1) GAAP requires that segment information be reported

A) by geographics, without regard to size of the segment

B) by geographics, without regard to industry or product-line

C) however management organizes the enterprise into units for internal

decision-making and performance-evaluation purposes

D) by industry or product-line, without regard to geographics

2) The risk premium on corporate bonds reflects the fact that corporate bonds have a

higher default risk and are ________ US Treasury bonds

A) less liquid than

B) less speculative than

C) tax-exempt unlike

D) lower-yielding than

3) If you have a very low tolerance for risk, which of the following bonds would you be

least likely to hold in your portfolio?

A) a US Treasury bond

B) a municipal bond

C) a corporate bond with a rating of Aaa

D) a corporate bond with a rating of Baa

4) A subsidiary can be excluded from consolidation if

A) control does not rest with the majority owner

B) the subsidiary is in legal reorganization

C) the subsidiary is operating under severe foreign-exchange restrictions

D) All of the above are correct

5) Everything else held constant, if income tax rates were lowered, then

A) the interest rate on municipal bonds would fall

B) the interest rate on Treasury bonds would rise

C) the interest rate on municipal bonds would rise

D) the price of Treasury bonds would fall

6) On January 1, 2011, Pamplin Corporation stockholders’ equity consisted of

$1,000,000 of $10 par value Common Stock, $750,000 of Additional Paid-in Capital,

and $3,000,000 of Retained Earnings. On January 1, 2011, Pamplin purchased 90% of

the outstanding common stock of Sage Corporation for $1,500,000 with all excess

purchase cost assigned to goodwill. The stockholders’ equity of Sage on this date

consisted of $800,000 of $100 par value, 8% cumulative, preferred stock callable at

$105, $900,000 of $10 par value common stock and $500,000 of Retained Earnings.

Sage’s net income for 2011 was $100,000.

On January 1, 2011, no preferred dividends are in arrears. No dividends are declared or

paid in 2011 . In a separate transaction on January 1, 2011, Pamplin purchased 70% of

Sage’s preferred stock for $600,000.

What is the goodwill on the consolidated balance sheet for Pamplin and Subsidiaries on

December 31, 2011 based on Pamplin’s purchase of Sage’s common stock?

A) $140,000

B) $240,000

C) $290,000

D) $306,667

7) Paint Corporation owns 82% of Achille Corporation and Achille Corporation owns

80% of Badrack Corporation. For the current year, the separate net incomes (excluding

investment income) of Paint, Achille, and Badrack are $120,000, $100,000, and

$50,000, respectively. The cost of each investment was equal to the book value of the

investment, which was also equal to the fair value.

Controlling interest share of consolidated net income for Paint Corporation and

Subsidiaries is:

A) $234,800

B) $244,800

C) $260,000

D) $270,000

8) Under parent company theory, noncontrolling interest is valued at ________ on the

consolidated balance sheet. Under entity theory, noncontrolling interest is valued at

________ on the consolidated balance sheet.

A) fair value; present value

B) present value; fair value

C) book value; fair value

D) fair value; book value

9) What is an advantage of filing a Chapter 11 petition?

A) The continuation of interest accrual on liabilities

B) Restrictions imposed by the bankruptcy court on day-to-day transactions

C) It is less costly than filing Chapter 7

D) The opportunity to cancel unfavorable contracts

10) According to the expectations theory of the term structure, the interest rate on a

long-term bond will equal the ________ of the short-term interest rates that people

expect to occur over the life of the long-term bond

A) average

B) sum

C) difference

D) multiple

11) The following are transactions for the city of Springfield.

a.Borrowed $20,000 by issuing a three-month, 5% note.

b.Paid $4,000 for equipment.

c.Services for $1,000 were billed and collected.

d.Year-end accrual of 3 months interest on note in (a).

Required:

Analyze the above transactions by using the accounting equation for a governmental

fund.

12) According to FASB Statement No. 141, liabilities assumed in an acquisition will be

valued at the ________.

A) estimated fair value

B) historical book value

C) current replacement cost

D) present value using market interest rates

13) Assume there are routine inventory sales between parent companies and

subsidiaries. When preparing the consolidated financial statements, which of the

following line items is indifferent to the sales being either upstream or downstream?

