Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1) Companies value and report short-term receivables at net realizable valuethe net

amount they expect to receive in cash.

2) The average days to sell inventory represents the average number of days sales for

which a company has inventory on hand.

3) IFRS and U.S. GAAP have significant differences in the reporting of securities with

characteristics of debt and equity, such as convertible debt.

4) When a company exchanges nonmonetary assets and a loss results, the company

recognizes the loss only if the exchange has commercial substance.

5) The expected cash flow approach uses a range of cash flows and incorporates the

probabilities of those cash flows to provide a more relevant present value measurement.

6) The accounts receivable turnover ratio is computed by dividing net sales by the

ending net receivables.

7) Both IFRS and U.S. GAAP allow that if determining the effect of a change in

accounting principle is considered impracticable, then a company should report the

effect of the change in the period in which it believes it practicable to do so.

8) When a company changes an accounting principle, it should report the change by

reporting the cumulative effect of the change in the current years income statement.

9) A mortgage bond is referred to as a debenture bond.

10) For a loan receivable, impairment loss is calculated as the difference between the

investment in the loan and the expected future cash flows discounted at the loans

historical effective interest rate.

11) Companies determine cash provided by operating activities by converting net

income on an accrual basis to a cash basis.

12) Executory costs should be excluded by the lessee in computing the present value of

the minimum lease payments.

13) Amortization of limited-life intangible assets should not be affected by expected

residual values.

14) When it is impossible to determine whether a change in principle or change in

estimate has occurred, the change is considered a change in estimate.

15) Which of the following is not an intangible asset?

a.Trade name

b.Research and development costs

c.Franchise

d.Copyrights

16) A company has not declared a dividend on its cumulative preferred stock for the

past three years. What is the required accounting treatment or disclosure in this

situation?

a.Record a liability for cumulative amount of preferred stock dividends not declared

b.Disclose the amount of the dividends in arrears

c.Record a liability for the current year's dividends only

d.No disclosure or recognition is required

17) Which of the following statements is correct?

a.Changes in accounting principle are always handled in the current or prospective

period

b.Prior statements should be restated for changes in accounting estimates

c.A change from expensing certain costs to capitalizing these costs due to a change in

the period benefited, should be handled as a change in accounting estimate

d.Correction of an error related to a prior period should be considered as an adjustment

to current year net income

18) Assume that a manufacturing corporation has (1) good quality control, (2) a

one-year operating cycle, (3) a relatively stable pattern of annual sales, and (4) a

continuing policy of guaranteeing new products against defects for three years that has

resulted in material but rather stable warranty repair and replacement costs. Any

liability for the warranty

a.should be reported as long-term

b.should be reported as current

c.should be reported as part current and part long-term

d.need not be disclosed

19) Eddy Co. is indebted to Cole under a $800,000, 12%, three-year note dated

December 31, 2013 . Because of Eddy's financial difficulties developing in 2015, Eddy

owed accrued interest of $96,000 on the note at December 31, 2015 . Under a troubled

debt restructuring, on December 31, 2015, Cole agreed to settle the note and accrued

interest for a tract of land having a fair value of $720,000. Eddy's acquisition cost of the

land is $580,000. Ignoring income taxes, on its 2015 income statement Eddy should

report as a result of the troubled debt restructuring

Gain on DisposalRestructuring Gain

a.$316,000$0

b.$220,000$0

c.$140,000$80,000

d.$140,000$176,000

20) Klayton Corporation purchased factory equipment that was installed and put into

service January 2, 2014, at a total cost of $120,000. Salvage value was estimated at

$8,000. The equipment is being depreciated over four years using the double-declining

balance method. For the year 2015, Klayton should record depreciation expense on this

equipment of

a.$28,000

b.$30,000

c.$56,000

d.$60,000

21) Under IFRS, current assets are listed in:

a.the order of liquidity

b.the reverse order of liquidity

c.the ascending order of their balances

d.the descending order of their balances

22) On July 1, 2014, Nall Co. issued 2,500 shares of its $10 par common stock and

