In 2014, Winn, Inc., issued $1 par value common stock for $35 per share. No other

common stock transactions occurred until July 31, 2016, when Winn acquired some of

the issued shares for $30 per share and retired them. Which of the following statements

correctly states an effect of this acquisition and retirement?

a. 2016 net income is decreased.

b. Additional paid-in capital is decreased.

c. 2016 net income is increased.

d. Retained earnings is increased.

Hanson Company had the following account balances for 2016:

Hanson reported net income of $90,000 for 2016. Assuming no other changes in current

account balances, what is the amount of net cash provided by operating activities for

2016 reported in the statement of cash flows?

a. $ 70,000.

b. $ 80,000.

c. $100,000.

d. $110,000.

A quality-assurance warranty typically results in the seller:

a. Accruing an expense for anticipated warranty costs at the time the warrantied product

is sold.

b. Recognizing an asset for accrued warranty costs which is amortized over the life of

the warranty.

c. Recognizing revenue over the life of the extended warranty.

d. Refunding warranty payments upon expiration of the warranty.

During 2016, Hoffman Co. decides to use FIFO to account for its inventory

transactions. Previously, it had used LIFO.

a. Hoffman is not required to make any accounting adjustments.

b. Hoffman has made a change in accounting principle requiring retrospective

adjustment.

c. Hoffman has made a change in accounting principle requiring prospective

application.

d. Hoffman needs to correct an accounting error.

During 2016 Marquis Company was encountering financial difficulties and seemed

likely to default on a $300,000, 10%, four-year note dated January 1, 2014, payable to

Third Bank. Interest was last paid on December 31, 2015. On December 31, 2016,

Third Bank accepted $250,000 in settlement of the note. Ignoring income taxes, what

amount should Marquis report as a gain from the debt restructuring in its 2016 income

statement?

a. $20,000.

b. $50,000.

c. $80,000.

d. $0.

