Coastal Shores Inc. (CSI) was destroyed by Hurricane Fred on August 5, 2016. At

January 1, CSI reported an inventory of $170,000. Sales from January 1, 2016, to

August 5, 2016, totaled $480,000 and purchases totaled $195,000 during that time. CSI

consistently marks up its products 60% over cost to arrive at a selling price. The

estimated inventory loss due to Hurricane Fred would be:

a. $131,175.

b. $ 65,000.

c. $ 69,000.

d. None of these answer choices are correct.

Oregon Co.’s employees are eligible for retirement with benefits at the end of the year

in which both age 60 is attained and they have completed 35 years of service. The

benefits provide 15 years reimbursement for health care services of $20,000 annually,

beginning one year from the date of retirement.

Ralph Young was hired at the beginning of 1977 by Oregon after turning age 22 and is

expected to retire at the end of 2018 (age 60). The discount rate is 4%. The plan is

unfunded.

The PV of an ordinary annuity of $1 where n = 15 and i = 4% is 11.11839.

The PV of $1 where n = 2 and i = 4% is 0.92456

With respect to Ralph, what is Oregon’s expected postretirement benefit obligation

(EPBO) at the end of 2016, rounded to the nearest dollar?

a. $137,045.

b. $205,593.

c. $246,810.

d. $768,000.

The Mateo Corporation’s inventory at December 31, 2016, was $325,000 based on a

physical count priced at cost, and before any necessary adjustment for the following:

– Merchandise costing $30,000, shipped f.o.b. shipping point from a vendor on

December 30, 2016, was received on January 5, 2017.

– Merchandise costing $22,000, shipped f.o.b. destination from a vendor on December

28, 2016, was received on January 3, 2017.

– Merchandise costing $38,000 was shipped to a customer f.o.b. destination on

December 28, arrived at the customer’s location on January 6, 2017.

– Merchandise costing $12,000 was being held on consignment by Traynor Company.

What amount should Mateo Corporation report as inventory in its December 31, 2016,

balance sheet?

a. $367,000.

b. $427,000.

c. $405,000.

d. $325,000.

Basic earnings per share ignores:

a. All potential common shares.

b. Some potential common shares, but not others.

c. Dividends declared on noncumulative preferred stock.

d. Stock splits.

On December 31, 2015, Beta Company had 300,000 shares of common stock issued

and outstanding. Beta issued a 5% stock dividend on June 30, 2016. On September 30,

2016, 40,000 shares of common stock were reacquired as treasury stock. What is the

appropriate number of shares to be used in the basic earnings per share computation for

2016?

a. 315,000.

b. 307,500.

c. 305,000.

d. 267,500.

Assume the actuary estimates the net cost of providing health care benefits to a

particular employee during his retirement years to have a present value of $60,000. If

the benefits relate to an estimated 25 years of service and five of those years have been

completed:

a. The EPBO would be $12,000.

b. The EPBO would be $8,400.

c. The APBO would be $8,400.

d. The APBO would be $12,000.

The most recent example of the political process at work in standard-setting is the

heated debate that occurred on the issue of:

a. Pension plan accounting.

b. Accounting for postretirement benefits other than pensions.

c. Accounting for business combinations.

d. Accounting for stock-based compensation.

