In its 2016 income statement, WME reported $11,000 of interest expense on its

outstanding bonds. During the year, WME paid its regular installments of $9,000 of

interest in cash. In its reconciliation schedule, WME should:

Each year, White Mountain Enterprises (WME) prepares a reconciliation schedule that

compares its income statement with its statement of cash flows on both the direct and

indirect method bases.

a. Show a $2,000 positive adjustment to net income under the indirect method for the

decrease in bond premium.

b. Show a $2,000 negative adjustment to net income under the indirect method for the

decrease in bond premium.

c. Show a $2,000 positive adjustment to net income under the indirect method for the

decrease in bond discount.

d. Show a $2,000 negative adjustment to net income under the indirect method for the

decrease in bond discount.

If convertible bonds were issued at a discount, when computing diluted EPS, the

amortization of the bond discount:

a. Will have no effect.

b. Will decrease the numerator.

c. Will increase the numerator.

d. May increase or decrease the numerator, depending on the amortization method used.

Which of the following does not represent potential shares?

a. Convertible preferred stock.

b. Convertible bonds.

c. Stock rights.

d. Participating preferred stock.

Retained earnings represent:

a. Earned capital.

b. Cash.

c. Assets.

d. Net assets.

When recognizing compensation under a stock option plan, unanticipated forfeitures

are treated as:

a. A change in accounting principle.

b. A loss.

c. An income item.

d. A change in estimate.

The lessee normally measures the lease liability to be recorded as the:

a. Future value of the minimum lease payments.

b. Sum of the cash payments over the term of the lease.

c. Present value of the minimum lease payments.

d. Fair market value of the leased asset.

Ford Motor Company purchases services from suppliers on account and sells its

products to distributors on short-term credit. As a result, do each of these events affect

net income faster than they affect net operating cash flows?

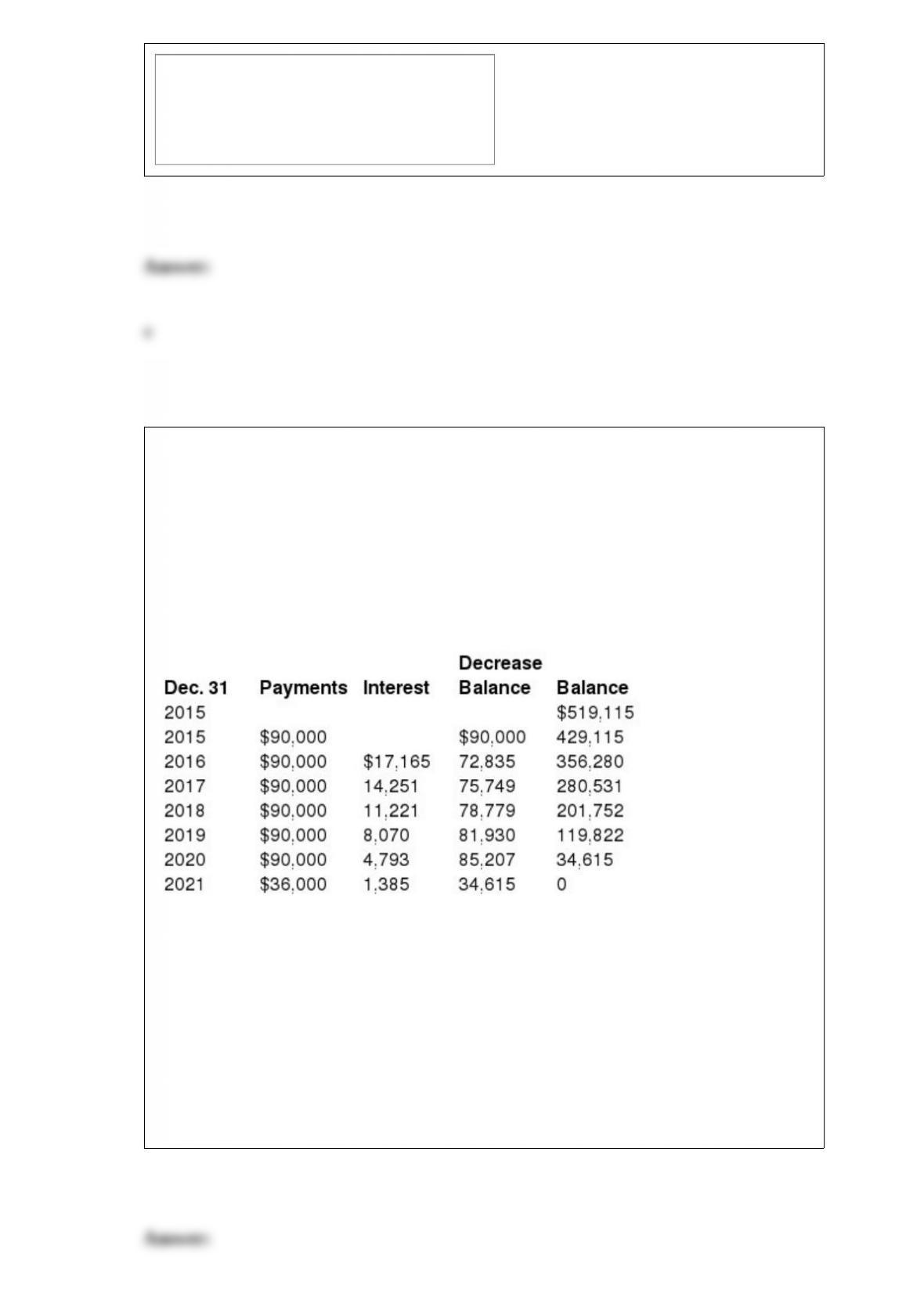

On December 31, 2015, Reagan Inc. signed a lease for some equipment having a

nine-year useful life with Silver Leasing Co. The lease payments are made by Reagan

annually, beginning at signing date. Title does not transfer to the lessee, so the

equipment will be returned to the lessor on December 31, 2021. There is no bargain

purchase option, and Reagan guarantees a residual value to the lessor on termination of

the lease.

Reagan’s lease amortization schedule appears below:

What is the amount of residual value guaranteed by Reagan to the lessor?

a. $ 1,385.

b. $34,615.

c. $36,000.

d. Cannot be determined from the given information.

Which of the following applies to a seller who is an agent?

a. Warehouses inventory

b. Liable for the delivery of goods or services to the client

c. Charges a commission for each transaction

d. Records revenue at full transaction price

Revenue should not be recognized until:

a. The seller has transferred goods or services to a customer.

b. Contracts have been signed and payment has been received.

c. Work has been performed and customer has been billed.

d. Collection has been made and warrantees have expired.

The net pension liability (PBO minus plan assets) is increased by:

a. Service cost.

b. Expected return on plan assets.

c. Amortization of prior service cost.

d. Cash contributions to plan assets.

Tim Howard Gloves issued 4.75% bonds with a face amount of $24 million, together

with 4 million shares of its $1 par value common stock, for a combined cash amount of

$44 million. The market value of Howard’s stock cannot be determined. The bonds

would have sold for $18 million if issued separately. For this transaction, Howard

should record paid-in capital’”-excess of par in the amount of:

a. $26 million

b. $22 million

c. $18 million

d. $16 million

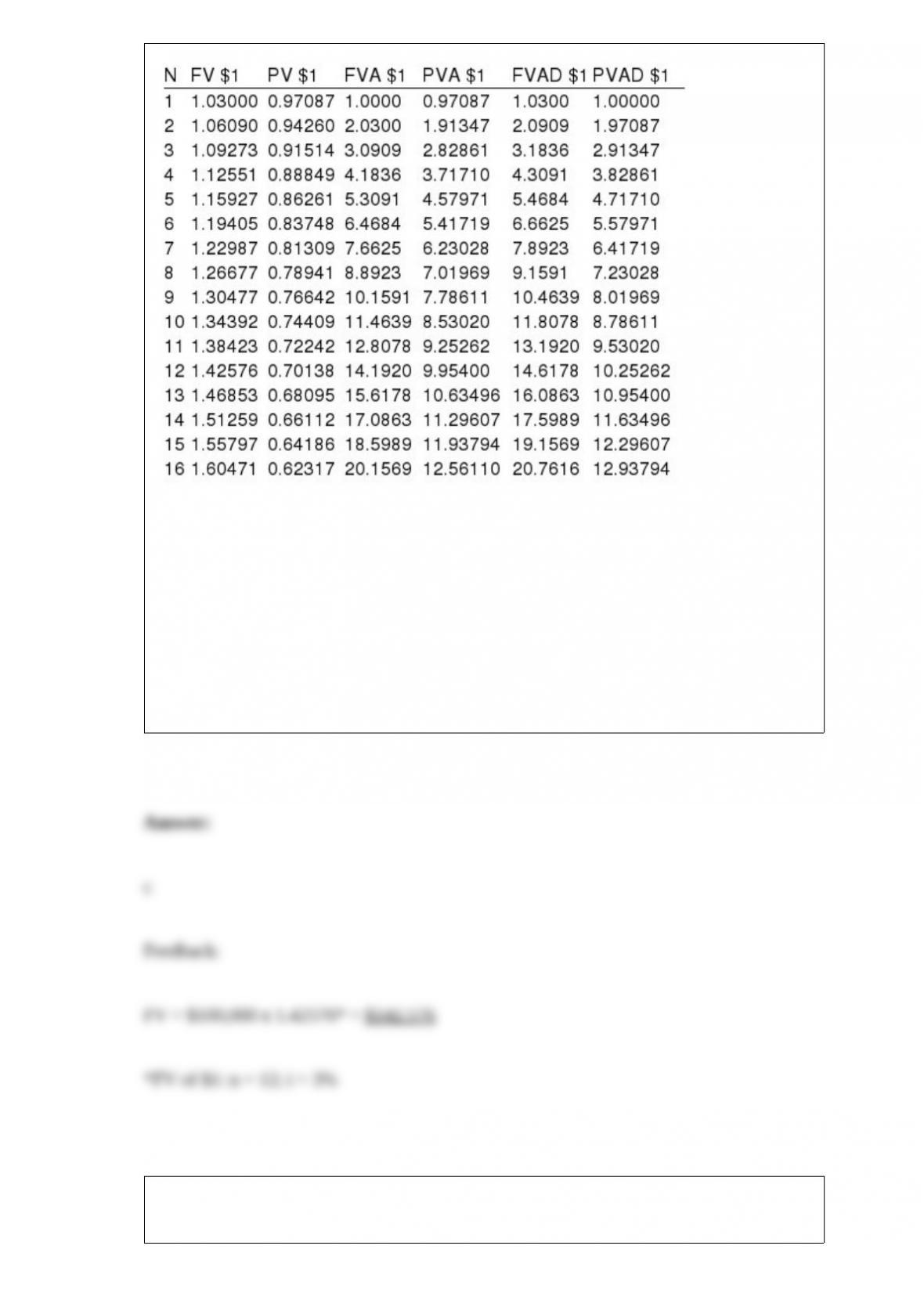

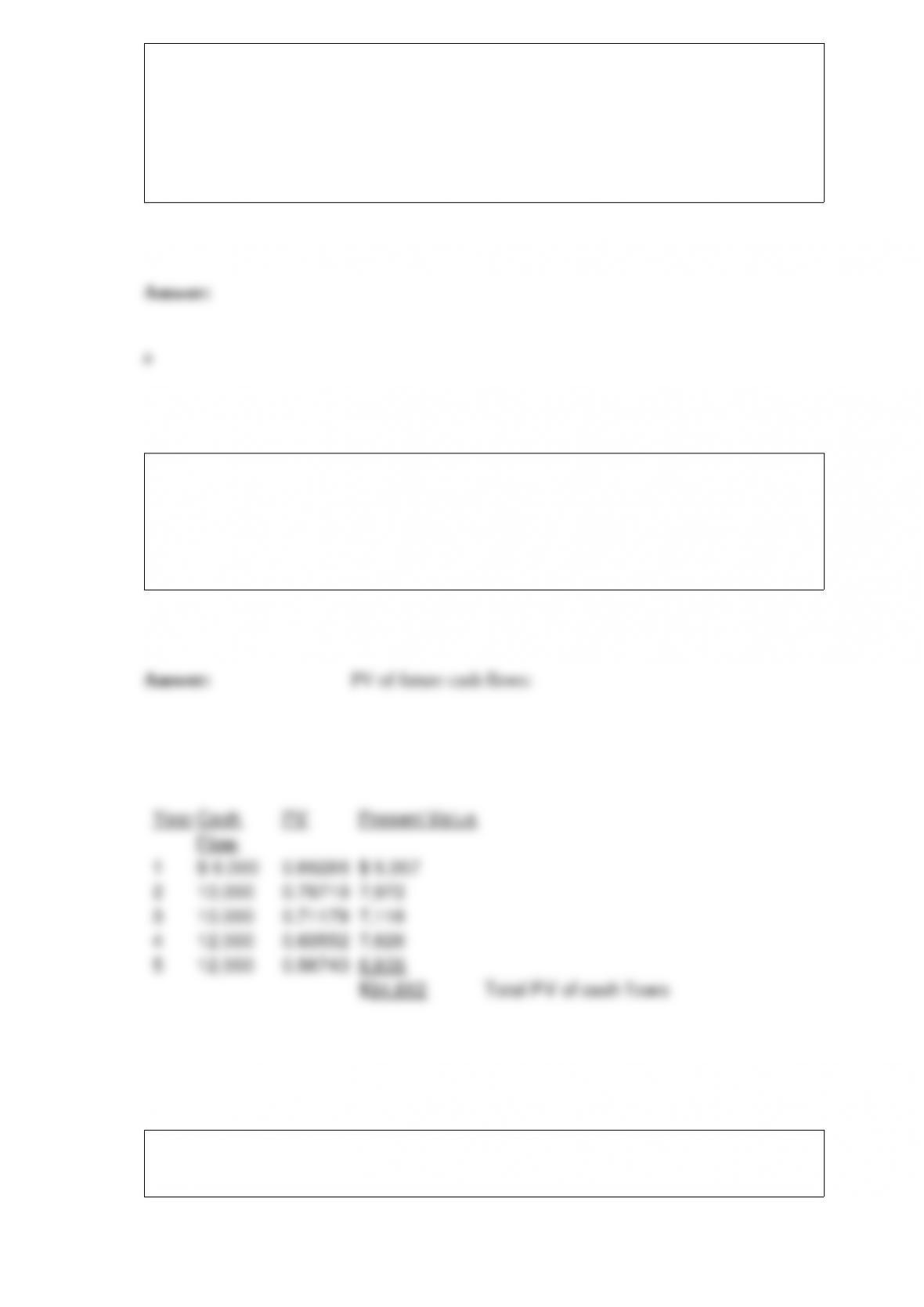

Present and future value tables of $1 at 3% are presented below:

Today, Thomas deposited $100,000 in a three-year, 12% CD that compounds quarterly.

What is the maturity value of the CD?

a. $109,270.

b. $119,410.

c. $142,576.

d. $309,090.

Hong Kong Clothiers reported revenue of $5,000,000 for its year ended December 31,

2016. Accounts receivable at December 31, 2015 and 2016, were $320,000 and

$355,000, respectively. Using the direct method for reporting cash flows from operating

activities, Hong Kong Clothiers would report cash collected from customers of:

a. $4,965,000.

b. $5,000,000.

c. $5,035,000.

d. $5,045,000.

