The purpose of assigning accounts receivable is to:

a. Satisfy a court order.

b. Complete the legal prerequisites to record their sale.

c. Comply with form and content rules of bankruptcy proceedings.

d. Provide collateral for a loan.

Recording revenue that is earned, but not yet collected, is an example of:

a. A prepaid expense transaction.

b. A deferred revenue transaction.

c. An accrued liability transaction.

d. An accrued receivable transaction.

XYZ paid $10,000 in dividends in January of the current year to its preferred

shareholders. The preferred stock is nonconvertible and noncumulative. The dividend:

a. Will be added to the denominator of the earnings per share fraction for the current

year.

b. Will be added to the numerator of the earnings per share fraction for the current year.

c. Will be subtracted from the numerator of the earnings per share fraction for the

current year.

d. May not affect earnings per share depending on the declaration date.

Which of the following is not true about EPS?

a. It must be reported by all corporations whose stock is publicly traded.

b. It must be reported separately for discontinued operations.

c. It must be reported on operating income.

d. None of the other answers is correct.

Sanjeev enters into a contract offering variable consideration. The contract pays him

$1,000/month for six months of continuous consulting services. In addition, there is a

60% chance the contract will pay an additional $2,000 and a 40% chance the contract

will pay an additional $3,000, depending on the outcome of the consulting contract.

Sanjeev concludes that this contract qualifies for revenue recognition over time.

Assume Sanjeev estimates variable consideration as the most likely amount. What is the

amount of revenue Sanjeev would recognize for the first month of the contract?

a. $1,000

b. $1,333

c. $1,400

d. $1,200

The method used to pay interest depends on whether the bonds are:

a. Registered or coupon.

b. Mortgaged or unmortgaged.

c. Indentured or debentured.

d. Callable or redeemable.

Tri Fecta, a partnership, had revenues of $360,000 in its first year of operations. The

partnership has not collected on $35,000 of its sales and still owes $40,000 on $150,000

of merchandise it purchased. There was no inventory on hand at the end of the year. The

partnership paid $25,000 in salaries. The partners invested $40,000 in the business and

$25,000 was borrowed on a five-year note. The partnership paid $3,000 in interest that

was the amount owed for the year and paid $8,000 for a two-year insurance policy on

the first day of business.

Compute the cash balance at the end of the first year for Tri Fecta.

Reliable Enterprises sells distressed merchandise on extended credit terms. Collections

on these sales are not reasonably assured, and bad debt losses cannot be reasonably

predicted. It is unlikely that repossessed merchandise is in condition to be re-sold.

Therefore, Reliable uses the cost recovery method. Merchandise costing $30,000 was

sold for $55,000 in 2015. Collections on this sale were $20,000 in 2015, $15,000 in

2016, and $20,000 in 2017.

In its 2016 year-end balance sheet, Reliable would report installment receivables (net)

of:

a. $0.

b. $20,000.

c. $ 4,000.

d. $15,000.