5,000 shares of its $10 par convertible preferred stock for a lump sum of $130,000. At

this date Nall's common stock was selling for $24 per share and the convertible

preferred stock for $18 per share. The amount of the proceeds allocated to Nall's

preferred stock should be

a.$65,000

b.$78,000

c.$90,000

d.$71,500

23) Lucas, Inc. enters into a lease agreement as lessor on January 1, 2015, to lease an

airplane to National Airlines. The term of the noncancelable lease is eight years and

payments are required at the end of each year. The following information relates to this

agreement:

1>National Airlines has the option to purchase the airplane for $12,000,000 when the

lease expires at which time the fair value is expected to be $20,000,000.

2>The airplane has a cost of $51,000,000 to Lucas, an estimated useful life of fourteen

years, and a salvage value of zero at the end of that time (due to technological

obsolescence).

3>National Airlines will pay all executory costs related to the leased airplane.

4>Annual beginning of year lease payments of $1,172,753 allow Lucas to earn an 8%

return on its investment.

5>Collectibility of the payments is reasonably predictable, and there are no important

uncertainties surrounding the costs yet to be incurred by Lucas.

Instructions

(a)What type of lease is this? Discuss.

(b)Prepare a lease amortization schedule for the lessor for the first two years

(2015-2016). (Round all amounts to nearest dollar.)

(c)Prepare the journal entries on the books of the lessor to record the lease agreement,

to reflect payments received under the lease, and to recognize revenue, for 2015 .

24) On January 1, 2015, Ritter Company granted stock options to officers and key

employees for the purchase of 15,000 shares of the company's $1 par common stock at

$20 per share as additional compensation for services to be rendered over the next three

years. The options are exercisable during a five-year period beginning January 1, 2018

by grantees still employed by Ritter. The Black-Scholes option pricing model

determines total compensation expense to be $135,000. The market price of common

stock was $26 per share at the date of grant. The journal entry to record the

compensation expense related to these options for 2015 would include a credit to the

Paid-in CapitalStock Options account for

a.$0

b.$27,000

c.$30,000

d.$45,000

25) On January 1, 2014, Huber Co. sold 12% bonds with a face value of $1,000,000.

The bonds mature in five years, and interest is paid semiannually on June 30 and

December 31 . The bonds were sold for $1,077,250 to yield 10%. Using the

effective-interest method of amortization, interest expense for 2014 is

a.$100,000

b.$107,419

c.$107,700

d.$120,000

26) Moon Inc assigns $3,000,000 of its accounts receivables as collateral for a $2

million loan with a bank. The bank assesses a 3% finance charge on the loan amount

and charges interest on the note at 6%. What would be the journal entry to record this

transaction?

a.Debit Cash for $1,940,000, debit Interest Expense for $60,000, and credit Notes

payable for $2,000,000

b.Debit Cash for $1,940,000, debit Interest Expense for $60,000, and credit Accounts

Receivable for $2,000,000

c.Debit Cash for $1,940,000, debit Interest Expense for $60,000, debit Due from Bank

for $1,000,000, and credit Accounts Receivable for $3,000,000

d.Debit Cash for $1,820,000, debit Interest Expense for $180,000, and credit Notes

Payable for $2,000,000

27) In matters of doubt and great uncertainty, accounting issues should be resolved by

choosing the alternative that has the least favorable effect on net income, assets, and

owners' equity. This guidance comes from

a.the cost constraint

b.the industry practices constraint

c.prudence or conservatism

d.the full disclosure principle

28) If a company purchases merchandise on terms of 1/10, n/30, the cash discount

available (assuming a 360-day year) is equivalent to an effective annual interest rate of

a.1%

b.12%

c.18%

d.30%

29) Dolan Co. received merchandise on consignment. As of March 31, Dolan had

recorded the transaction as a purchase and included the goods in inventory. The effect

of this on its financial statements for March 31 would be

a.no effect

b.net income was correct and current assets and current liabilities were overstated

c.net income, current assets, and current liabilities were overstated

d.net income and current liabilities were overstated

30) Provide clear, concise answers for the following.

