An asset for a gain contingency should not be accrued unless it is probable that the gain

contingency will be realized.

All current assets are either cash or assets that will be converted into cash or consumed

within 12 months or the operating cycle, whichever is longer.

Capital leases are agreements that are formulated outwardly as leases, but are

installment purchases in substance.

FIFO periodic and FIFO perpetual always produce the same dollar amounts for cost of

goods sold.

Amortization of discount on bonds payable results in interest expense that is less than

the actual cash outflow.

No allocation of contract price is required if the transaction involves multiple

performance obligations that are satisfied at different points in time.

Intraperiod tax allocation is the process of associating income tax effects with the

income statement components that create those effects.

Statutory depletion is the maximum amount of depletion that may be reported in

financial statements prepared according to GAAP.

In a statement of cash flows prepared under International Financial Reporting

Standards, interest paid is most often classified as a financing cash flow.

The journal entry to record the replenishment of a petty cash fund includes a credit to

the petty cash fund.

Advocates of accelerated depreciation methods argue that their use tends to level out

the total cost of ownership of an asset over its benefit period if one considers both

depreciation and repair and maintenance costs.

Owners’ equity can be expressed as assets minus liabilities.

Initial franchise fees are always recognized on the date they are received.

Given identical current amounts owed and identical interest rates, annual payments of

an ordinary annuity will be greater than annual payments of an annuity due.

Which of the following does not pertain to accounting for asset retirement obligations?

a. They accrete (increase over time) at the company’s credit-adjusted risk-free rate.

b. They must be recognized according to GAAP.

c. Statement of Financial Accounting Concepts No. 7 is applied when adjusting cash

flow obligations for uncertainty.

d. All of these answer choices pertain to accounting for asset retirement obligations.

When treasury stock is sold at an amount less than its cost, the sale is classified as:

a. A financing activity.

b. An operating activity.

c. A financing activity and an operating activity.

d. An investing activity.

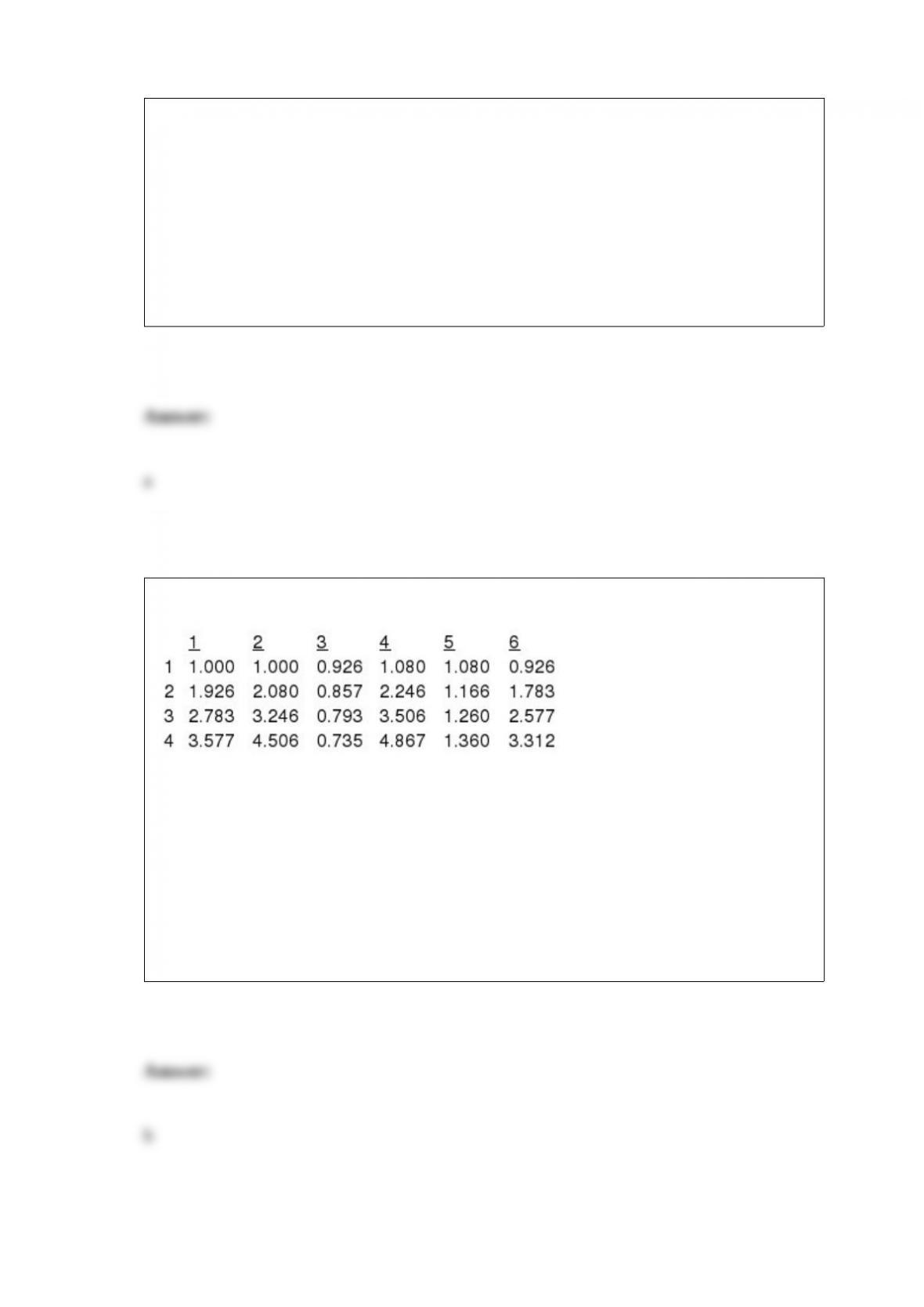

Below are excerpts from time value of money tables for the 8% rate.

Column 2 is an interest table for the:

a. Present value of an ordinary annuity of 1.

b. Future value of an ordinary annuity of 1.

c. Present value of an annuity due of 1.

d. Future value of an annuity due of 1.

California Inc., through no fault of its own, lost an entire plant due to an earthquake on

May 1, 2016. In preparing its insurance claim on the inventory loss, the company

developed the following data: Inventory January 1, 2016, $300,000; sales and purchases

from January 1, 2016, to May 1, 2016, $1,300,000 and $875,000, respectively.

California consistently reports a 40% gross profit. The estimated inventory on May 1,

2016, is:

a. $302,500.

b. $360,000.

c. $395,000.

d. $455,000.

If the lessor records deferred rent revenue at the beginning of a lease term, the lease

must:

a. Be a direct financing lease.

b. Be a sales-type lease.

c. Contain a bargain renewal option.

d. Be an operating lease.

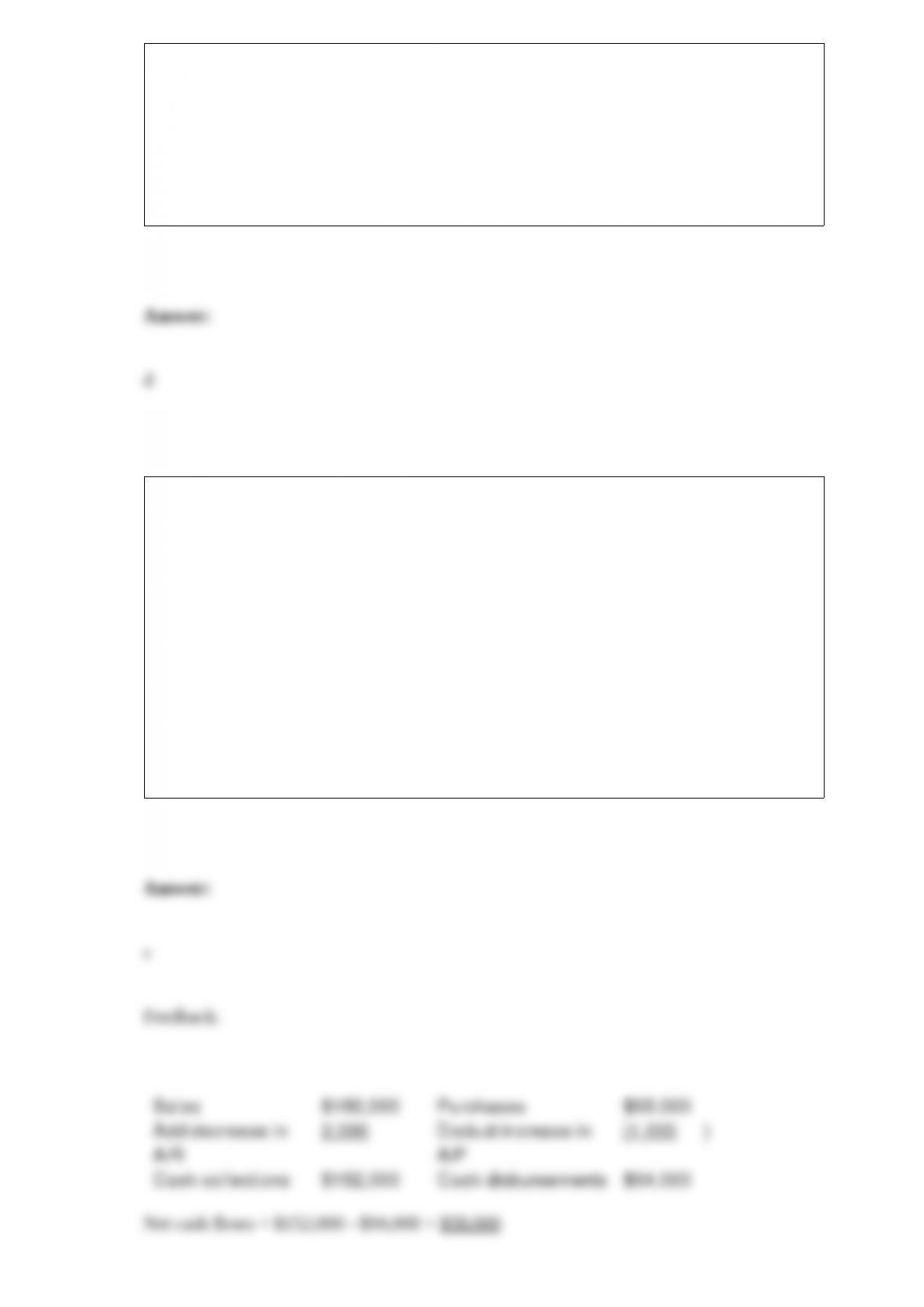

The Hamada Company sales for 2016 totaled $150,000 and purchases totaled $95,000.

Selected January 1, 2016, balances were: accounts receivable, $18,000; inventory,

$14,000; and accounts payable, $12,000. December 31, 2016, balances were: accounts

receivable, $16,000; inventory, $15,000; and accounts payable, $13,000. Net cash flows

from these activities were:

a. $45,000.

b. $55,000.

c. $58,000.

d. $74,000.

Authorized common stock refers to the total number of shares:

a. Outstanding.

b. Issued.

c. Issued and outstanding.

d. That can be issued.

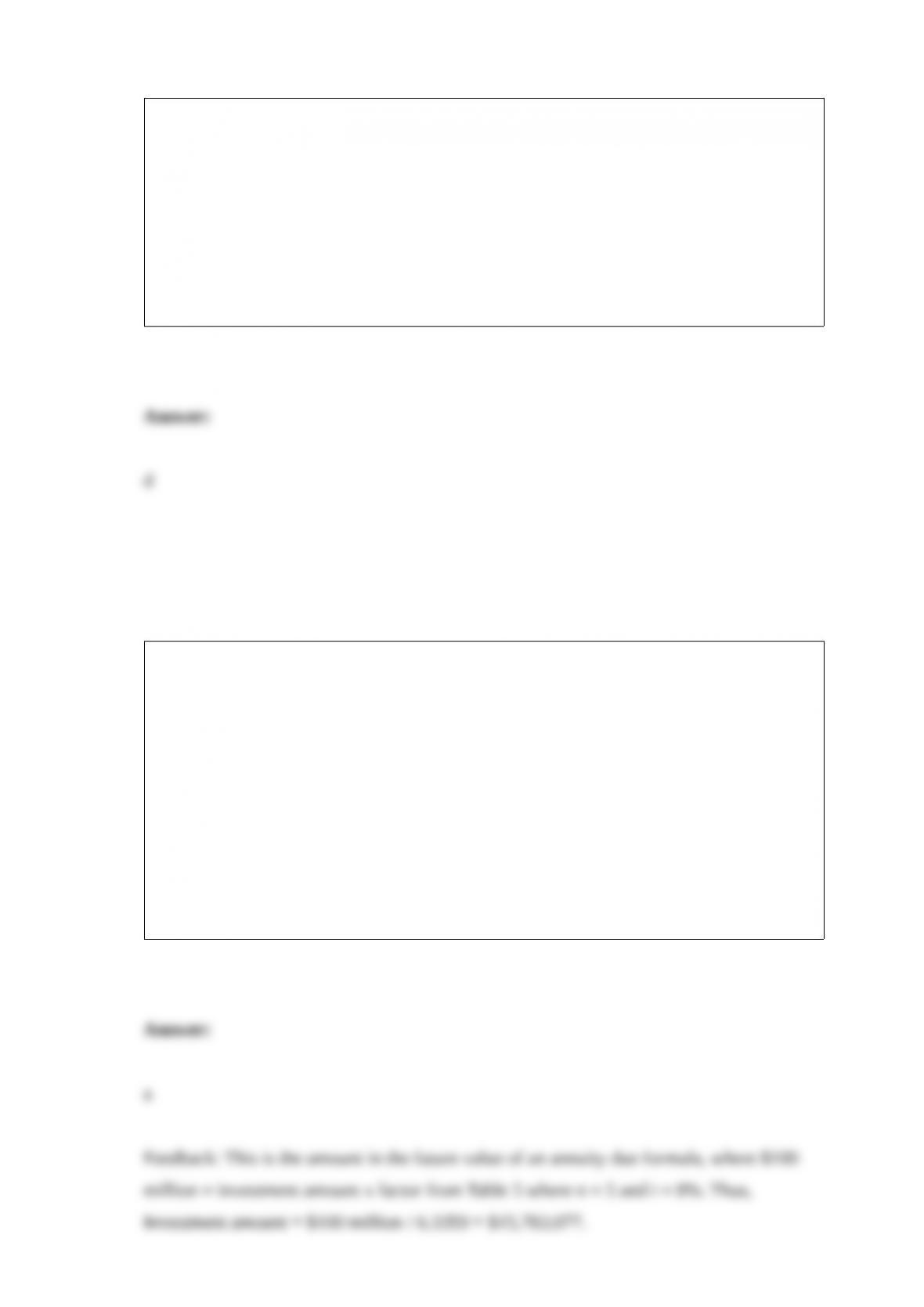

Fenland Co. plans to retire $100 million in bonds in five years, so it wishes to create a

fund by making equal investments at the beginning of each year during that period in an

account it expects to earn 8% annually. What amount does Fenland need to invest each

year?

a. $15,783,077.

b. $17,045,650.

c. $23,190,400.

d. Cannot be determined from the given information.

A gain from changing an estimate regarding the obligation for pension plans will:

a. Increase assets.

b. Increase liabilities.

c. Decrease shareholders’ equity.

d. Increase shareholders’ equity.

Gabriel Company views share buybacks as treasury stock. In its first treasury stock

transaction, Gabriel purchased treasury stock for more than the price at which the stock

was originally issued. What is the effect of the purchase of the treasury stock on each of

the following?

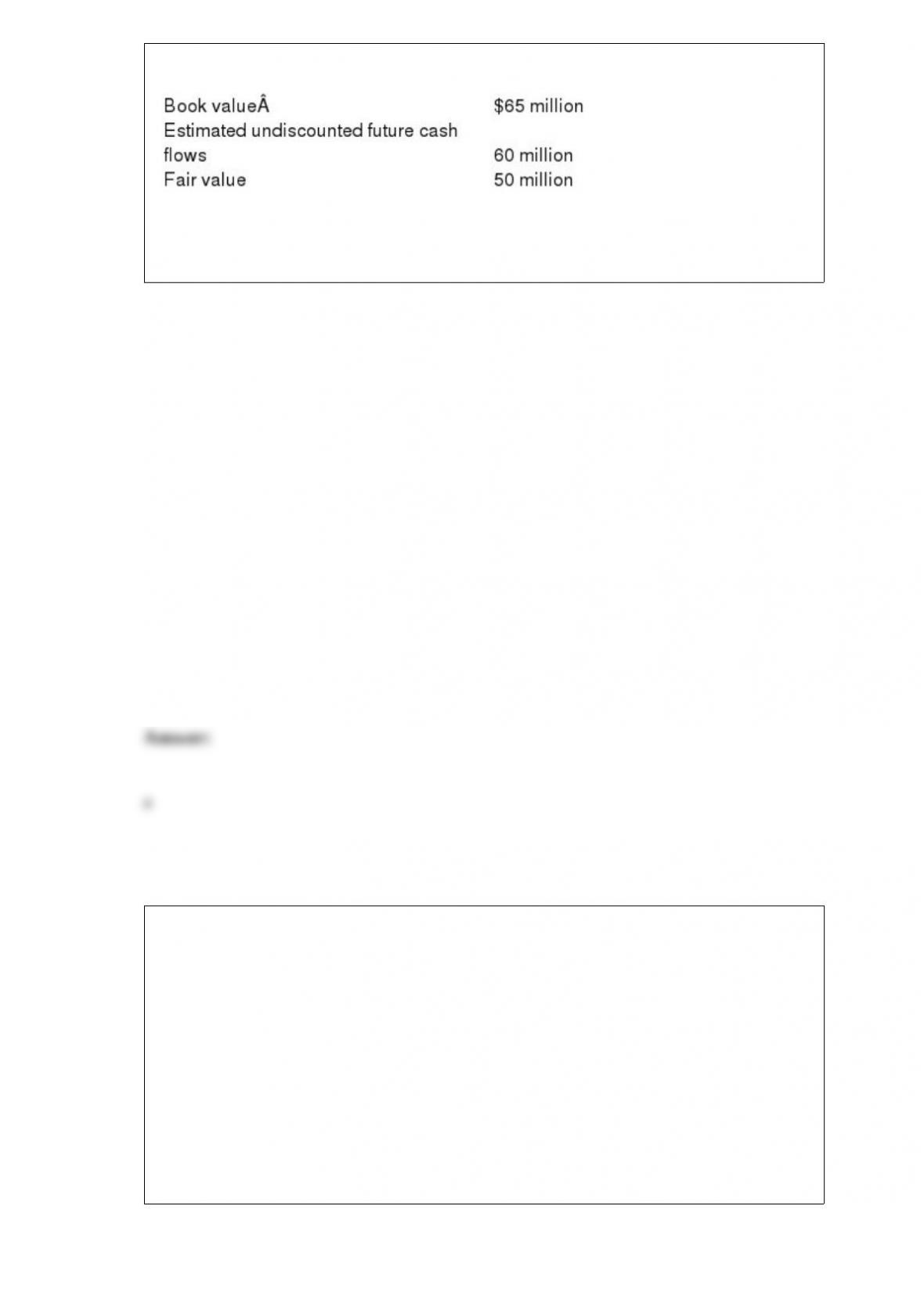

At the end of its 2016 fiscal year, a triggering event caused Janero Corporation to

perform an impairment test for one of its manufacturing facilities. The following

information is available:

The manufacturing facility is:

a. Impaired because its book value exceeds undiscounted future cash flows.

•

Not impaired because its book value exceeds undiscounted future cash flows.

•

•

Not impaired because it continues to produce revenue.

•

d. Impaired because its book value exceeds fair value.

On December 31, 2016, Tiras Company reported net income of $50,000 and sales of

$200,000. The company also reported beginning and ending accounts receivable at

$20,000 and $25,000, respectively. Tiras will report cash collected from customers in its

2016 statement of cash flows (direct method) in the amount of:

a. $0.

b. $245,000.

c. $205,000.

d. $195,000.

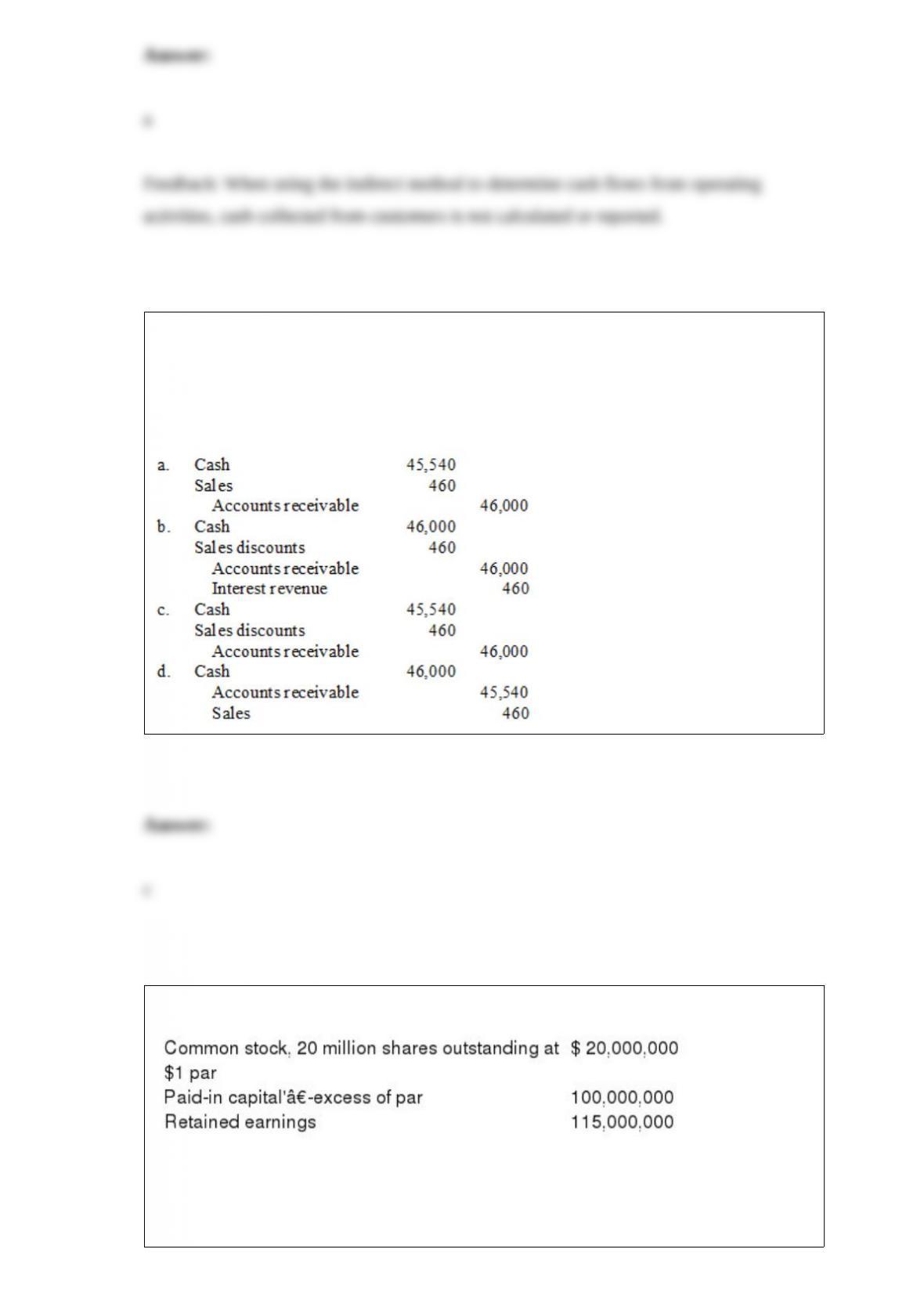

Oswego Clay Pipe Company sold $46,000 of pipe to Southeast Water District #45 on

April 12 of the current year with terms 1/15, n/60. Oswego uses the gross method of

accounting for cash discounts. What entry would Oswego make on April 23, assuming

the customer made the correct payment on that date?

The December 31, 2016, balance sheet of MBI Company included the following:

MBI completed the following transactions in 2016 relating to treasury stock:

March 17: Reacquired 2 million shares at $10.

May 17: Reacquired 2 million shares at $9.

August 10: Issued 3 million shares at $12.

Required:

Assuming MBI uses the cost method, prepare journal entries to record the foregoing

transactions on a weighted average basis.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

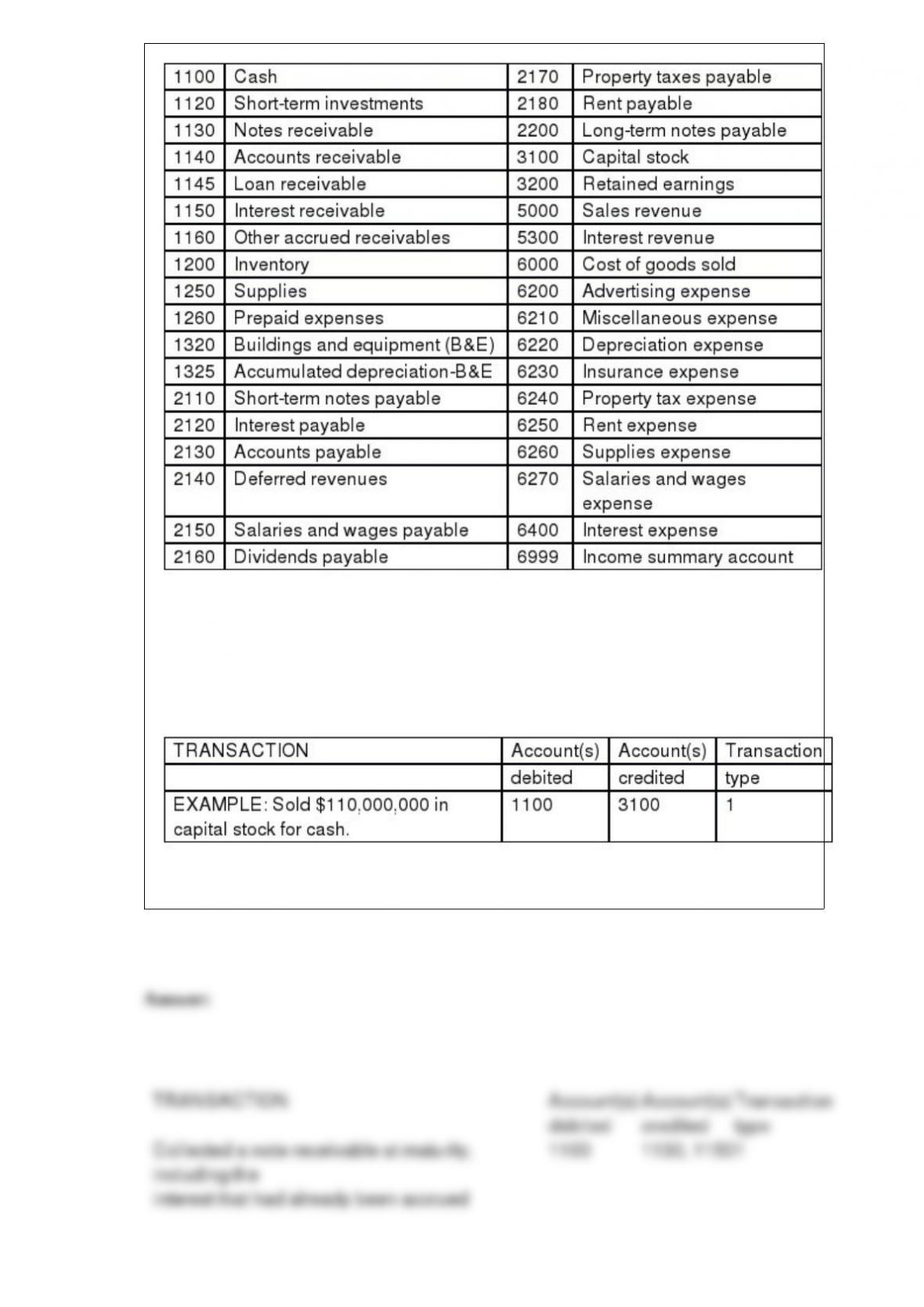

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Collected a note receivable at maturity, including the interest that had already been

accrued.

() What net effect would the valuation of these stock investments have on 2015 net

income? On 2016 net income?

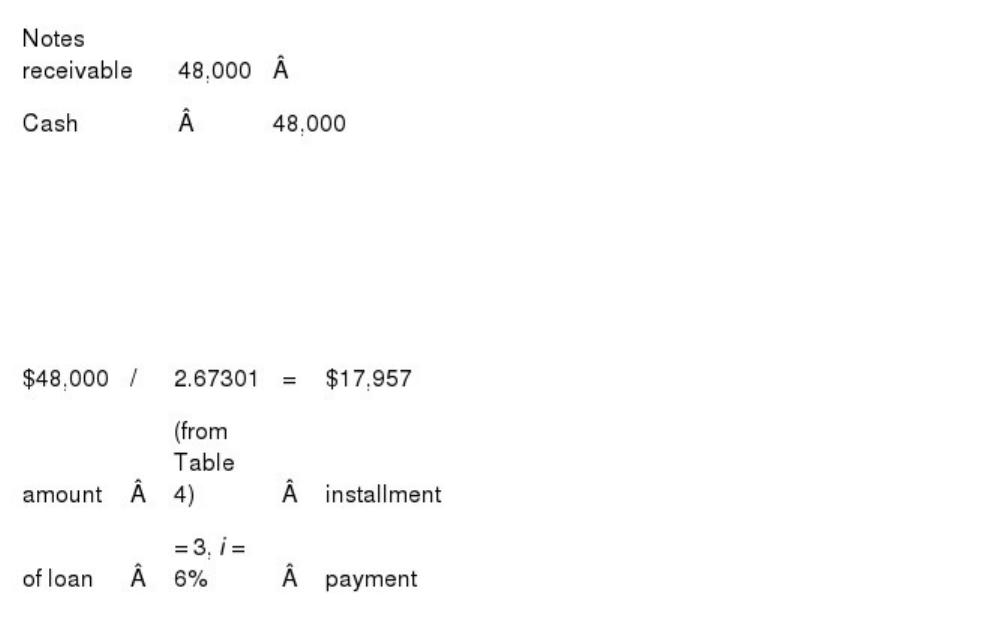

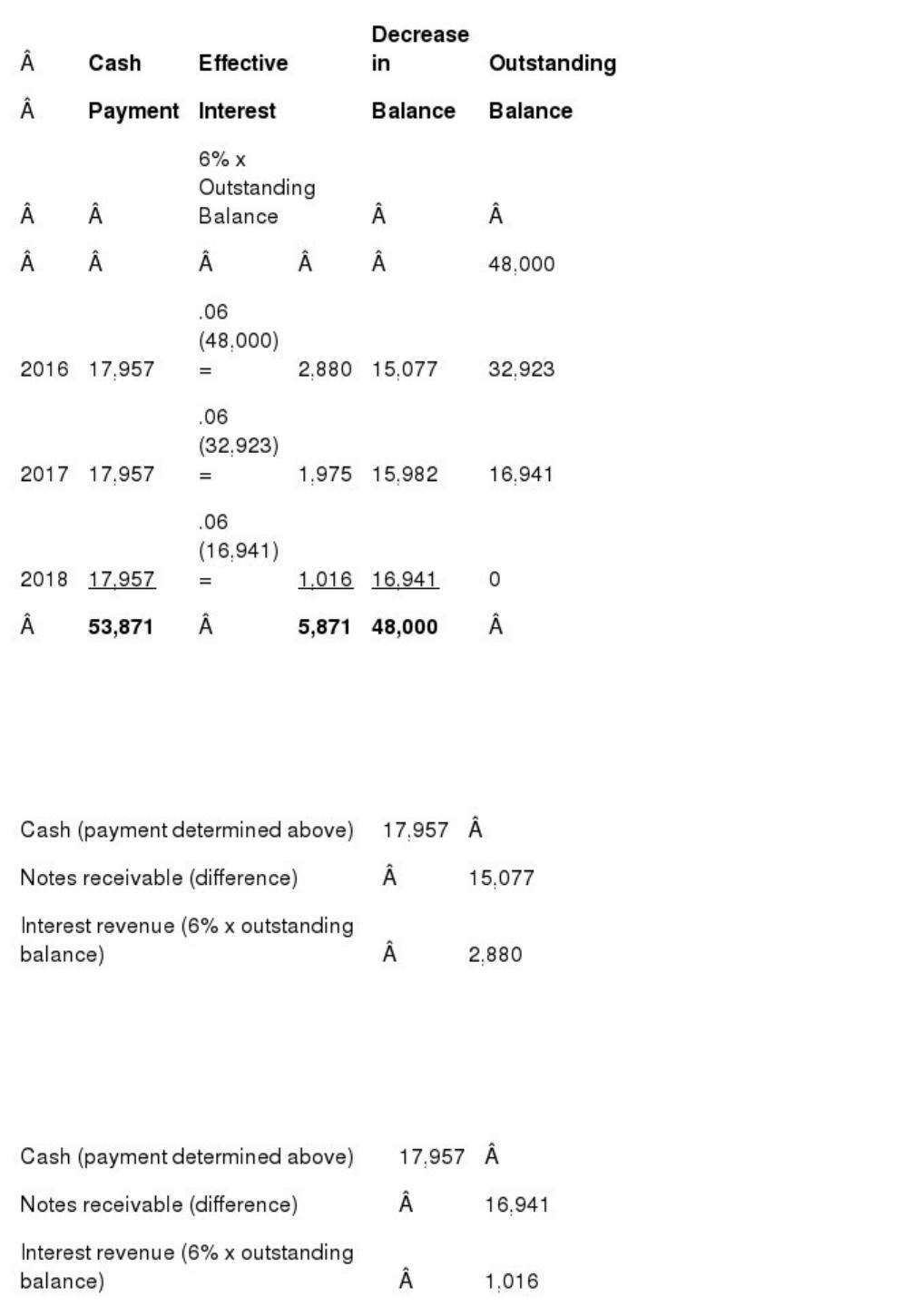

Little Company borrowed $48,000 from Sockets on January 1, 2016, and signed a

three-year, 6% installment note to be paid in three equal payments at the end of each

year. The present value of an ordinary annuity of $1 for 3 periods at 6% is 2.67301.

Required:

(1.) Prepare the journal entry on January 1, 2016, for Sockets’ lending the funds.

(2.) Calculate the amount of one installment payment.

(3.) Prepare an amortization schedule for the three-year term of the installment note.

(4.) Prepare the journal entry for Sockets’ first installment payment received on

December 31, 2016.

(5.) Prepare the journal entry for Sockets’ third installment payment received on

December 31, 2018.