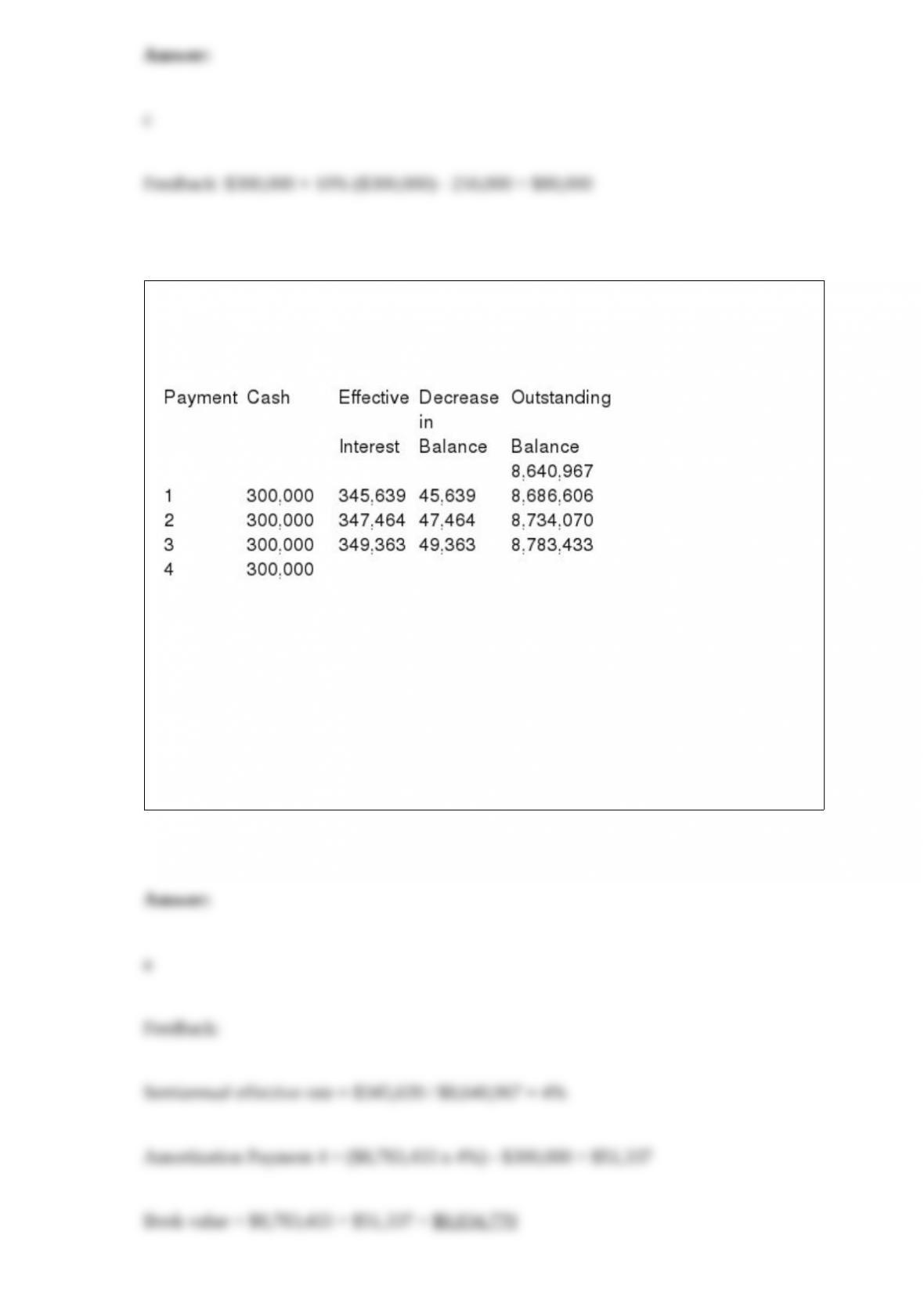

Discount-Mart issued ten thousand $1,000 bonds on January 1, 2016. The bonds have a

10-year term and pay interest semiannually. This is the partial bond amortization

schedule for the bonds.

What is the book value of the bonds as of December 31, 2017?

a. $8,834,770.

b. $8,686,606.

c. $8,734,070.

d. $8,783,433.

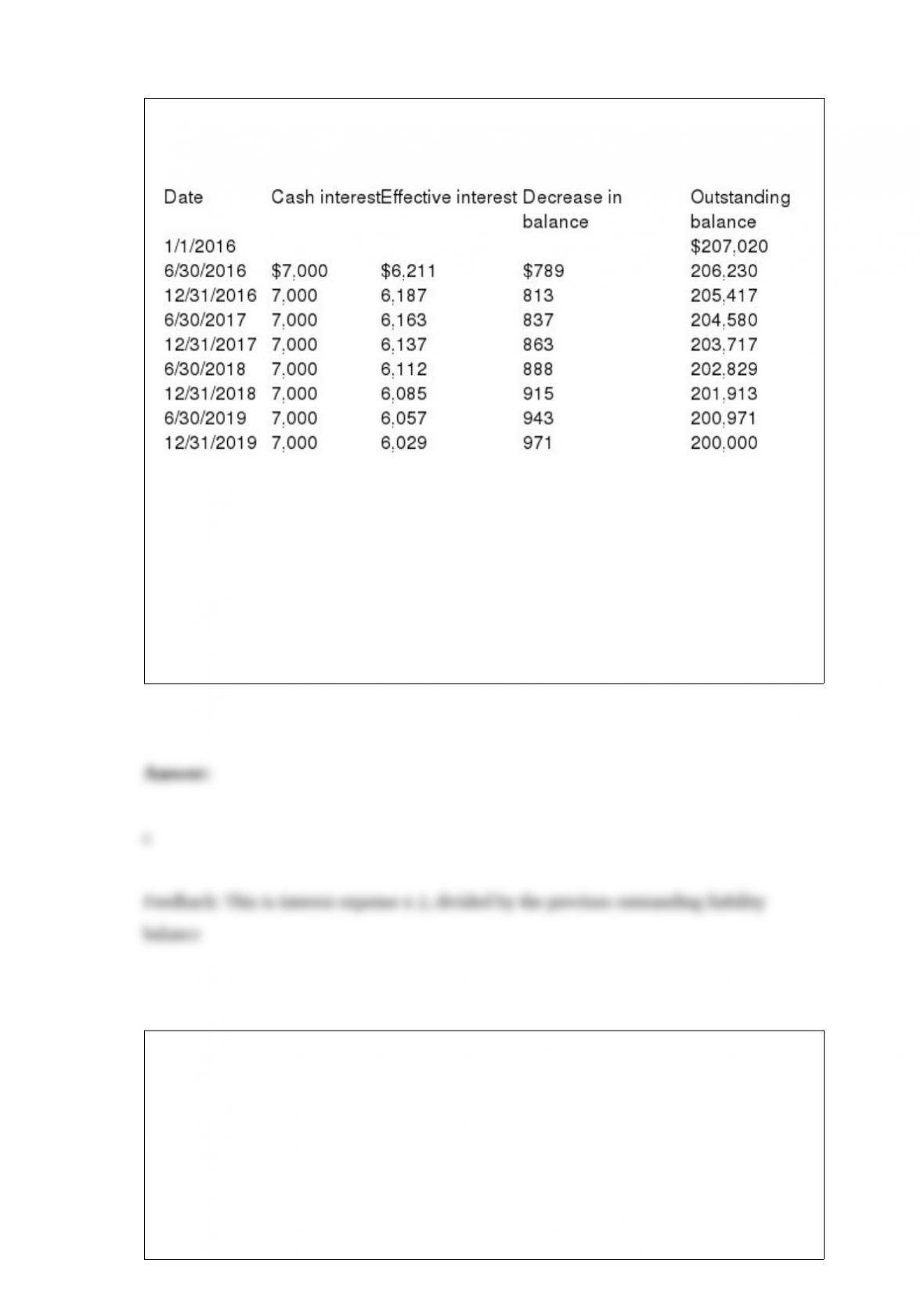

Lopez Plastics Co. (LPC) issued callable bonds on January 1, 2016. LPC’s accountant

has projected the following amortization schedule from issuance until maturity:

What is the annual effective interest rate on the bonds?

a. 3%

b. 3.5%

c. 6%

d. 7%

The compensation associated with executive stock option plans is:

a. The book value of a share of the company’s shares times the number of options.

b. The estimated fair value of the options.

c. Allocated to expense over the number of years until expiration.

d. Recorded as compensation expense on the date of grant.

How many acceptable approaches are there for changes in accounting principles?

a. One.

b. Two.

c. Three.

d. Four.

Which of the following usually results in an increase in a deferred tax liability?

a. Accrual of estimated operating expenses.

b. Revenue collected in advance.

c. Prepaid operating expenses, currently deductible.

d. All of these answer choices are correct.

The corporate charter sometimes is known as (a):

a. Articles of incorporation.

b. Statement of organization.

c. By-laws.

d. Registration statement.

Wilson Inc. owns equipment for which it paid $70 million. At the end of 2016, it had

accumulated depreciation on the equipment of $12 million. Due to adverse economic

conditions, Wilson’s management determined that it should assess whether an

impairment loss should be recognized for the equipment. The estimated undiscounted

future cash flows to be provided by the equipment total $60 million, and the

equipment’s fair value at that point is $50 million. Under these circumstances, Wilson:

a. Would record no impairment loss on the equipment.

b. Would record an $8 million impairment loss on the equipment.

c. Would record a $20 million impairment loss on the equipment.

d. None of these answer choices are correct.

On June 30, 2016, K Co. had outstanding 9%, $10,000,000 face value bonds maturing

on June 30, 2021. Interest is payable semiannually every June 30 and December 31. On

June 30, 2016, after amortization was recorded for the period, the unamortized bond

premium and bond issue costs were $60,000 and $100,000, respectively. On that date,

K acquired all its outstanding bonds on the open market at 98 and retired them. At June

30, 2016, what amount should K Co. recognize as gain on redemption of bonds before

income taxes?

a. $ 40,000.

b. $160,000.

c. $240,000.

d. $360,000.

