In using a spreadsheet to prepare the statement of cash flows, the summary entries

duplicate the actual journal entries used to record the transactions during the year.

Subsequent events are significant developments that take place after a firm’s year-end,

and after the financial statements are issued or available to be issued.

An annuity is a series of equal periodic payments.

By the replacement depreciation method, depreciation is recorded when assets are

replaced.

Accounting for quality-assurance warranties includes a credit to warranty expense and a

debit to contingent liability.

In the future value of an ordinary annuity, the last cash payment will not earn any

interest.

Recognizing sales returns when merchandise is returned could result in an

overstatement of income in the period of the related sale.

When revenue is recognized over time versus upon completion of the contract, different

amounts of total profit or loss are recognized for a particular contract.

Which of the following is not an adjusting entry?

a. Prepaid rentRent expense

b. CashDeferred revenue

c. Interest expenseInterest payable

d. Salaries expenseSalaries payable

What is the effective annual rate of interest on the bonds?

a. 3%.

b. 4%.

c. 6%.

d. 8%.

Which of the following is not true about contract liabilities?

a. Contract liabilities are only recognized when the seller has a conditional right to

receive payment.

b. Contract liabilities might be called deferred revenue.

c. Contract liabilities are recognized when the seller has been paid in advance of

satisfying its performance obligations.

d. Contract liabilities may be shown on a separate line of the balance sheet.

