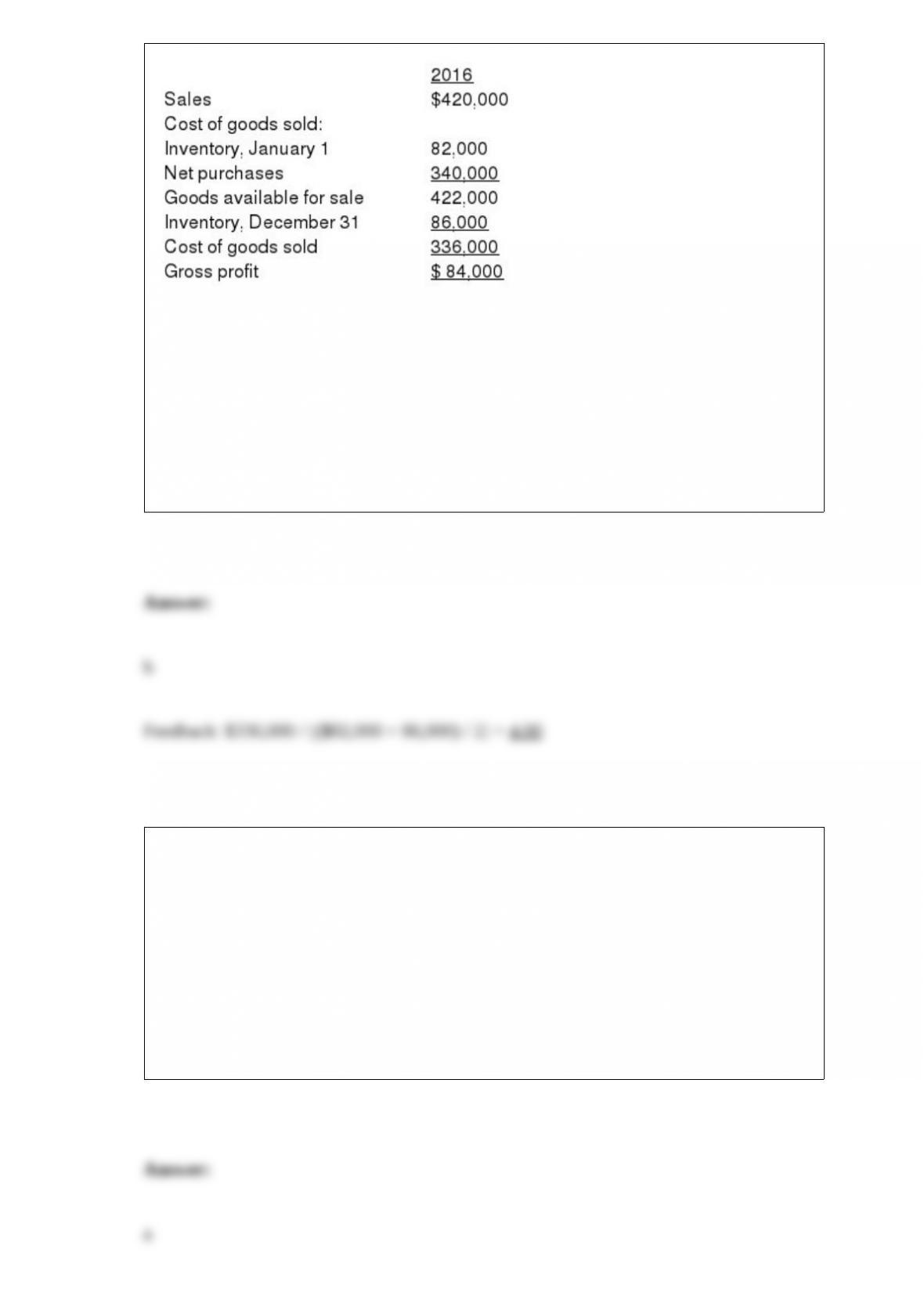

Thompson TV and Appliance reported the following in its 2016 financial statements:

Thompson’s 2016 inventory turnover ratio is:

a. 3.91.

b. 4.00.

c. 4.88.

d. 5.00.