1>What is the accrual-basis of accounting?

2>What is an accrued expense?

3>What is accrued revenue?

4>What is a prepaid expense?

5>What is unearned revenue?

6>State the rule that indicates which adjusting entries for prepaid and unearned items

should be reversed.

31) Moore Corporation follows a policy of a 10% depreciation charge per year on all

machinery and a 5% depreciation charge per year on buildings. The following

transactions occurred in 2015:

March 31, 2015Negotiations which began in 2014 were completed and a building

purchased 1/1/06 ( depreciation has been properly charged through December 31,

2014 ) at a cost of $6,400,000 with a fair value of $4,000,000 was exchanged for a

second building which also had a fair value of $4,000,000. The exchange had no

commercial substance. Both parcels of land on which the buildings were located were

equal in value, and had a fair value equal to book value.

June 30, 2015Machinery with a cost of $720,000 and accumulated depreciation through

January 1 of $540,000 was exchanged with $450,000 cash for a parcel of land with a

fair value of $690,000. The exchange had commercial substance.

Instructions

Prepare all appropriate journal entries for Moore Corporation for the above dates.

32) A central issue in reporting on operating segments of a business enterprise is the

determination of which segments are reportable.

Instructions

1>What are the tests to determine whether or not an operating segment is reportable?

2>What is the test to determine if enough operating segments have been separately

reported upon, and what is the guideline on the maximum number of operating

segments to be shown?

33) Carey Company owns a plot of land on which buried toxic wastes have been

discovered. Since it will require several years and a considerable sum of money before

the property is fully detoxified and capable of generating revenues, Carey wishes to sell

the land now. It has located two potential buyers: Buyer A, who is willing to pay

$575,000 for the land now, and Buyer B, who is willing to make 20 annual payments of

$90,000 each, with the first payment to be made 5 years from today. Assuming that the

appropriate rate of interest is 9%, to whom should Carey sell the land? Show

calculations.

