If the direct method is used to report cash flows from operating activities in the body of

the statement of cash flows, a reconciliation of net income to net cash flows from

operating activities also is required.

The primary function of financial accounting is to provide relevant financial

information to parties external to business enterprises.

At the inception of a lease agreement, the company’s debt to equity ratio and rate of

return on assets are both affected whether the lease is classified as a capital lease or as

an operating lease.

The decomposition of return on assets illustrates why some companies with low profit

margins can be very profitable if their asset turnover is high.

A deferred tax asset represents the tax effect of the temporary difference between the

financial carrying value of an asset or liability and its tax basis.

The specific provisions of a bond issue are described in a document called a bond

indenture.

When the lessee guarantees an estimated residual value of $75,000, the amount the

lessee records as a leased asset and lease liability is increased by $75,000.

A company that prepares its financial statements according to International Financial

Reporting Standards can use all of the same inventory valuation methods as a company

that prepares its statements under U.S. GAAP.

The book value of zero-coupon bonds increases by the periodic amount of interest

recognized.

MACRS depreciation typically creates deferred tax liabilities early in the life of an

asset.

A common output method used to measure progress towards completion is to determine

the proportion of promised goods and services that have been transferred to date.

Inventory is valued at the lower of cost, net realizable value, and replacement cost.

A company that prepares its financial statements according to International Financial

Reporting Standards must calculate amortization of capitalized software development

costs in the same way as under U.S. GAAP.

Illegal acts will only need to be disclosed if the impact of the act is material.

Materiality can be affected by the dollar amount of an item, the nature of the item, or

both.

Chancellor Ltd. sells an asset with a $1 million fair value to Sophie Inc. Sophie agrees

to make six equal payments, one year apart, commencing on the date of sale. The

payments include principal and 6% annual interest. Compute the annual payments.

a. $166,651.

b. $135,252.

c. $203,351.

d. $191,852.

Which of the following transactions decreases retained earnings?

a. A property dividend.

b. A stock dividend.

c. A cash dividend.

d. All of these answer choices are correct.

The changes in account balances for Allen Inc. for 2016 are as follows:

Assuming the only changes in retained earnings in 2016 were for net income and a

$25,000 dividend, what was net income for 2016?

a. $30,000.

b. $20,000.

c. $15,000.

d. $ 5,000.

The conceptual framework’s qualitative characteristic of relevance includes:

a. Predictive value.

b. Verifiability.

c. Completeness.

d. Neutrality.

On June 1, 2016, Emmet Property Management entered into a 2-year contract to

oversee leasing and maintenance for an apartment building. The contract starts on July

1, 2016. Under the terms of the contract, Emmet will be paid a fixed fee of $50,000 per

year and will receive an additional 15% of the fixed fee at the end of each year provided

that building occupancy exceeds 90%. Emmet estimates a 30% chance it will exceed

the occupancy threshold, and concludes the revenue recognition over time is

appropriate for this contract.

Assume Emmet estimates variable consideration as the most likely amount. How much

revenue should Emmet recognize on this contract in 2016?

a. $25,000

b. $26,125

c. $28,750

d. $50,000

If an available-for-sale investment is sold for which there are unrealized gains in

accumulated other comprehensive income (AOCI), a reclassification adjustment affects

other comprehensive income (OCI) in the period of sale by:

a. Reducing OCI for the amount of unrealized gains in AOCI.

b. Increasing OCI for the amount of unrealized gains in AOCI.

c. No effect on OCI, as OCI only includes the effects of unrealized gains and losses.

d. No effect on OCI, as the realized gain is included in AOCI.

Collection of accounts receivable that previously have been written off results in an

increase in cash and an increase in:

a. Accounts receivable.

b. Allowance for uncollectible accounts.

c. Bad debts expense.

d. Retained earnings.

Four different competent accountants independently agree on the amount and method of

reporting an economic event. The concept demonstrated is:

a. Reliability.

b. Comparability.

c. Completeness.

d. Verifiability.