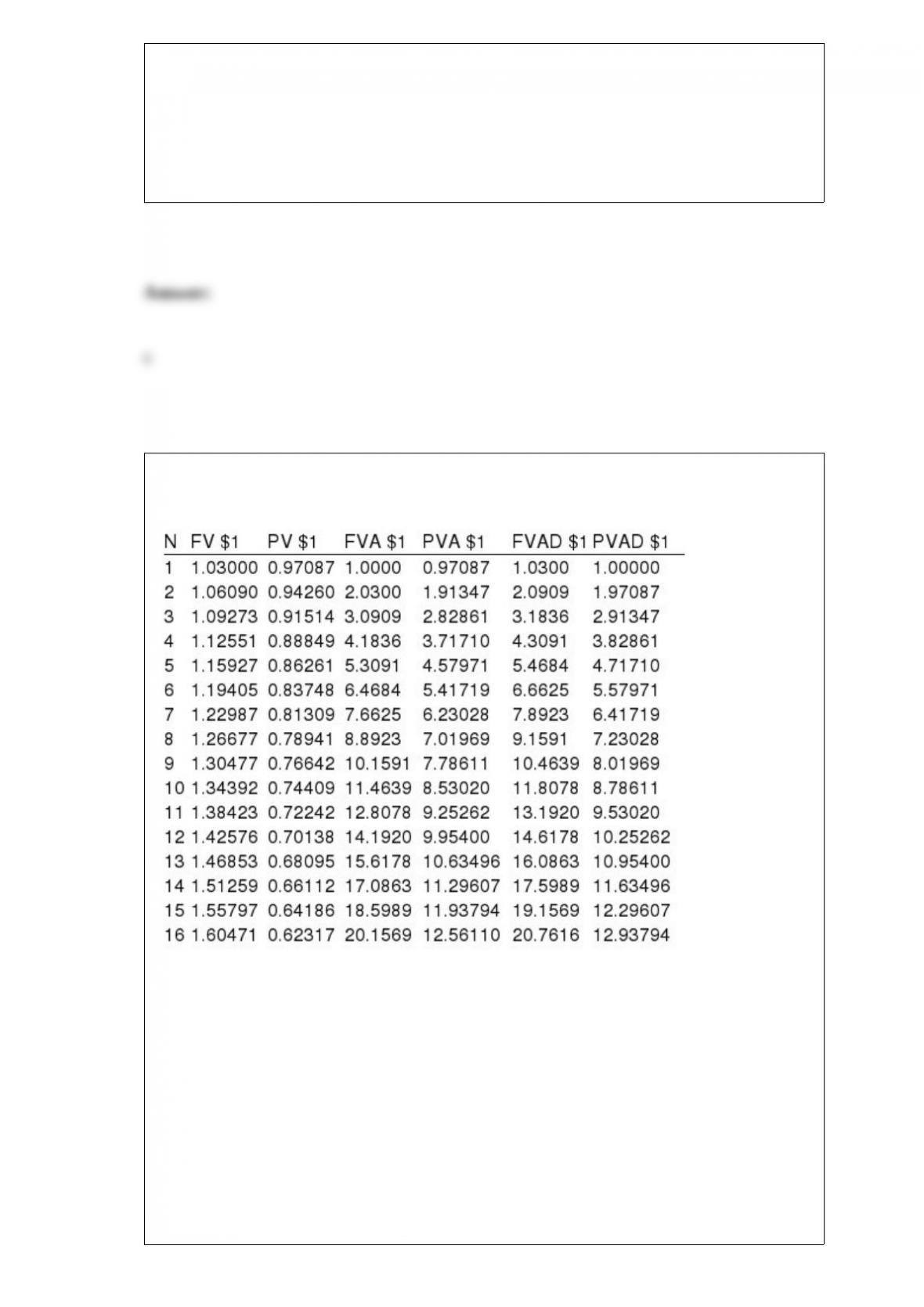

Present and future value tables of $1 at 3% are presented below:

On January 1, 2016, you are considering making an investment that will pay three

annual payments of $10,000. The first payment is not expected until December 31,

2019. You are eager to earn 3%. What is the present value of the investment on January

1, 2016?

a. $28,286.

b. $25,886.

c. $26,662.

d. $27,300.

Inventory is valued at:

a. Net realizable value.

b. Cost.

c. Replacement cost.

d. Lower of cost and net realizable value.

Rebound Inc. reports under IFRS. In 2016 Rebound recognized an impairment of

$200,000 due to a troubled debt restructuring. In 2017 Rebound was pleased to

determine that more cash flows would be received from the receivable than was

previously thought, such that, if the total impairment were to be calculated in 2017, it

would be estimated as $150,000 rather than $200,000. How should Rebound treat this

in its 2017 income statement?

a. Rebound should ignore the change, given that recovery of its previous impairments is

not allowed under IFRS.

b. Rebound should make a prior period adjustment of 2016 income, given that the

impairment charge was in error.

c. Rebound should recognize an increase in 2017 net income of $50,000.

d. None of these answer choices are correct.

CPAs are licensed by:

a. The AICPA.

b. The SEC.

c. The federal government.

d. State governments.

Which of the following differences between financial accounting and tax accounting

ordinarily creates a deferred tax asset?

a. Depreciation early in the life of an asset.

b. Unrealized gain from recording investments at fair value.

c. Subscriptions collected in advance.

d. None of these answer choices are correct.

Companies may report interest received and dividends received as investing activities

using:

a. U.S. GAAP.

b. IFRS.

c. Both U.S. GAAP and IFRS.

d. Neither U.S. GAAP nor IFRS.