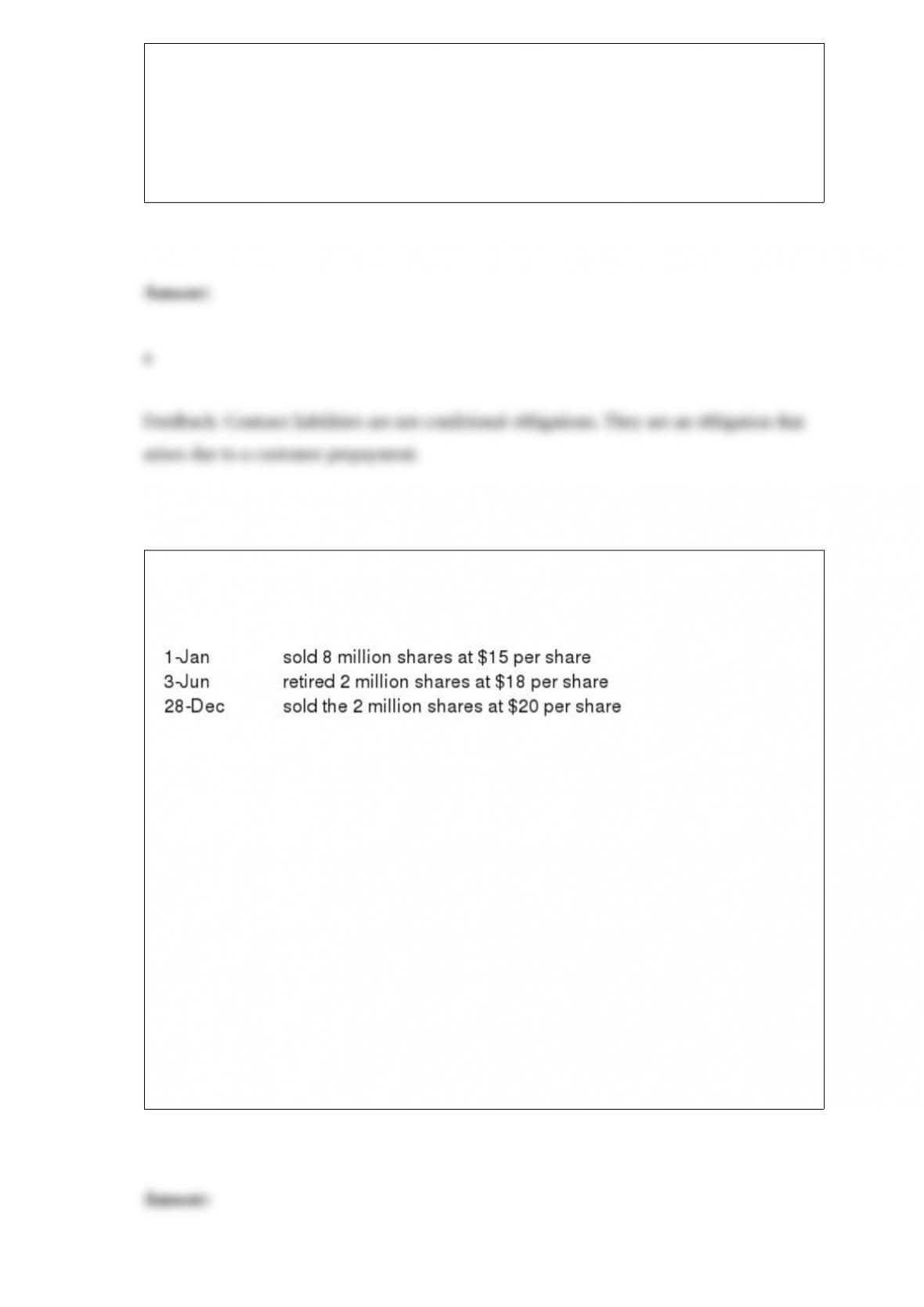

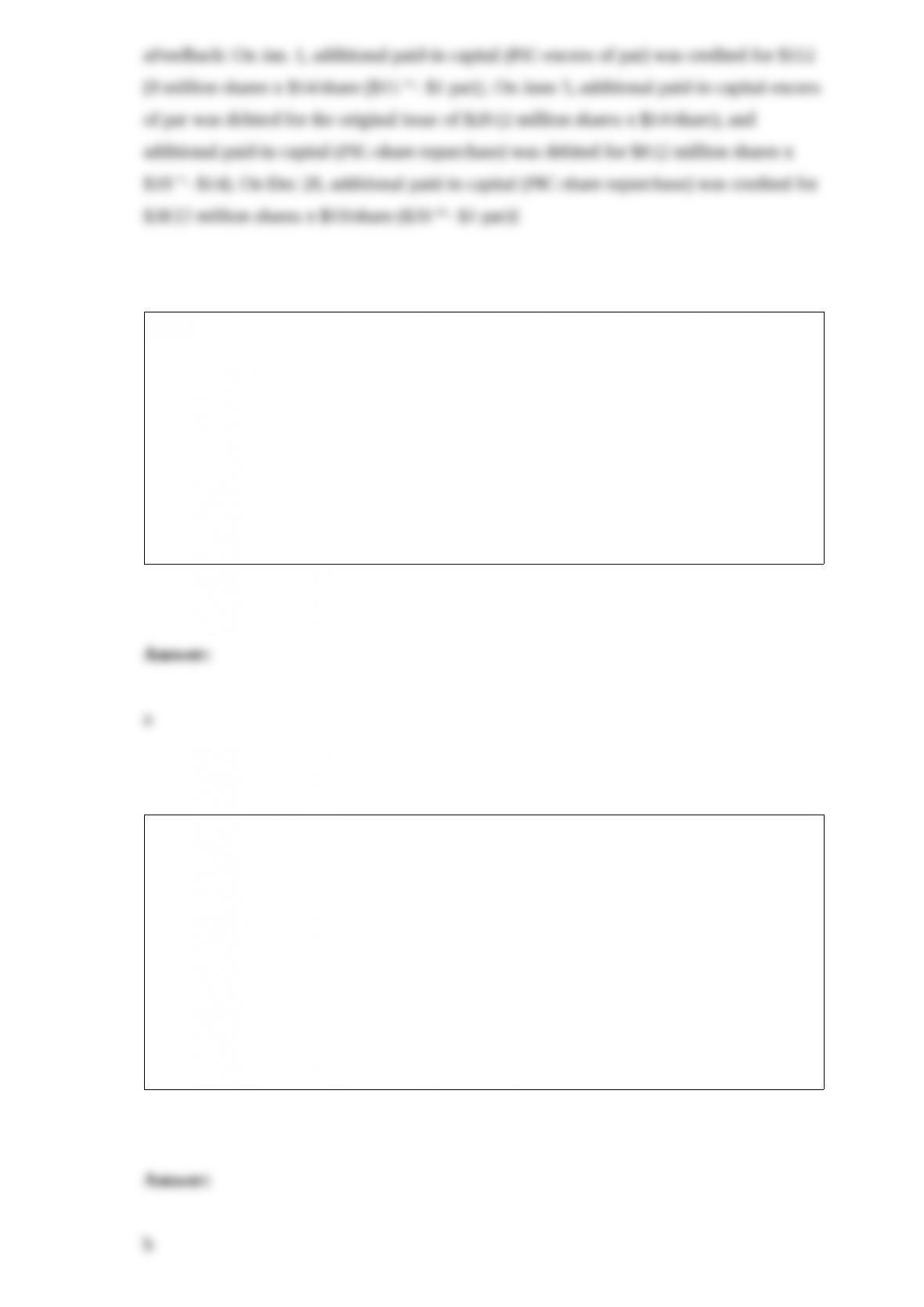

The corporate charter of Alpaca Co. authorized the issuance of 10 million, $1 par

common shares. During 2016, its first year of operations, Alpaca had the following

transactions:

January 1 sold 8 million shares at $15 per share

June 3 retired 2 million shares at $18 per share

December 28 sold the 2 million shares at $20 per share

What amount should Alpaca report as additional paid-in capital ‘’- excess of par, in its

December 31, 2016, balance sheet?

a. $122 million

b. $116 million

c. $112 million

d. $ 74 million

Estimated employee compensation expenses earned during the current period but

expected to be paid in the next period causes:

a. An increase in a deferred tax asset.

b. A decrease in a deferred tax asset.

c. An increase in a deferred tax liability.

d. A decrease in a deferred tax liability.

Johnson sells $100,000 of product to Robbins, and also purchases $10,000 of

advertising services from Robbins. The advertising services have a fair value of $8,000.

Johnson should record revenue on its sale of product to Robbins of:

a. $100,000

b. $98,000

c. $92,000

d. $90,000

General Product Inc. distributed 100 million coupons in 2016. The coupons are

redeemable for 30 cents each. General anticipates that 70% of the coupons will be

redeemed. The coupons expire on December 31, 2017. There were 45 million coupons

redeemed in 2016 and 30 million redeemed in 2017. What was General’s coupon

liability as of December 31, 2016?

a. $7.5 million.

b. $13.5 million.

c. $16.5 million.

d. $21.0 million.

Which of the following circumstances creates a future deductible amount?

a. Earning of non-taxable interest on municipal bonds.

b. Sales of property (installment method for tax purposes).

c. Prepaid advertising expense.

d. Accrued warranty expenses.

In 2016, Bodily Corporation reported $300,000 pretax accounting income. The income

tax rate for that year was 30%. Bodily had an unused $120,000 net operating loss

carryforward from 2014 when the tax rate was 40%. Bodily’s income tax payable for

2016 would be

a. $54,000

b. $42,000

c. $90,000

d. $72,000

Gupta Industries received a $300,000 prepayment from Packard Associates for the sale

of new equipment. Gupta will bill Packard an additional $100,000 upon delivery of the

equipment. Upon receipt of the $300,000 prepayment, how much should Holt recognize

for a contract asset, a contract liability, and accounts receivable? a. Contract asset: $0;

contract liability: $300,000, accounts receivable, $0.

b. Contract asset: $300,000; contract liability: $0, accounts receivable, $0.

c. Contract asset: $0; contract liability: $300,000, accounts receivable, $100,000.

d. Contract asset: $300,000; contract liability: $0, accounts receivable, $100,000.

Creble Company reported net income for 2016 in the amount of $40,000. The

company’s financial statements also included the following:

In the statement of cash flows what is net cash provided by operating activities under

the indirect method?

a. $36,000.

b. $41,000.

c. $40,000.

d. $38,000.

Cost of goods sold is given by:

a. Beginning inventory – net purchases + ending inventory.

b. Beginning inventory + accounts payable – net purchases.

c. Net purchases + ending inventory – beginning inventory.

d. Net Purchases + beginning inventory – ending inventory.

Under which of the following circumstances is it most appropriate to use the residual

method to estimate stand-alone selling prices?

a. The seller hasn’t previously sold the product and hasn’t determined a price for it.

b. The seller provides the product bundled with other goods and services.

c. The seller does not have competitors from which to observe market prices of similar

products.

d. The seller is unable to accurately estimate variable consideration associated with the

contract.

In 2016, Magic Table Inc. decides to add a 36-month warranty on its new product sales.

Warranty costs are tax deductible when claims are settled. In its financial statements for

2016, Magic Table Inc incurs:

a. An increase in a deferred tax asset.

b. A decrease in a deferred tax asset.

c. An increase in a deferred tax liability.

d. A decrease in a deferred tax liability.

