Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1) When numerous adjustments are necessary, companies often use a cash flow

worksheet instead of preparing a statement of cash flows.

2) When a company amends its defined benefit plan, and recognizes prior service, the

projected benefit obligation is increased to recognize this additional liability.

3) IFRS does not provide detailed guidance for leases of natural resources,

sale-leasebacks, and leveraged leases.

4) The cost of purchased patents should be amortized over the remaining legal life of

the patent.

5) The lower-of-cost-or-market method is used for inventory despite being less

conservative than valuing inventory at market value.

6) A pension plan is contributory when the employer makes payments to a funding

agency.

7) In determining present value, a company moves backward in time using a process of

accumulation.

8) Interest is the excess cash received or repaid over and above the amount lent or

borrowed.

9) When land with an old building is purchased as a future building site, the cost of

removing the old building is part of the cost of the new building.

10) If a stock dividend occurs after year-end, but before issuing the financial

statements, a company must restate the weighted-average number of shares outstanding

for the year.

11) The Supplies account had a balance at the beginning of year 3 of $8,000 (before the

reversing entry). Payments for purchases of supplies during year 3 amounted to $50,000

and were recorded as expense. A physical count at the end of year 3 revealed supplies

costing $11,500 were on hand. Reversing entries are used by this company. The

required adjusting entry at the end of year 3 will include a debit to:

a.Supplies Expense for $3,500

b.Supplies for $3,500

c.Supplies Expense for $46,500

d.Supplies for $11,500

12) In the context of dollar-value LIFO, what is a LIFO layer?

a.The difference between the LIFO inventory and the amount used for internal reporting

purposes

b.The LIFO value of the inventory for a given year

c.The inventory in base year dollars

d.The LIFO value of an increase in the inventory for a given year

13) On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to

lease a storage building from Holt Warehouse Company. Collectibility of lease

payments is reasonably predictable and no important uncertainties surround the amount

of costs yet to be incurred by the lessor. The following information pertains to this lease

agreement.

(a)The agreement requires equal rental payments at the beginning each year.

(b)The fair value of the building on January 1, 2015 is $4,000,000; however, the book

value to Holt is $3,300,000.

(c)The building has an estimated economic life of 10 years, with no residual value.

Yancey depreciates similar buildings on the straight-line method.

(d)At the termination of the lease, the title to the building will be transferred to the

lessee.

(e)Yanceys incremental borrowing rate is 11% per year. Holt Warehouse Co. set the

annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by

Yancey, Inc.

(f)The yearly rental payment includes $10,000 of executory costs related to taxes on the

property.

Future Value of Ordinary Annuity of 1

Period 5% 6% 8% 10% 12%

11.000001.000001.000001.000001.00000

22.050002.060002.080002.100002.12000

33.152503.183603.246403.310003.37440

44.310134.374624.506114.641004.77933

55.525635.637095.866606.105106.35285

66.801916.975327.335927.715618.11519

78.142018.393848.922809.4871710.08901

89.549119.8974710.6366311.4358912.29969

911.0265611.4913212.4875613.5794814.77566

1012.5778913.1807914.4865615.9374317.54874

Present Value of an Ordinary Annuity of 1

Period 5% 6% 8% 10% 12%

1.95238.94340.92593.90909.89286

21.859411.833391.783261.735541.69005

32.723252.673012.577102.486852.40183

43.545953.465113.312133.169863.03735

54.329484.212363.992713.790793.60478

65.075694.917324.622884.355264.11141

75.786375.582385.206374.868424.56376

86.463216.209795.746645.334934.96764

97.107826.801696.246895.759025.32825

107.721737.360096.710086.144575.65022

What is the amount of the minimum annual lease payment? (Rounded to the nearest

dollar.)

a.$181,801

b.$581,801

c.$591,801

d.$601,801

14) The balance sheet data of Kohler Company at the end of 2015 and 2014 follow:

2015 2014

Cash$ 100,000$ 140,000

Accounts receivable (net)240,000180,000

Inventory280,000180,000

Prepaid expenses40,000100,000

Buildings and equipment360,000300,000

Accumulated depreciationbuildings and equipment(72,000)(32,000)

Land 360,000 160,000

Totals$1,308,000$1,028,000

Accounts payable$272,000$220,000

Accrued expenses48,00072,000

Notes payablebank, long-term160,000

Mortgage payable120,000

Common stock, $10 par836,000636,000

Retained earnings (deficit) 32,000 (60,000)

$1,308,000$1,028,000

Land was acquired for $200,000 in exchange for common stock, par $200,000, during

the year; all equipment purchased was for cash. Equipment costing $20,000 was sold

for $8,000; book value of the equipment was $16,000 and the loss was reported as an

ordinary item in net income. Cash dividends of $40,000 were charged to retained

earnings and paid during the year; the transfer of net income to retained earnings was

the only other entry in the Retained Earnings account. In the statement of cash flows for

the year ended December 31, 2015, for Naley Company:

The net cash provided (used) by investing activities was

a.$52,000

b.$(80,000)

c.$(272,000)

d.$(72,000)

15) During 2014, which was the first year of operations, Oswald Company had

merchandise purchases of $985,000 before cash discounts. All purchases were made on

terms of 2/10, n/30. Three-fourths of the items purchased were paid for within 10 days

of purchase. All of the goods available had been sold at year end.

