1) ( An investment project has the following characteristics:

The life of the equipment is closest to:

A.It is impossible to determine from the data given.

B.7 years

C.12 years

D.4.56 years.

2) If the company bases its predetermined overhead rate on capacity, the predetermined

overhead rate is closest to:

The management of Richbourg Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. The company’s controller

has provided an example to illustrate how this new system would work. In this

example, the allocation base is machine-hours and the estimated amount of the

allocation base for the upcoming year is 63,000 machine-hours. In addition, capacity is

70,000 machine-hours and the actual level of activity for the year is 66,200

machine-hours. All of the manufacturing overhead is fixed and is $2,866,500 per year.

For simplicity, it is assumed that this is the estimated manufacturing overhead for the

year as well as the manufacturing overhead at capacity. It is further assumed that this is

also the actual amount of manufacturing overhead for the year.

A.$9.28

B.$12.56

C.$11.52

D.$10.34

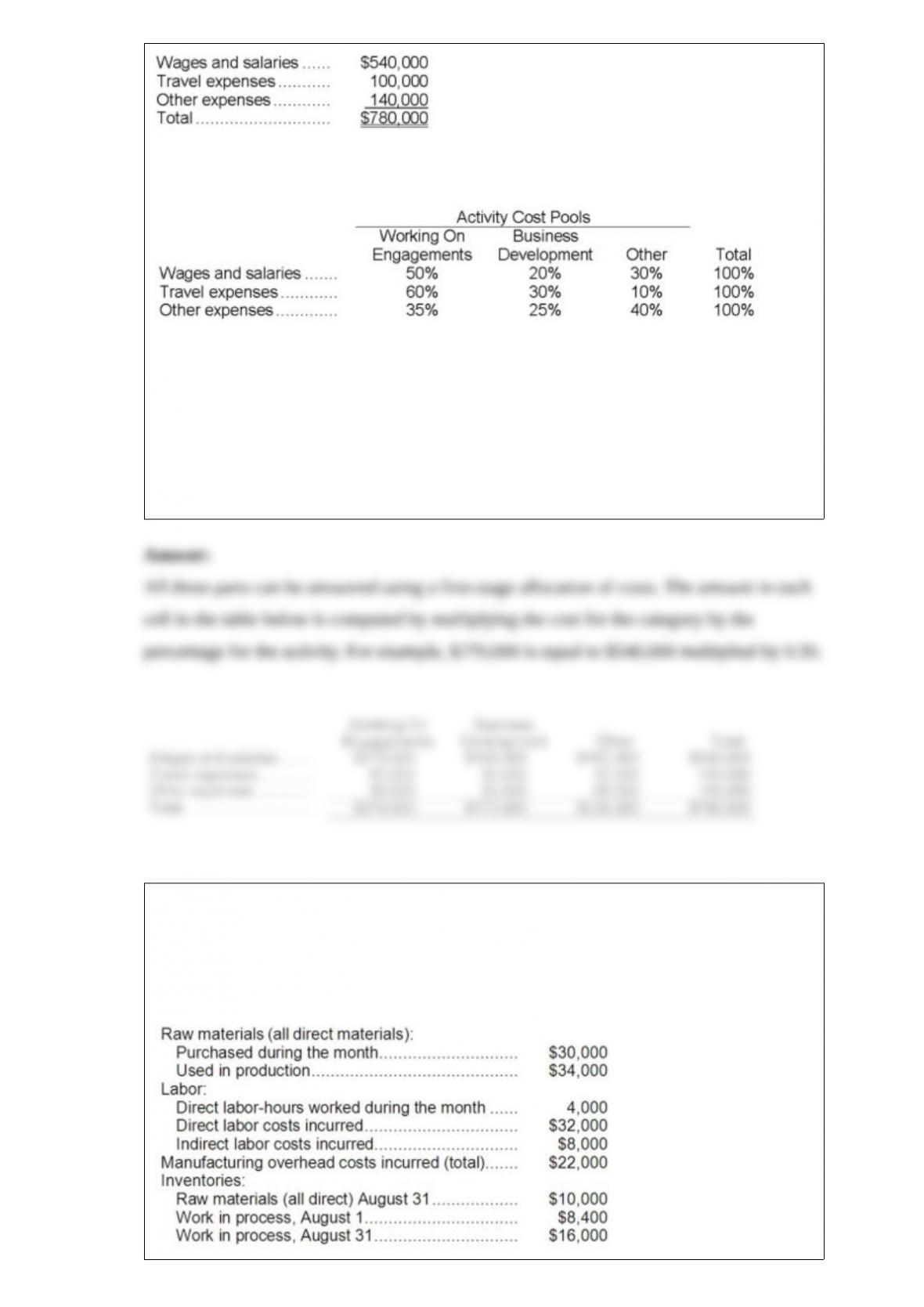

3) Fife & Jones PLC, a consulting firm, uses an activity-based costing in which there

are three activity cost pools. The company has provided the following data concerning

its costs and its activity based costing system:

Costs:

Distribution of resource consumption:

Required:

a. How much cost, in total, would be allocated to the Working On Engagements activity

cost pool?

b. How much cost, in total, would be allocated to the Business Development activity

cost pool?

c. How much cost, in total, would be allocated to the Other activity cost pool?

4) Maggie Manufacturing Company applies manufacturing overhead to jobs using a

predetermined overhead rate of 75% of direct labor cost. Any underapplied or

overapplied overhead is closed to Cost of Goods Sold at the end of the month. During

August, the following transactions were recorded by the company:

Required:

Determine the following:

a. The August 1 balance of Raw Materials.

b. The amount of manufacturing overhead applied to jobs in August.

c. The Cost of Goods Manufactured for August.

d. The overapplied or underapplied manufacturing overhead for the month. Label this

amount appropriately.

5) Sand Company has an acid-test ratio of 0.8. Which of the following actions would

improve the acid-test ratio?

A.Collect some accounts receivable.

B.Acquire some inventory on account.

C.Sell some equipment for cash.

D.Use cash to pay off some accounts payable.

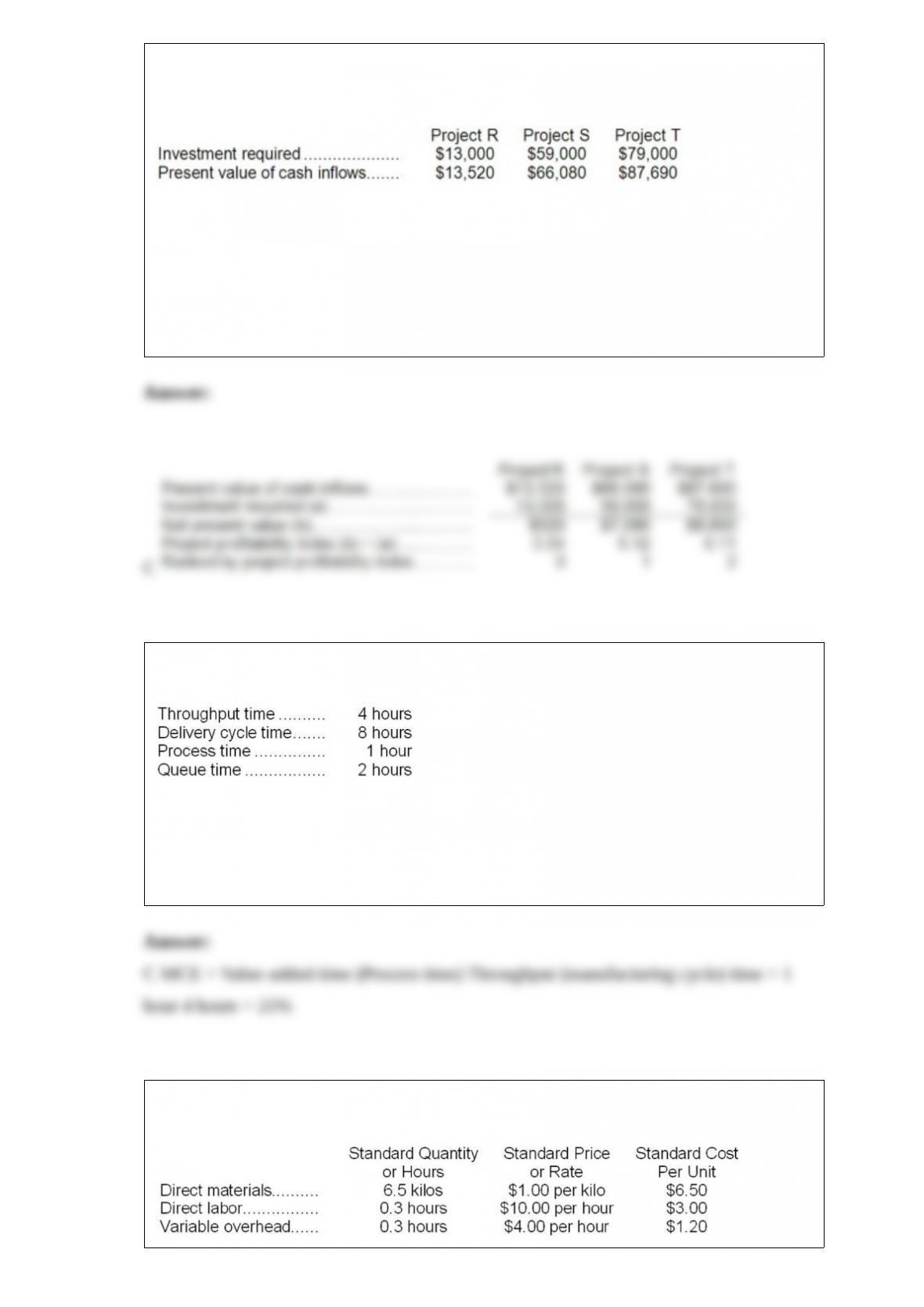

6) ( The management of Edelmann Corporation is considering the following three

investment projects:

Rank the projects according to the profitability index, from most profitable to least

profitable.

A.T, S, R

B.R, T, S

C.S, T, R

D.T, R, S

7) The following data pertain to operations at Quick Incorporated:

The manufacturing cycle efficiency (MCE) for this operation would be:

A.50%

B.75%

C.25%

D.12%

8) Eliezrie Corporation makes a product with the following standard costs:

In January the company’s budgeted production was 7,400 units but the actual

production was 7,500 units. The company used 45,580 kilos of the direct material and

2,030 direct labor-hours to produce this output. During the month, the company

purchased 48,500 kilos of the direct material at a cost of $53,350. The actual direct

labor cost was $18,473 and the actual variable overhead cost was $7,714.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The variable overhead efficiency variance for January is:

A.$836 F

B.$836 U

C.$880 F

D.$880 U

9) Bosques Corporation has in stock 35,800 kilograms of material L that it bought five

years ago for $5.55 per kilogram. This raw material was purchased to use in a product

line that has been discontinued. Material L can be sold as is for scrap for $1.67 per

kilogram. An alternative would be to use material L in one of the company’s current

products, Q08C, which currently requires 2 kilograms of a raw material that is available

for $9.15 per kilogram. Material L can be modified at a cost of $0.78 per kilogram so

that it can be used as a substitute for this material in the production of product Q08C.

However, after modification, 4 kilograms of material L is required for every unit of

product Q08C that is produced. Bosques Corporation has now received a request from a

company that could use material L in its production process. Assuming that Bosques

Corporation could use all of its stock of material L to make product Q08C or the

company could sell all of its stock of the material at the current scrap price of $1.67 per

kilogram, what is the minimum acceptable selling price of material L to the company

that could use material L in its own production process?