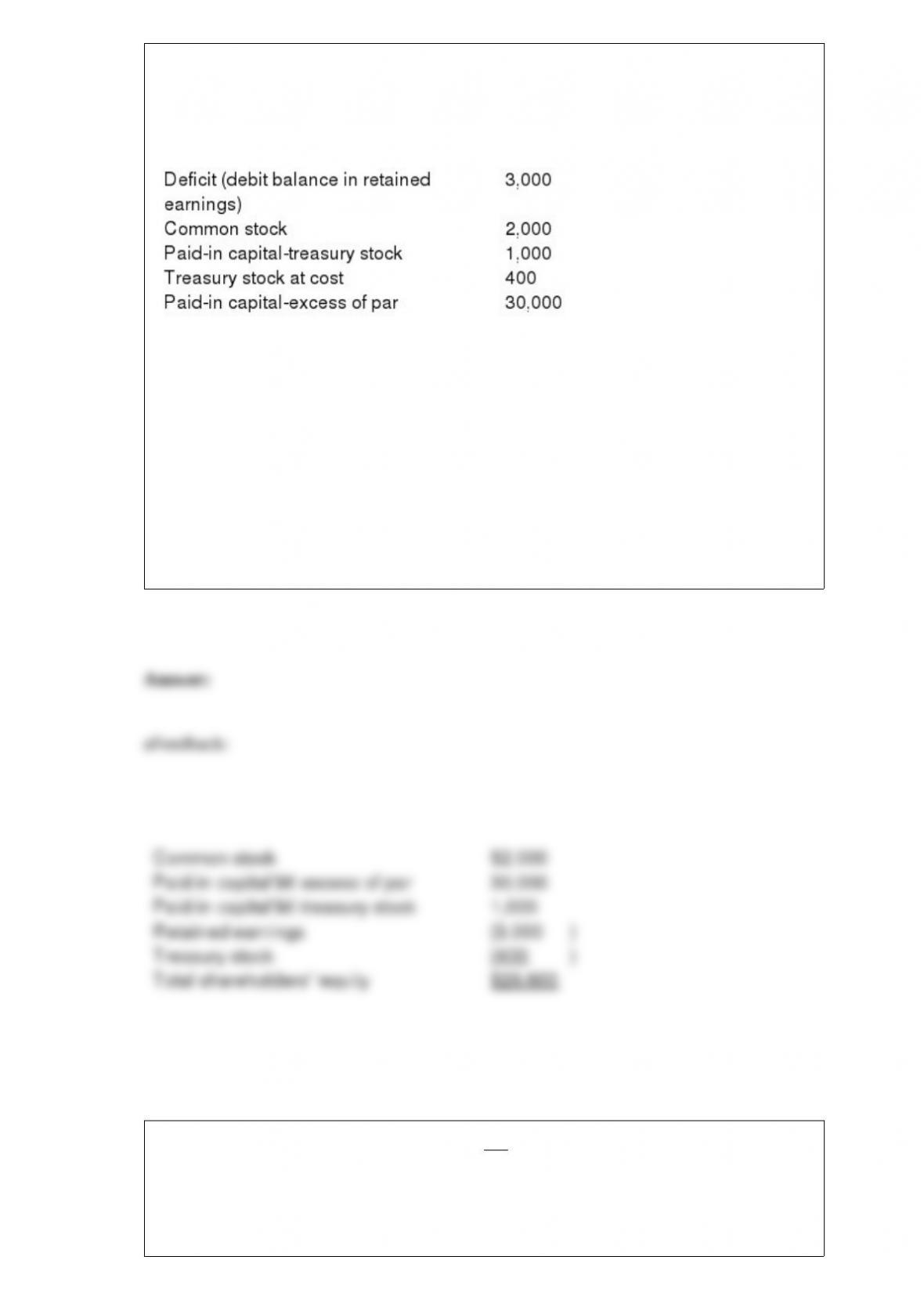

What ($ in 000s) was shareholders’ equity as of December 31, 2016?

Yellow Enterprises reported the following ($ in 000s) as of December 31, 2016. All

accounts have normal balances.

During 2017 ($ in 000s), net income was $9,000; 25% of the treasury stock was resold

for $450; cash dividends declared were $600; cash dividends paid were $500.

a. $29,600.

b. $35,600.

c. $30,400.

d. $28,600.

A statement of comprehensive income does not include:

a. Net income.

b. Losses resulting from the return on pension assets exceeding expectations.

c. Losses from changes in estimates regarding the PBO.

d. Prior service cost.

On January 1, 2016, Jeans-R-Us Company awarded 15 million of its $1 par common

shares to key personnel, subject to forfeiture if employment is terminated within three

years. On the date of the grant, the stock had a market price of $3 per share.

Required:

(1) Determine the total compensation cost pertaining to the restricted shares.

(2) Prepare the appropriate journal entry to record the award on January 1, 2016.

(3) Prepare the appropriate journal entry to record compensation expense on December

31, 2016.