A) Consolidated retained earnings

B) Consolidated gross profit

C) Noncontrolling interest share

D) Controlling interest share of consolidated net income

14) In a business combination, which of the following will occur?

A) All identifiable assets and liabilities are recorded at fair value at the date of

acquisition

B) All identifiable assets and liabilities are recorded at book value at the date of

acquisition

C) Goodwill is recorded if the fair value of the net assets acquired exceeds the book

value of the net assets acquired

D) None of the above is correct

15) If 1-year interest rates for the next five years are expected to be 4, 2, 5, 4, and 5

percent, and the 5-year term premium is 1 percent, than the 5-year bond rate will be

A) 2 percent

B) 3 percent

C) 4 percent

D) 5 percent

16) Subsequent to an acquisition, the parent company and consolidated financial

statement amounts would not be the same for

A) investments in unconsolidated subsidiaries

B) investments in consolidated subsidiaries

C) capital stock

D) ending retained earnings

17) Park Incorporated purchased a 70% interest in Silk Company in 2008 at book value.

On January 1, 2010, equipment having a historical cost of $100,000 and a net book

value of $70,000 is sold in an intercompany transfer for $90,000. The equipment has a

remaining useful life of five years and no salvage value. Straight-line depreciation is

used by both companies. Silk reports net income of $180,000 in 2010 and $200,000 in

2011 .

Required:

1>Assume Park sold the equipment to Silk.

A. Prepare the consolidating worksheet entries for the equipment for 2010 and 2011 .

B. Calculate the noncontrolling interest share in Silk’s income for 2010 and 2011 .

2>Assume that Silk sold the equipment to Park.

A. Prepare the consolidating worksheet entries for the equipment for 2010 and 2011 .

B. Calculate the noncontrolling interest share in Silk’s income for 2010 and 2011 .

18) On November 1, 2010, Rolleks Corporation sold merchandise to Watchem

Corporation, a Swiss firm. Rolleks measured and recorded the account receivable from

the sale at $107,100. Watchem paid for this account on November 30, 2010 . Spot rates

for Swiss francs on November 1 and November 30, respectively, were $1.05 and $1.02.

If the sale of the merchandise was denominated in Swiss francs, the November 30 entry

to record the receipt of payment from Watchem included a

A) credit to Accounts Receivable for $104,040

B) credit to Exchange Gain for $3,060

C) debit to Cash for $107,100

D) debit to Exchange Loss for $3,060

19) Pearl Corporation paid $150,000 on January 1, 2010 for a 25% interest in Sandlin

Inc. On January 1, 2010, the book value of Sandlin’s stockholders’ equity consisted of

$200,000 of common stock and $200,000 of retained earnings. All the excess purchase

cost over book value acquired was attributable to a patent with an estimated life of 5

years. During 2010 and 2011, Sandlin paid $3,000 of dividends each quarter and

reported net income of $60,000 for 2010 and $80,000 for 2011 . Pearl used the equity

method.

Required:

1>Calculate Pearl’s income from Sandlin for 2010 .

2>Calculate Pearl’s income from Sandlin for 2011 .

3>Determine the balance of Pearl’s Investment in Sandlin account on December 31,

2011 .

20) For each of the following events or transactions, identify the type of fund(s) that

will be affected.

1>A central purchasing department was established to handle all the purchasing needs

of a county government.

2>A county government levies sales taxes restricted as to use for job creation.

3>A county government receives a large contribution specifying that income from the

contribution be distributed each year to the county zoo. The principal is to remain intact

indefinitely.

4>A city government paid construction costs of $12,000 on city hall building.

5>A city government paid general operating costs.

21) The following information is available about the operations for a private,

not-for-profit university.

1>The university sold $20,000,000 of 5% bonds to finance the construction of a new

building for the business school. The bonds were sold on January 1 and pay interest on

December 31 of each year. The bonds were sold at par and mature in 20 years.

2>The university received $7,500,000 cash in alumni and corporate donations for the

new business school building.

3>The building was constructed at a total cost of $22,000,000 and the contractor was

paid in full.

