1) Information and idea exchange sessions by the audit team are required by SAS No.

99.

A) True

B) False

2) To test for proper sales cutoff, an auditor would obtain the number of the last bill of

lading issued during the period under audit and verify that the item shipped had been

excluded from the inventory listing.

A) True

B) False

3) Why does the auditor divide the financial statements into smaller segments?

A) Using the cycle approach makes the audit more manageable

B) Most accounts have few relationships with others and so it is more efficient to break

the financial statements into smaller pieces

C) The cycle approach is used because auditing standards require it

D) All of the above are correct

4) The process of “final evidence accumulation” is always done late in the engagement.

Which one of the following would be done the earliest in the engagement?

A) final analytical procedures

B) search for contingent liabilities

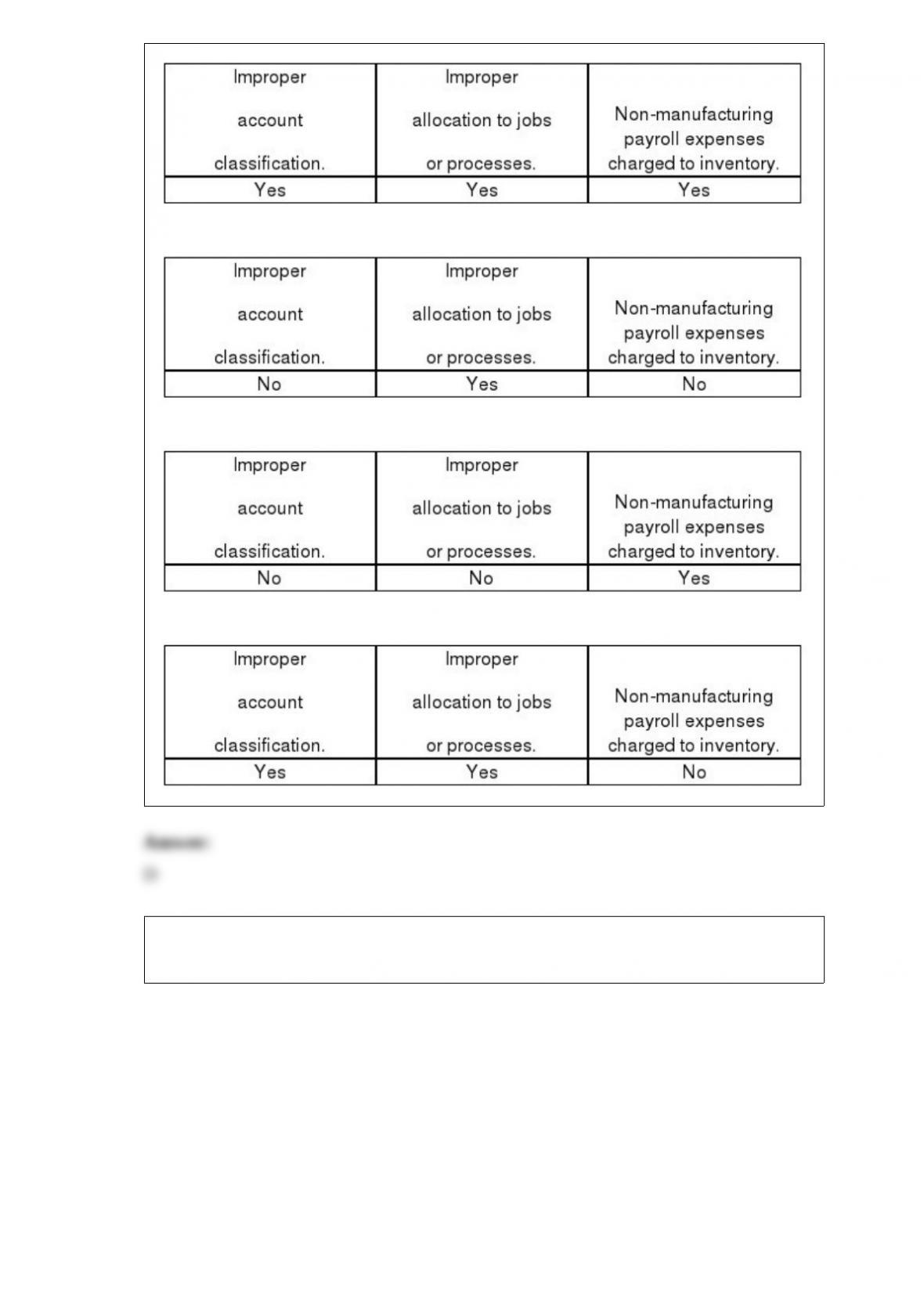

C) evaluate the going concern assumption

D) acquire the client’s letter of representation

5) Professional standards prohibit which one of the following types of engagements for

prospective financial statements from being undertaken?