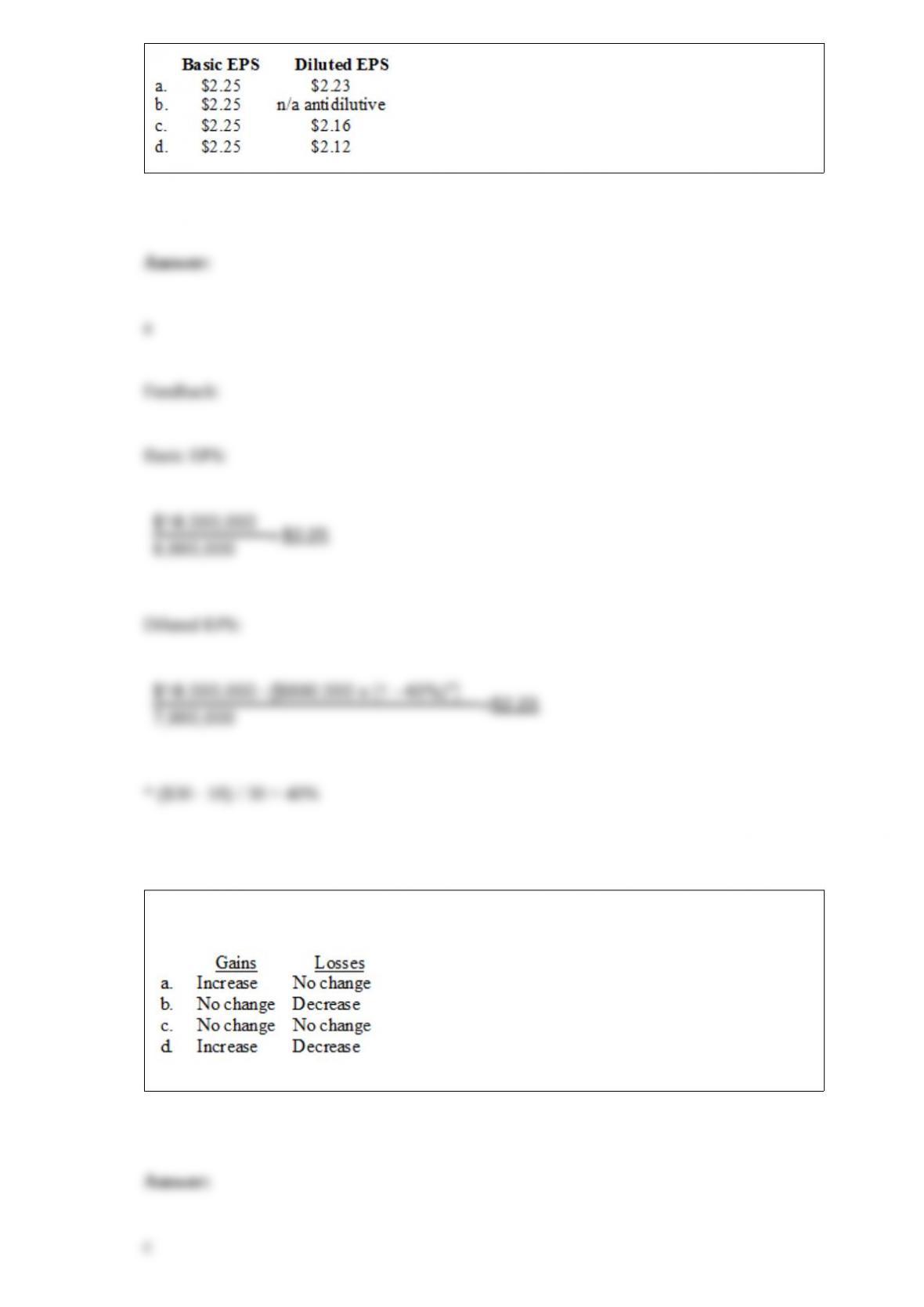

Jet Corporation had 8 million shares of common stock outstanding during the current

calendar year. On July 1, Jet issued ten thousand $1,000 face value, convertible bonds.

Each bond is convertible into 50 shares of common stock. The bonds were issued at

face amount and pay interest quarterly for 20 years. They have a stated rate of 12%. Jet

had income before tax of $30 million and a net income of $18 million. Jet would report

the following EPS data (rounded):

Unrealized holding gains and losses on securities available for sale would have the

following effects on retained earnings:

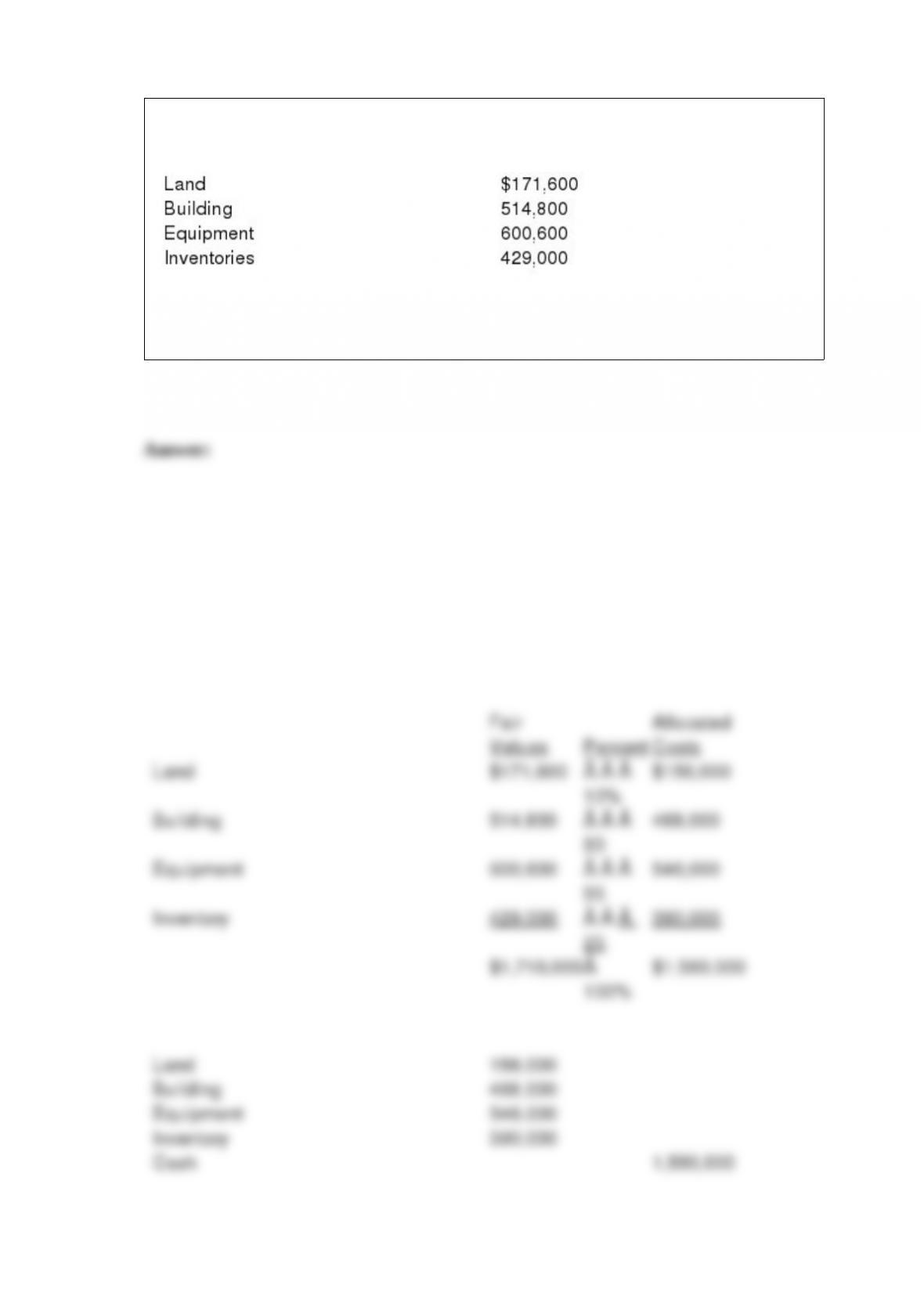

Eli Company purchased assets of Whitney Inc. at auction for $1,560,000. An

independent appraisal of the fair value of the assets acquired is listed below:

Required:

Prepare the journal entry to record the purchase of the assets.

Sometimes companies change the extent to which they can significantly influence an

investee, such that they have to change to the equity method or from the equity method

of accounting for the investment. Required:

Describe the adjustments necessary when a company (1) changes to the equity method

from another method, and (2) when a company changes from the equity method to

another method.