Magenta Company purchased a machine from Pink Corporation on October 31, 2016.

In payment for the $288,000 purchase, Magenta issued a one-year installment note to be

paid in equal monthly payments of $25,588 at the end of each month. The payments

include interest at the rate of 12%. The amount of interest expense that Magenta will

report in its income statement for the year ended December 31, 2016, is:

a. $2,559.

b. $2,880.

c. $5,533.

d. $5,760.

Calistoga Produce estimates bad debt expense at ½% of credit sales. The company

reported accounts receivable and allowance for uncollectible accounts of $471,000 and

$1,650, respectively, at December 31, 2015. During 2016, Calistoga’s credit sales and

collections were $315,000 and $319,000, respectively, and $1,720 in accounts

receivable were written off. Calistoga’s accounts receivable at December 31, 2016, are:

a. $467,000.

b. $473,280.

c. $465,280.

d. $469,280.

The attribution period for postretirement benefits spans each year of service from the

employee’s date of hire to the employee’s date of:

a. Full eligibility.

b. Death.

c. Retirement.

d. Termination.

To determine the future value factor for an annuity due for period n when given tables

only for an ordinary annuity:

a. Obtain the FVA factor for n + 1 and deduct 1.

b. Obtain the FVA factor for n and deduct 1.

c. Obtain the FVA factor for n – 1 and add 1.

d. Obtain the FVA factor for n + 1 and add 1.

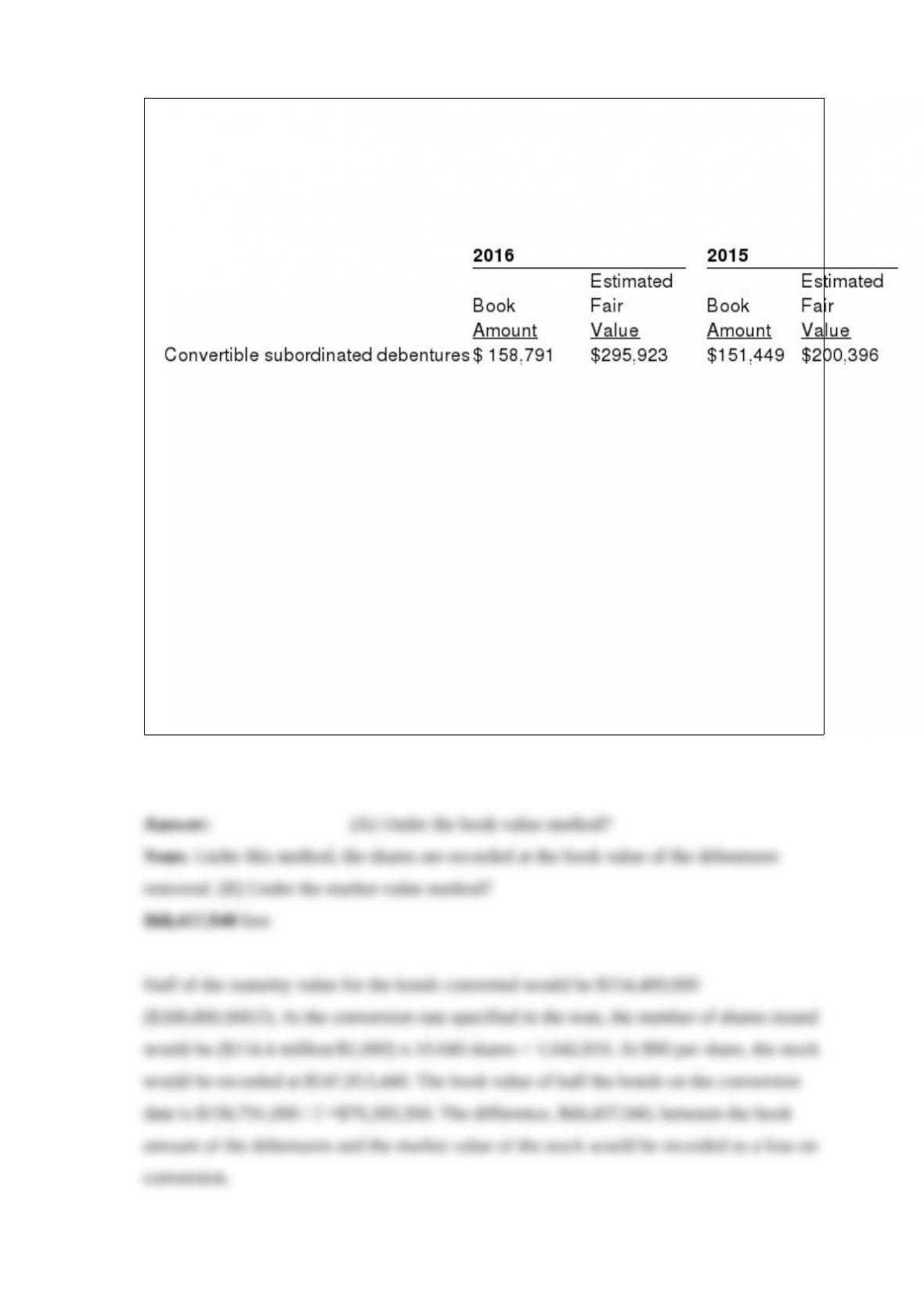

In its 2016 annual report to shareholders, Health Foods, Inc., disclosed the following

information about some of its indebtedness: The fair value of convertible subordinated

debentures is estimated using quoted market prices. Book amounts and estimated fair

values of our financial instruments other than those for which book amounts

approximate fair values as noted above are as follows (in thousands)

In addition, the company disclosed the following: We have outstanding zero coupon

convertible subordinated debentures which had a book amount of approximately $158.8

million and $151.4 million at September 26, 2016, and September 28, 2015,

respectively. The debentures have an effective yield to maturity of 5 percent and a

principal amount at maturity on March 2, 2030, of approximately $308.8 million. The

debentures are convertible at the option of the holder, at any time on or prior to

maturity, unless previously redeemed or otherwise purchased. The debentures have a

conversion rate of 10.64 shares per $1,000 principal amount at maturity, representing

3,285,632 shares. The debentures may be redeemed at the option of the holder on

March 2, 2020, or March 2, 2025, at the issue price plus accrued original discount

totaling approximately $188 million and $241 million, respectively.

Required: Suppose that half of the bondholders had converted them into Health Foods’

stock at the end of the 2016 fiscal year when the stock price is $90 per share. What gain

or loss from this conversion would Health Foods have recorded on the transaction using

the book value method? The market value method?

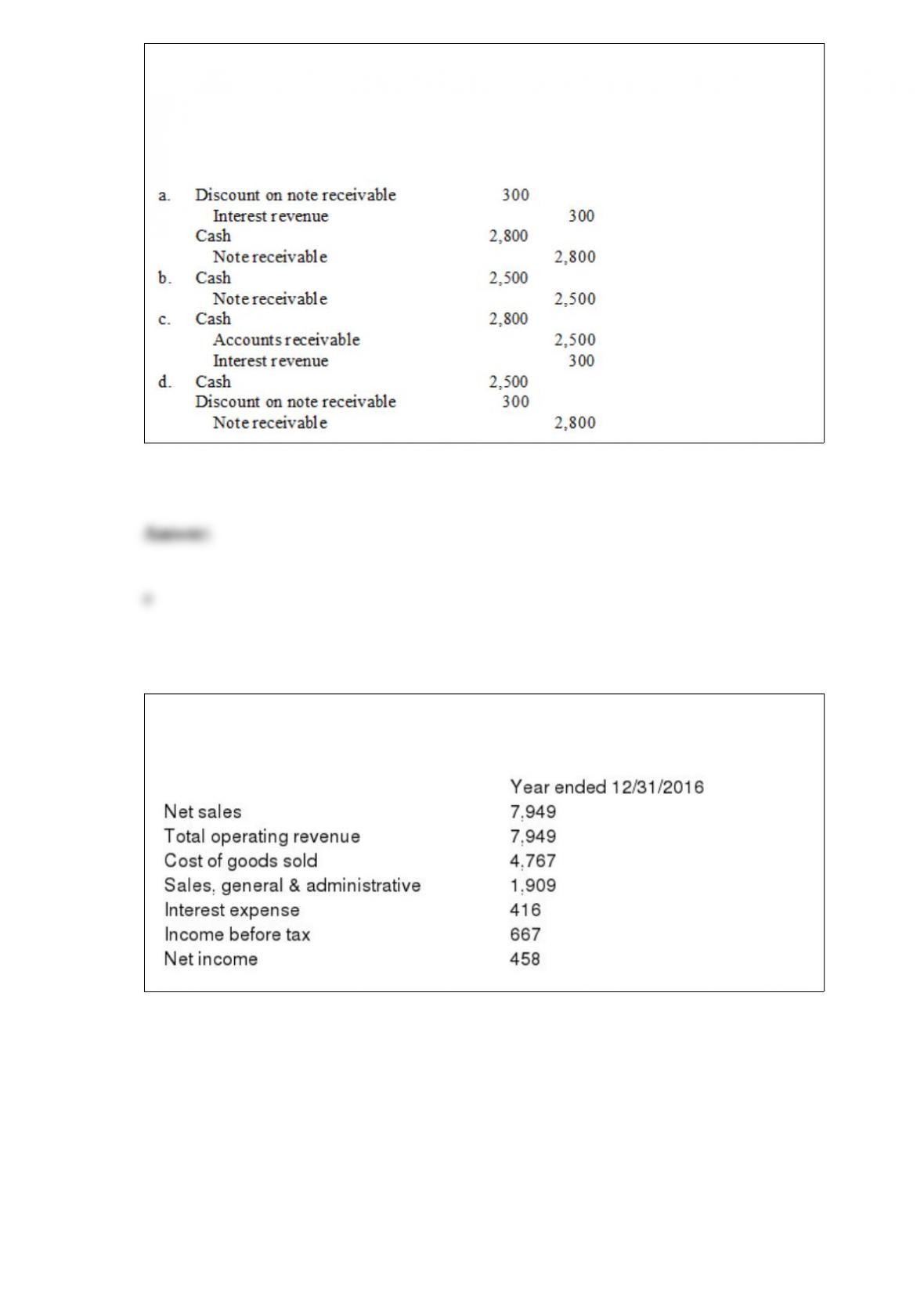

Plunder Inc. accepted a six-month noninterest-bearing note for $2,800 on January 1,

2016. The note was accepted as payment of a delinquent receivable of $2,500.

The cash collection on July 1, 2016, would be recorded as:

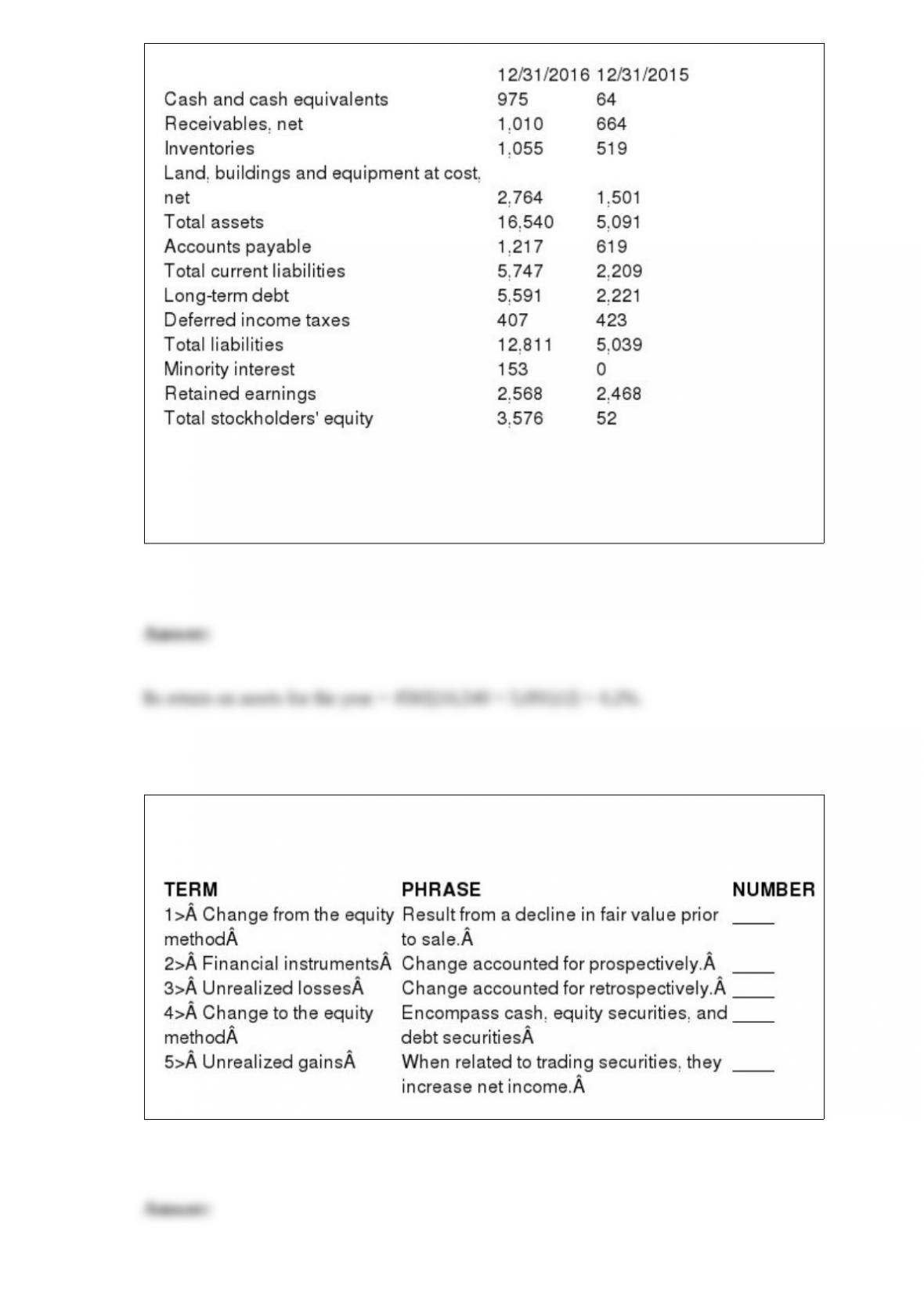

The following partial income statement and balance sheet information (in $ millions)

comes from the Annual Report of Saratoga Springs Co. for the year ending 12/31/2016:

Required: Compute the following amounts for Saratoga Springs Co.

Its return on assets for 2016. Round your answer to one decimal place, e.g., .1234 as

12.3%.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

Capital Consulting Company had 400,000 shares of common stock outstanding on

December 31, 2016. On that date, there were also 5,000 shares of $100 par, 6%

noncumulative preferred stock outstanding. On March 1, 2016, the company’s common

stock split 3-for-1. On December 15, 2016, a preferred dividend was declared and paid

in the amount of $25,000. Net income for 2016 was $3,000,000.

Required:

Compute basic earnings per share (rounded to 2 decimal places) for the year ended

December 31, 2016.