Which of the following recording procedures would result in the highest cost of goods

sold for 2014?

1>Recording purchases at gross amounts

2> Recording purchases at net amounts, with the amount of discounts not taken shown

under "other expenses" in the income statement

a. 1

b.2

c.Either 1 or 2 will result in the same cost of goods sold

d.Cannot be determined from the information provided

16) Which dividends do not reduce stockholders' equity?

a.Cash dividends

b.Stock dividends

c.Property dividends

d.Liquidating dividends

17) Hayes Corp. is a manufacturer of truck trailers. On January 1, 2014, Hayes Corp.

leases ten trailers to Lester Company under a six-year noncancelable lease agreement.

The following information about the lease and the trailers is provided:

1>Equal annual payments that are due on January 1 each year provide Hayes Corp. with

an 8% return on net investment (present value factor for 6 periods at 8% is 4.99271).

2>Titles to the trailers pass to Lester at the end of the lease.

3>The fair value of each trailer is $50,000. The cost of each trailer to Hayes Corp. is

$45,000. Each trailer has an expected useful life of nine years.

4>Collectibility of the lease payments is reasonably predictable and there are no

important uncertainties surrounding the amount of costs yet to be incurred by Hayes

Corp.

Instructions

(a)What type of lease is this for the lessor? Discuss.

(b)Calculate the annual lease payment. (Round to nearest dollar.)

(c)Prepare a lease amortization schedule for Hayes Corp. for the first three years.

(d)Prepare the journal entries for the lessor for 2014 to record the lease agreement, the

receipt of the lease rentals, and the recognition of revenue (assume the use of a

perpetual inventory method and round all amounts to the nearest dollar).

18) The methods of accounting for a lease by the lessee are

a.operating and capital lease methods

b.operating, sales, and capital lease methods

c.operating and leveraged lease methods

d.None of these answers are correct

19) Which statement is true about the retail inventory method?

a.It may not be used to estimate inventories for interim statements

b.It may not be used to estimate inventories for annual statements

c.It may not be used by auditors

d.None of these answers are correct

20) The following costs are incurred during the research and development phases of a

laser bone scanner

Identify which of these are development phase items and will be immediately expensed

under

U.S. GAAP and IFRS.

U.S. GAAP IFRS

a. $1,200,000$1,200,000

b. 2,400,0001,400,000

c. 2,400,0003,400,000

d. 3,400,0003,400,000

21) Antique Company has notes receivable that have a fair value of $920,000 and a

carrying amount of $710,000. Antique decides on December 31, 2014, to use the fair

value option for these recently-acquired receivables. The adjusting entry to record this

change will include a:

a.debit to Unrealized Holding Gain or LossIncome for $210,000

b.credit to Notes Receivable for $210,000

c.credit to Unrealized Holding Gain or LossIncome for $210,000

d.debit to Notes Receivable for $920,000

22) Presented below is information related to Hale Corporation:

Common Stock, $1 par$4,500,000

Paid-in Capital in Excess of ParCommon Stock550,000

Preferred 8 1/2% Stock, $50 par2,000,000

Paid-in Capital in Excess of ParPreferred Stock400,000

Retained Earnings1,500,000

Treasury Common Stock (at cost)150,000

The total stockholders' equity of Hale Corporation is

a.$8,800,000

b.$8,950,000

c.$7,300,000

d.$7,450,000

23) Minimum lease payments may include a

a.penalty for failure to renew

b.bargain purchase option

c.guaranteed residual value

d.any of these

24) When is a contingent liability recorded?

a.When the amount can be reasonably estimated

b.When the future events are probable to occur and the amount can be reasonably

estimated

c.When the future events are probable to occur

d.When the future events will possibly occur and the amount can be reasonably

estimated

25) Equipment that cost $400,000 and has accumulated depreciation of $315,000 is

exchanged for equipment with a fair value of $160,000 and $40,000 cash is received.

The exchange lacked commercial substance.

Instructions

(a)Show the calculation of the gain to be recognized from the exchange.

(b)Prepare the entry for the exchange. Show a check of the amount recorded for the

new equipment.