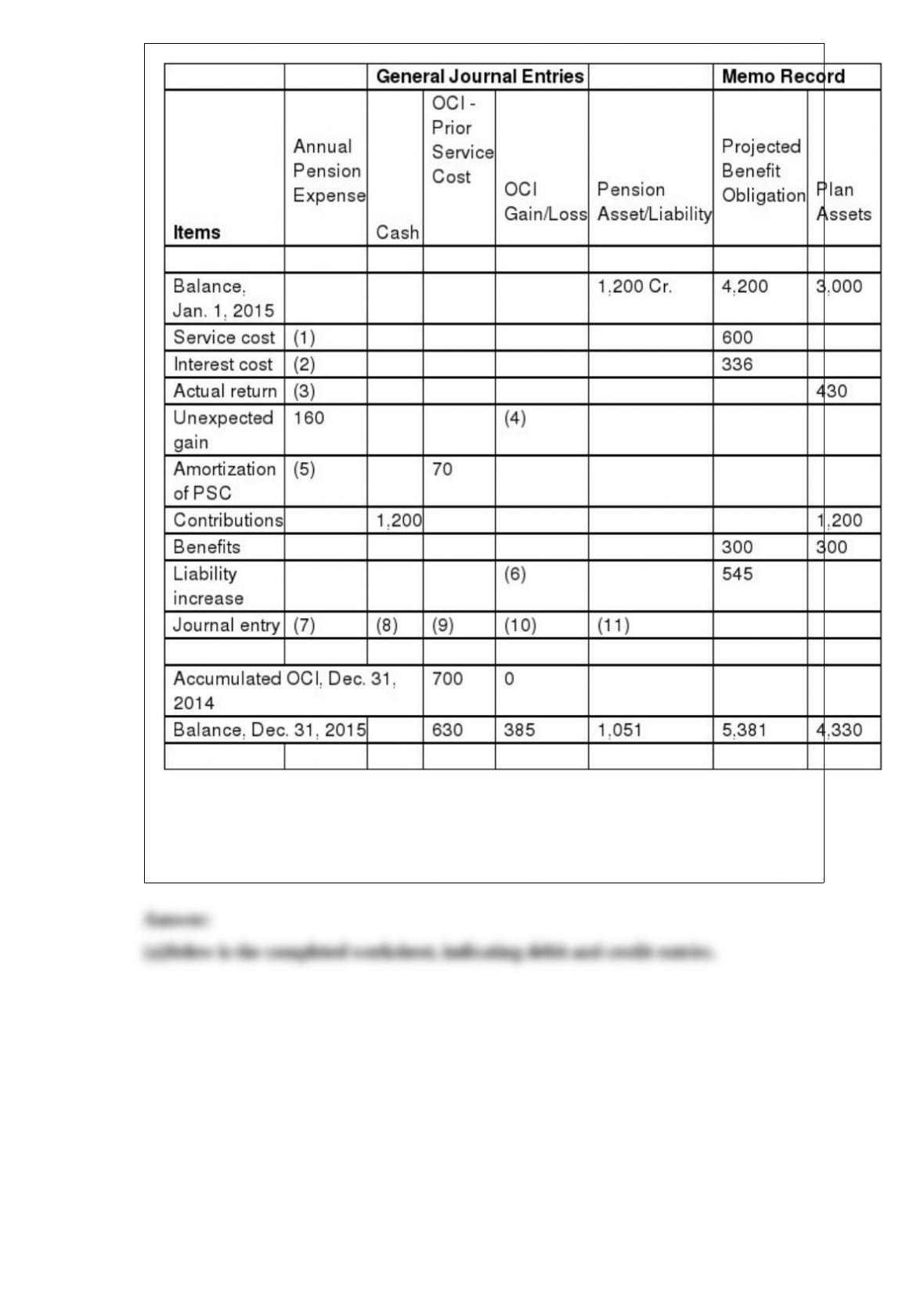

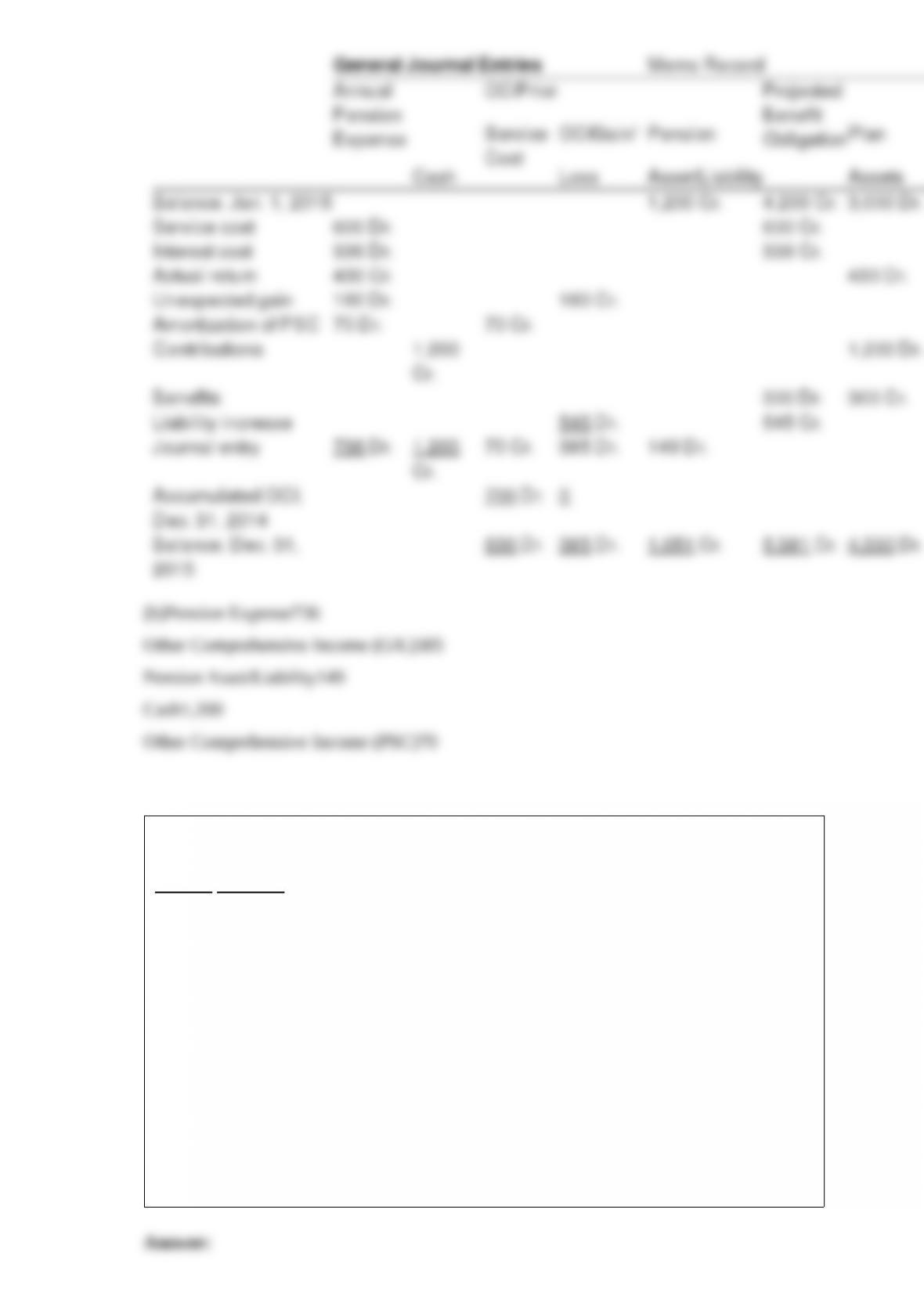

34) The accounting staff of Elias Inc. has prepared the following pension worksheet.

Unfortunately, several entries in the worksheet are not readable. The company has

asked your assistance in completing the worksheet and completing the accounting tasks

related to the pension plan for 2015 .

Instructions

Determine the missing amounts in the 2015 pension worksheet, indicating whether the

amounts are debits or credits.

Prepare the journal entry to record 2015 pension expense for Elias Inc.

35) When you undertook the preparation of the financial statements for Telfer Company

at January 31, 2015, the following data were available:

At Cost At Retail

Inventory, February 1, 2014$70,800$ 98,500

Markdowns35,000

Markups63,000

Markdown cancellations20,000

Markup cancellations10,000

Purchases219,500294,000

Sales revenue345,000

Purchases returns and allowances4,3005,500

Sales returns and allowances10,000

Instructions

Compute the ending inventory at cost as of January 31, 2015, using the retail method

which approximates lower of cost or market. Your solution should be in good form with

amounts clearly labeled.

36) The Financial Accounting Standards Board requires the reporting of disaggregated

financial data about the different types of business activities in which an enterprise

engages.

Instructions

Identify 4 of the 6 items of disaggregated information the FASB requires that an

enterprise report.

37) Determine the market price of a $500,000, ten-year, 10% (pays interest

semiannually) bond issue sold to yield an effective rate of 12%.

38) Colson Corp. had $700,000 net income in 2015 . On January 1, 2015 there were

200,000 shares of common stock outstanding. On April 1, 20,000 shares were issued

and on September 1, Colson bought 30,000 shares of treasury stock. There are 30,000

options to buy common stock at $40 a share outstanding. The market price of the

common stock averaged $50 during 2015 . The tax rate is 40%.

During 2015, there were 40,000 shares of convertible preferred stock outstanding. The

preferred is $100 par, pays $3.50 a year dividend, and is convertible into three shares of

common stock.

Colson issued $2,000,000 of 8% convertible bonds at face value during 2014 . Each

$1,000 bond is convertible into 30 shares of common stock.

Instructions

Compute diluted earnings per share for 2015 . Complete the schedule and show all

computations.

NetAdjust-AdjustedAdjust-Adjusted

SecurityIncomementNet IncomeSharesmentSharesEPS