Flexible budgeting builds the effect of changes in level of activity into the budget

system.

a. True

b. False

Answer:

If the activities causing overhead costs are different across different departments and

products, use of a plantwide factory overhead rate will cause distorted product costs.

a. True

b. False

Answer:

A formal written statement of management’s plans for the future, expressed in financial

terms, is a

a. gross profit report

b. responsibility report

c. budget

d. performance report

Answer:

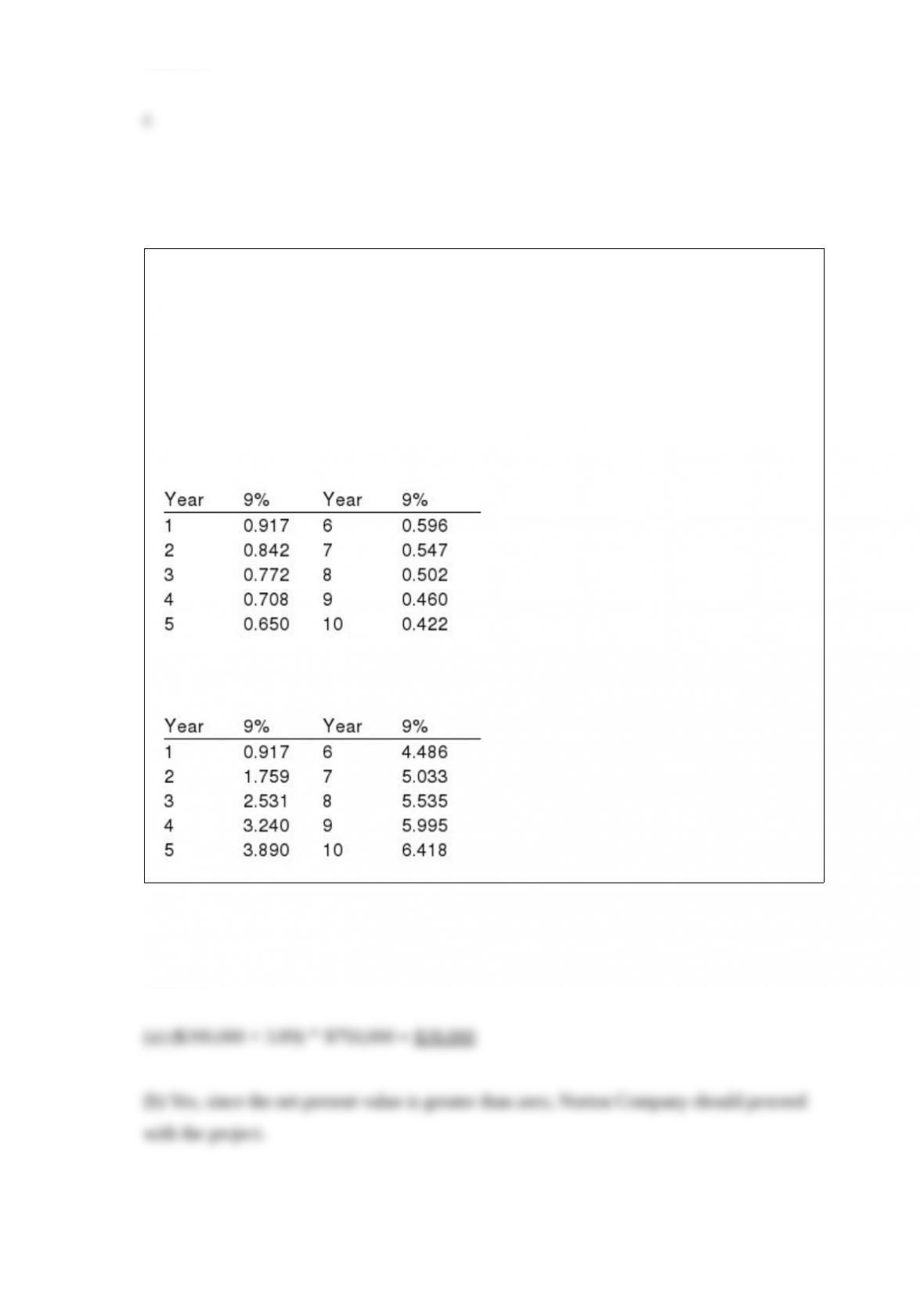

Norton Company is considering a project that will require an initial investment of

$750,000 and will return $200,000 each year for 5- years.

(a) If taxes are ignored and the required rate of return is 9%, what is the project’s net

present value?

(b) Based on this analysis, should Norton Company proceed with the project?

Below is a table for the present value of $1 at compound interest.

Below is a table for the present value of an annuity of $1 at compound interest.