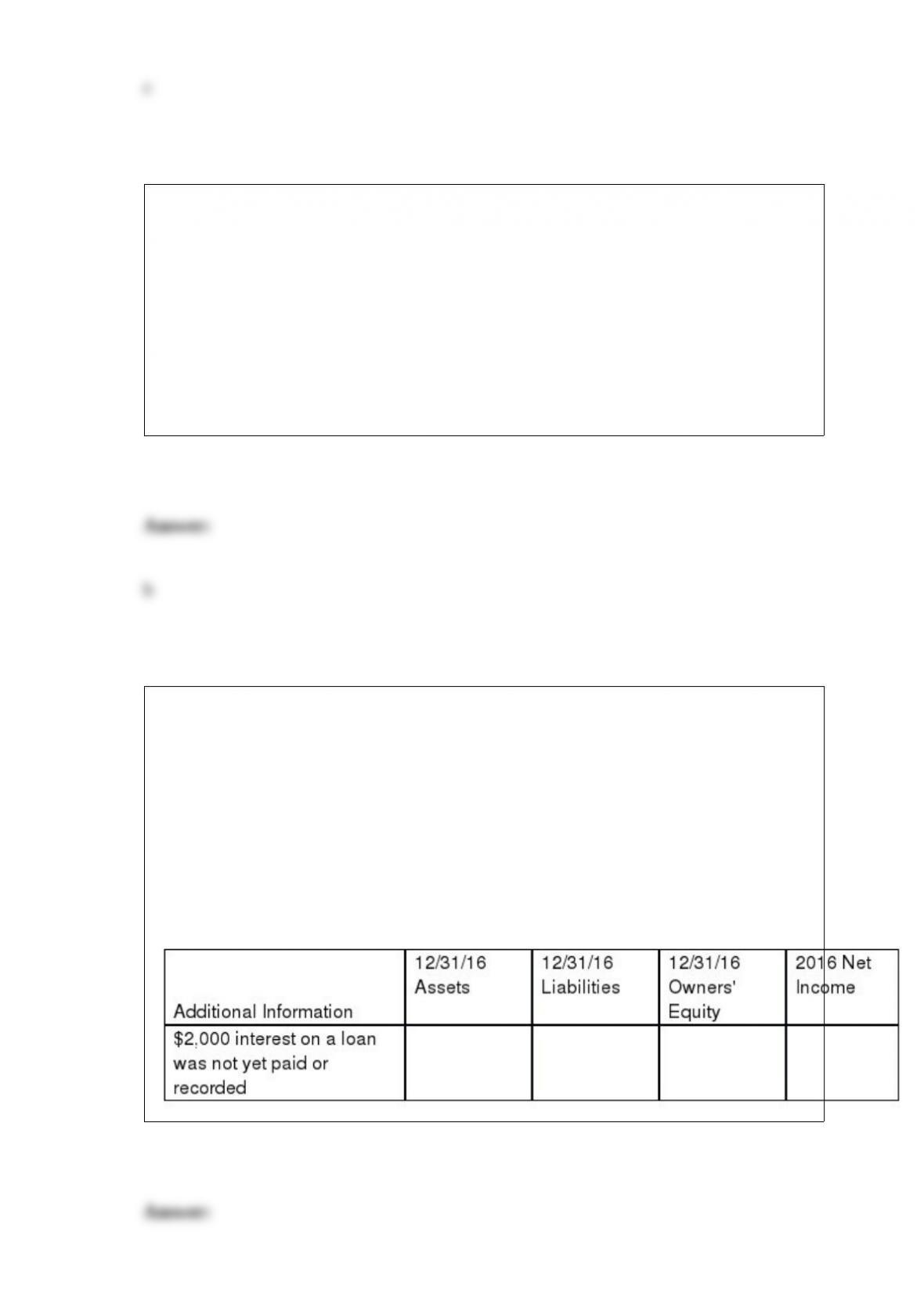

Suppose that Laramie Company’s adjusted trial balance ignored the following

information. For each item of information, indicate what effects, if any, these omissions

would have on the stated components of Laramie Company’s 2016 Income Statement

and 12/31/16 Balance Sheet. Assume no income taxes. Use the following code for your

answers and be sure to include the dollar amounts of the effects next to the letter O or

U: N = No Effect

O = Overstated

U = Understated

The tax code differentiates between qualified and nonqualified incentive plans. What

are the major differences in tax treatment between the two?

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

The shareholders’ equity of Nick Co. includes the items shown below. The board of

directors of Nick declared cash dividends of $4 million, $8 million, and $50 million in

each of its first 3 years of operation: 2014, 2015, and 2016, respectively.

Common stock, $1 par, 50,000,000 shares outstanding

Preferred stock, 6%, $100 par, 1,000,000 shares outstanding

Required:

Determine the amount of dividends per share on preferred and common stock for each

of the three years. The preferred stock is noncumulative and nonparticipating.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

Some preferred stock is cumulative while other preferred stock is noncumulative. What

does this mean?

Which of the following is a characteristic of a contract for purposes of revenue

recognition?

e. Commercial substance.

f. Nonverbal.

g. Reasonable profit margin.

h. Notarized within the company’s state of incorporation.

On November 10 of the current year, Cherokee Industries sold materials to a customer

for $8,000 with credit terms 2/10, n/30. Cherokee uses the net method of accounting for

cash discounts. What entry would Cherokee make on November 17, assuming the

correct payment was received on that date?

On February 1, 2016, Lynda Brown, proud mother of newborn daughter Goldie,

purchased $600,000 in zero-coupon bonds that mature on February 1, 2036. The bonds

pay no interest during the period of time they are outstanding. The interest rate for such

borrowings is at 12%.

Required: Calculate the price Lynda paid for the bonds.