1) The business entity principle means that accounting information reflects a

presumption that the business will continue operating instead of being closed or sold.

2) Using the retail inventory method, if the cost to retail ratio is 70% and ending

inventory at retail is $145,000, then estimated ending inventory at cost is $207,143.

3) The process of preparing departmental income statements begins with allocating

service department expenses.

4) The full disclosure principle requires the reporting of contingent liabilities that are

reasonably possible.

5) The times interest earned ratio is calculated by dividing interest expense by income

before interest expense and income taxes.

6) Process costing systems are commonly used by companies that produce a large

volume of standardized units on a continuous basis.

7) A company issued 8%, 15-year bonds with a par value of $550,000 that pay interest

semi-annually. The current market rate is 8%. The journal entry to record each

semiannual interest payment is:

A.Debit Bond Interest Expense $22,000; credit Cash $22,000.

B.Debit Bond Interest Expense $44,000; credit Cash $44,000.

C.Debit Bond Interest Payable $22,000; credit Cash $22,000.

D.Debit Bond Interest Expense $550,000; credit Cash $550,000.

E.No entry is needed, since no interest is paid until the bond is due.

8) Wallace and Simpson formed a partnership with Wallace contributing $60,000 and

Simpson contributing $40,000. Their partnership agreement calls for the income (loss)

division to be based on the ratio of capital investments. The partnership had income of

$150,000 for its first year of operation. When the Income Summary is closed, the

journal entry to allocate partner income is:

A.Debit Income Summary $150,000; credit Wallace, Capital $75,000; credit Simpson,

Capital $75,000.

B.Debit Wallace, Capital $75,000; debit Simpson, Capital $75,000; credit Income

Summary $150,000.

C.Debit Income Summary $150,000; credit Wallace, Capital $90,000; credit Simpson,

Capital $60,000.

D.Debit Cash $150,000; credit Wallace, Capital $90,000; credit Simpson, Capital

$60,000.

E.Debit Wallace, Capital $90,000; debit Simpson, Capital $60,000; credit Cash

$150,000.

9) Landmark buys $300,000 of Schroeter Company’s 8% five-year bonds payable at par

value on September 1. Interest payments are made semiannually on March 1 and

September 1. The journal entry Landmark should record to accrue interest earned at

year-end December 31 is:

A.Debit Interest Receivable $8,000, credit Interest Revenue $8,000.

B.Debit Interest Receivable $12,000, credit Interest Revenue $12,000.

C.Debit Cash $8,000, credit Interest Revenue $8,000.

D.Debit Cash $12,000, credit Interest Revenue $12,000.

E.Debit Interest Revenue $8,000, credit Interest Receivable $8,000.

10) Palmer Company is at the end of its annual accounting period. The accountant has

journalized and posted all external transactions and all adjusting entries, had prepared

an adjusted trial balance, and completed the financial statements. The next step in the

accounting cycle is:

A.Prepare a work sheet.

B.Prepare reversing entries.

C.Close temporary accounts.

D.Prepare a post-closing trial balance.

E.Prepare an unadjusted trial balance.

11) Which of the following journals would a company use to record a merchandise

return?

A.General journal.

B.Cash receipts journal.

C.Cash disbursements journal.

D.Purchases journal.

E.Sales journal.

12) Activity based costing can improve costing activity for:

A.Manufacturing companies only.

B.Service companies only.

C.Merchandising companies only.

D.Any company in any industry.

E.Government entities only.

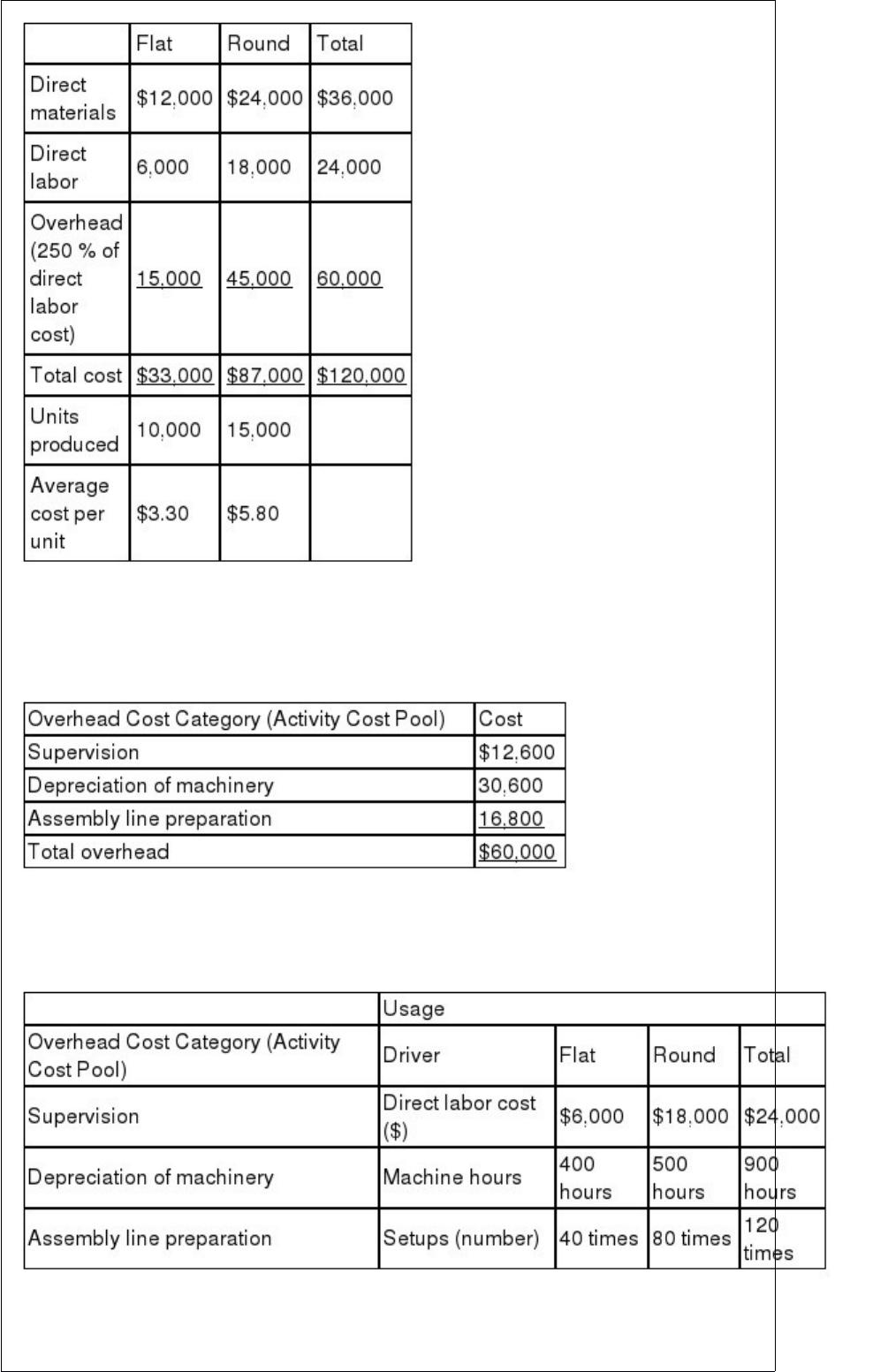

13) Rockaway Company produces two types of product, flat and round, on the same

production line. For the current period, the company reports the following data.

Rockaway’s controller wishes to apply activity-based costing (ABC) to allocate the

$60,000 of overhead costs incurred by the two product lines to see whether cost per unit

would change markedly from that reported above. She has collected the following

information.

She has also collected the following information about the cost drivers for each

category (cost pool) and the amount of each driver used by the two product lines.

Assign these three overhead cost pools to each of the two products using ABC. Show

each overhead cost allocation by product and the total overhead allocated to each

product. Determine average cost per unit for each of the two products using ABC.

(Round your answer to 2 decimal places.) Which overhead cost allocation method

would you recommend to the controller?

14) Costs that the manager has the power to determine or at least significantly affect are

called:

A.Uncontrollable costs.

B.Controllable costs.

C.Joint costs.

D.Direct costs.

E.Indirect costs.

15) Par value of a stock refers to the:

A.Issue price of the stock.

B.Value assigned per share by the corporate charter.

C.Market value of the stock on the date of the financial statements.

D.Maximum selling price of the stock.

E.Dividend value of the stock.

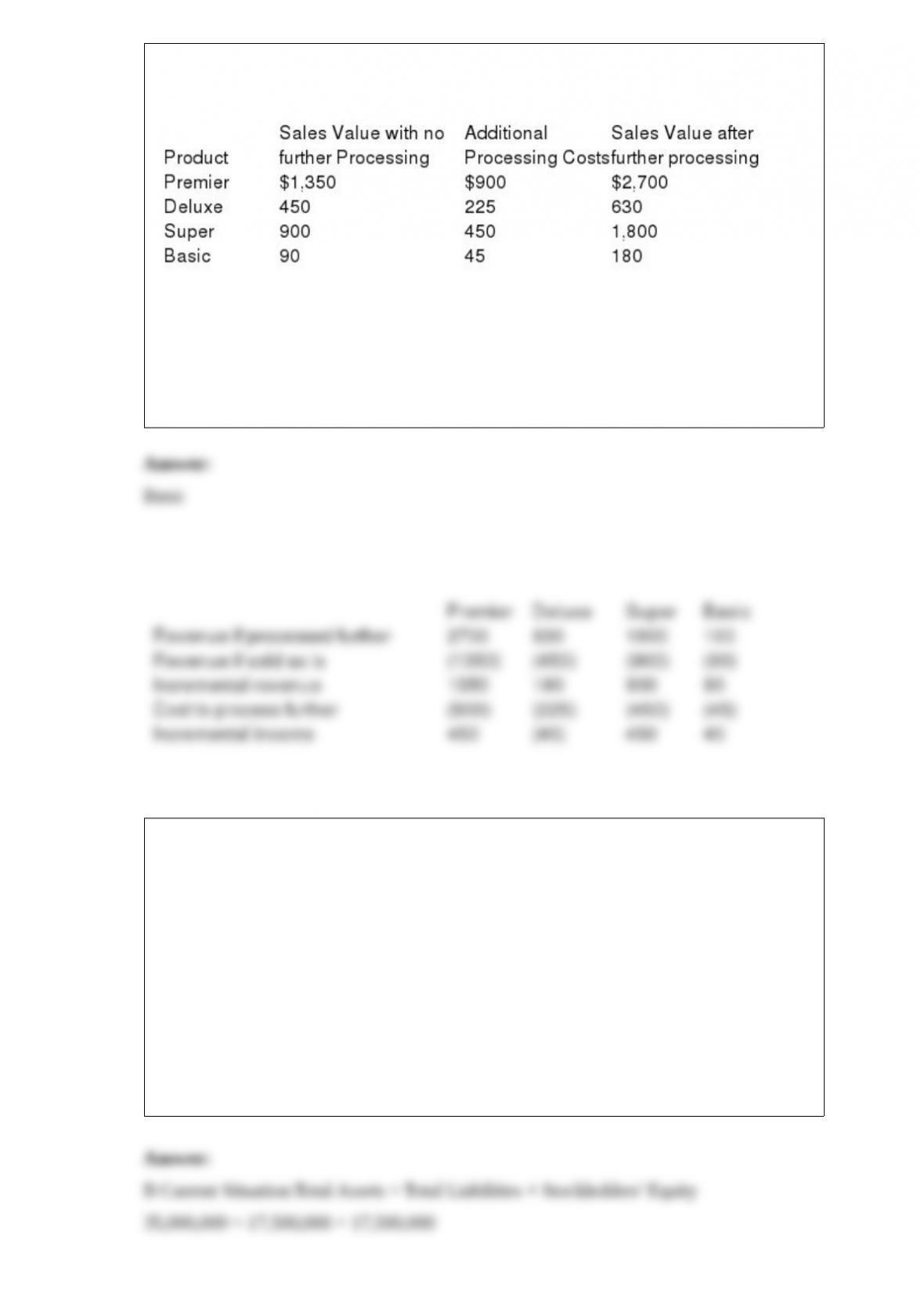

16) Listmann Corp. processes four different products that can either be sold as is or

processed further.

Listed below are sales and additional cost data:

Which product(s) should not be processed further?

A.Premier.

B.Deluxe.

C.Super.

D.Basic.

E.Premier and Basic.

17) Seedly Corporation’s most recent balance sheet reports total assets of $35,000,000

and total liabilities of $17,500,000. Management is considering issuing $5,000,000 of

par value bonds (at par) with a maturity date of ten years and a contract rate of 7%.

What effect, if any, would issuing the bonds have on the company’s debt-to-equity

ratio?

A.Issuing the bonds would cause the firm’s debt-to-equity ratio to improve from 1.0 to

1.3.

B.Issuing the bonds would cause the firm’s debt-to-equity ratio to worsen from 1.0 to

1.3.

C.Issuing the bonds would cause the firm’s debt-to-equity ratio to remain unchanged.

D.Issuing the bonds would cause the firm’s debt-to-equity ratio to improve from .5 to .8.

E.Issuing the bonds would cause the firm’s debt-to-equity ratio to worsen from .5 to .8.

18) If a company failed to make the end-of-period adjustment to move the amount of

management fees that were earned from the Unearned Management Fees account to the

Management Fees Revenue account, this omission would cause:

A.An overstatement of net income.

B.An overstatement of assets.

C.An overstatement of liabilities.

D.An overstatement of equity.

E.An understatement of liabilities.

19) A resource that the owner takes from the company is called a(n):

A.Liability.

B.Withdrawal.

C.Expense.

D.Contribution.

E.Investment.

20) At the end of the day, the cash register tape shows $1,020 in cash sales but the count

of cash in the register is $1,035. The proper entry to account for this excess is:

A.Debit Cash $1,020; credit Sales $1,020.

B.Debit Cash $1,035; credit Sales $1,035.

C.Debit Cash $1,035; credit Sales $1,020; credit Cash Over and Short $15.

D.Debit Cash $1,020; debit Cash Over and Short for $15; credit Sales $1,035.

E.Debit Cash Over and Short $15; credit Cash $15.

21) A plan that shows the expected cash inflows and cash outflows during the budget

period, including receipts from loans needed to maintain a minimum cash balance and

repayments of such loans, is called a(n):

A.Capital expenditures budget.

B.Operating budget.

C.Rolling budget.

D.Cash budget.

E.Income statement.

22) On a bank reconciliation, the amount of an unrecorded bank service charge should

be:

A.Added to the book balance of cash.

B.Deducted from the book balance of cash.

C.Added to the bank balance of cash.

D.Deducted from the bank balance of cash.

E.Noted in memorandum form only.

23) The ability to generate future revenues and meet long-term obligations is referred to

as:

A.Liquidity and efficiency.

B.Solvency.

C.Profitability.

D.Market prospects.

E.Creditworthiness.

24) Minor Company installs a machine in its factory at the beginning of the year at a

cost of $135,000. The machine’s useful life is estimated to be 5 years, or 300,000 units

of product, with a $15,000 salvage value. During its first year, the machine produces

64,500 units of product. Determine the machines’ first year depreciation under the

double-declining-balance method.

A.$66,000.

B.$54,000.

C.$24,000.

D.$25,800.

E.$48,000.

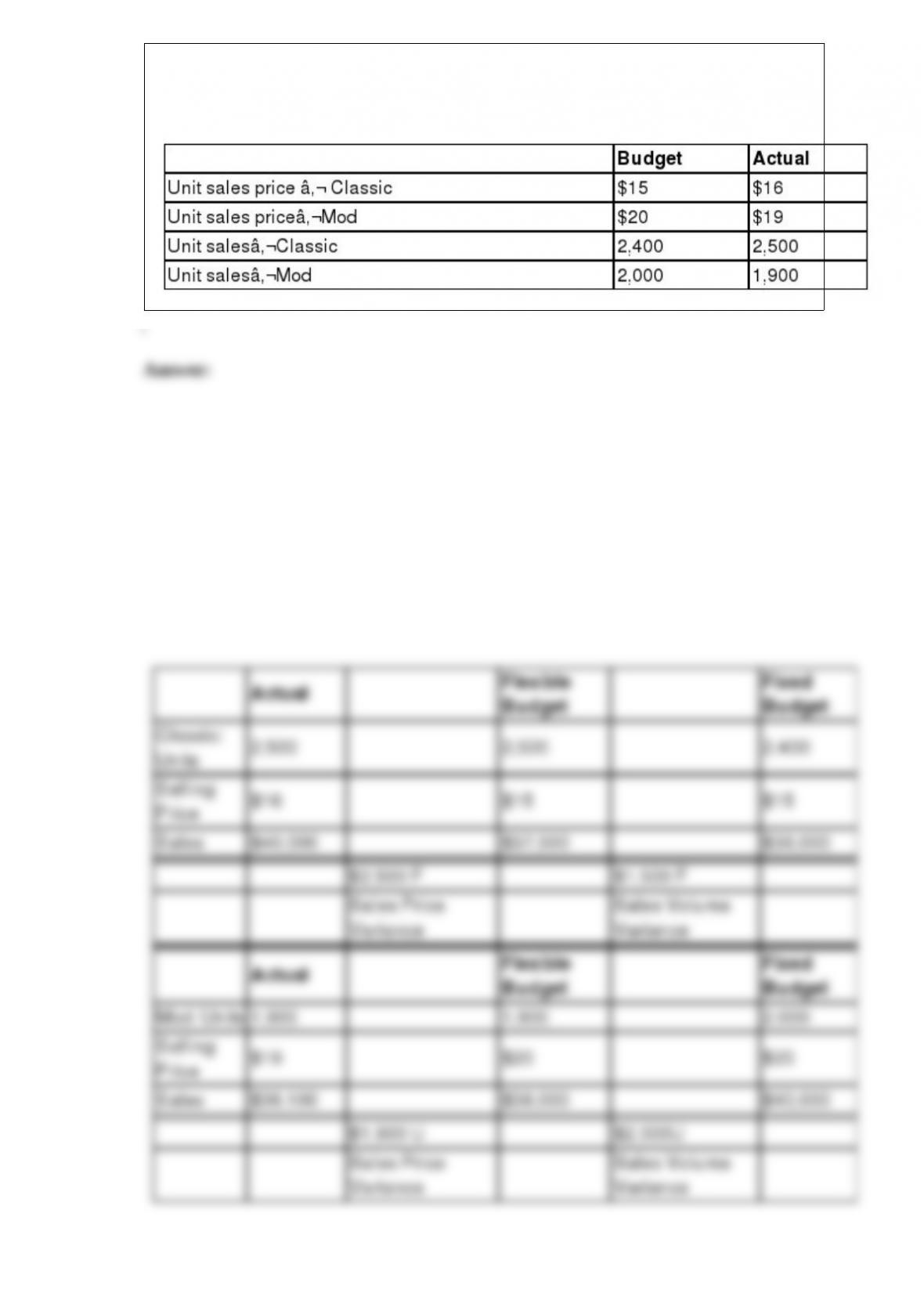

25) Oxford Co. produces and sells two lines of t-shirts, Classic and Mod. Oxford

provides the following data. Compute the sales price and the sales volume variances for

each product.

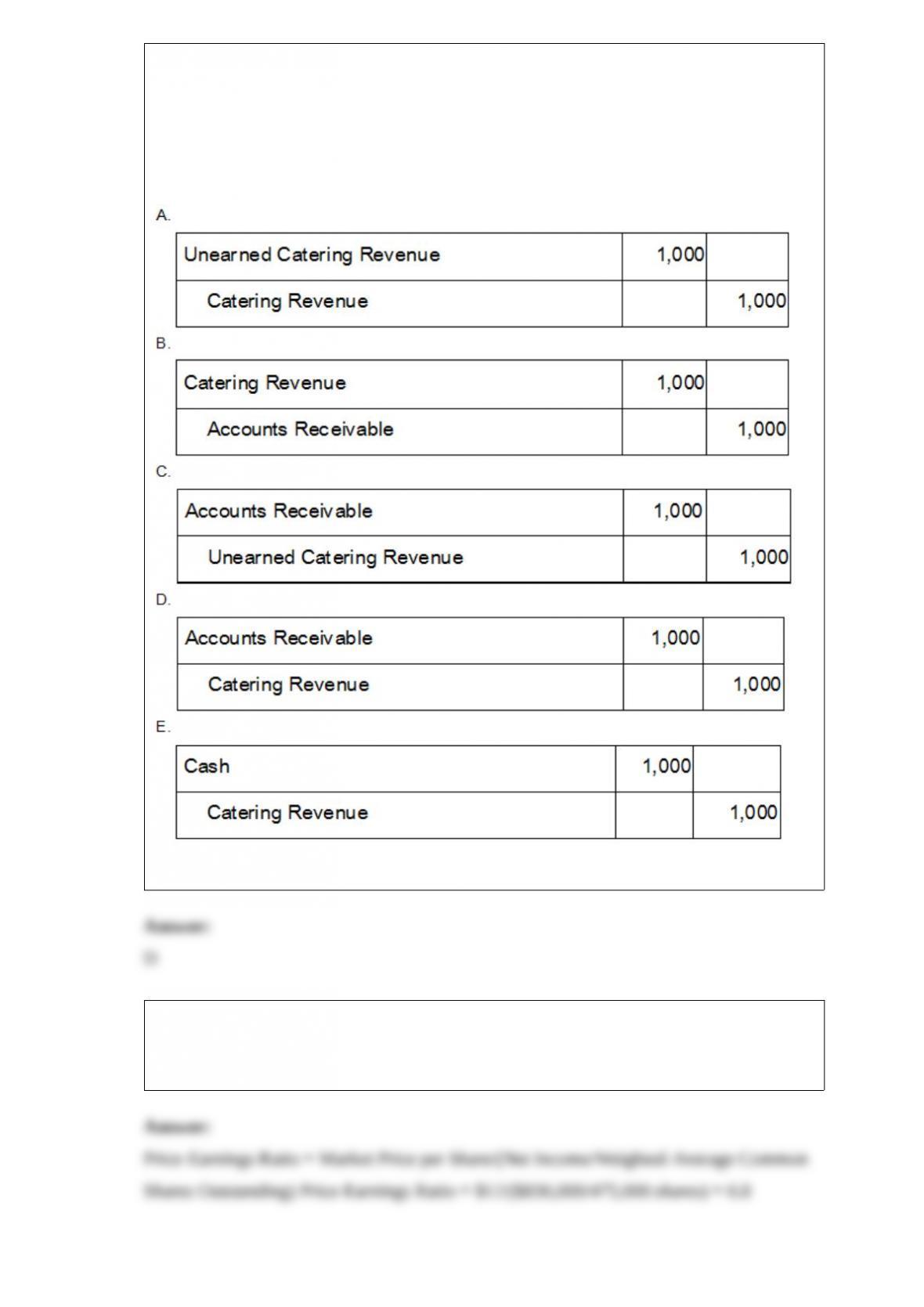

26) Grills R Us Catering provided $1,000 of catering services and billed its client for

the amount owed. Given the choices below, determine the general journal entry that

Grills R Us Catering will make to record this transaction.

27) A company reported net income of $836,000 for the current year. The year-end

market price per common share was $12 and there were 475,000 weighted-average

shares of common stock outstanding. Calculate the company’s price-earnings ratio.

28) You have evaluated three projects of similar investment amount and risk using the

net present value (NPV) method. How would you decide which one of the projects to

select?

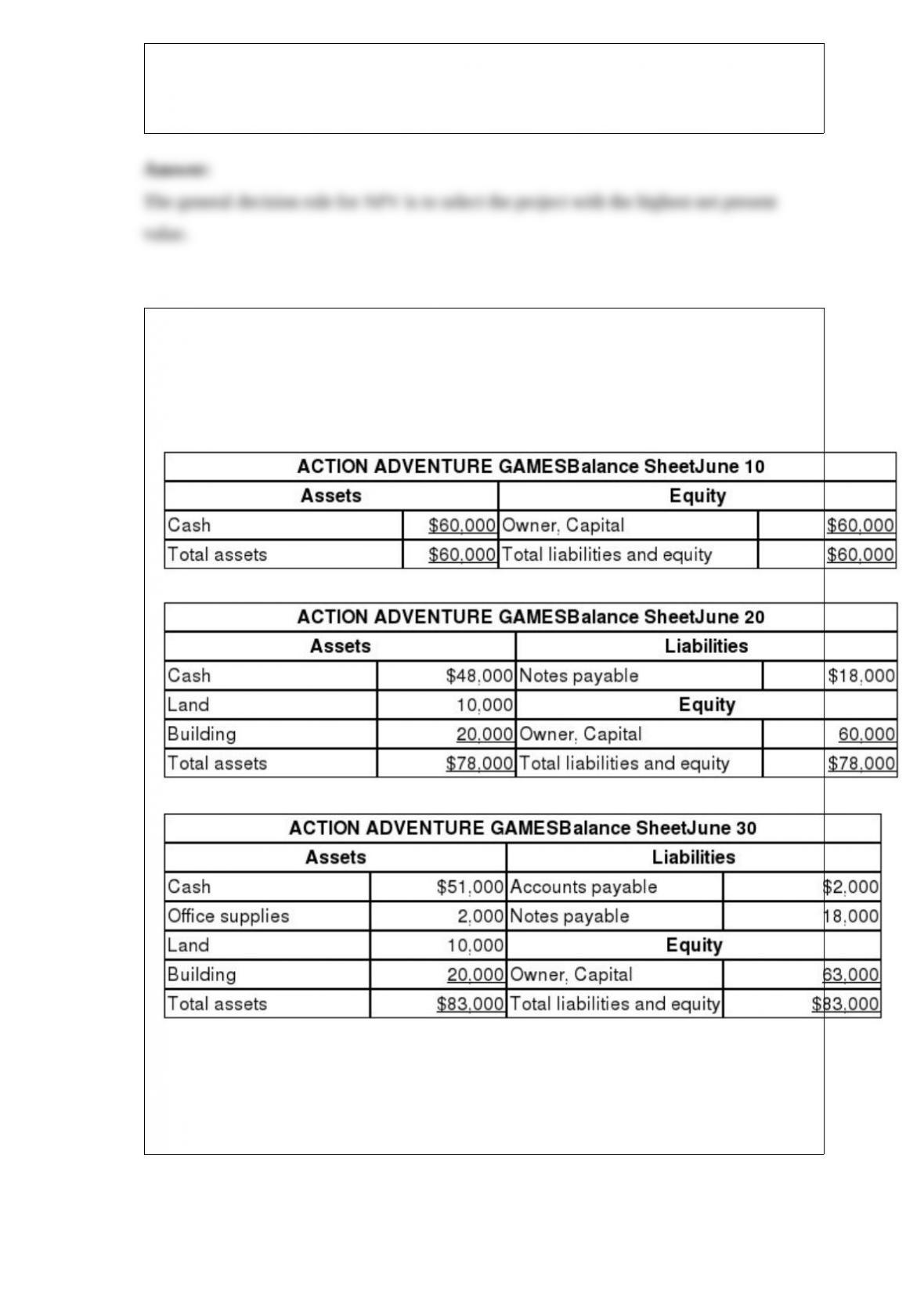

29) The accountant of Action Adventure Games prepared a balance sheet after every 10

day period. The only resources invested by the owner were at the start of the company

on June 1. During June, the first month of operation, the following balance sheets were

prepared:

Required:

Describe the nature of each of the four transactions that took place between the balance

sheet dates shown. Assume only one transaction affected each account.

30) On June 30, a company declared a cash dividend of $0.35 per common share to the

shareholders of record on July 15. The cash dividend will be paid on July 31. This

company has 500,000 shares authorized and 100,000 shares outstanding. Prepare the

journal entries required on June 30, July 15 and July 31.