Answer:

On a common-sized income statement, all items are stated as a percent of total assets or

equities at year-end.

a. True

b. False

Answer:

Starling Co. is considering disposing of a machine with a book value of $12,500 and

estimated remaining life of five years. The old machine can be sold for $1,500. A new

high-speed machine can be purchased at a cost of $25,000. It will have a useful life of

five years and no residual value. It is estimated that the annual variable manufacturing

costs will be reduced from $26,000 to $23,500 if the new machine is purchased. The

total net differential increase or decrease in cost for the new equipment for the entire

five years is

a. decrease of $11,000

b. decrease of $15,000

c. increase of $11,000

d. increase of $15,000

Answer:

Which of the following is not a cost concept commonly used in applying the cost-plus

approach to product pricing?

a. total cost concept

b. product cost concept

c. variable cost concept

d. fixed cost concept

Answer:

When using the variable cost concept of applying the cost-plus approach to product

pricing, what is included in the markup?

a. total costs plus desired profit

b. desired profit

c. total selling and administrative expenses plus desired profit

d. total fixed manufacturing costs, total fixed selling and administrative expenses, and

desired profit

Answer:

Activity cost pools are cost accumulations associated with a given activity.

a. True

b. False

Answer:

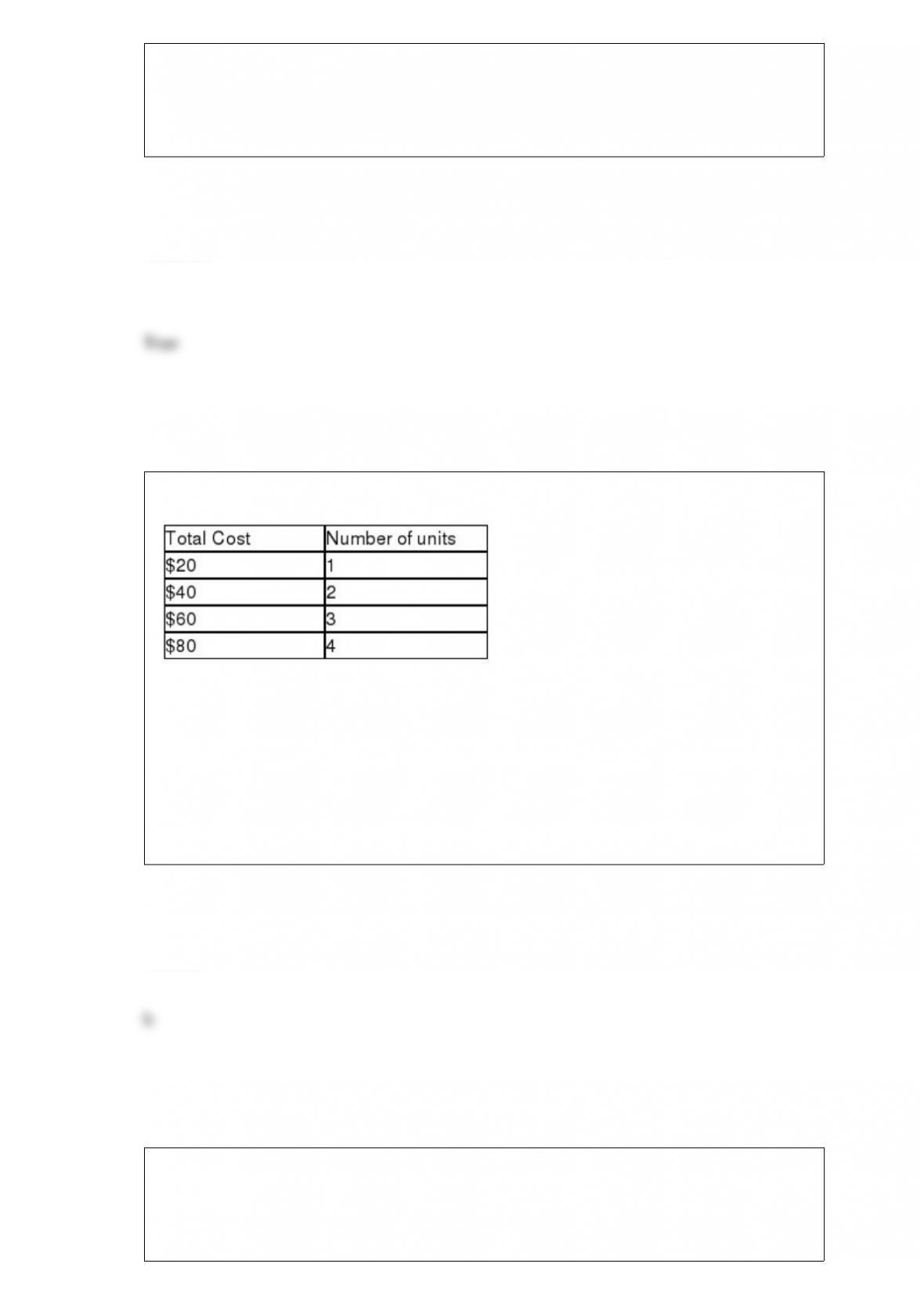

Given the following cost data, what type of cost is shown?