4>Interest was paid on the bonds.

5>Depreciation on the new building the first year was $275,000.

Required:

Prepare the appropriate journal entries for the university for these transactions.

22) The unadjusted trial balance for the general fund of the City of Jordan at June 30,

2011 is as follows:

Debits

Accounts receivable$90,000

Cash110,000

Due from agency fund19,000

Encumbrances18,000

Estimated revenues1,250,000

Expenditures1,090,000

Taxes receivable175,000

Credits

Allowance for doubtful accounts15,000

Allowance for uncollectible taxes35,000

Appropriations1,180,000

Due to internal service fund51,000

Fund balance – unassigned52,000

Reserve for encumbrances18,000

Revenues1,130,000

Taxes received in advance22,000

Vouchers payable249,000

Supplies on hand at June 30, 2011 totaled $17,000. The $18,000 encumbrance relates to

equipment ordered but not received by fiscal year-end.

Required:

Prepare a balance sheet for the general fund of the City of Jordan at June 30, 2011 .

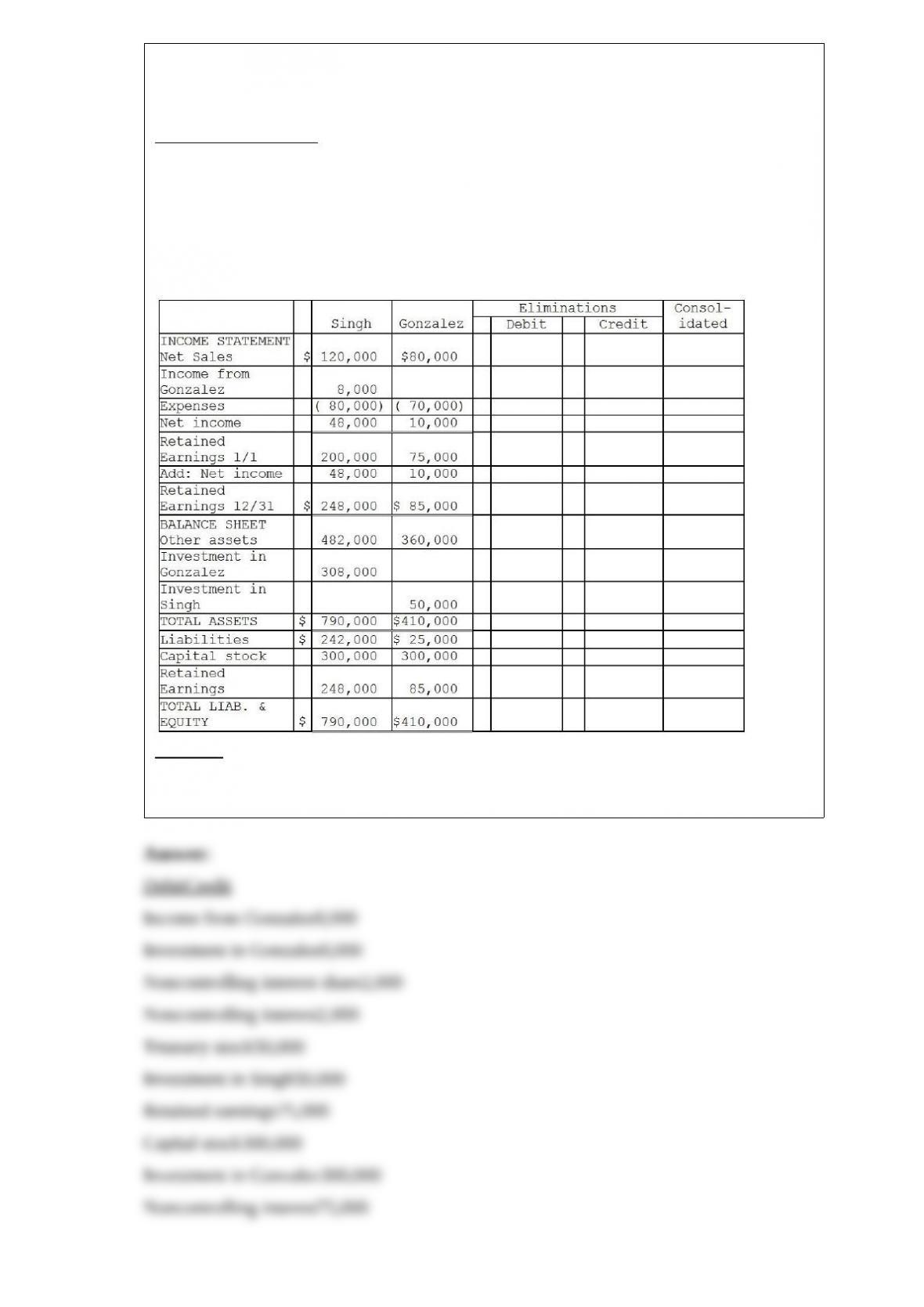

23) On January 1, 2011, Singh Company acquired an 80 percent interest in Gonzalez

Company for $300,000. On January 1, 2011, Gonzalez’s total stockholders’ equity was

$375,000. The fair value and book value of Gonzalez’s individual assets and liabilities

were equal.

On January 2, 2011, Gonzalez Company acquired a 10 percent interest in Singh

Company for $50,000. On January 2, 2011, Singh’s total stockholders’ equity was

$500,000. The fair value and book value of Singh’s individual assets and liabilities were

equal.

For the year ending December 31, 2011, the following data is available:

Net incomeDividends

Singh Company$40,000$0

Gonzalez Company$10,000$0

The treasury stock method is used to account for the mutual stock holdings between

Singh and Gonzalez. The separate net incomes do not include investment income. A

partial consolidating worksheet is below.

Required:

Prepare the elimination entries for the year ending December 31, 2011 .

Do not enter them onto the worksheet. Instead, list them below.

24) The accountant for Baxter Corporation has assigned most of the company’s assets to

its three segments as follows:

Electronics$1,760,000

Hardware3,420,000

Plumbing490,000

Total$5,670,000

The unassigned assets consist of $430,000 of unallocated goodwill and $270,000 of

assets attached to the corporate headquarters. For internal decision-making purposes,

goodwill is not assigned to the segments and the assets assigned to the corporate

headquarters are allocated equally to the operating segments.

Required:

1> What is the proper threshold value to use in determining which of the operating

segments shown above are reporting segments?

2> Which of the operating segments are considered reporting segments?