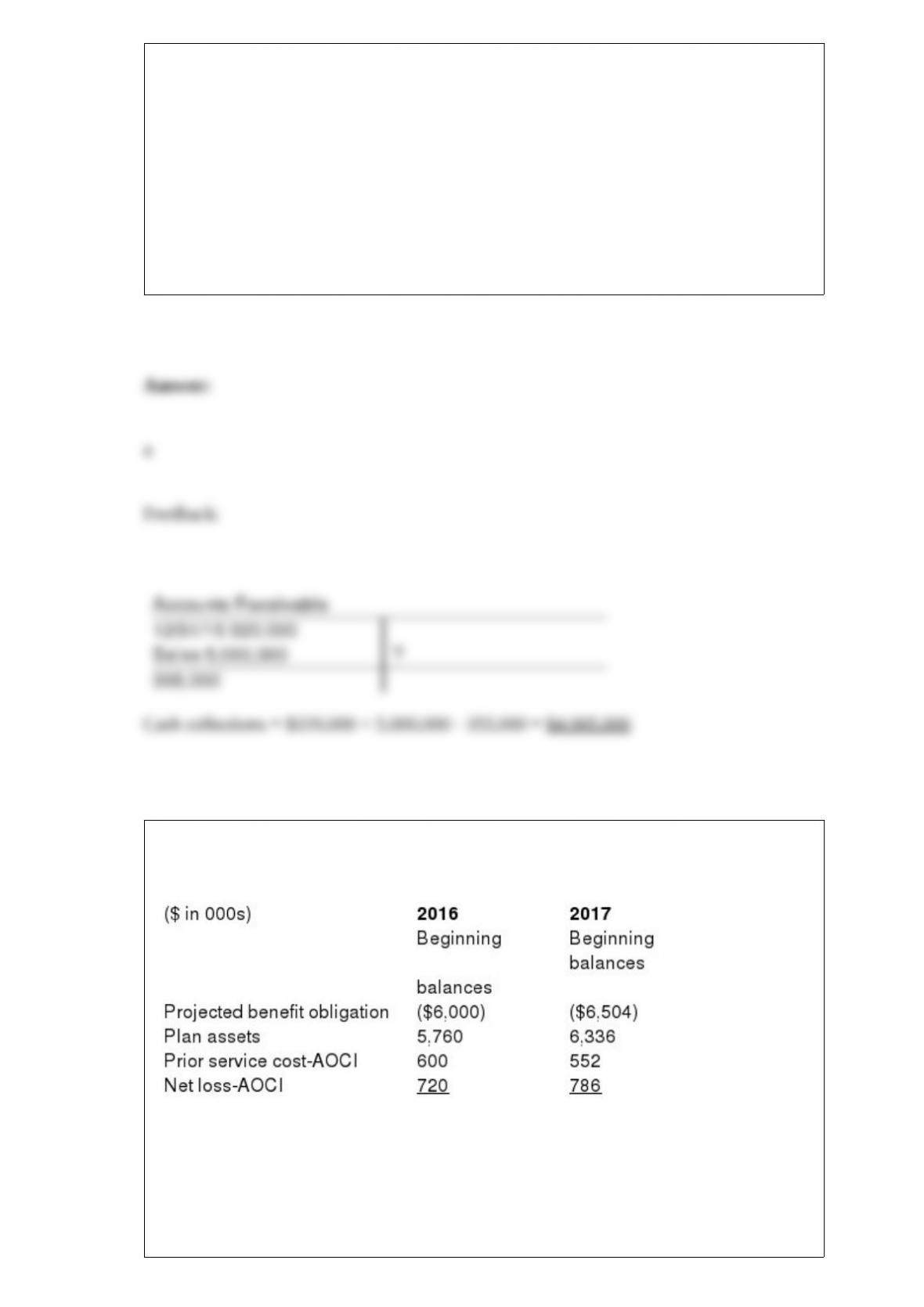

The following information pertains to Havana Corporation’s defined benefit pension

plan:

At the end of 2016, Havana contributed $696 thousand to the pension fund and benefit

payments of $624 thousand were made to retirees. The expected rate of return on plan

assets was 10%, and the actuary’s discount rate is 8%. There were no changes in

actuarial estimates and assumptions regarding the PBO.

What is the 2016 pension expense for Havana’s plan?

a. $594 thousand.

b. $606 thousand.

c. $678 thousand.

d. None of these answer choices is correct.

The cost of self-constructed fixed assets should:

a. Include allocated indirect costs just as they are for production of products.

b. Include only incremental indirect costs.

c. Include only specifically identifiable indirect costs.

d. Not include indirect costs.

Touche Manufacturing is considering a rearrangement of its manufacturing operations.

A consultant estimates that the rearrangement should result in after-tax cash savings of

$6,000 the first year, $10,000 for the next two years, and $12,000 for the next two

years. Interest is at 12%. Assume cash flows occur at the end of the year.

Required: Calculate the total present value of the cash flows.

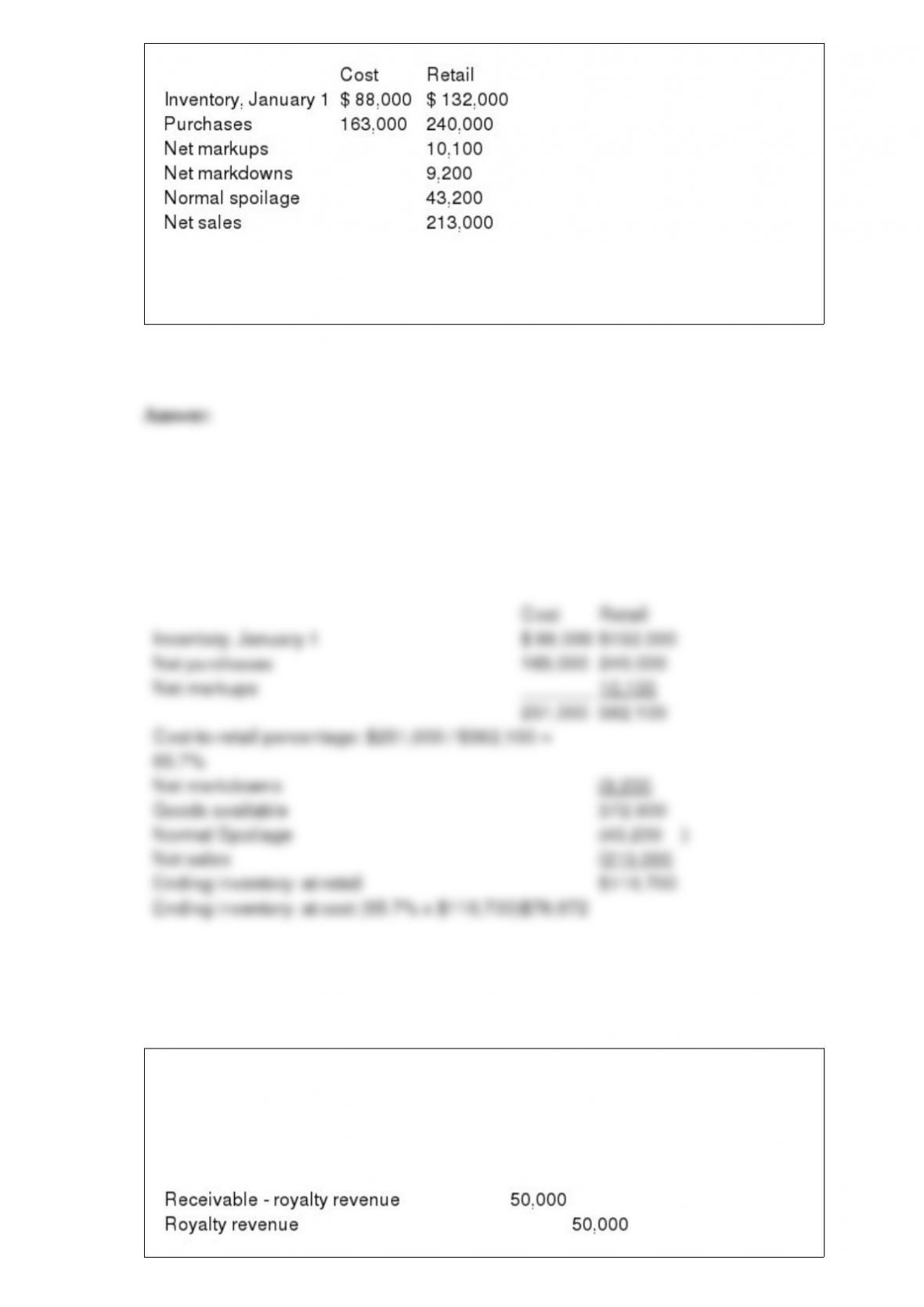

Zanesville Pots Co. uses the conventional retail method to estimate ending inventories.

The following data has been summarized for the year ended December 31, 2016:

Required:

Estimate the cost of ending inventory applying the conventional retail method.

Johnson Company receives royalties on a patent it developed several years ago.

Royalties are 5% of net sales, to be received on September 30 for sales from January

through June and receivable on March 31 for sales from July through December. The

patent rights were distributed on July 1, 2015, and Johnson accrued royalty revenue of

$50,000 on December 31, 2015, as follows:

Johnson received royalties of $65,000 on March 31, 2016, and $90,000 on September

30, 2016. In December, 2016, the patent user indicated to Johnson that sales subject to

royalties for the second half of 2016 should be $600,000.

Required:

Prepare any journal entries Johnson should record during 2016 related to the royalty

revenue.

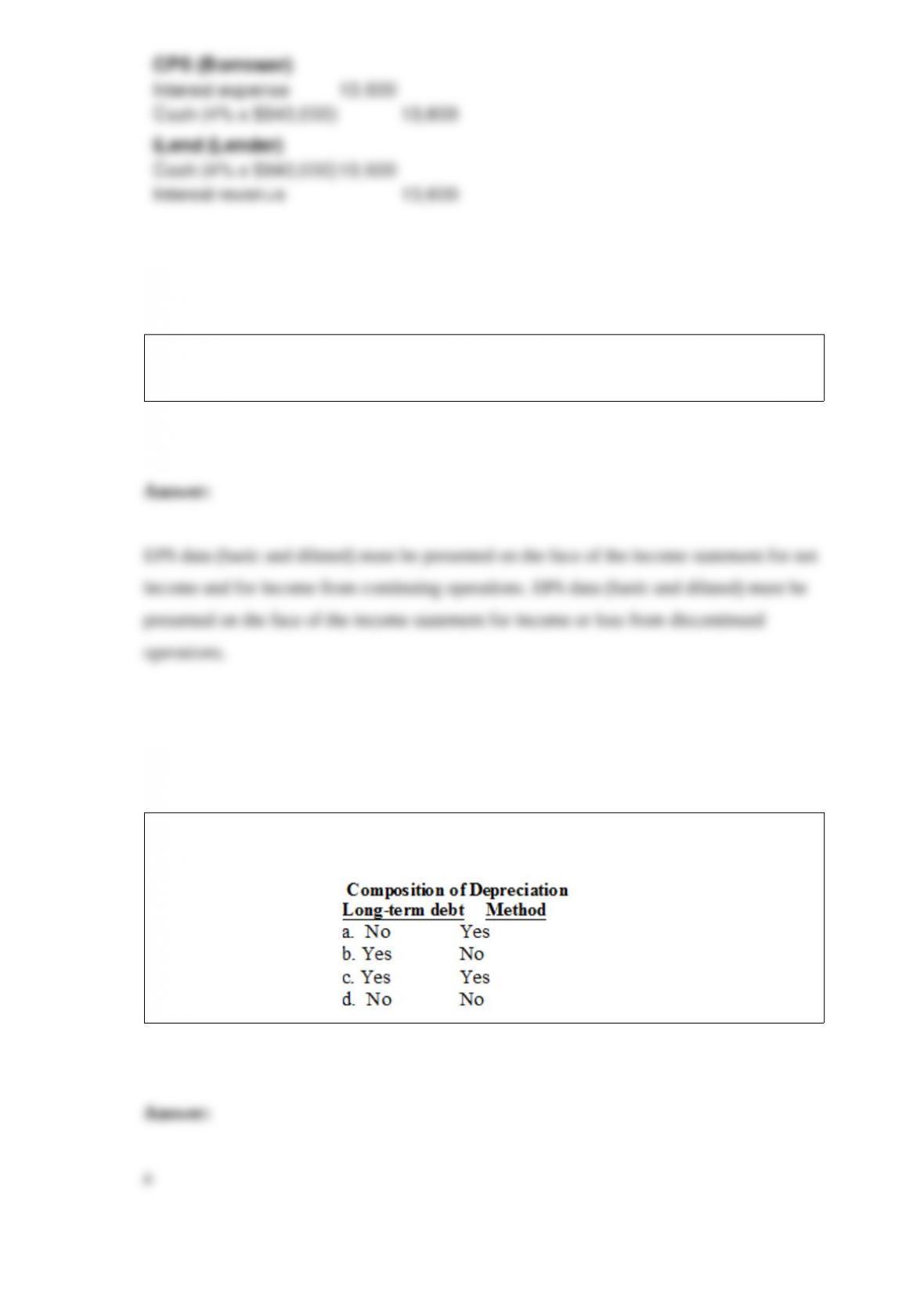

On January 1, 2016, CPS Co. borrowed $340,000 cash from iLend and issued a

five-year, $340,000, 4% note. Interest was payable annually on December 31.

Required:

Prepare the journal entries for both firms to record interest at December 31, 2016.

When the income statement includes discontinued operations, which amounts require

per share presentation?

Which of the following would be disclosed in the summary of significant accounting

policies disclosure note?