Eligibility requirements and the nature of benefits for postretirement health care plans

usually are specified in the:

a. Written plan.

b. Informal plan.

c. Substantive plan.

d. Severance plan.

In a statement of cash flows using the indirect method, an increase in available-for-sale

securities due to an increase in their fair value should be reported as:

a. A deduction from net income in determining cash flows from operating activities.

b. An addition to net income in determining cash flows from operating activities.

c. An investing activity.

d. Not reported.

On May 1, Foxtrot Co. agreed to sell the assets of its Footwear Division to Albanese

Inc. for $80 million. The sale was completed on December 31, 2016. The following

additional facts pertain to the transaction:

– The Footwear Division qualifies as a component of the entity according to GAAP

regarding discontinued operations.

– The book value of Footwear’s assets totaled $48 million on the date of the sale.

– Footwear’s operating income was a pre-tax loss of $10 million in 2016.

– Foxtrot’s income tax rate is 40%.

In the 2016 income statement for FoxtrotCo., it would report:

a. All income taxes combined into one line item.

b. Income taxes separated for continuing and discontinued operations.

c. Income taxes reported for income and gains only.

d. None of the other answers is correct.

Loan C has the same principal amount, payment amount, and maturity date as Loan D.

However, Loan C is structured as an annuity due, while Loan D is structured as an

ordinary annuity. Loan C’s interest rate is:

a. Higher than Loan D.

b. Less than Loan D.

c. The same as Loan D.

d. Indeterminate compared to Loan D.

Under IAS No. 39, which is not a category for accounting for investments?

a. Fair value through profit and loss.

b. Fair value through other comprehensive income.

c. Held-to-maturity.

d. Available-for-sale.

A small stock dividend is defined as one that is:

a. Less than or equal to 40%.

b. Less than 40%.

c. Less than or equal to 10%.

d. Less than 25%.