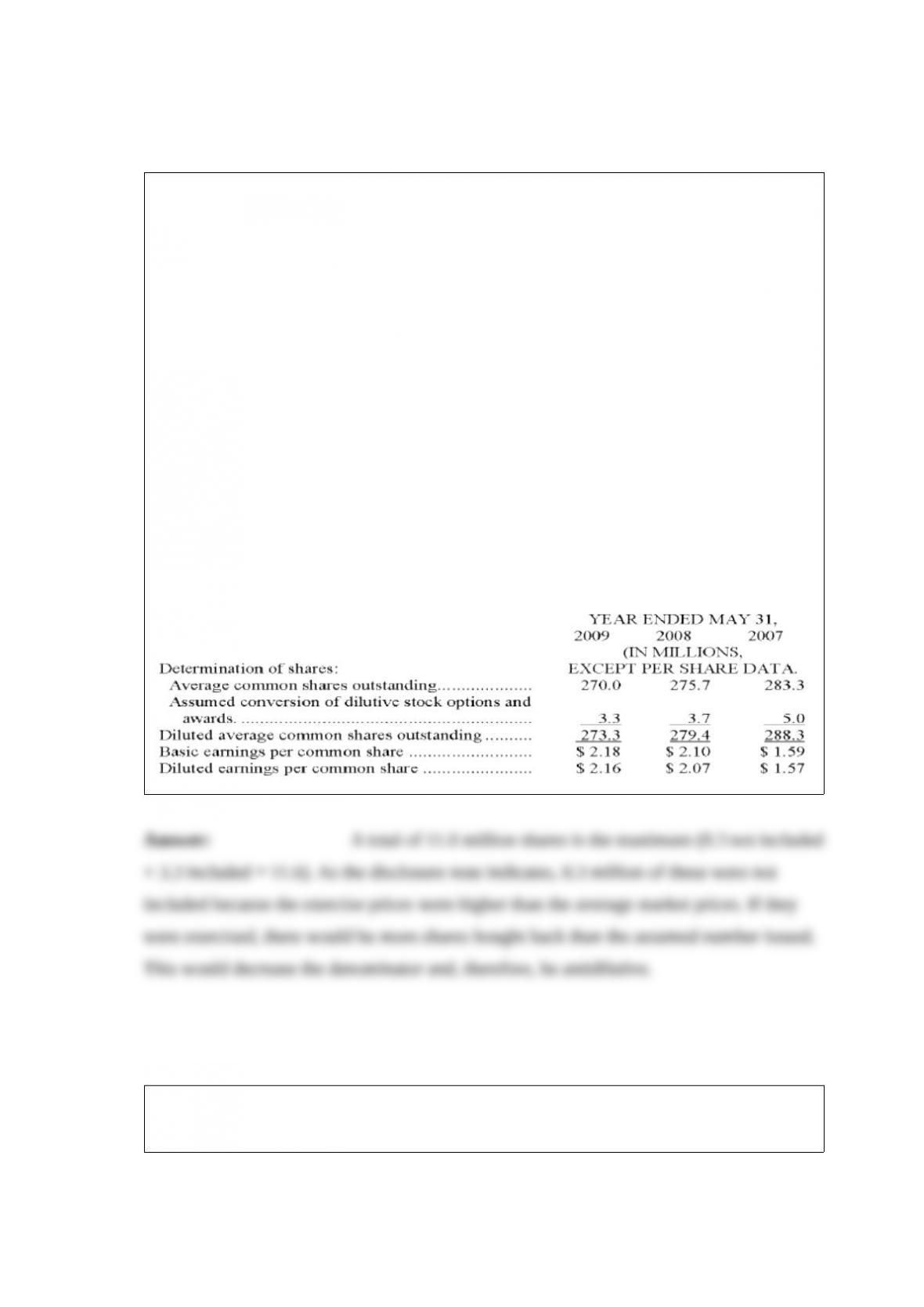

At the end of 2016, what is the maximum number of shares that could possibly be

issued if all stock options and awards are exercised? Explain why V Co. used only 3.3

million in its computation for 2016.

In its 2016 Annual Report to shareholders, V Co. had the following disclosure note

about its EPS:

NOTE 9 – EARNINGS PER SHARE:

The following represents the reconciliation from basic earnings per share to diluted

earnings per share. Options to purchase 8.3 million and 9.7 million shares of common

stock were outstanding at May 31, 2016 and May 31, 2015, respectively, but were not

included in the computation of diluted earnings per share because the options’ exercise

prices were greater than the average market price of the common shares and, therefore,

the effect would be antidilutive. No such antidilutive options were outstanding at May

31, 2014.

