1) on a classified balance sheet, companies usually list current assets

a.in alphabetical order

b.with the largest dollar amounts first

c.in the order in which they are expected to be converted into cash

d.in the order of acquisition

2) green realty company received a check for $24,000 on july 1 which represents a 6

month advance payment of rent on a building it rents to a client. unearned rent was

credited for the full $24,000. financial statements will be prepared on july 31. green

realty should make the following adjusting entry on july 31:

a.debit unearned rent, $4,000; credit rental revenue, $4,000

b.debit rental revenue, $4,000; credit unearned rent, $4,000

c.debit unearned rent, $24,000; credit rental revenue, $24,000

d.debit cash, $24,000; credit rental revenue, $24,000

3) the term residual claim refers to a stockholders right to

a.receive dividends

b.share in assets upon liquidation

c.acquire additional shares when offered

d.exercise a proxy vote

4) under the equity method, the stock investments account is credited when the

a.investee reports net income

b.investee reports a net loss

c.investment is originally acquired

d.investee reports net income and when the investment is originally acquired

5) if a bond has a contract rate of interest of 6%, but the discount rate of interest is 8%,

the bond

a.will sell at a discount (less than face value)

b.will sell at a premium (more than face value)

c.may sell at either a premium or a discount

d.will sell at its face value

6) the order of presentation of items that may appear on the income statement is

a.extraordinary items, discontinued operations, income before income taxes

b.discontinued operations, extraordinary items, income before income taxes

c.income before income taxes, discontinued operations, extraordinary items

d.income before income taxes, extraordinary items, discontinued operations

7) reporting which one of the following allows analysts to make adjustments to

compare companies using different cost flow methods?

a.fifo reserve

b.inventory turnover ratio

c.lifo reserve

d.current replacement cost

8) ace inc. has 10,000 shares of 6%, $100 par value, cumulative preferred stock and

50,000 shares of $1 par value common stock outstanding at december 31, 2012. what is

the annual dividend on the preferred stock?

a.$60 per share

b.$60,000 in total

c.$6,000 in total

d.$0.60 per share

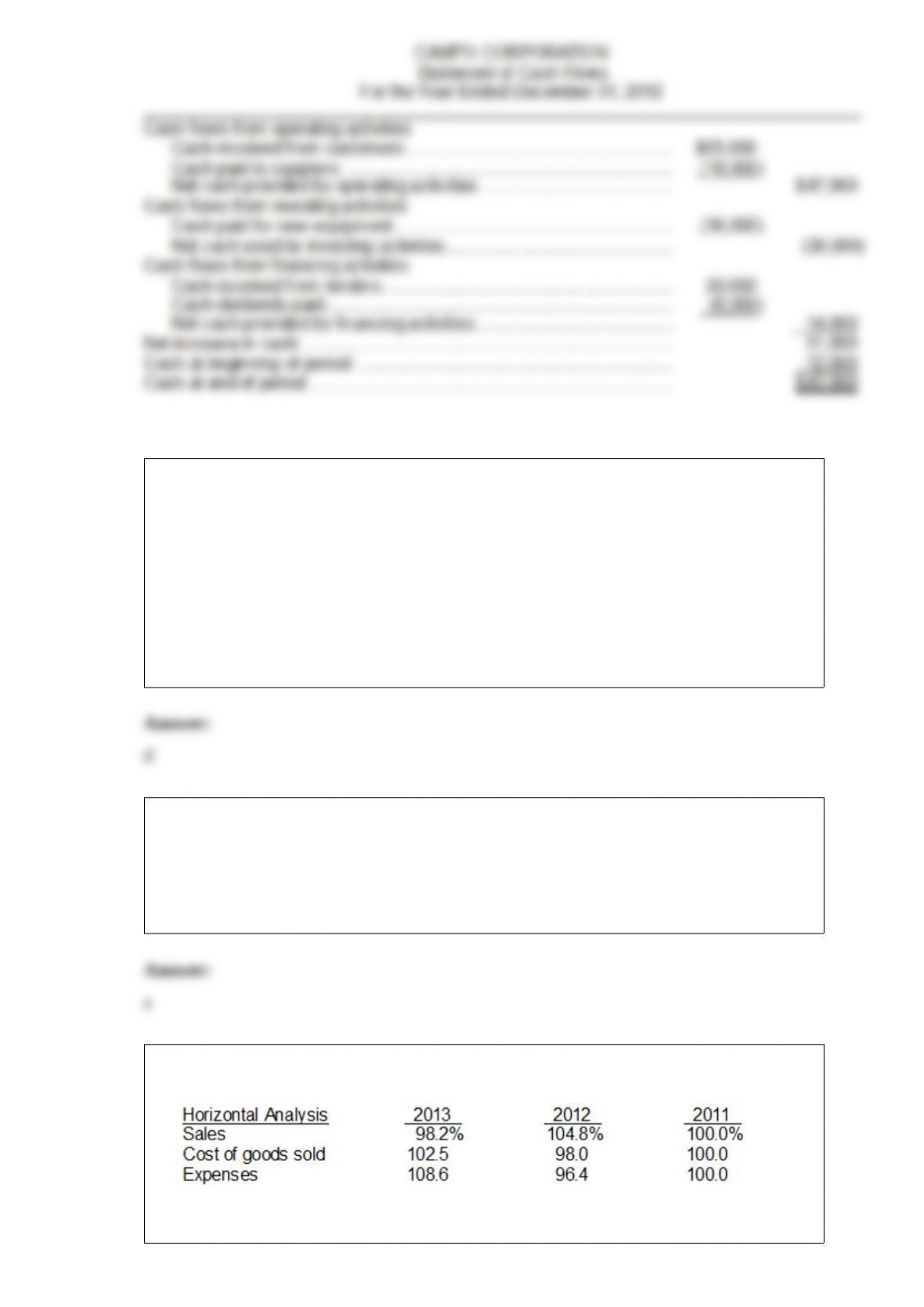

9) this information is for campo corporation for the year ended december 31, 2012.

instructions

prepare the 2012 statement of cash flows for campo corporation.

10) which of the following statements is true with respect to financial statement

reporting for all cases when a company changes from one acceptable accounting

method to another?

a.comparability across periods is impaired

b.only a footnote is required to report the change

c.changes in both depreciation methods and inventory methods are reported

retroactively

d.management must indicate that the accounting method change is preferable to the old

method

11) bonds that are secured by real estate are termed

a.mortgage bonds

b.serial bonds

c.debentures

d.convertible bonds

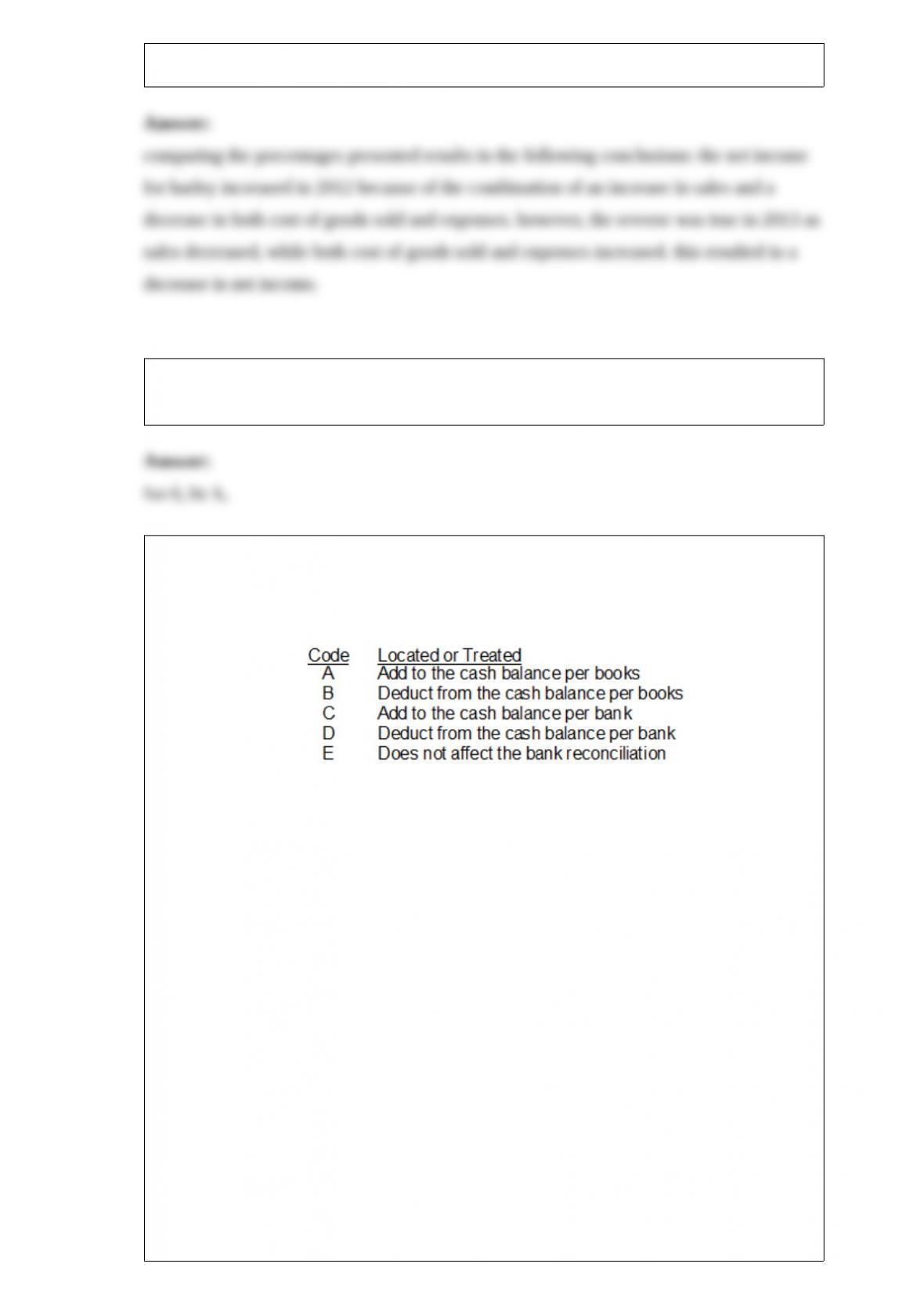

12) horizontal analysis (trend analysis) percentages for harley companys sales, cost of

goods sold, and expenses are listed here.

instructions

explain whether harleys net income increased, decreased, or remained unchanged over

the 3-year period.

13) an adjusted trial balance must be prepared before the adjusting entries can be

recorded.

14) listed below are items that may be useful in preparing the march 2010, bank

reconciliation for the carrinton machine works.

using the code letters below, insert in the space before each item the letter where the

amount would be located or otherwise treated in the bank reconciliation process.

1>included with the bank statement materials was a check from joe terrell for $40

stamped “account closed.

2>a personal deposit by ron carrinton to his personal account in the amount of $300 for

dividends on his general electric common stock was credited to the company account.

3>the bank statement included a debit memorandum for $22.00 for four books of blank

checks for carrinton machine works.

4>the bank statement contains a credit memorandum for $42.75 interest on the average

checking account balance.

5>the daily deposits of march 30 and march 31 for $3,362 and $3,125, respectively,

were not included in the bank statement postings.

6>two checks totaling $316.86, which were outstanding at the end of february, cleared

in march and were returned with the march statement.

7>the bank statement included a credit memorandum dated march 28, 2012, for $62.00

for the monthly interest on a 6-month, $15,000 certificate of deposit that the company

owns.

8>four checks, #8712, #8716, #8718, #8719, totaling $5,369.65, did not clear the bank

during march.

9>on march 24, 2012, carrinton machine works delivered to the bank for collection a

$3,400, 3-month note from tom jacobs. a credit memorandum dated march 29, 2012,

indicated the collection of the note and $102.00 of interest.

10>the bank statement included a debit memorandum for $20.00 for the collection

service on the above note and interest.

15) trent company is considering an investment that will return a lump sum of

$1,000,000 six years from now. what amount should trent company pay for this

investment to earn a 12% return?

16) a contra asset account is subtracted from a related account in the balance sheet.

17) for each item below, indicate whether a debit or credit applies.

18) accrued revenues are revenues that have been received but not yet earned.

19) goodwill is an unusual asset in that it cannot be sold individually apart from a

business as a whole. if goodwill is an intangible asset, why can’t it be sold like other

intangible assets such as copyrights and patents? briefly explain what makes goodwill

different.

20) compute the maturity value as indicated for each of the following notes receivable.

21) explain sustainable income. what relationship does this concept have to the

treatment of irregular items on the income statement?