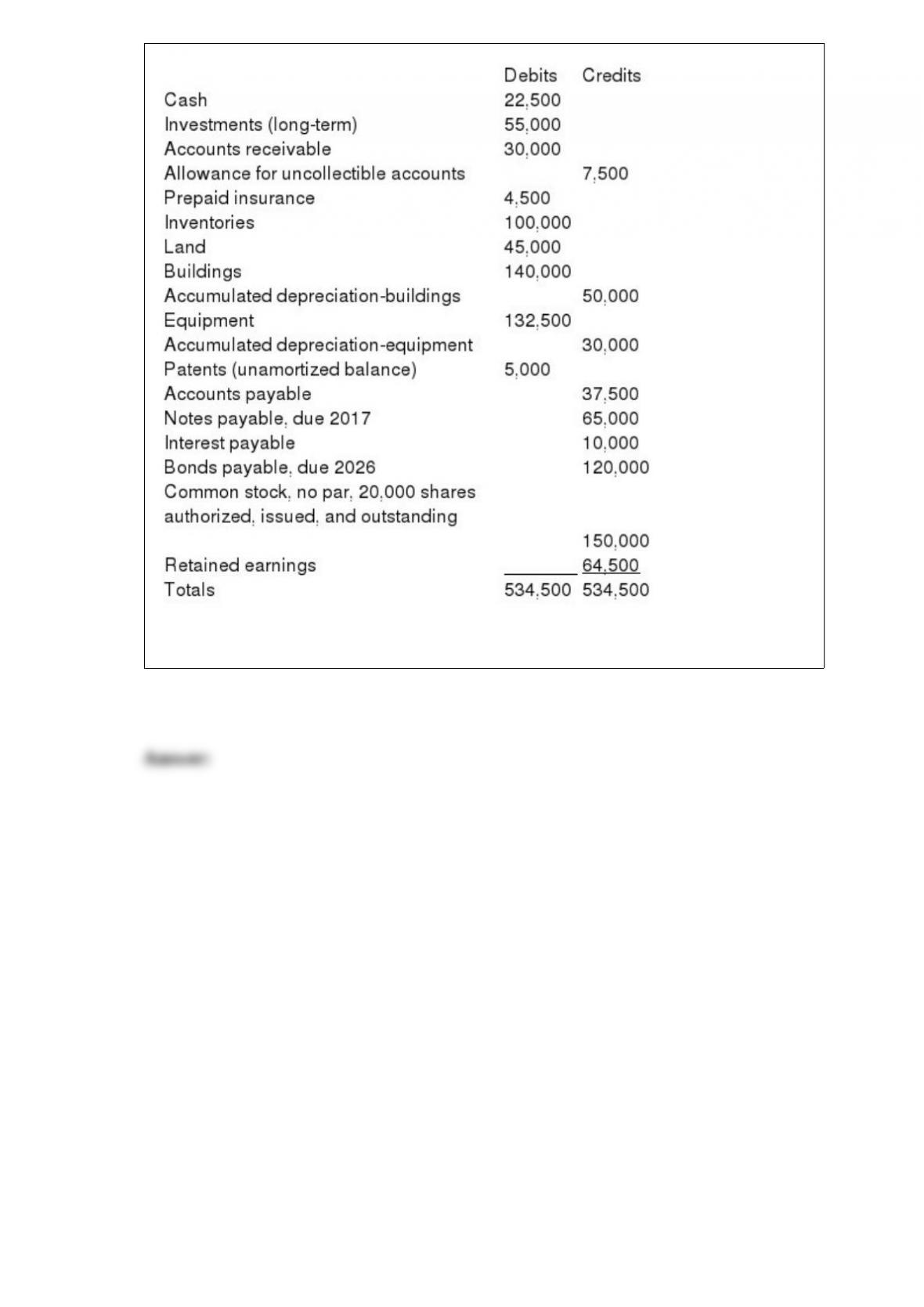

The December 31, 2016, post-closing trial balance ($ in thousands) for Libby

Corporation is presented below:

Required: Prepare a classified balance sheet for Libby Corporation at December 31,

2016.

On December 31, 2015, Jackson Company had 100,000 shares of common stock

outstanding and 30,000 shares of 7%, $50 par, cumulative preferred stock outstanding.

On February 28, 2016, Jackson purchased 24,000 shares of common stock on the open

market as treasury stock for $35 per share. Jackson sold 6,000 treasury shares on

September 30, 2016, for $37 per share. Net income for 2016 was $180,905. Also

outstanding during the year were fully vested incentive stock options giving key

personnel the option to buy 50,000 common shares at $40. The market price of the

common shares averaged $39 during 2016.

Required:

Compute Jackson’s basic and diluted earnings per share (rounded to 2 decimal places)

for 2016.

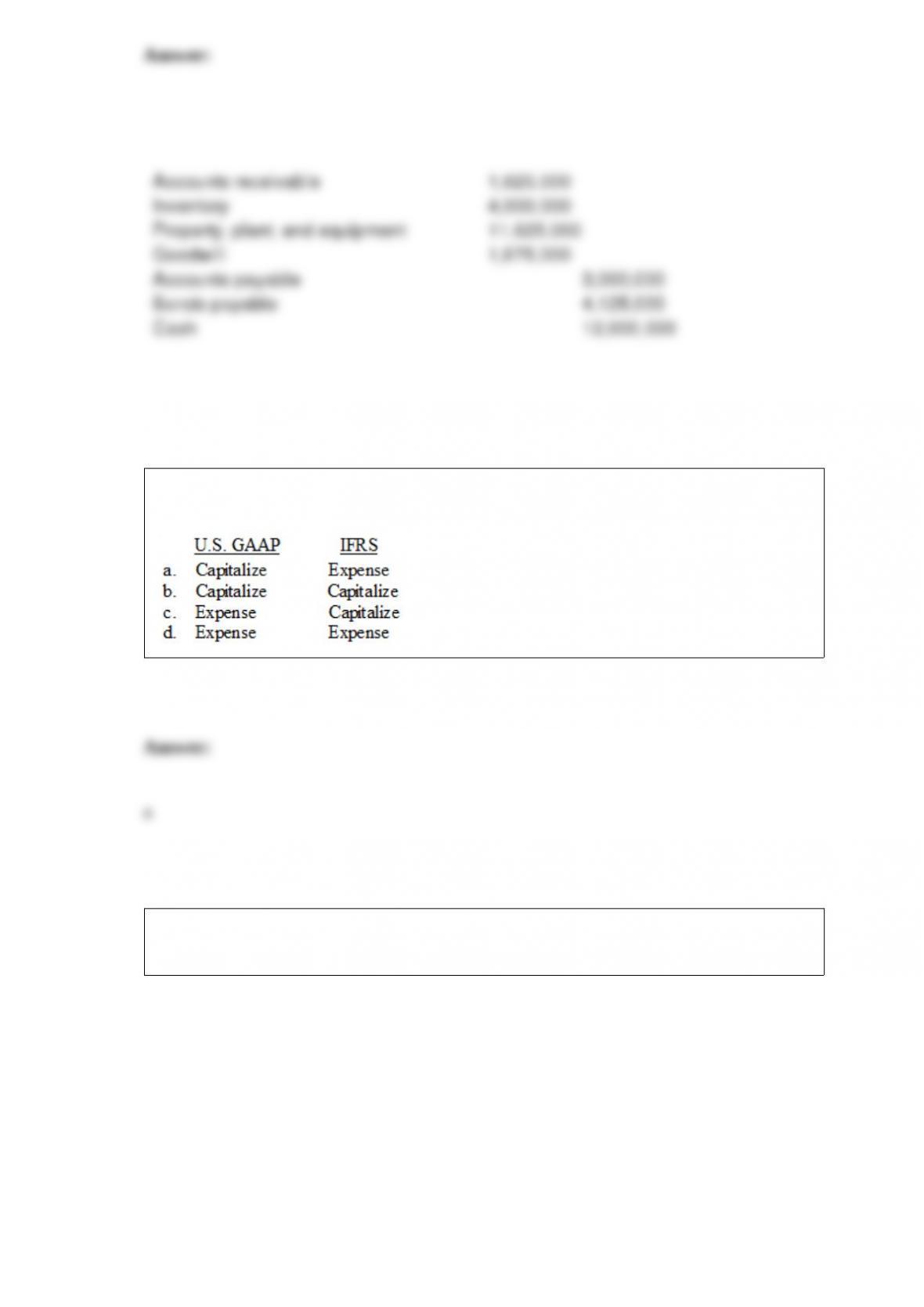

During the current year, Brewer Company acquired all of the outstanding common

stock of Miller Inc. paying $12,000,000 cash. The book values and fair values of

Miller’s assets and liabilities acquired are listed below:

Required:

Prepare the journal entry to record the acquisition by Brewer Company.

The normal treatment of litigation costs to successfully defend an intangible right under

U.S. GAAP and International Financial Reporting Standards (IFRS), respectively, is:

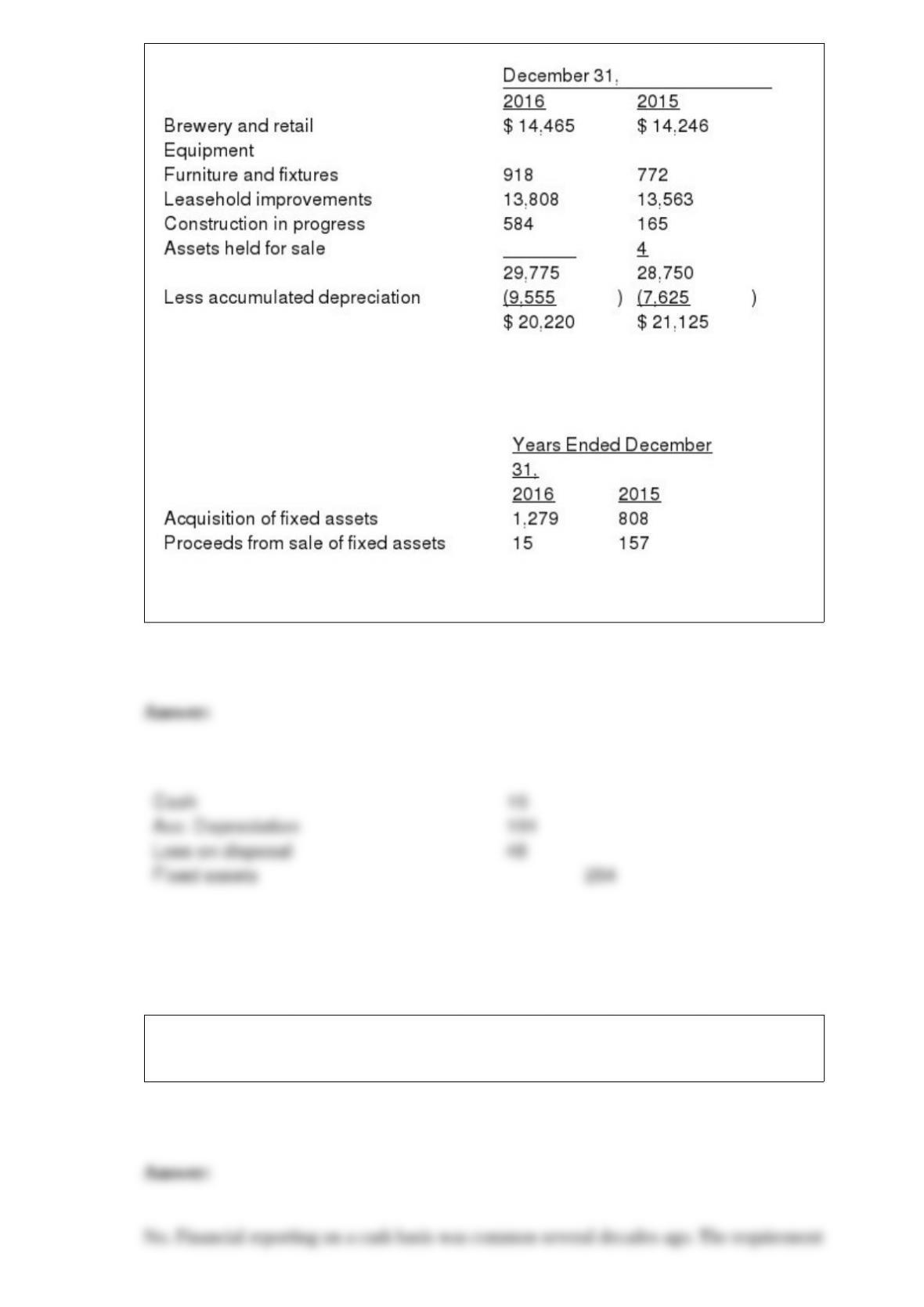

In its 2016 annual report to shareholders, Plank Breweries included the following note:

Fixed Assets Fixed assets consist of the following (in $ thousands):

Total depreciation expense was approximately $2.121 million and $2.179 million for

the years ended December 31, 2016 and 2015, respectively. Also, Plank Breweries

reported the following information in its annual report (in $ thousands):

Required: Show the journal entry to record Plank’s disposal of the fixed assets during

2016.

The statement of cash flows has been a required financial statement since 1988, but is

the reporting of cash flows a relatively new concept? Explain.

Woolery, Inc., had 50,000 shares of common stock outstanding at January 1, 2016. On

March 31, 2016, an additional 12,000 shares were sold for cash. Woolery also had

$4,000,000 of 6% convertible bonds outstanding throughout the year. The bonds are

convertible into 40,000 shares of common stock. Net income for the year was $350,000.

The tax rate is 35%.

Required: Compute basic and diluted earnings per share (rounded to 2 decimal places)

for the year ended December 31, 2016.

Incognito Company is contemplating the purchase of a machine that provides it with net

after-tax cash savings of $80,000 per year for five years. Interest is 8%. Assume the

cash savings occur at the end of each year.