A) a compilation

B) a review

C) an examination

D) an agreed-upon procedures engagement

6) Auditors typically rely on internal controls of their private company clients:

A) only as needed to complete the audit and satisfy Sarbanes-Oxley requirements

B) only if the controls are determined to be effective

C) only if the client asks an auditor to test controls

D) only if the controls are sufficient to increase Control Risk to an acceptable level

7) Improperly classifying a fixed asset by recording the amount in the repairs and

maintenance expense account will have an effect on which of the following financial

statements until the asset would normally have been depreciated?

A) The balance sheet

B) The income statement

C) The cash flow statement

D) Both the income statement and the balance sheet

8) Information obtained by a CPA from a client is legally privileged in federal court.

A) True

B) False

9) Perpetual inventory records should be maintained by persons having access to

inventory.

A) True

B) False

10) Acceptable risk of incorrect acceptance (ARIA) and sample size are inversely

related; that is, as ARIA increases, sample size decreases.

A) True

B) False

11) The word below that best explains the relationship between required sample size

and the acceptable risk of incorrect acceptance is:

A) inverse

B) direct

C) proportional

D) indeterminate

12) The audit committee is responsible for determining an organization’s financial

reporting and internal control processes.

A) True

B) False

13) Confirmations are ordinarily used to verify account balances, but may be used to

verify transactions.

A) True

B) False

14) Under the

A) True

B) False

15) In “auditing” financial accounting data, the primary concern is with:

A) determining whether recorded information properly reflects the economic events

that occurred during the accounting period

B) determining if fraud has occurred

C) determining if taxable income has been calculated correctly

D) analyzing the financial information to be sure that it complies with government

requirements

16) Acceptable risk of incorrect rejection is the statistical risk that the auditor has

concluded that a population is materially misstated when it is not.

A) True

B) False

17) Sampling used for tests of details of balances provides results in terms of:

A) exception rates

B) percentages

C) dollars

D) expectation rates

18) When the client’s physical inventory occurs before the last day of the year, it is still

necessary to perform an accounts payable cutoff at the time of the count. In addition,

the auditor must verify whether all acquisitions taking place between the count and the

end of the year were added to:

A) the physical inventory

B) Accounts Payable

C) Accounts Payable and Cost of Goods Sold

D) the physical inventory and Accounts Payable

19) What potential problems may arise when an auditor considers the relationship

between payroll and inventory valuation?

A)

B)

C)

D)

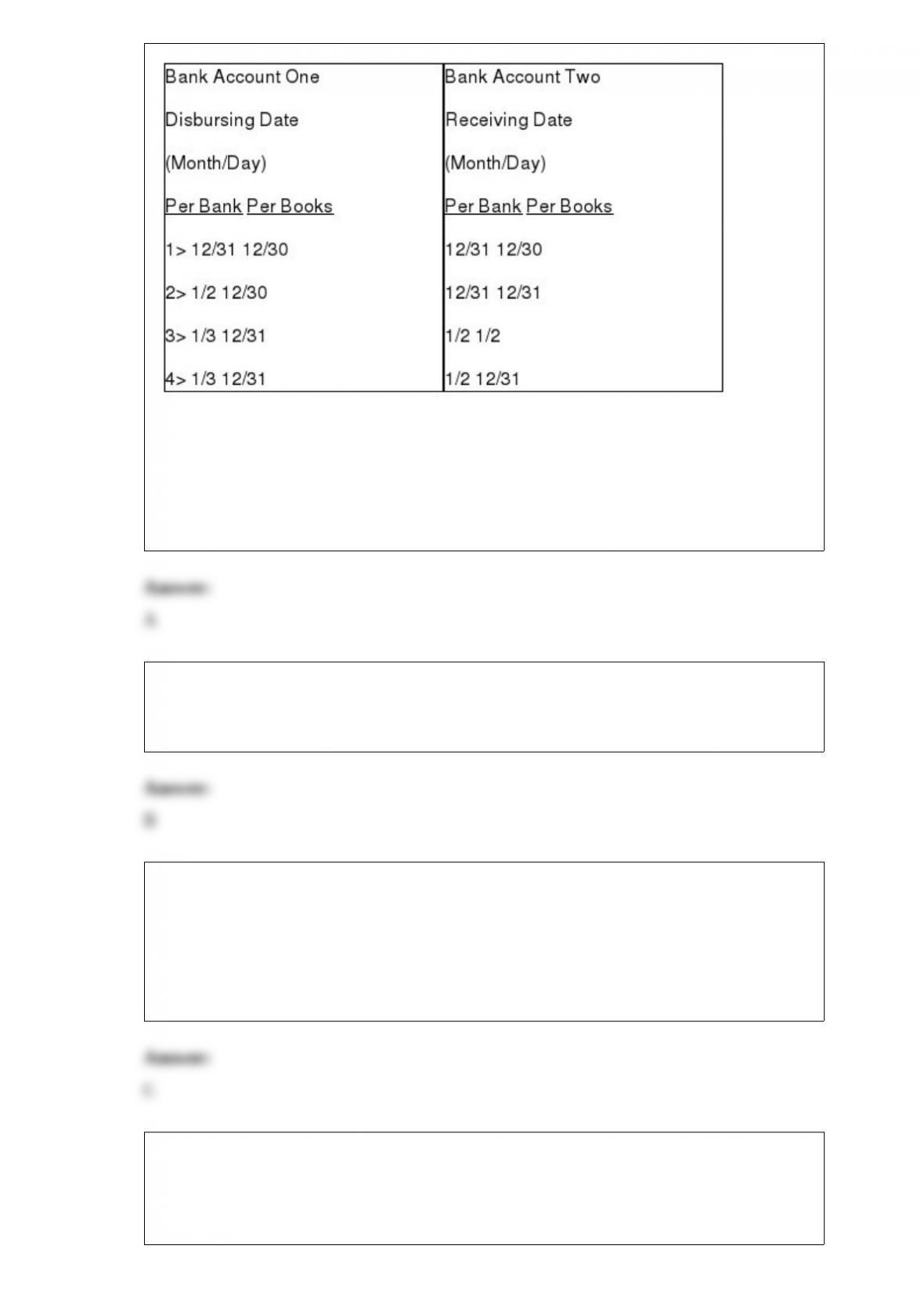

20) Listed below are four interbank cash transfers, indicated by the numbers 1, 2, 3, and

4, of a client for late December 2007 and early January 2008:

Based on the schedule of interbank transfers above, which of the cash transfers would

not appear as an outstanding check on the December 31, 2007 bank reconciliation?

A) 1

B) 2

C) 3

D) 4

21) The preparation of a sales invoice is the final step in the sales and collection cycle.

A) True

B) False

22) The auditor normally does not need to test the accuracy or classification of fixed

assets recorded in prior periods if they are the continuing auditor because:

A) they are rarely material to the audit

B) they rarely contain misstatements

C) they are verified in previous audits

D) they don’t affect the balance sheet

23) Subsequent events for which disclosure, but no adjustment, is required provide

information about significant events/conditions which existed at the balance sheet date.

A) True

B) False

24) Auditors must communicate in writing about internal control weaknesses to the

audit committee or those charged with governance.

A) True

B) False

25) Ordinarily, the auditor should review corporate minutes during the later stages of an

audit.

A) True

B) False

26) The

A) attestation engagements

B) services performed by accountants in public practice

C) accounting and auditing services performed

D) professional work performed by CPAs

27) The prelisting of cash receipts should be prepared by the individual who has

primary responsibility for the recording of cash receipts.

A) True

B) False

28) In planning the audit, an auditor takes 3 basic steps in determining the audit

procedures to be performed for any business cycle or class of transactions in order to

gather audit evidence concerning possible misstatement due to error or fraud. List those

three basic steps below.

29) What types of exceptions are auditors most concerned with when evaluating

populations of accounting data?

30) Processing controls include the following tests:

Validation

Sequence

Data Reasonableness

Completeness

Describe what each control is designed to do:

31) Explain why monetary-unit sampling, or probability proportional to size sampling,

is not useful for detecting understatements.

32) Discuss each of the six possible courses of action the auditor can take when he or

she has concluded that the population is misstated by more than a tolerable amount.

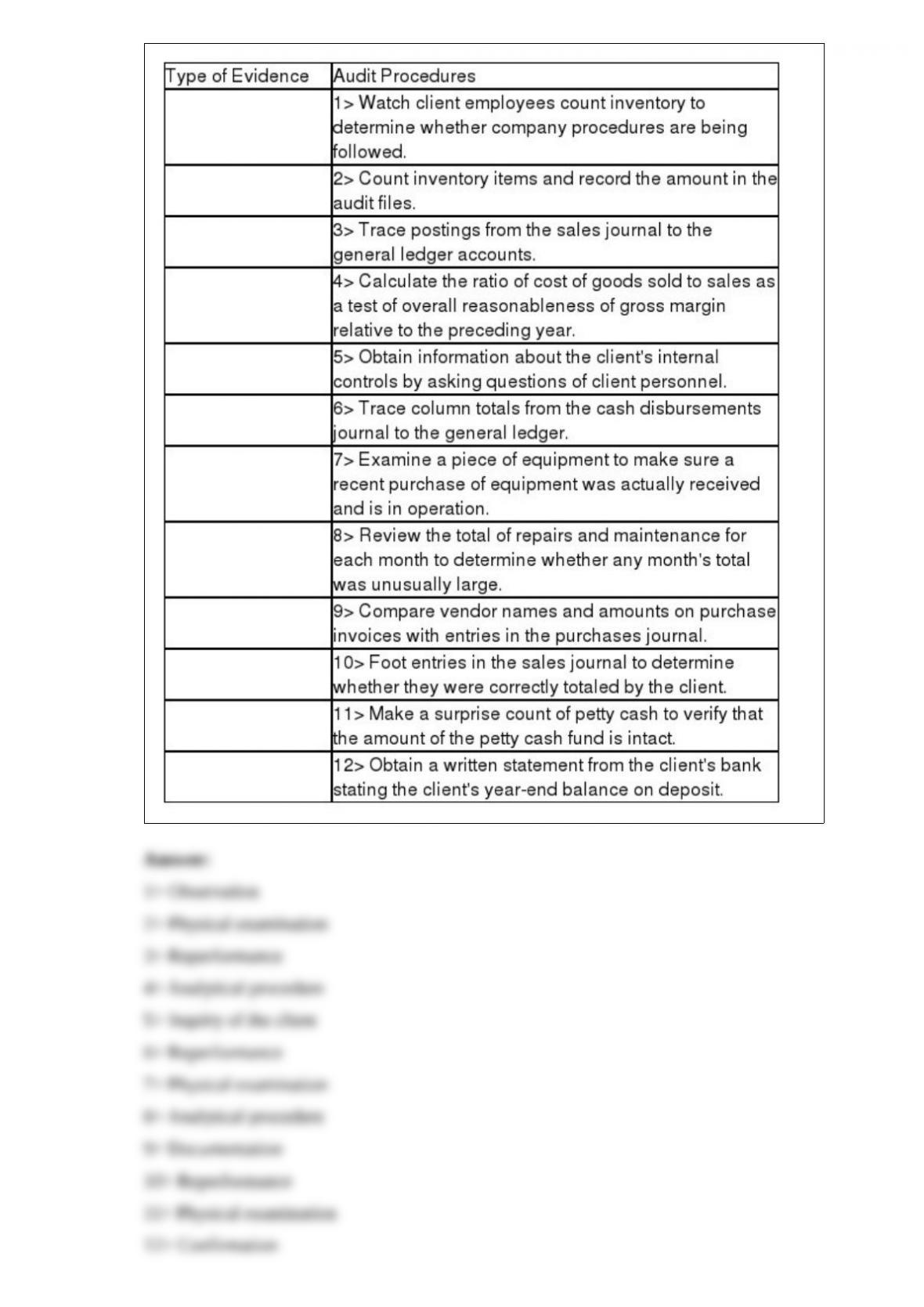

33) Below are 12 audit procedures. Classify each procedure according to the following

types of audit evidence: (1) physical examination, (2) confirmation, (3) documentation,

(4) observation, (5) inquiry of the client, (6) reperformance, and (7) analytical

procedure.

34) What are the five categories of attestation services?

35) Explain the decision rule used in monetary-unit sampling to determine whether the

population value (account balance) is acceptable.