a. mixed cost

b. variable cost

c. fixed cost

d. period cost

Answer:

Methods that ignore present value in capital investment analysis include the average

rate of return method.

a. True

b. False

Answer:

The contribution margin and the manufacturing margin are usually equal.

a. True

b. False

Answer:

Direct materials, direct labor, and factory overhead are assigned to each manufacturing

process in a process costing system.

a. True

b. False

Answer:

Under variable costing, which of the following costs would not be included in finished

goods inventory?

a. wages of machine operator

b. steel costs for a machine tool manufacturer

c. salary of factory supervisor

d. electricity used by factory machinery

Answer:

Standards that represent levels of operation that can be attained with reasonable effort

are called

a. theoretical standards

b. ideal standards

c. variable standards

d. normal standards

Answer:

Mocha Company manufactures a single product by a continuous process, involving

three production departments. The records indicate that direct materials, direct labor,

and applied factory overhead for Department 1 were $100,000, $125,000, and

$150,000, respectively. The records further indicate that direct materials, direct labor,

and applied factory overhead for Department 2 were $55,000, $65,000, and $80,000,

respectively. In addition, work in process at the beginning of the period for Department

1 totaled $75,000, and work in process at the end of the period totaled $60,000.

The journal entry to record the flow of costs into Department 1 during the period for

direct materials is

a. Work in Process’”Department 1 Materials 100,000

100,000

b. Work in Process’”Department 1 Materials 55,000

55,000

c. Materials Work in Process’”Department 1 100,000

100,000

d. Materials Work in Process’”Department 1 55,000

55,000

Answer:

Department E had 4,000 units in Work in Process that was 40% completed at the

beginning of the period at a cost of $12,500. 14,000 units of direct materials were added

during the period at a cost of $28,700. 15,000 units were completed during the period,

and 3,000 units were 75% completed at the end of the period. All materials are added at

the beginning of the process. Direct labor was $32,450 and factory overhead was

$18,710.

The number of equivalent units of production for the period for conversion if the

average cost method is used to cost inventories was

a. 15,650

b. 14,850

c. 18,000

d. 17,250

Answer:

Management should focus its sales and production efforts on the product or products

that will provide

a. the highest sales revenue

b. the lowest product costs

c. the maximum contribution margin

d. the lowest direct labor hours

Answer:

If sales are $820,000, variable costs are 55% of sales, and operating income is

$260,000, what is the contribution margin ratio?

a. 45%

b. 55%

c. 62%

d. 32%

Answer:

The recording of the application of factory overhead costs to jobs would include a

credit to

a. Factory Overhead

b. Wages Payable

c. Work in Process

d. Cost of Goods Sold

Answer:

The Porter Beverage Factory owns a building for its operations. Porter uses only half of

the building and is considering two options for the unused space. The Popcorn Store

would like to purchase the half of the building that is not being used for $550,000. A

5% commission would have to be paid at the time of purchase. Salty Snacks would like

to lease the half of the building for the next 5 years at $100,000 each year. Stewart

would have to continue paying $15,000 of property taxes each year and $2,000 of

yearly insurance on the property, according to the proposed lease agreement.

Determine the differential income or loss from the lease alternative.

Answer:

Average income as a percentage of average investment

Match the definition that follows with the term (a’“e) it defines.

p. Capital investment analysis

q. Time value of money concept

r. Net present value method

s. Average rate of return

t. Cash payback period

Answer:

The cost of direct materials transferred into the Bottling Department of the Mountain

Springs Water Company is $27,225. The conversion cost for the period in the Bottling

Department is $7,596. The total equivalent units for direct materials and conversion are

60,500 and 63,300, respectively. Determine the direct materials and conversion cost per

equivalent unit. Round answers to nearest cent.

Answer:

Not relevant to future decisions

Match the definitions that follow with the term (a’“e) it defines.

p. Opportunity cost

q. Sunk cost

r. Theory of constraints

s. Differential analysis

t. Product cost distortion

Answer:

Kamin Company’s Mixing Department had a beginning inventory of 4,000 units which

had accumulated conversion costs of $55,000. During the period, the Mixing

Department accumulated conversion costs of $92,000 and started 8,000 new units.

Ending inventory was 2,500 units which were 40% complete with respect to conversion

costs. Kamin uses the average cost method to cost inventories.