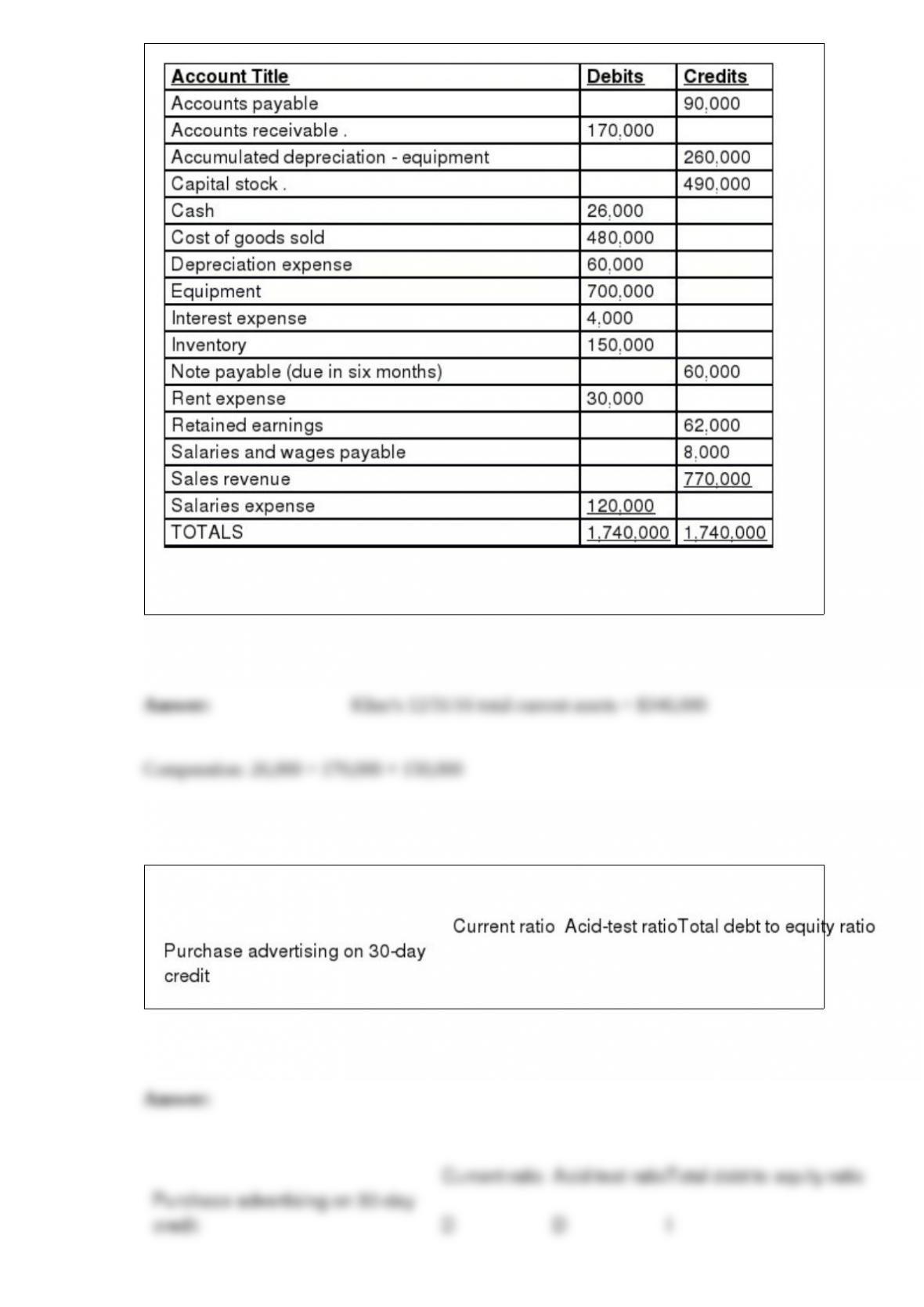

The December 31, 2016 (pre-closing) adjusted trial balance for Kline Enterprises was

as follows:

Required: Assuming no income taxes, compute the following, and place your answer

in the space provided: Kline’s 12/31/16 total current assets:

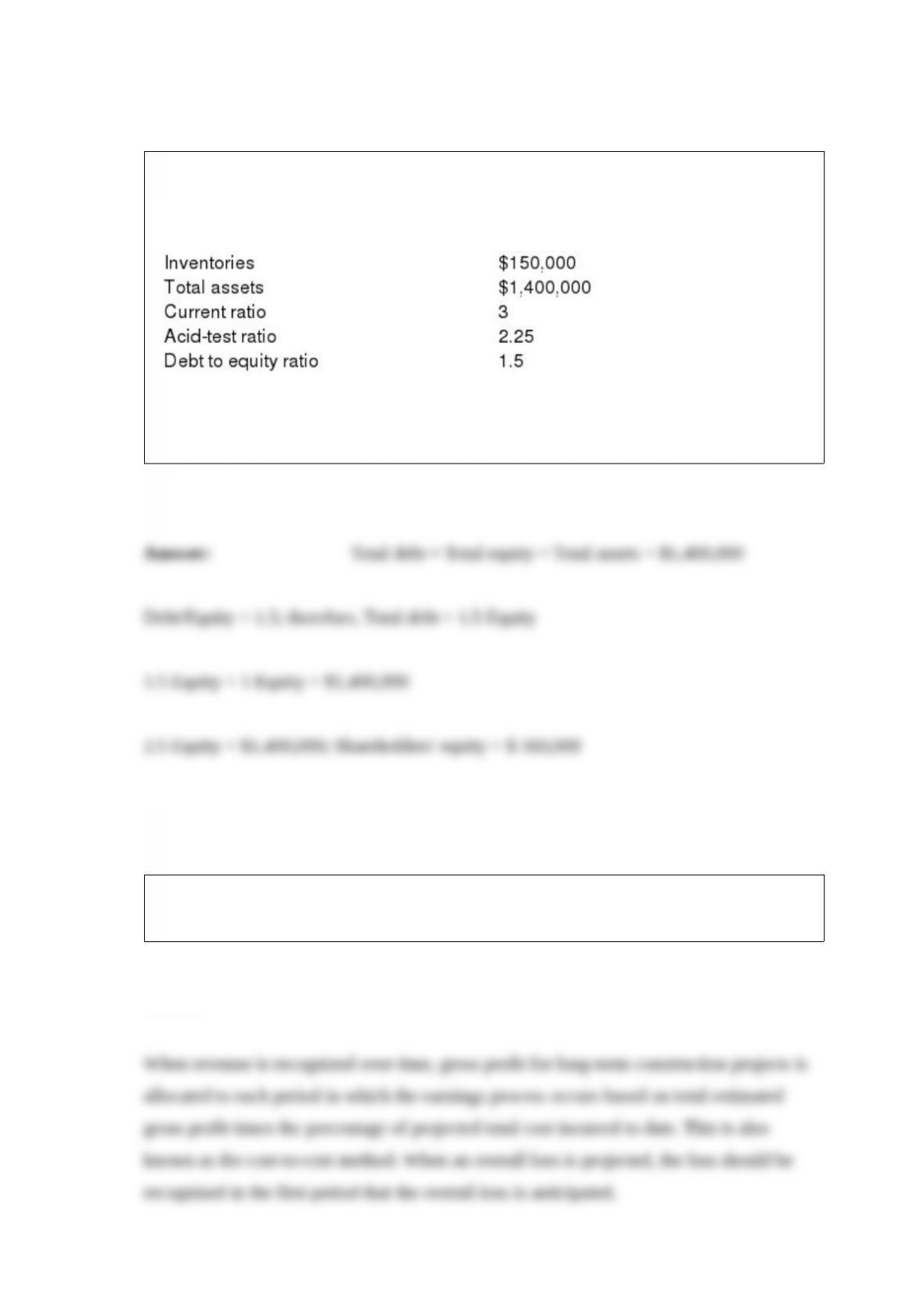

Bronco Electronics’ current assets consist of cash, marketable securities, accounts

receivable, and inventories. The following data were abstracted from a recent financial

statement:

Required: Compute the following for Bronco:

Shareholders’ equity

Briefly explain how gross profit is recorded when revenue on long-term construction

projects is recognized over time according to percentage of completion.