26) Which of the following is a characteristic of the expense warranty approach, but not

the sales warranty approach?

a.Estimated liability under warranties

b.Warranty expense

c.Unearned warranty revenue

d.Warranty revenue

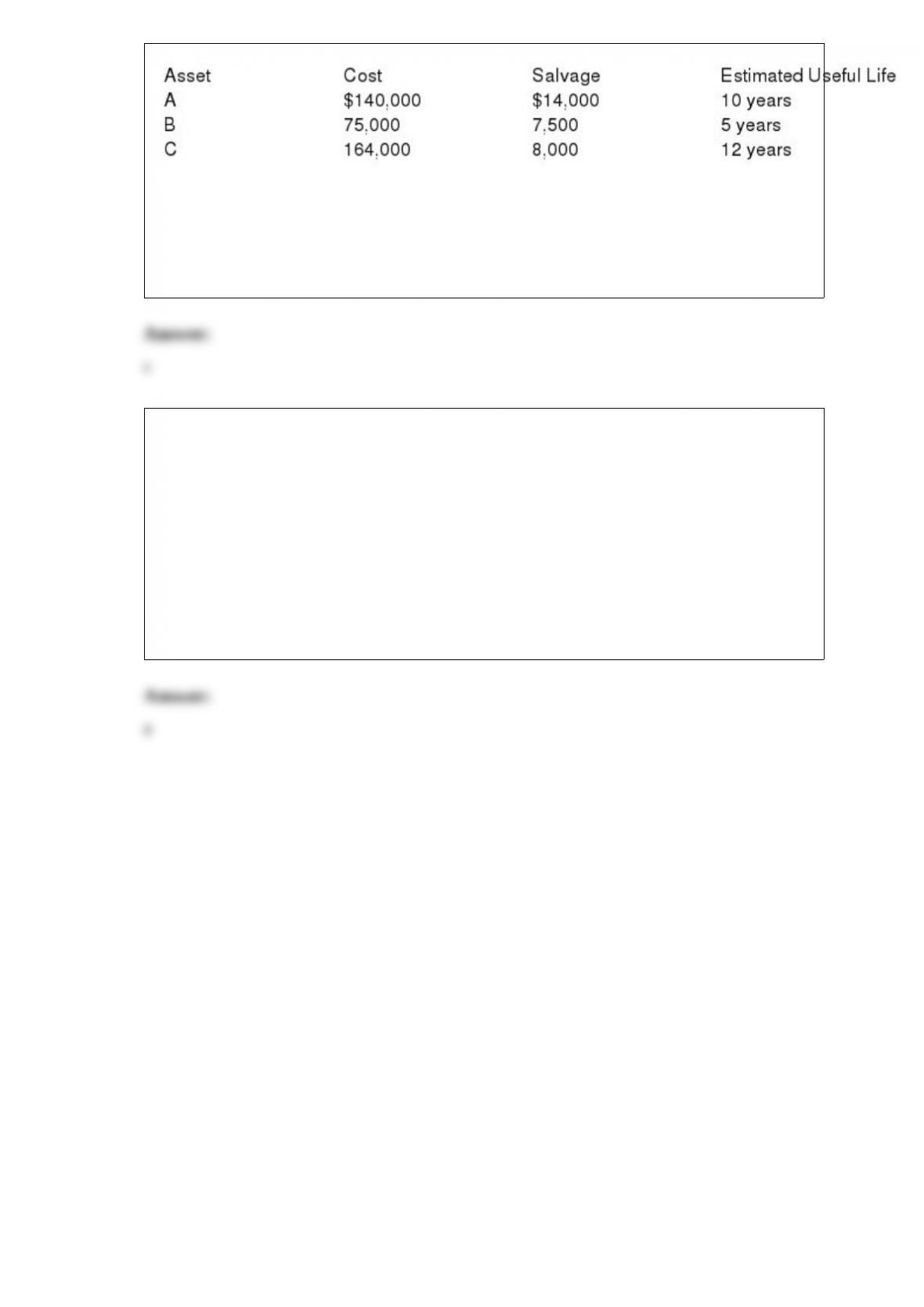

27) Exiter Inc. owns the following assets:

What is the composite life of Exiter's assets?

a.14.0 years

b.9.7 years

c.8.9 years

d.10.3 years

28) Ernst Company purchased equipment that cost $2,250,000 on January 1, 2014 . The

entire cost was recorded as an expense. The equipment had a nine-year life and a

$90,000 residual value. Ernst uses the straight-line method to account for depreciation

expense. The error was discovered on December 10, 2016 . Ernst is subject to a 40%

tax rate.

Ernsts net income for the year ended December 31, 2014, was understated by

a.$1,206,000

b.$1,350,000

c.$2,010,000

d.$2,250,000