Required: Calculate the present value of the cash savings.

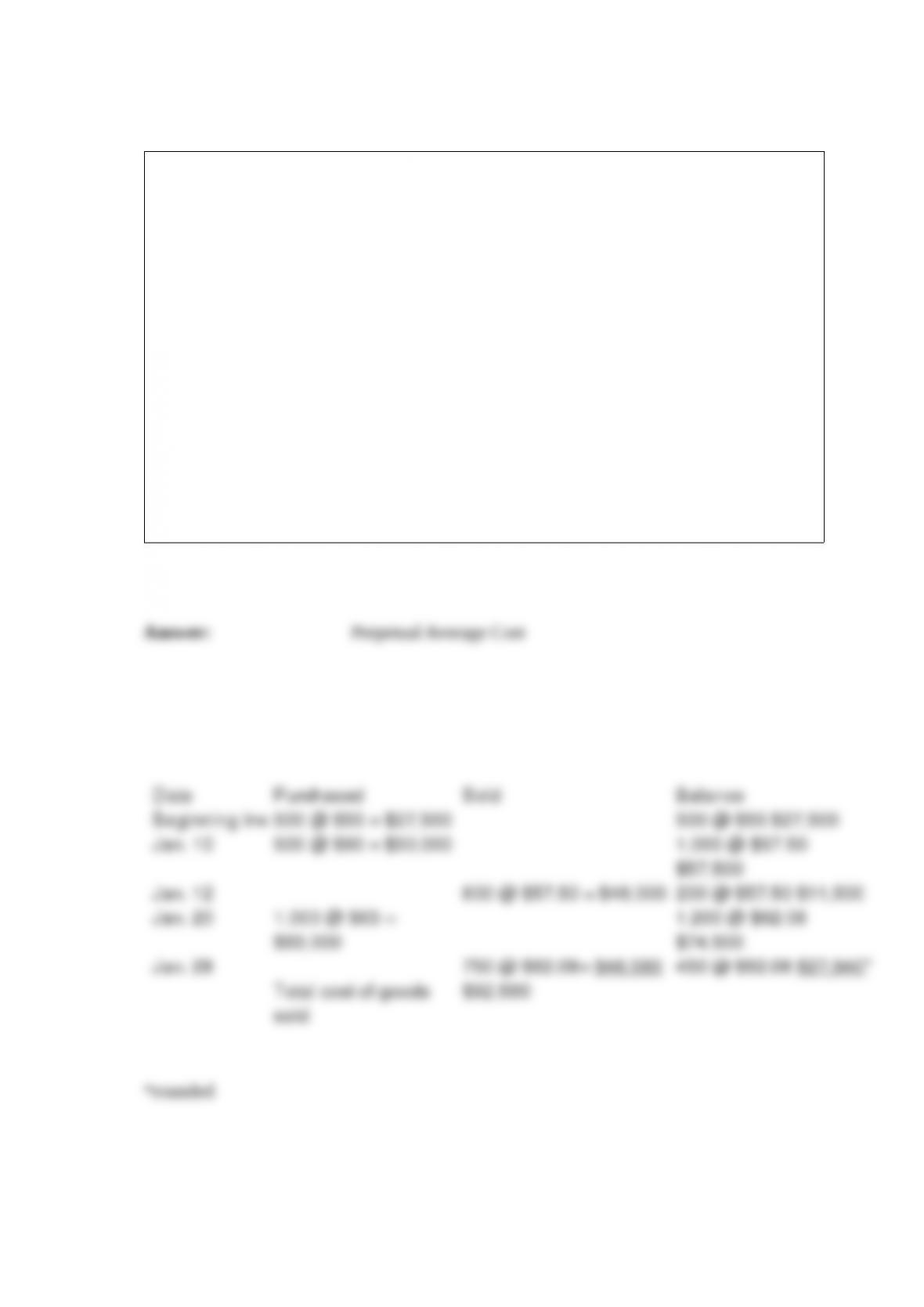

Shown below is activity for one of the products of Denver Office Equipment: January 1

balance, 500 units @ $55 $27,500

Purchases:

January 10: 500 units @ $60

January 20: 1,000 units @ $63

Sales:

January 12: 800 units

January 28: 750 units Required: Compute the January 31 ending inventory and cost of

goods sold for January, assuming Denver uses average cost and a perpetual inventory

system.