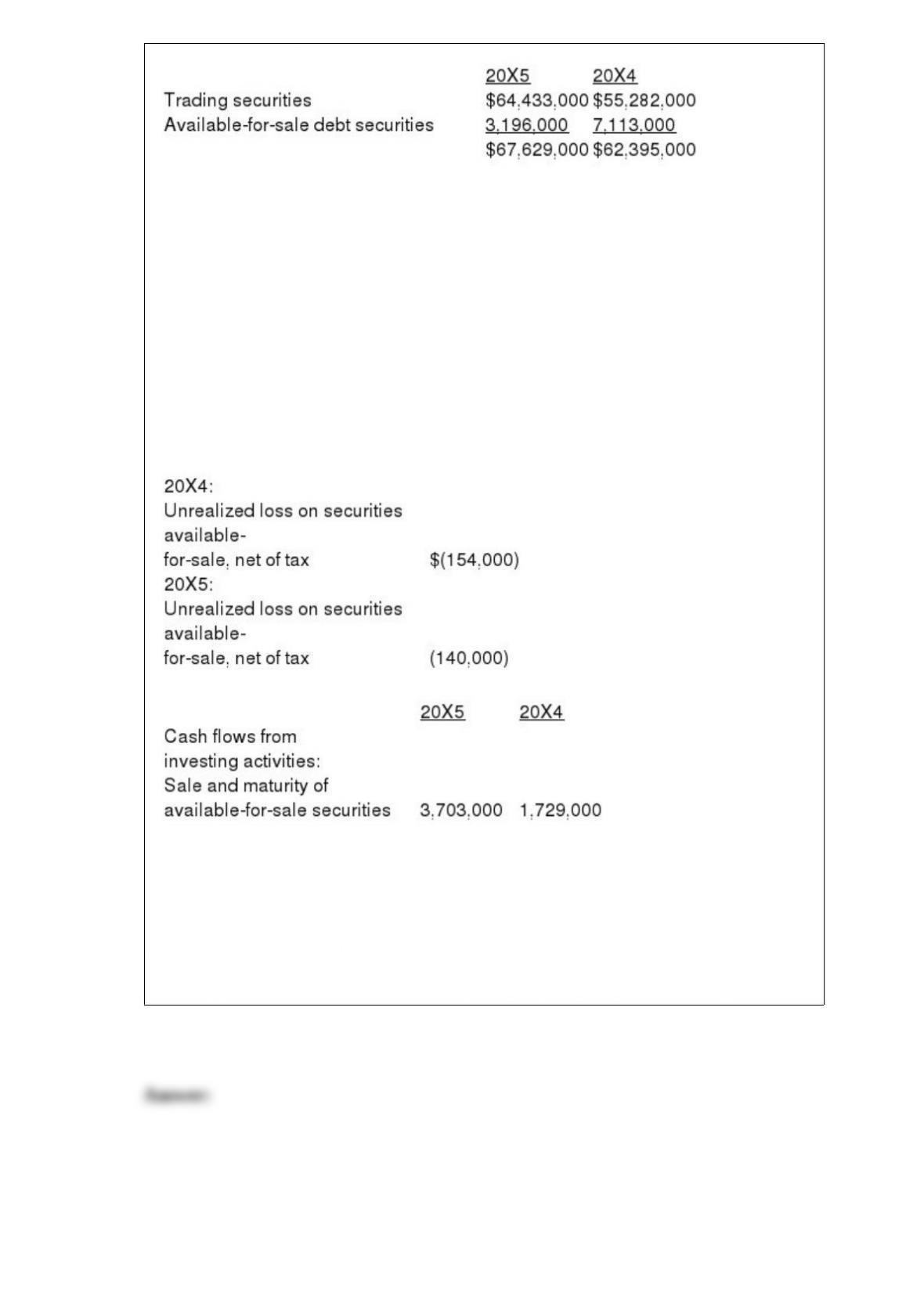

Arctic Cat Inc., the snowmobile manufacturer, reported the following in its 20X5

annual report to shareholders: NOTE B – SHORT-TERM INVESTMENTS

Short-term investments consist primarily of a diversified portfolio of municipal bonds

and money market funds and are classified as follows at March 31:

Trading securities consist of $54,608,000 and $41,707,000 invested in various money

market funds at March 31, 20X5 and 20X4, respectively, while the remainder of trading

securities and available-for-sale securities consist primarily of A-rated or higher

municipal bond investments. The amortized cost and fair value of debt securities

classified as available-for-sale was $3,105,000 and $3,196,000, at March 31, 20X5. The

unrealized gain on available-for-sale debt securities is reported, net of tax, as a separate

component of shareholders’ equity. Arctic Cat Inc.

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

Years Ended March 31, Accumulated Other Comprehensive Income changed by the

following amounts:

In its 20X4 annual report, Arctic Cat disclosed, “The contractual maturities of

available-for-sale debt securities at March 31, 20X4, are $3,573,000 within one year

and $3,340,000 from one year through five years.”

Assume Arctic Cat did not purchase any trading securities during 20X5. Write a journal

entry to record any unrealized holding gains or losses on trading securities during

20X5.

Briefly explain the purpose of the disclosure note on significant accounting policies.

Provide two examples of what might be found in this note.

Hart Corporation has an unfunded postretirement health care benefit plan. Life

insurance and medical care benefits are provided to employees who render 12 years of

service and attain age 55 while in service to the company. At the end of 2016, John

Sousa is 35. He was hired by Hart five years ago at age 30 and is expected to retire at

the age of 62. The expected postretirement benefit obligation for John is $50,000 at the

end of 2016.

Required:

Calculate the accumulated postretirement benefit obligation at the end of 2016 and the

service cost for 2016 pertaining to John.

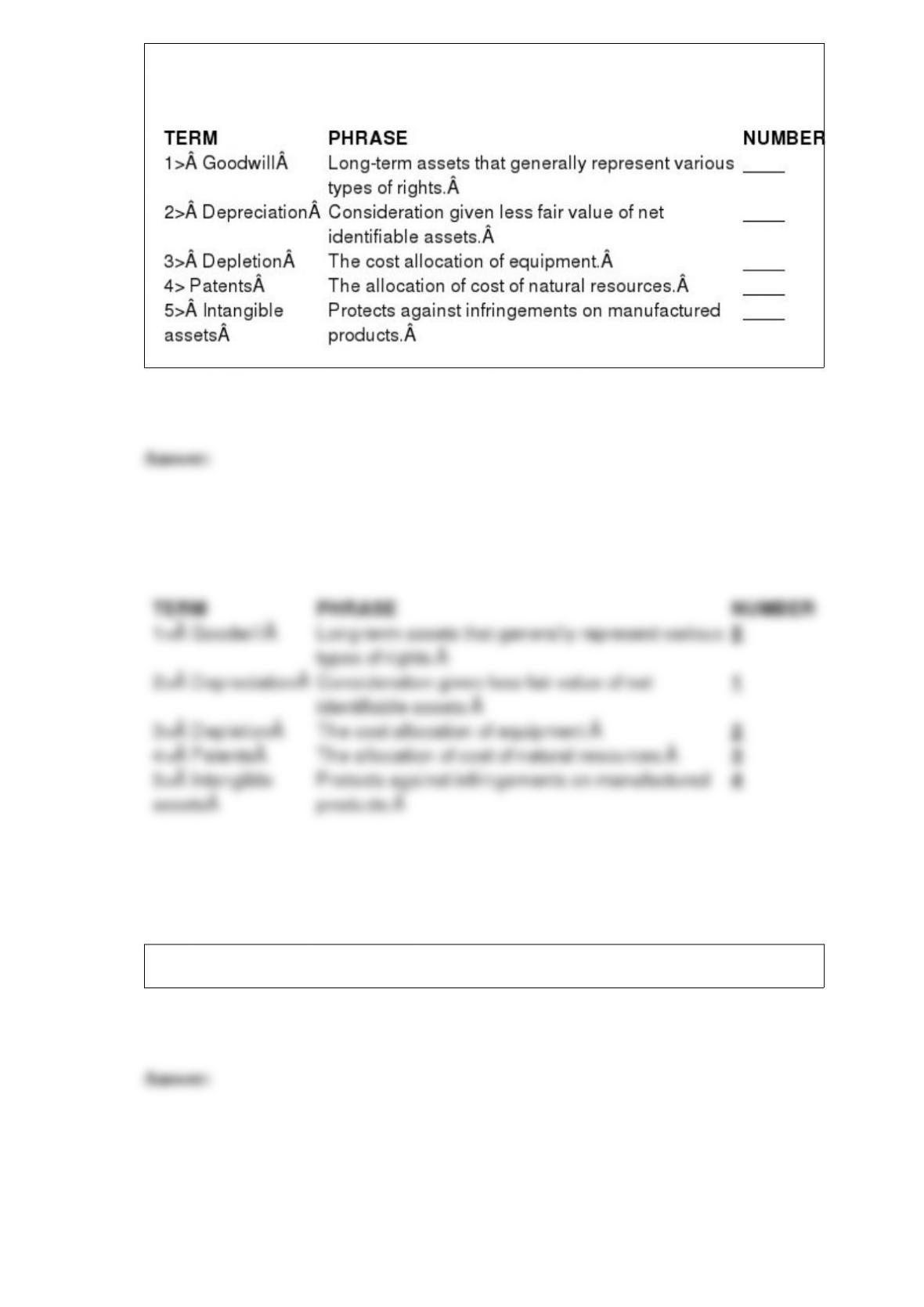

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

On January 1, 2016, Happy Tubs sold a hot tub to Monica, receiving a two-month,

noninterest-bearing note in exchange for a hot tub that normally sells for $8,000. The

note is for an amount that achieves an effective interest rate of 10% per year.

Required:

1> Prepare the journal entry to record the sale.

2> Prepare any adjusting entry necessary on December 31, 2016.

3> Prepare any adjusting entry necessary on December 31, 2017.

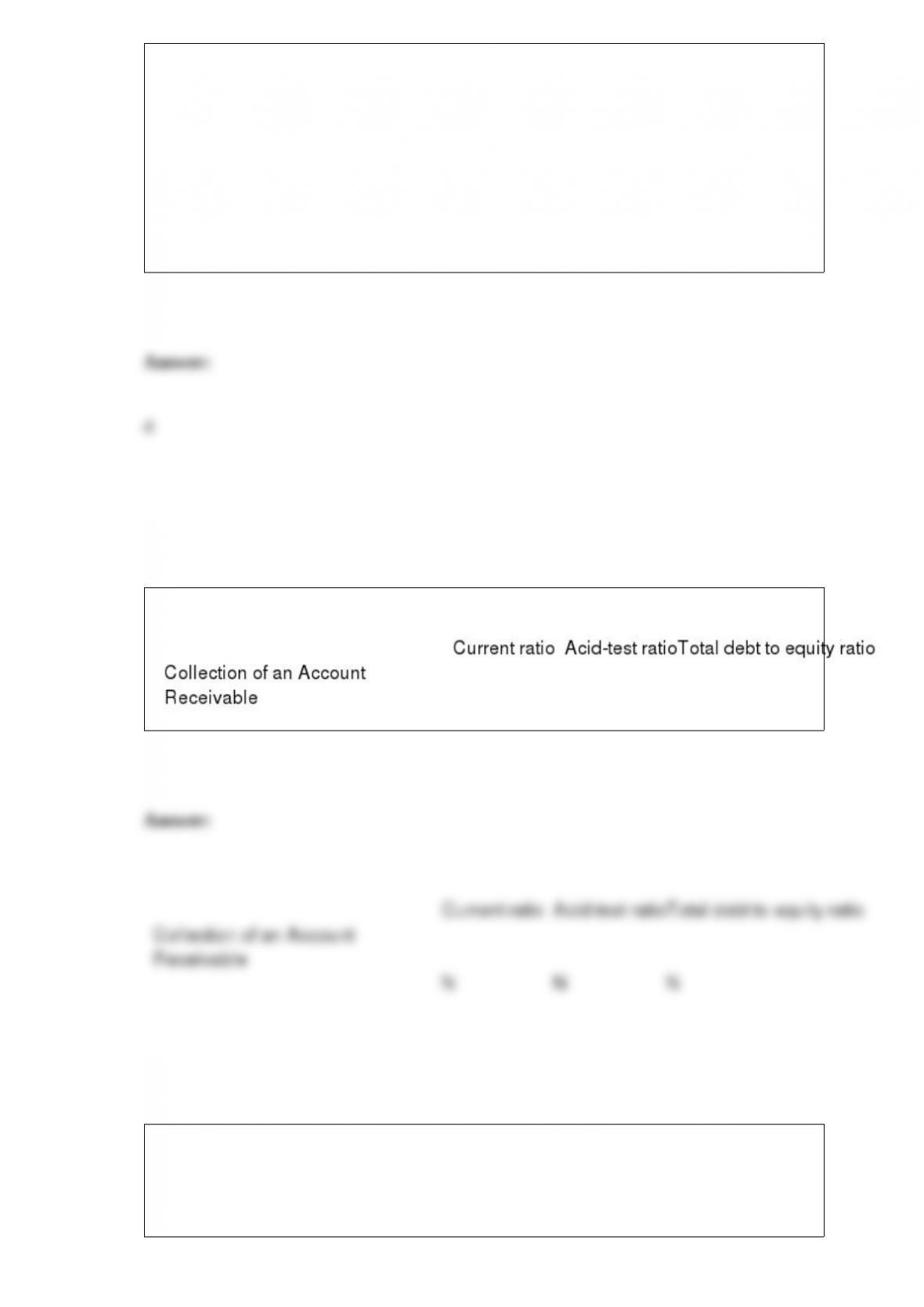

Below is a list of accounts in no particular order. Assume that all accounts have normal

balances. Required: In column A, indicate whether a debit will:

1> Increase the account balance, or

2> Decrease the account balance. In column B, classify each account according to the

following scheme. For contra accounts, indicate the classification of the account to

which it relates.

1>A current asset in the balance sheet.

2>A noncurrent asset in the balance sheet.

3>A current liability in the balance sheet.

4>A long-term liability in the balance sheet.

5>A permanent equity account in the balance sheet.

6>A revenue account in the income statement.

7>An expense account shown in the income statement.

8> Account does not appear in either the balance sheet or the income statement.

Retained earnings