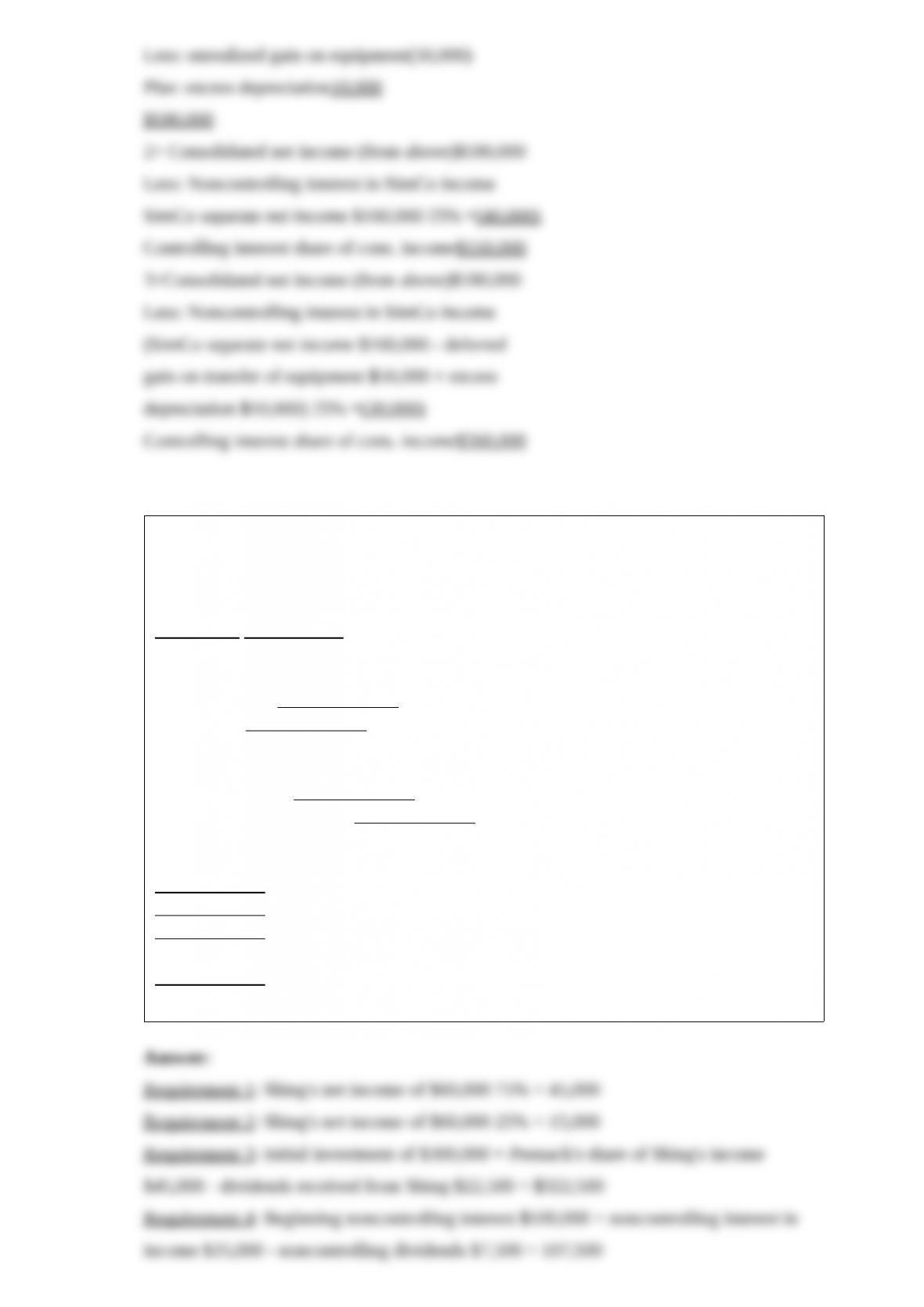

25) On January 2, 2012, Pal Corporation sold warehouse equipment to SimCo, a

wholly-owned subsidiary. The equipment had an original cost of $130,000 and a net

book value of $100,000 when it was sold to SimCo for $150,000. Both companies

agreed that the equipment had a five-year remaining life and compute depreciation on

the straight-line method. The equipment has no salvage value.

Pal reported $470,000 in net income in 2012 (prior to reporting any income from

SimCo), and SimCo reported $160,000 in net income.

Required:

1>Calculate consolidated net income for 2012 .

2>Determine the controlling share of net income for the year if Pal only owned 75% of

SimCo.

3>Determine the controlling share of net income for the year if Pal only owned 75% of

SimCo AND the equipment transfer was upstream.

26) Pennack Corporation purchased 75% of the outstanding stock of Shing Corporation

on January 1, 2011 for $300,000 cash. At the time of the purchase, the book value and

fair value of Shing’s assets and liabilities were equal. Shing’s balance sheet at the time

of acquisition and December 31, 2011 are shown below.

Jan 1, 2011 Dec 31, 2011

Cash$75,000 80,000

Other current assets 175,000160,000

Plant Assets net 250,000240,000

Total assets 500,000480,000

Liabilities 100,000 50,000

Capital stock 100,000100,000

Retained earnings 300,000330,000

Total liabilities and equity 500,000480,000

Shing earned $60,000 in income during the year, and paid out $30,000 in dividends.

Pennack uses the equity method to account for its investment in Shing.

Requirement 1: Calculate Pennack’s net income from Shing in 2011 .

Requirement 2: Calculate the noncontrolling interest share in Shing’s income for 2011 .

Requirement 3: Calculate the balance in the Investment in Shing account reported on

Pennack’s separate general ledger at December 31, 2011 .

Requirement 4: Calculate the noncontrolling interest that will be reported on the

consolidated balance sheet at December 31, 2011 .