Year ended May 31,

2016 2015 2014

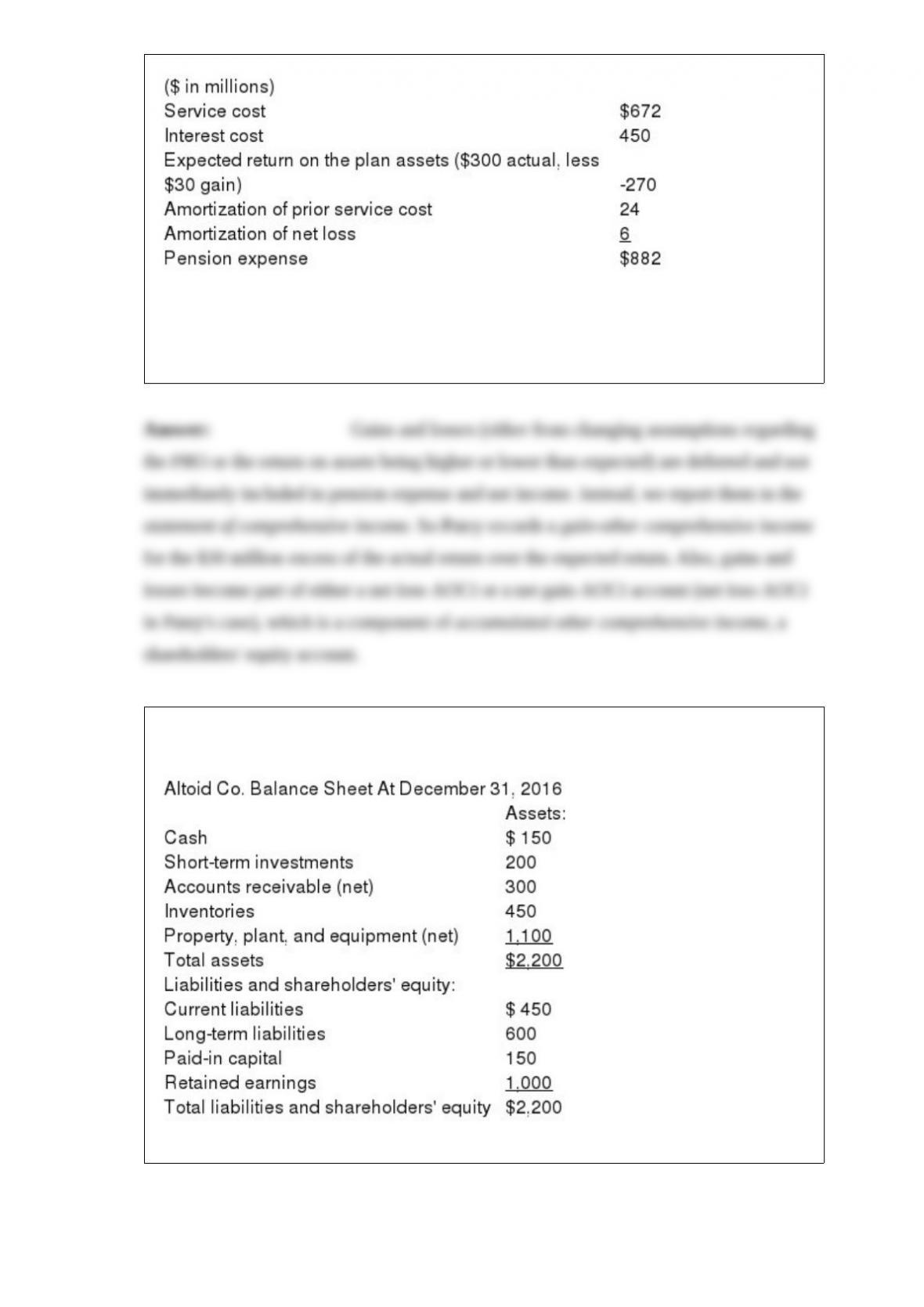

Patey Technologies calculated pension expense for its underfunded pension plan as

follows:

Required:

What is the effect of the components of pension expense on Patey’s statement of

comprehensive income?

The balance sheet for Altoid Co. is shown below.

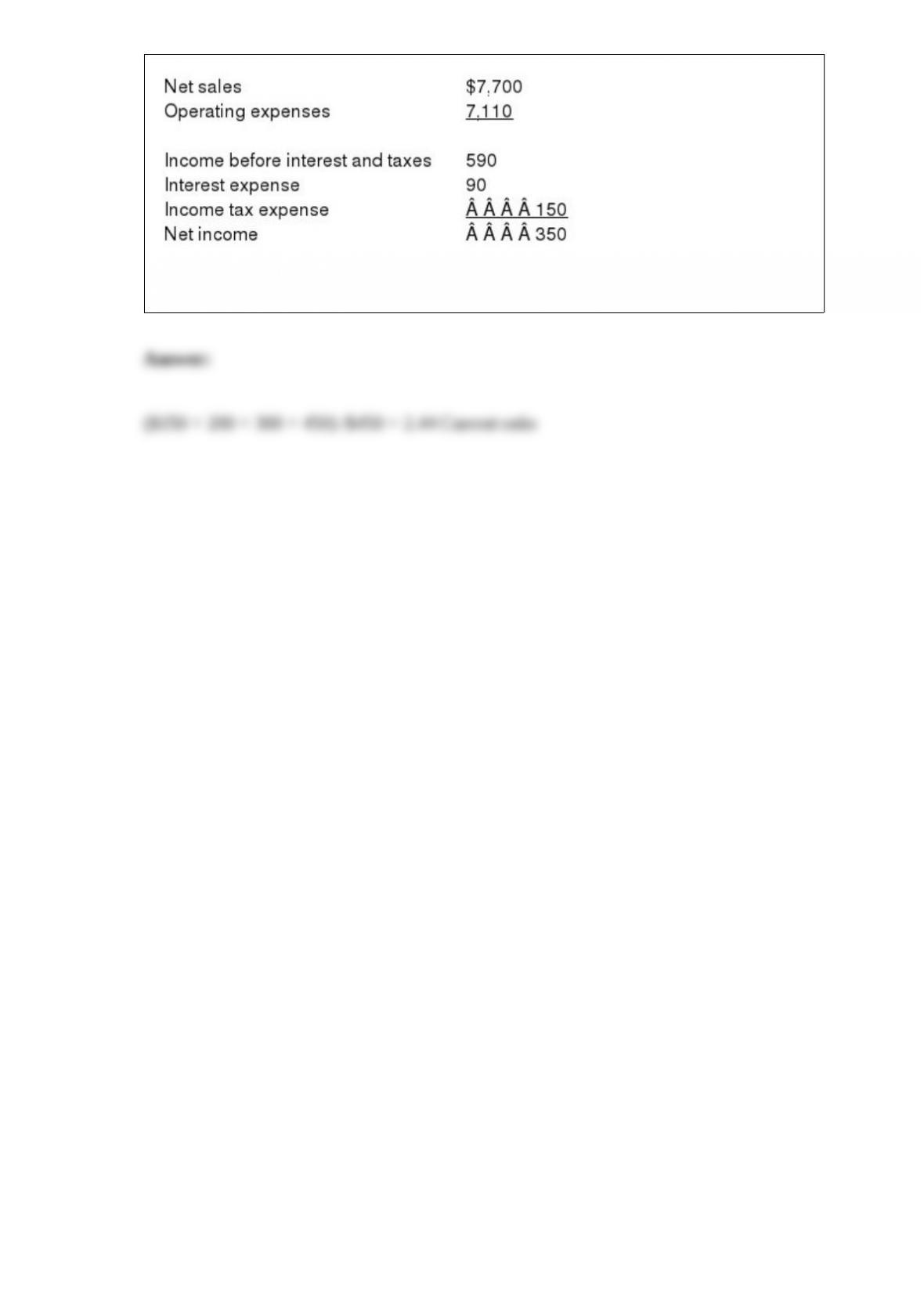

Selected 2016 income statement information for Altoid Co. includes:

Required: Compute the following financial statement ratios for 2016: Altoid Co.’s

current ratio. Round your answer to two decimal places.