When the cost recovery method is used to account for a long-term construction contract

under IFRS, an equal amount of cost and revenue is typically recognized during the

early life of the contract, such that high initial gross profit is recognized in net income.

A company should accrue a liability for a loss contingency if it is at least reasonably

possible that assets have been impaired and the amount of potential loss can be

reasonably estimated.

Contract liability, deferred revenue and unearned revenue are all ways to describe a

liability that the seller recognizes with respect to unsatisfied performance obligations

for which the seller has already been paid.

The successful efforts method of accounting for oil and gas exploration costs allows

costs incurred in searching for oil and gas within a large geographical area to be

capitalized.

The FASB”s framework for measuring fair value doesn”t change the situations in which

fair value is used under current GAAP.

Biological assets are valued at fair value less estimated costs to sell under International

Financial Reporting Standards (IFRS).

In the United States the conceptual framework indicates GAAP when a more specific

accounting standard does not apply.

An option for a customer to purchase additional goods at a discount from list price is

always a performance obligation, because it confers a material right.

The criteria for determining which items comprise cash equivalents often is disclosed in

the summary of significant accounting policies.

The division’s book value and fair value less cost to sell on December 31 were

$3,000,000 and $2,500,000, respectively. What before-tax amount(s) should Mercedes

report as loss on discontinued operations in its 2016 income statement?

On October 28, 2016, Mercedes Company committed to a plan to sell a division that

qualified as a component of the entity according to GAAP regarding discontinued

operations and was properly classified as held for sale on December 31, 2016, the end

of the company’s fiscal year. The division’s loss from operations for 2016 was

$2,000,000. a. $2,000,000 loss.

b. $2,500,000 loss.

c. No loss would be reported.

d. $500,000 impairment loss included in continuing operations and a $2,000,000 loss

from discontinued operations.

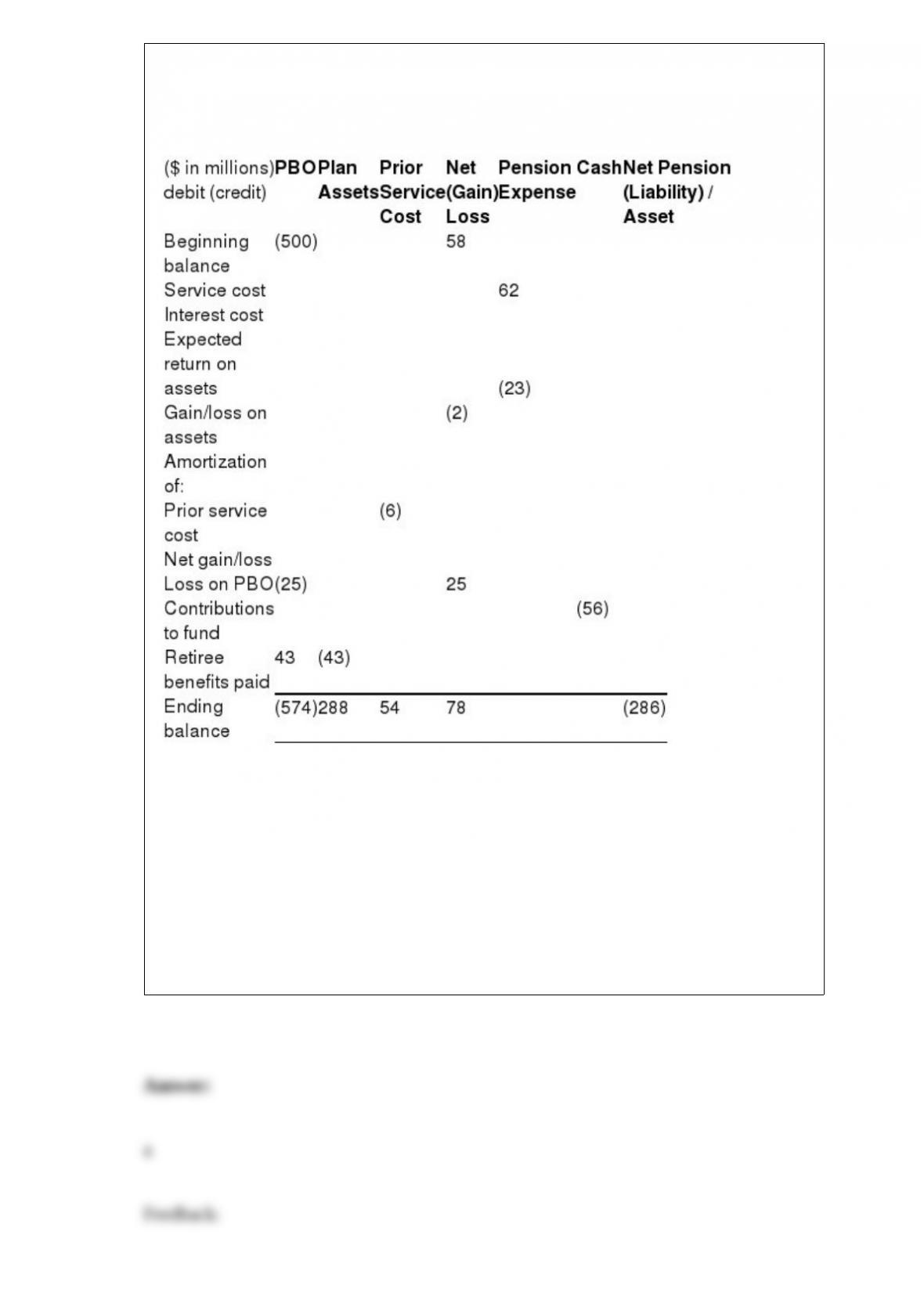

The following incomplete (columns have missing amounts) pension spreadsheet is for

Old Tucson Corporation (OTC).

What is OTC’s pension expense for the year?

a. $78.

b. $72.

c. $66.

d. $18.

Under IFRS, a deferred tax asset for stock options:

a. Is created for the cumulative amount of the fair value of the options the company has

recorded for compensation expense.

b. Is the portion of the options’ intrinsic value earned to date times the tax rate.

c. Is the tax rate times the amount of compensation.

d. Isn’t created if the award is “in the money;” that is, it has intrinsic value.

Puritan Corp. reported the following pretax accounting income and taxable income for

its first three years of operations:

Puritan’s tax rate is 40% for all years. Puritan elected a loss carryback.

As of December 31, 2016.Puritan was certain that it would recover the full tax benefit

of the

NOL that remained after the operating loss carryback.

What did Puritan report on December 31, 2016, as the deferred tax asset for the NOL

carryforward?

a. $280,000.

b. $200,000.

c. $100,000.

d. $ 0.

On January 1, 2016, Badger Inc. adopted the dollar-value LIFO method. The inventory

cost on this date was $100,000. The 2016 ending inventory, valued at year-end costs,

was $126,000. The relative cost index for this inventory in 2016 was 1.05. Suppose that

Badger’s 2018 ending inventory, valued at year-end costs, was $153,600 and that the

relative cost index for this inventory in 2018 was 1.20. What inventory balance would

Badger report on its 12/31/18 balance sheet?

a. $128,000.

b. $129,800.

c. $153,600.

d. None of these answer choices is correct.

On September 30, 2016, Bricker Enterprises purchased a machine for $200,000. The

estimated service life is 10 years with a $20,000 residual value. Bricker records

partial-year depreciation based on the number of months in service. Depreciation (to the

nearest dollar) for 2016, using sum-of-the-years’ digits, would be:

a. $ 9,091.

b. $24,545.

c. $27,273.

d. $ 8,182.

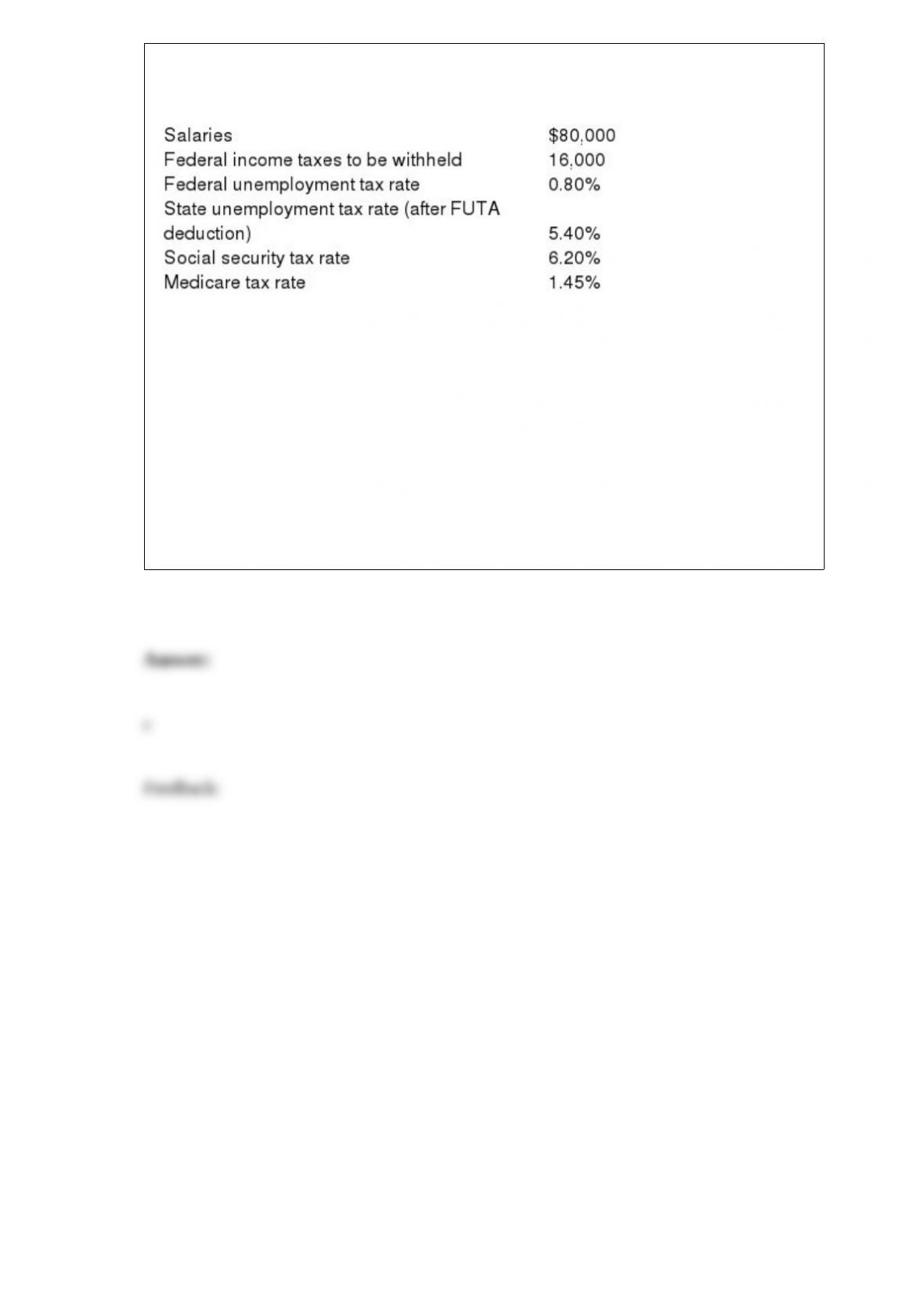

Barbara Muller Services (BMS) pays its employees monthly. The payroll information

listed below is for January 2016, the first month of BMS’s fiscal year.

The journal entry to record payroll for the January 2016 pay period will include a debit

to payroll tax expense of:

a. $ 6,120.

b. $ 4,960.

c. $11,080.

d. $57,880.

Listed below are 5 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term. 1> Long-term liabilities a. Obligations

payable in more than one year or longer than the operating cycle.

2> Current liabilities

3> Intangible asset b. Ownership of an exclusive right.

4> Current assets c. Items expected to be converted to cash or consumed within one

year or the operating cycle.

5> Property, plant, and equipment

d. Obligations payable within one year or the operating cycle.

e. Includes buildings and land used in operations.

Gerken Company concluded at the beginning of 2016 that the company’s ownership

interest in DillCo had increased to the point that it became appropriate to begin using

the equity method to account for the investment. The balance in the investment account

is $50,000 at the time of the change, and accountants working with company records

determined that the balance would have been $75,000 if the account had been adjusted

for investee net income and dividends as prescribed by the equity method. After

implementing the change to the equity method, if financial statements were prepared:

a. Net income and retained earnings will be higher by $25,000.

b. Net income will be unchanged, and retained earnings will be higher by $25,000.

c. Net income and retained earnings will be higher by $75,000.

d. The accounts will be unchanged, because no adjustment is necessary.

GAAP is an abbreviation for:

a. Generally authorized accounting procedures.

b. Generally applied accounting procedures.

c. Generally accepted auditing practices.

d. Generally accepted accounting principles.

Which of the following is not a change in reporting entity?

a. Reporting using comparative financial statements for the first time.

b. Changing the companies that comprise a consolidated group.

c. Presenting consolidated financial statements for the first time.

d. All are changes in reporting entity.

The net assets of a corporation are equal to:

a. Contributed capital.

b. Retained earnings.

c. Shareholders’ equity.

d. None of the above.

Which of the following causes a change in cash?

a. Accrual of interest payable.

b. Recording of depreciation expense.

c. Write-off of an uncollectible account.

d. Payment of a cash dividend declared in the previous fiscal year.

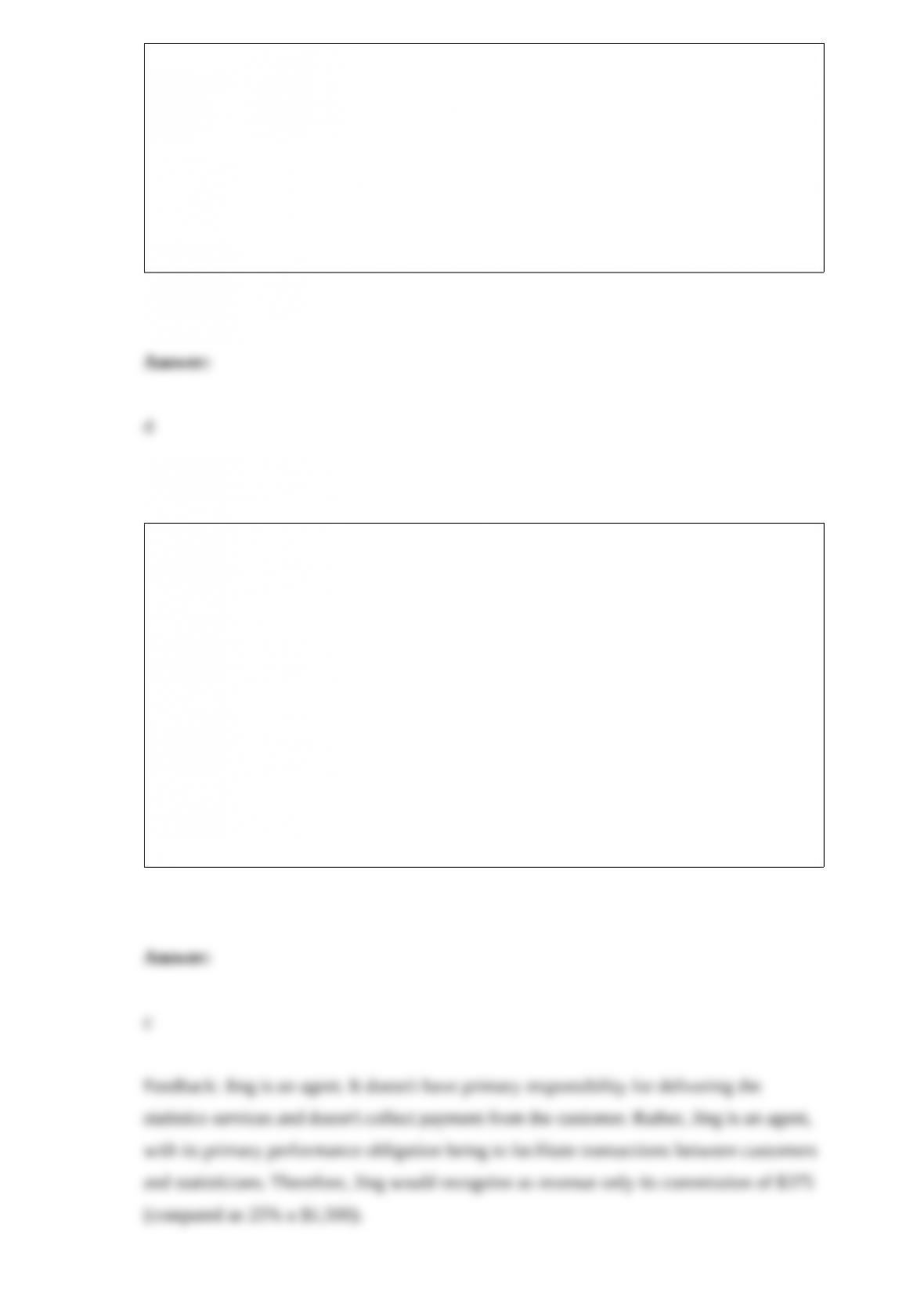

Jing Statistical Services operates a website that links experienced statisticians with

businesses that need data analyzed. Statisticians post their rates, qualifications, and

references on the website, and Jing receives 25% of the fee paid to the statisticians in

exchange for identifying potential customers. VetMed Associates contacts Jing and

arranges to pay a consultant $1,500 in exchange for analyzing some data. Jing’s income

statement would include the following with respect to this transaction:

a. Revenue of $1,500

b. Revenue of $1,500, and cost of services of $1,125

c. Revenue of $375

d. Revenue of $1,875 and cost of services of $1,500

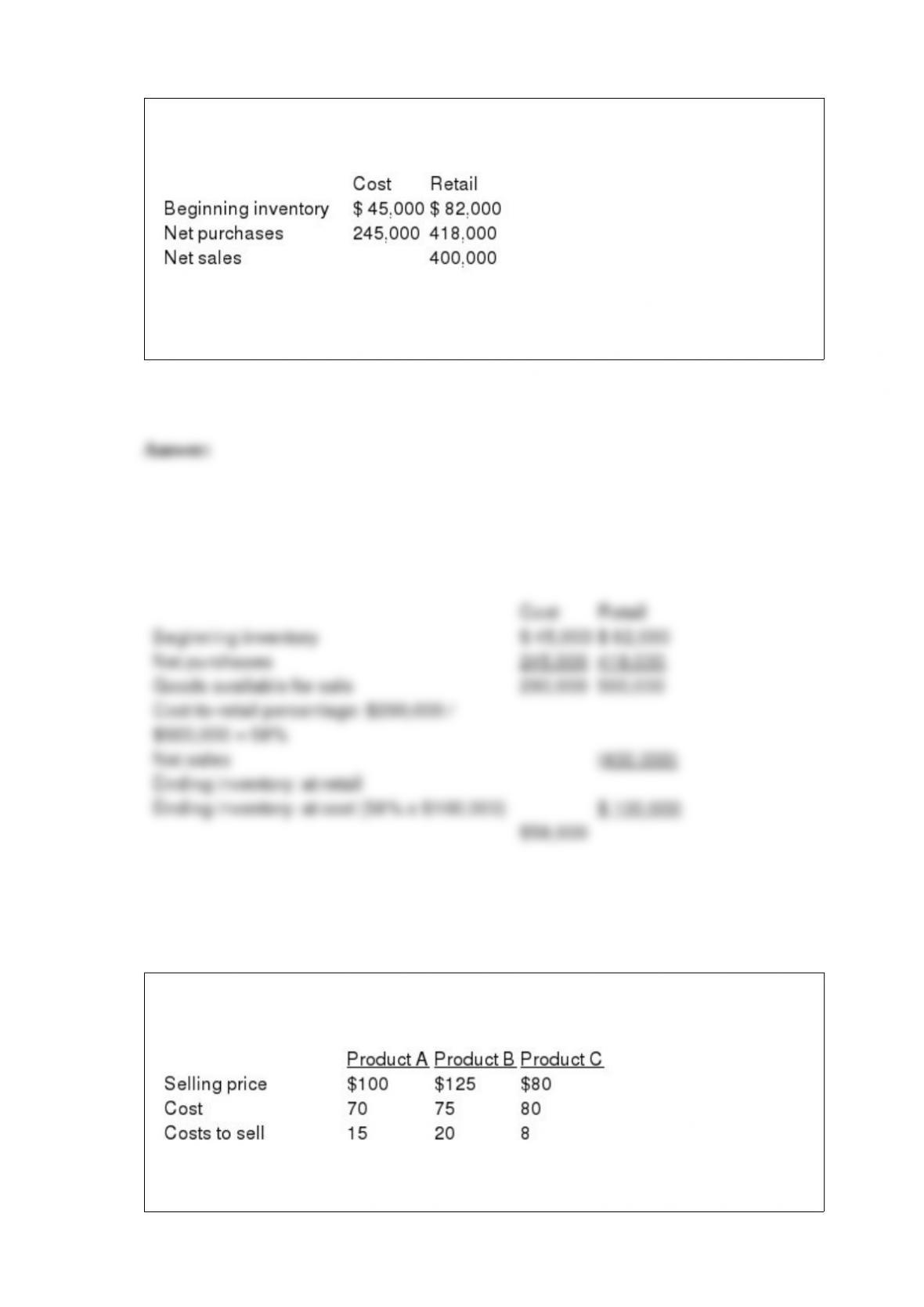

Andover Stores uses the average cost retail method to estimate its ending inventory.

Information as of June 30, 2016, is as follows:

Required:

Use the retail method to estimate the June 30, 2016, inventory.

Memphis Wholesale Market applies the lower of cost and net realizable valuation to

individual products and has collected the following data:

Determine the inventory book value for Products A, B, and C.

ABC Company will issue $5,000,000 in 6%, 10-year bonds when the market rate of

interest is 8%. Interest is paid semiannually.

Required: Determine how much cash ABC Company will realize from the bond issue.

At December 31, 2016, Cordova Leather’s liabilities include the following:

1> $15 million of noncallable 9% notes were issued for $15 million on August 31,

1994. The notes mature on July 31, 2017. Sufficient cash is expected to be available to

retire the notes at maturity.

2> $30 million of 8% notes were issued for $30 million on May 31, 2012. The notes

mature on May 31, 2022, but investors have the option of calling (demanding payment

on) the notes on June 30, 2017. However, the call option is not expected to be

exercised, given prevailing market conditions.

3> $18 million of 10% notes are due on March 31, 2018. A debt covenant requires

Cordova to maintain current assets at least equal to 150% of its current liabilities. On

December 31, 2016, Cordova is in violation of this covenant. Cordova obtained a

waiver from Village Bank until June 2017, having convinced the bank that the

company’s normal 2 to 1 ratio of current assets to current liabilities will be reestablished

during the first half of 2017. Required:

For each of the three liabilities, indicate the portion of the debt that can be excluded

from classification as a current liability (that is, reported as a noncurrent liability).

Explain.

IFRS No. 9 is a standard that indicates accounting for investments when the investor

does not have significant influence under the investee. Required:

Explain how debt investments are accounted for under IFRS No. 9. What alternative

accounting approaches are available, what determines whether an investment qualifies

for each approach, and what are the key features of each approach with respect to

accounting for unrealized gains and losses?

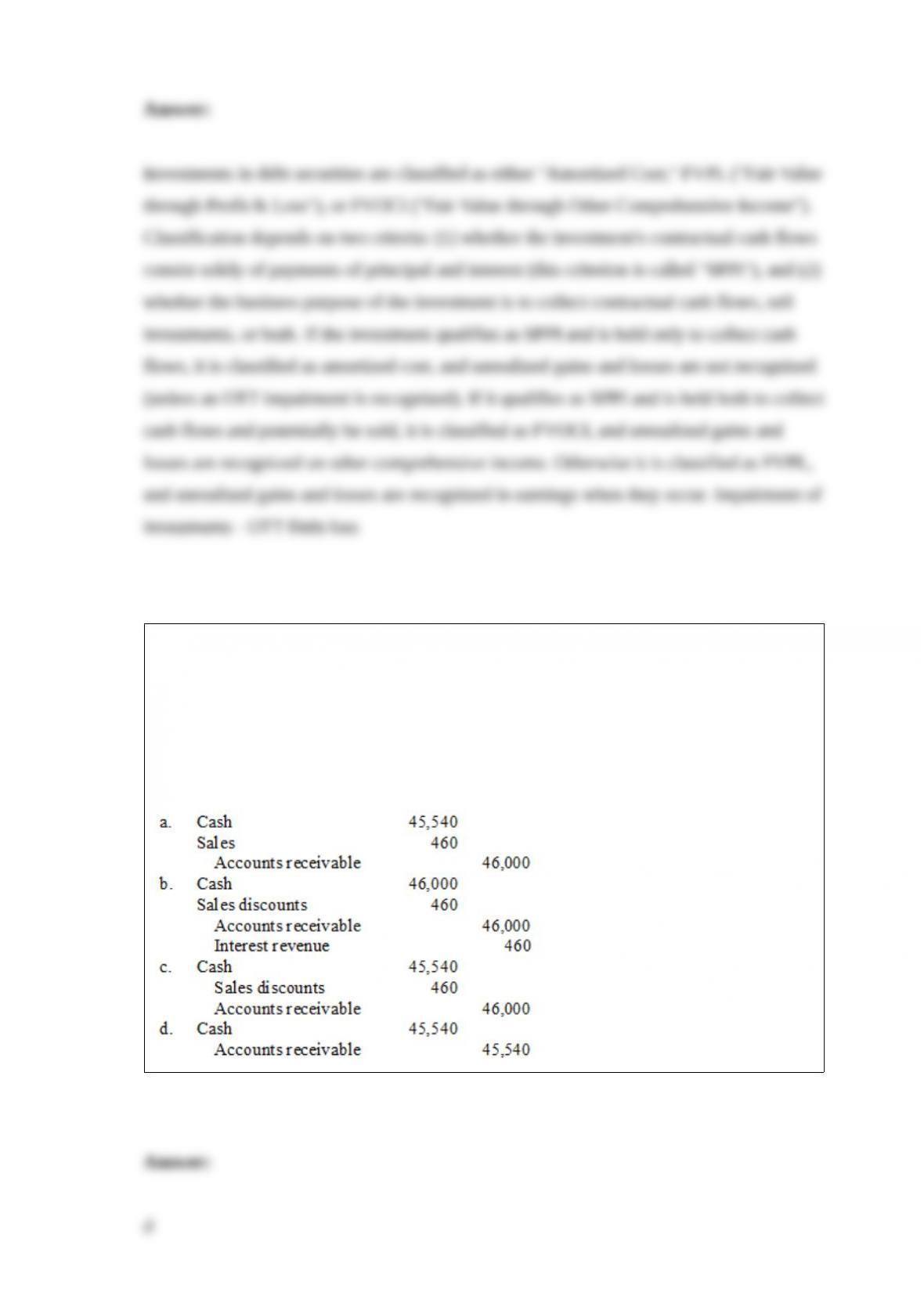

Harvey’s Wholesale Company sold supplies of $46,000 to Northeast Company on April

12 of the current year, with terms 1/15, n/60. Harvey uses the net method of accounting

for cash discounts.

What entry would Harvey’s make on April 23, assuming the customer made the correct

payment on that date?

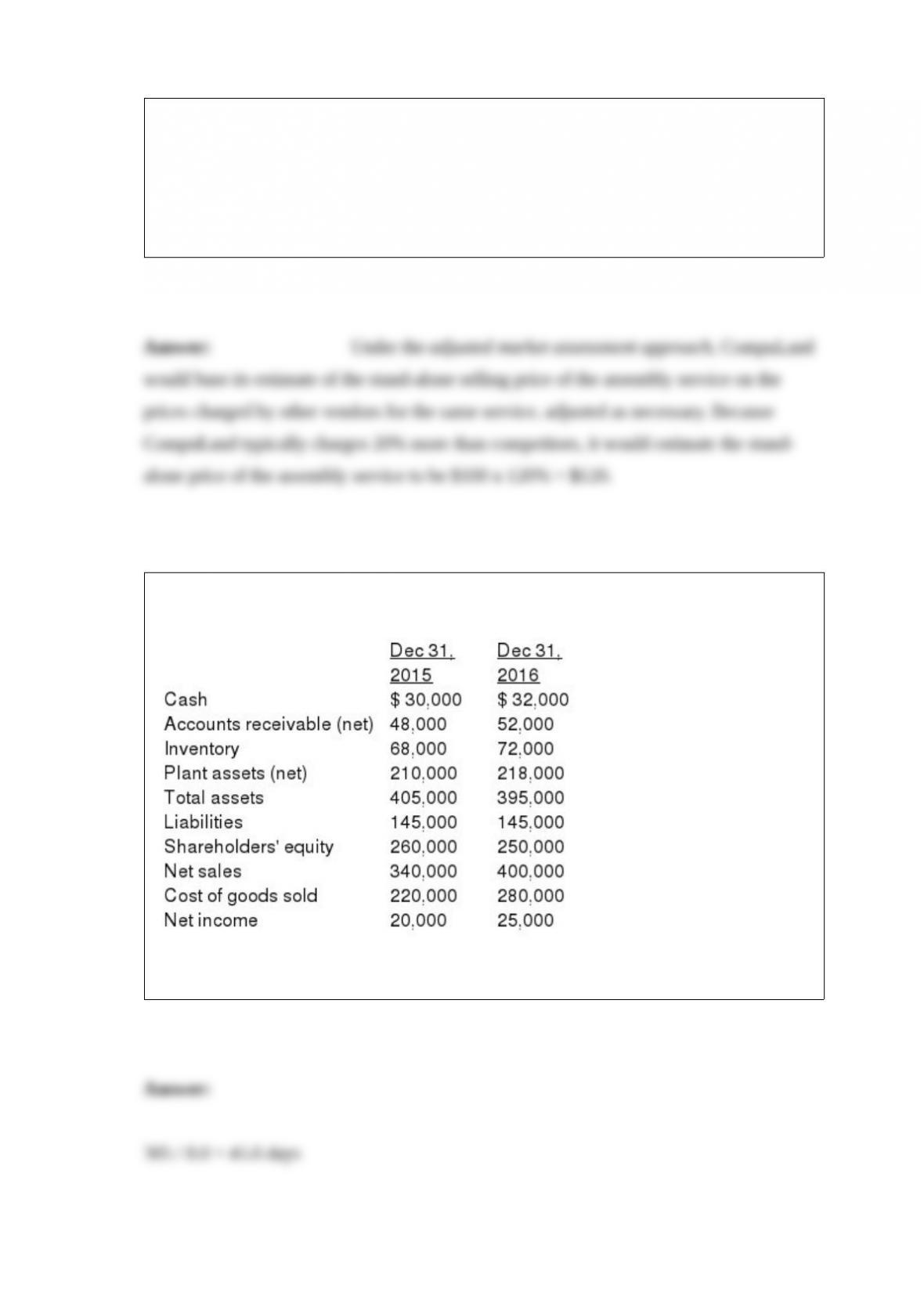

CompuLand Center sells a full assortment of computer parts, including motherboards,

video cards, and cables, and also offers complementary computer assembly services.

The assembly service is offered by other vendors for $100 on average, and CompuLand

typically charges approximately 20% more than other vendors for similar services on a

stand-alone basis. Required: Estimate the stand-alone selling price of the assembly

service using the adjusted market assessment approach.