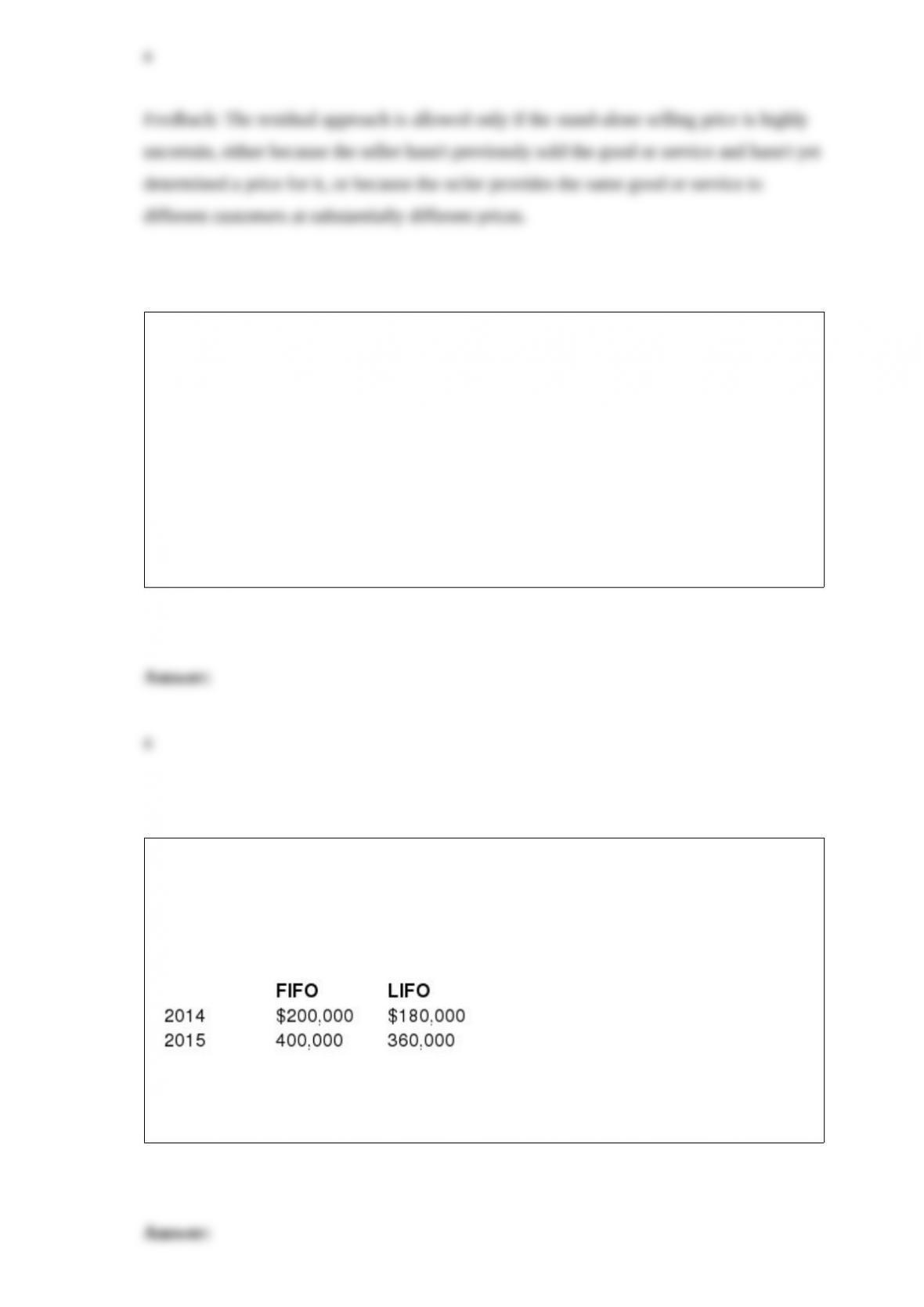

Macintosh Inc. changed from LIFO to the FIFO inventory costing method on January 1,

2016.

Inventory values at the end of each year since the inception of the company are as

follows:

Required:

Ignoring income tax considerations, prepare the entry to report this accounting change.

What disclosures are required relative to interest costs incurred during the year?

On December 31, 2015, Central Freight reported an allowance for uncollectible

accounts of $15,300. During 2016, Central wrote off $17,000 in accounts receivable.

Included in the write-off was Roskoff Corp.’s account in the amount of $750. Roskoff

subsequently paid this balance. At December 31, 2016, an analysis of the accounts

receivable aging schedule indicated the need for an allowance for uncollectible

accounts of $14,900.

Required:

Prepare all implied journal entries relative to bad debt expense and the allowance for

uncollectible accounts.

Costa Co. has the following cash balances at local banks as of 12/31/2016: National

Bank: $100,000

K&P Bank: 25,000

Insolvent Trust: ( 5,000) Required:

1> Prepare the Current Assets and Current Liabilities section of Costa’s 2016 balance

sheet, assuming Parker reports under U.S. GAAP.

2> Prepare the Current Assets and Current Liabilities section of Costa’s 2016 balance

sheet, assuming Parker reports under IFRS.

Many corporations own more than 50% of the voting stock in other corporations.

Sometimes these affiliated companies operate within the same industry, and many times

the companies are in unrelated industries.

Required:

What is the significance of owning more than 50% of the voting common stock of

another company?

Answer:

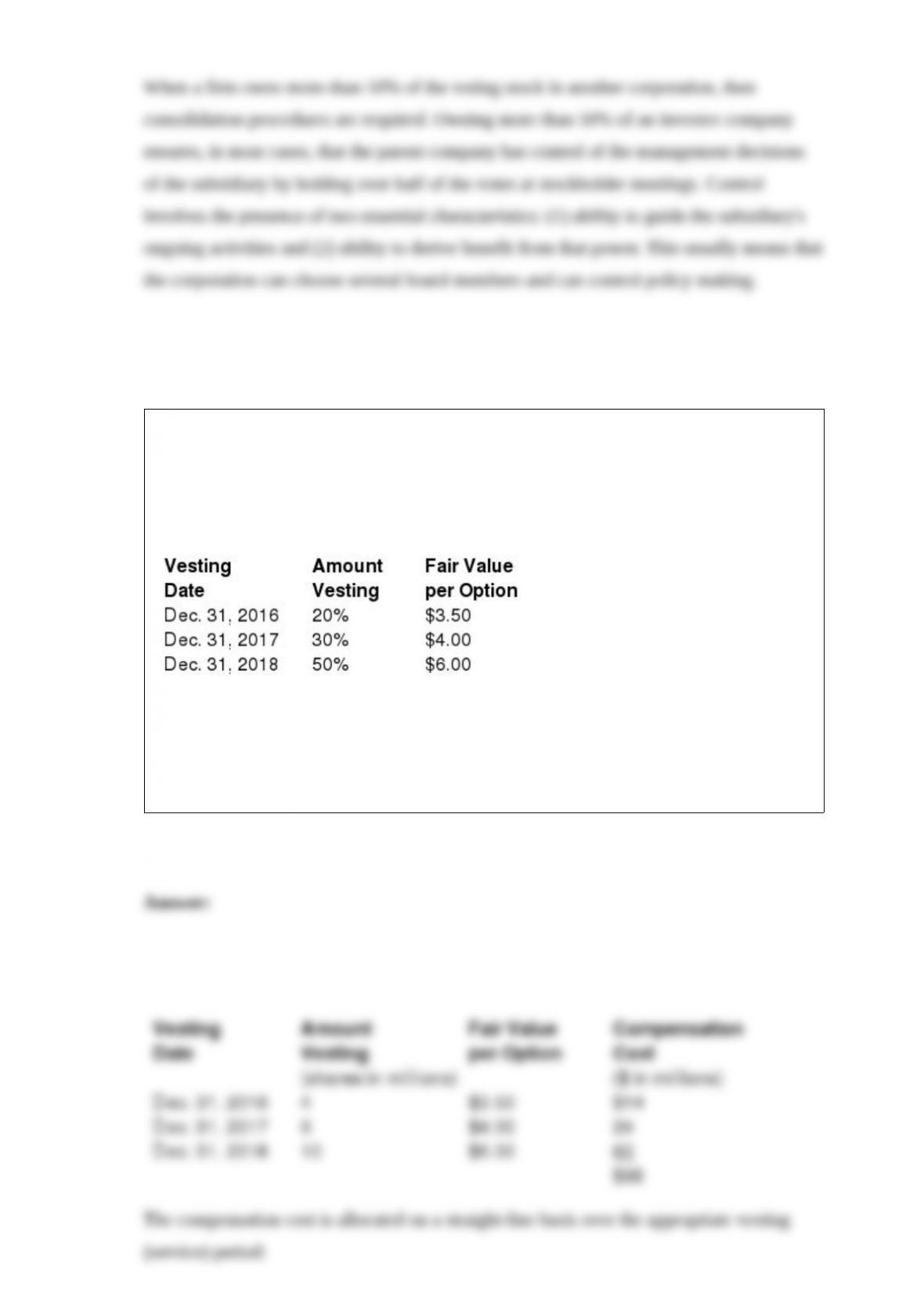

Pastner Brands is a calendar-year firm with operations in several countries. As part of

its executive compensation plan, at January 1, 2016, the company had issued 20 million

executive stock options permitting executives to buy 20 million shares of stock for $25.

The vesting schedule is 20% the first year, 30% the second year, and 50% the third year

(graded-vesting). The fair value of the options is estimated as follows:

Required:

Determine the compensation expense related to the options to be recorded each year for

2016-2018, assuming Pastner prepares its financial statements in accordance with

International Financial Reporting Standards (IFRS).