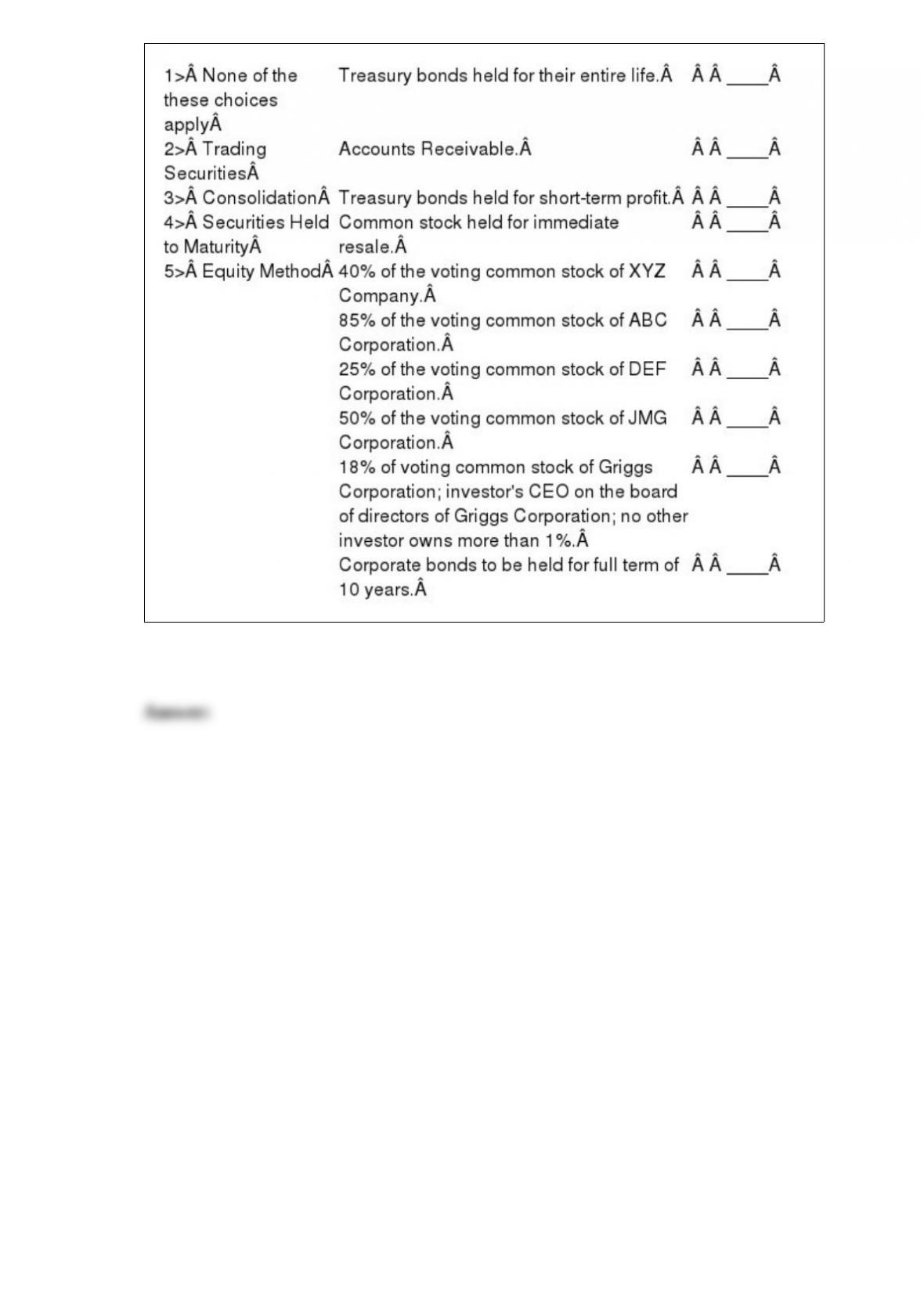

Indicate (by number) the way each of the investments listed below usually should be

accounted for under U.S. GAAP based on the information provided.

The employees of Neat Clothes work Monday through Friday. Every other Friday the

company issues payroll checks totaling $32,000. The current pay period ends on Friday,

July 3. Neat Clothes is now preparing quarterly financial statements for the three

months ended June 30. What is the adjusting entry to record accrued salaries at the end

of June?

() No entry