Missoula Inc. reported the following selected financial statement data:

Required: Compute the average collection period (rounded to one decimal place) for

2016.

L Company discovered that a three-year insurance premium payment of $240,000 one

year ago was debited to insurance expense.

Required:

1) What action is required? Ignore taxes.

2) What action is required if the error is not discovered until four years after it

occurred?

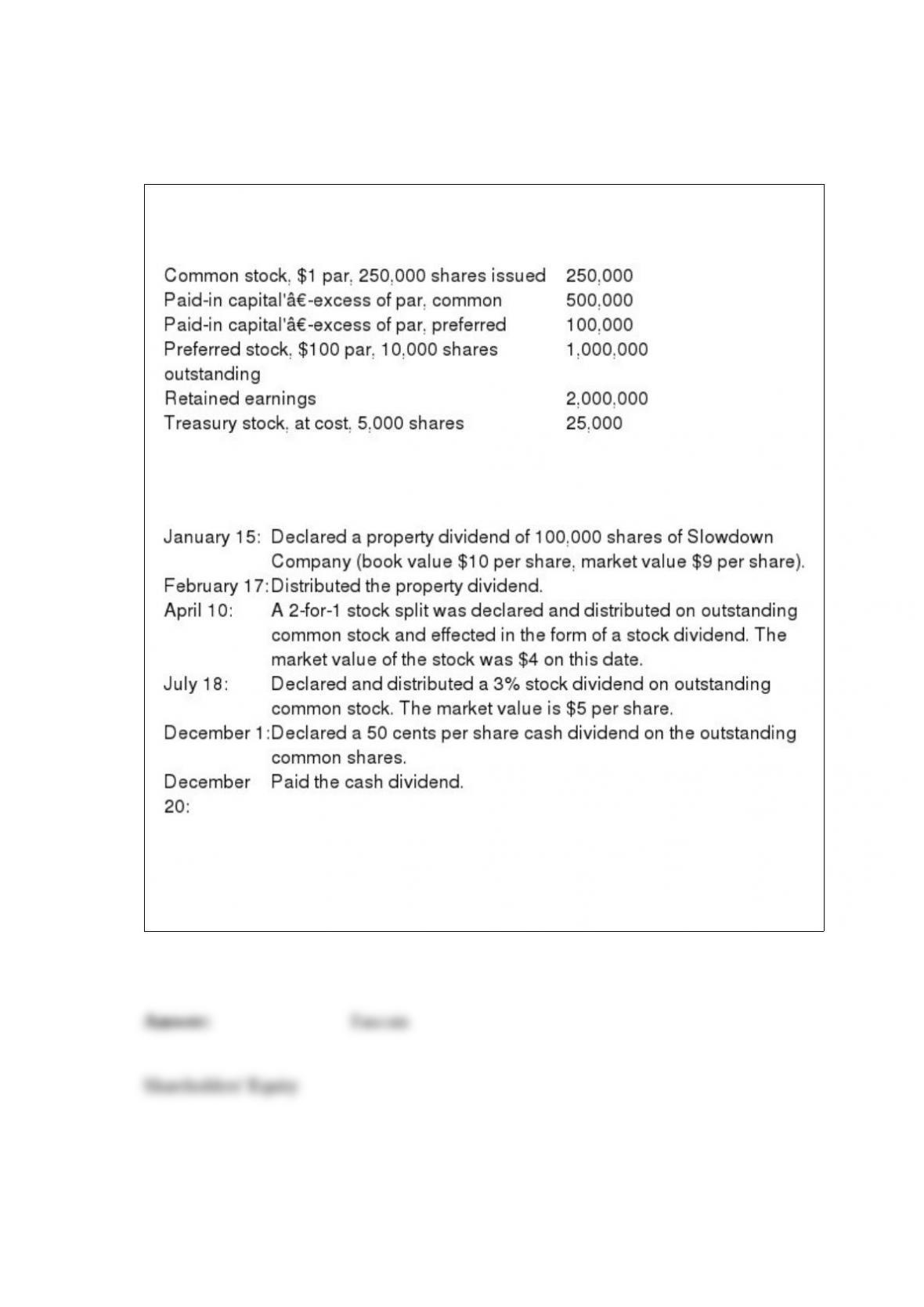

On January 1, 2016, Fascom had the following account balances in its shareholders’

equity accounts.

During 2016, Fascom Inc. had several transactions relating to common stock.

Required:

Without preparing journal entries, prepare the shareholders’ equity section of Fascom’s

balance sheet as of December 31, 2016. Assume net income is $500,000 for 2016.