A) $5.365 per kg

B) $3.795 per kg

C) $2.133 per kg

D) $1.675 per kg

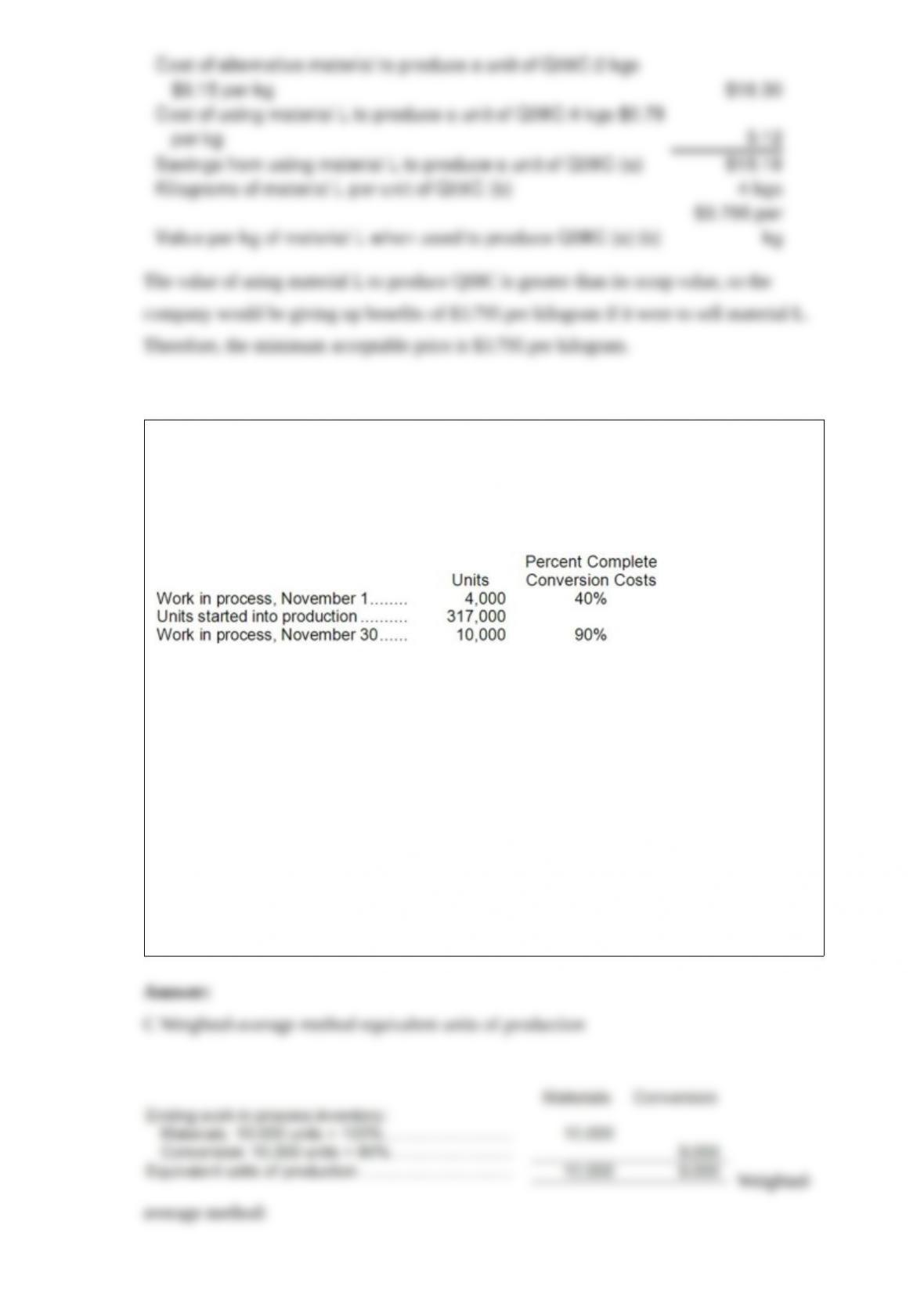

10) The following information relates to the Assembly Department of Jataca

Corporation for the month of November. Jataca uses a weighted-average process

costing system. All materials at Jataca are added at the beginning of the production

process.

On November 1, the work in process inventory account contained $6,400 of material

cost and $4,400 of conversion cost. Cost per equivalent unit for November was $1.50

for materials and $2.80 for conversion costs.

What total amount of cost should be assigned to the units in work in process on

November 30?

A.$17,800

B.$38,700

C.$40,200

D.$43,000

11) Derf Corporation uses a standard cost system in which it applies manufacturing

overhead on the basis of standard direct labor-hours. Two direct labor-hours are

required for each unit produced. The denominator activity was set at 9,000 units.

Manufacturing overhead was budgeted at $135,000 for the period; 20 percent of this

cost was fixed. The 17,200 hours worked during the period resulted in production of

8,500 units. Variable manufacturing overhead cost incurred was $108,500 and fixed

manufacturing overhead cost was $28,000.

The fixed manufacturing overhead budget variance for the period was:

A.$6,300 Unfavorable

B.$2,500 Unfavorable

C.$1,500 Unfavorable

D.$1,000 Unfavorable

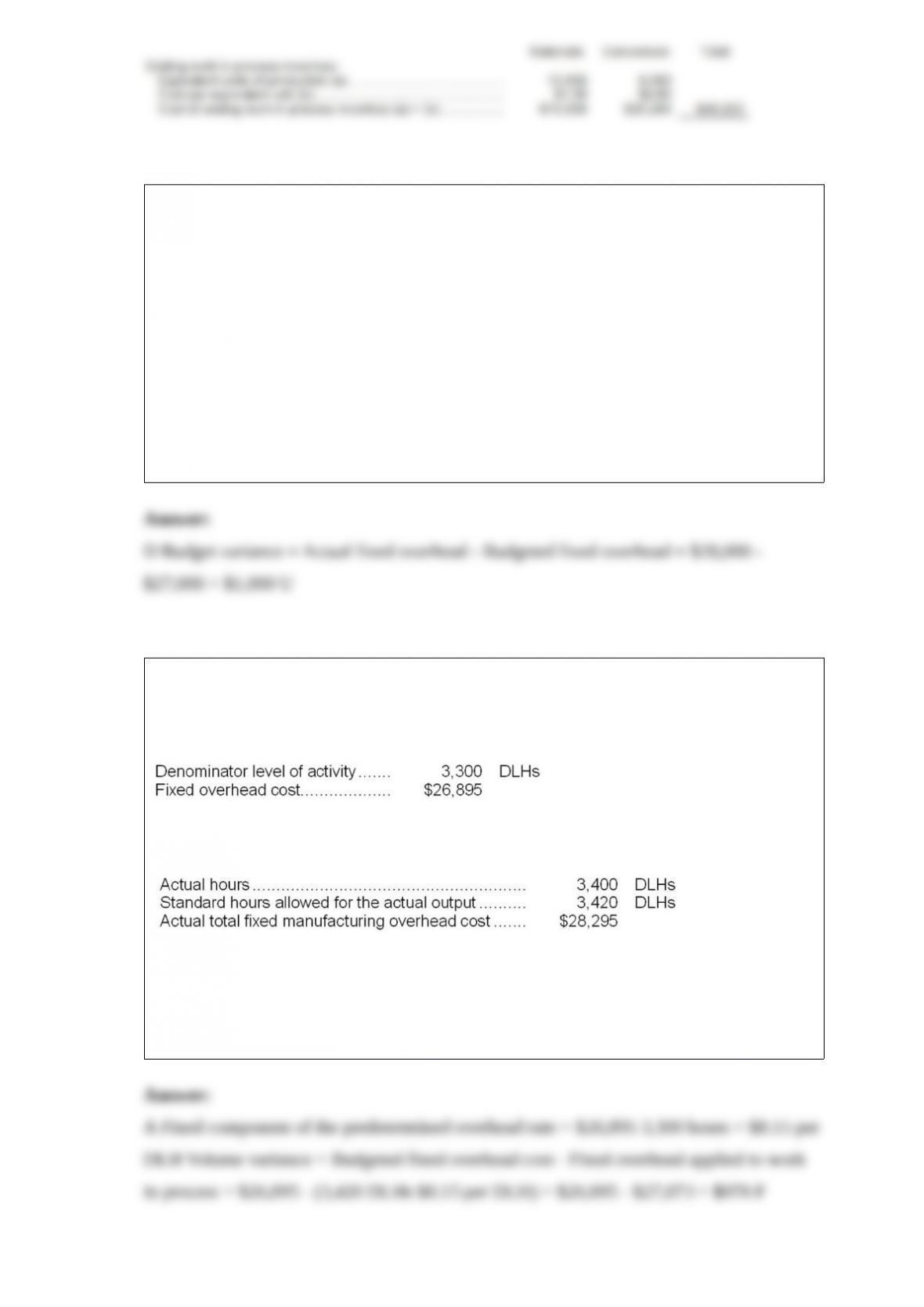

12) An outdoor barbecue grill manufacturer has a standard costing system based on

standard direct labor-hours (DLHs) as the measure of activity. Data from the company’s

flexible budget for manufacturing overhead are given below:

The following data pertain to operations for the most recent period:

The fixed manufacturing overhead volume variance for the period is closest to:

A.$978 F

B.$993 F

C.$163 F

D.$815 F

13) Overapplied manufacturing overhead means that:

A.the applied manufacturing overhead cost was less than the actual manufacturing

overhead cost.

B.the applied manufacturing overhead cost was greater than the actual manufacturing

overhead cost.

C.the estimated manufacturing overhead cost was less than the actual manufacturing

overhead cost.

D.the estimated manufacturing overhead cost was less than the applied manufacturing

overhead cost.

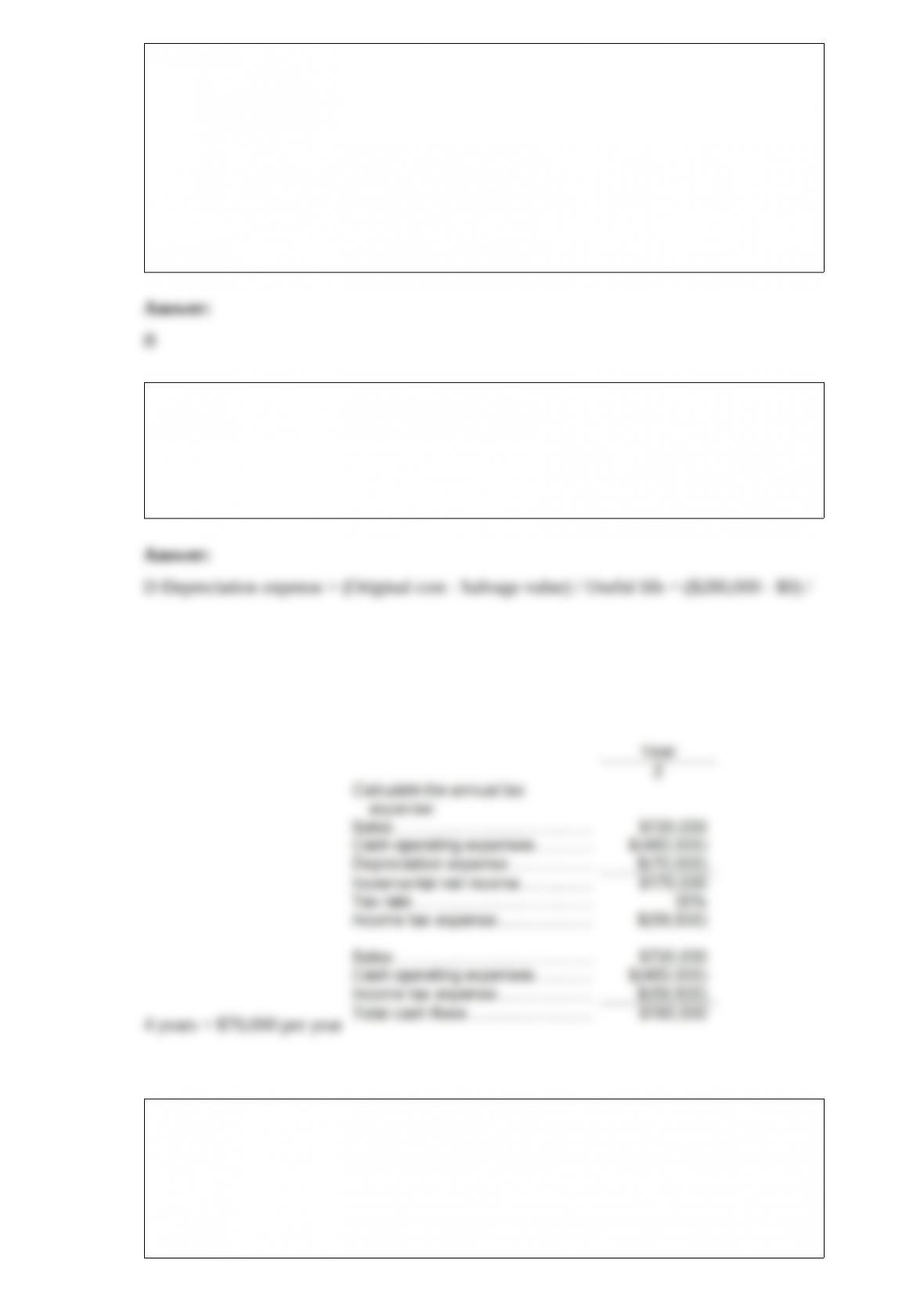

14) The total cash flow net of income taxes in year 2 is:

A.$170,000

B.$115,500

C.$240,000

D.$180,500

15) Kosakowski Corporation processes sugar beets in batches. A batch of sugar beets

costs $66 to buy from farmers and $17 to crush in the company’s plant. Two

intermediate products, beet fiber and beet juice, emerge from the crushing process. The

beet fiber can be sold as is for $23 or processed further for $13 to make the end product

industrial fiber that is sold for $36. The beet juice can be sold as is for $42 or processed

further for $20 to make the end product refined sugar that is sold for $84. How much

profit (loss) does the company make by processing one batch of sugar beets into the end

products industrial fiber and refined sugar?

A) $(18)

B) $4

C) $22

D) $(116)

16) Eberley Corporation’s cost formula for its manufacturing overhead is $25,700 per

month plus $10 per machine-hour. For the month of July, the company planned for

activity of 5,900 machine-hours, but the actual level of activity was 5,920

machine-hours. The actual manufacturing overhead for the month was $86,800.

The activity variance for manufacturing overhead in July would be closest to:

A.$2,100 U

B.$200 U

C.$200 F

D.$2,100 F