Calculate the cost per equivalent unit for conversion costs in the Mixing Department.

Answer:

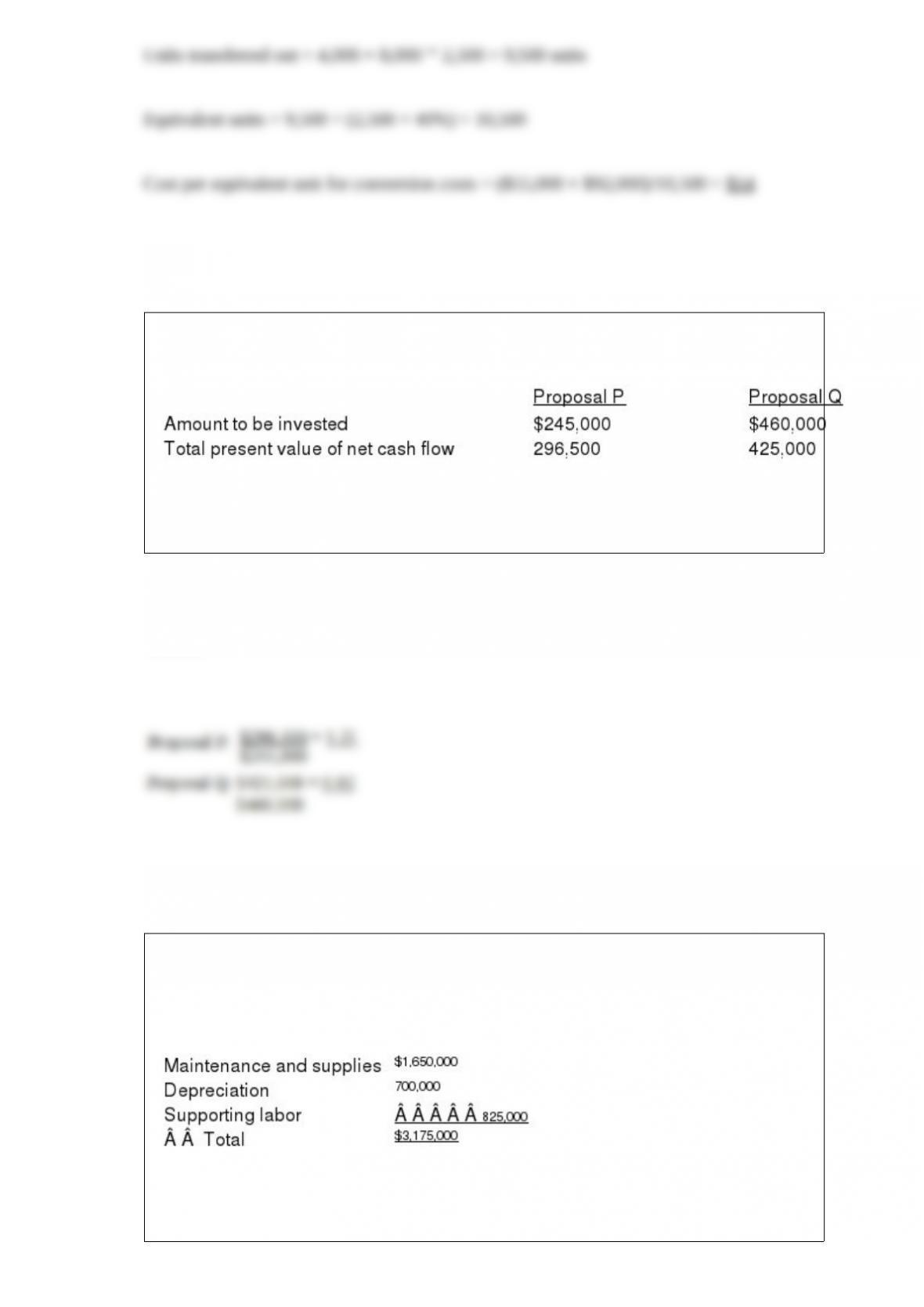

The net present value has been computed for Proposals P and Q. Relevant data are as

follows:

Determine the present value index for each proposal. Round your answers to two

decimal places.

Answer:

Alaskan Pattern Company makes dressmakers’ patterns using a machine that stamps the

pattern outline onto tissue paper. The stamping center produced 40,000 patterns in

August, with a machine time per pattern of 20 seconds. Annual budgeted cell

conversion costs were as follows:

Alaskan planned 2,500 total machine hours for the year.

Calculate Alaskan’s budgeted cell conversion cost rate for the year.

Answer:

Also referred to as capital budgeting

Match the definition that follows with the term (a’“e) it defines.

k. Capital investment analysis

l. Time value of money concept

m. Net present value method

n. Average rate of return

o. Cash payback period

Answer: