1) According to the liquidity premium theory of the term structure, a downward sloping

yield curve indicates that short-term interest rates are expected to

A) rise in the future

B) remain unchanged in the future

C) decline moderately in the future

D) decline sharply in the future

2) For internal decision-making purposes, Geogh Corporation identifies its industry

segments by geographical area. For 2011, the total revenues of each segment are

provided below. There are no intersegment revenues.

Total

Revenues

Canada$980,000

United States1,410,000

Mexico1,260,000

South America430,000

China710,000

Russia660,000

Australia370,000

European Union1,220,000

Other European1,650,000

Total revenues$8,690,000

Required:

1> Which operating segments will be considered reporting segments based on the

revenue test?

2> What is the test value for determining whether a sufficient number of segments are

reported?

3> What will be the minimum number of segments that must be reported?

3) Which condition must be met for fresh-start reporting for an emerging company from

Chapter 11?

A) Holders of existing voting shares immediately before confirmation of the

reorganization plan must receive more than fifty percent of the emerging entity

B) The loss of control by voting shareholders must be temporary

C) The reorganization value of the emerging entity’s assets immediately before the date

of the confirmation of the reorganization plan must be less than the total of all

postpetition liabilities and allowed claims

D) The fresh-start entity must have a deficit

4) Lola, Melvin, and Nettie are in the process of liquidating their partnership. Since it

may take several months to convert the other assets into cash, the partners agree to

distribute all available cash immediately, except for $12,000 that is set aside for

contingent expenses. The balance sheet and residual profit and loss sharing percentages

are as follows:

Cash$500,000Accounts payable$225,000

Other assets225,000Lola, capital (20%)168,000

Melvin, capital (30%)270,000

Nettie, capital (50%)62,000

Total assets$725,000Total liab./equity$725,000

Using a safe payments schedule, how much cash should Melvin receive in the first

distribution?

A) $ 81,000

B) $165,000

C) $168,600

D) $202,500

5) According to the liquidity premium theory of the term structure, a steeply upward

sloping yield curve indicates that short-term interest rates are expected to

A) rise in the future

B) remain unchanged in the future

C) decline moderately in the future

D) decline sharply in the future

6) A comprehensive annual financial report has the following three major sections:

A) introductory, financial, and management’s discussion and analysis

B) introductory, financial, and statistical

C) transmittal, financial, and statistical

D) transmittal, financial, and management’s discussion and analysis

7) Not-for-profit, private colleges classify student unions, dining halls, and residence

halls as

A) educational and general services

B) auxiliary enterprises

C) independent operations

D) restricted enterprises

8) A subsidiary split its stock 2 for 1. Which of the following statements is false?

A) A stock split does not affect the amount of net assets of the subsidiary

B) A stock split does not affect parent and noncontrolling interest ownership

percentages

C) A stock split does not affect consolidation procedures

D) A 2 for 1 stock split decreases the number of shares outstanding

9) Prussia Corporation owns 80% the voting stock of Stad Corporation. On January 1,

2010, Prussia paid $391,000 cash for $400,000 par of Stad’s 10% $1,000,000 par value

outstanding bonds, due on April 1, 2015 . Stad’s bonds had a book value of $1,045,000

on January 1, 2010 . Straight-line amortization is used. The gain or loss on the

constructive retirement of $400,000 of Stad bonds on January 1, 2010 was reported in

the 2010 consolidated income statement in the amount of

A) $14,000

B) $21,600

C) $23,000

D) $27,000

10) Palm owns a 70% interest in Sable, a domestic subsidiary. Sable is not part of

Palm’s affiliated group. Palm will pay taxes on

A) none of the dividends it receives from Sable

B) 20% of the dividends it receives from Sable

C) 66% of the dividends it receives from Sable

D) 80% of the dividends it receives from Sable

11) The preferred habitat theory of the term structure is closely related to the

A) expectations theory of the term structure

B) segmented markets theory of the term structure

C) liquidity premium theory of the term structure

D) the inverted yield curve theory of the term structure

12) On January 5, 2011, Eagle Corporation paid $50,000 in real estate taxes for the

calendar year. In March of 2011, Eagle paid $180,000 for an annual machinery overhaul

and $10,000 for the annual CPA audit fee. What amount was expensed for these items

on Eagle’s quarterly interim financial statements?

A)

B)

C)

D)

13) According to this theory of the term structure, bonds of different maturities are not

substitutes for one another

A) Segmented markets theory

B) Expectations theory

C) Liquidity premium theory

D) Separable markets theory

14) Risk premiums on corporate bonds tend to ________ during business cycle

expansions and ________ during recessions, everything else held constant

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

15) Cirtus Corporation, a U.S. corporation, placed an order for inventory from a

Mexican supplier on September 18 when the spot rate was $0.0840 = 1 peso. The

invoice price will be denominated in pesos. At that time, they entered into a 30-day

forward contract (designated as a fair value hedge of the firm commitment to purchase)

to purchase 860,000 pesos at a forward rate of $0.0810. On October 18 when the

inventory was received, the spot rate was $0.0890. At what amount should the

inventory be carried on Cirtus’ books?

A) $69,660

B) $72,240

C) $76,540

D) $860,000

16) Taydus Corporation, a U.S. corporation, sold goods on December 2 to a company

overseas, and is now carrying a receivable denominated in euros. Taydus signed a

60-day forward contract on that same date to sell euros. The spot rate was $1.40 on the

date they signed the contract and the 60-day forward rate was $1.36. At the end of that

month when they closed the books at their fiscal year-end, the spot rate was $1.42 and

the 30-day forward rate was $1.40. Assume this is a fair value hedge. The forward

contract will not be settled net. What would be reported by Taydus for the year ending

December 31?

A) Net exchange gain

B) Net exchange loss

C) Deferred exchange gain

D) Deferred exchange loss

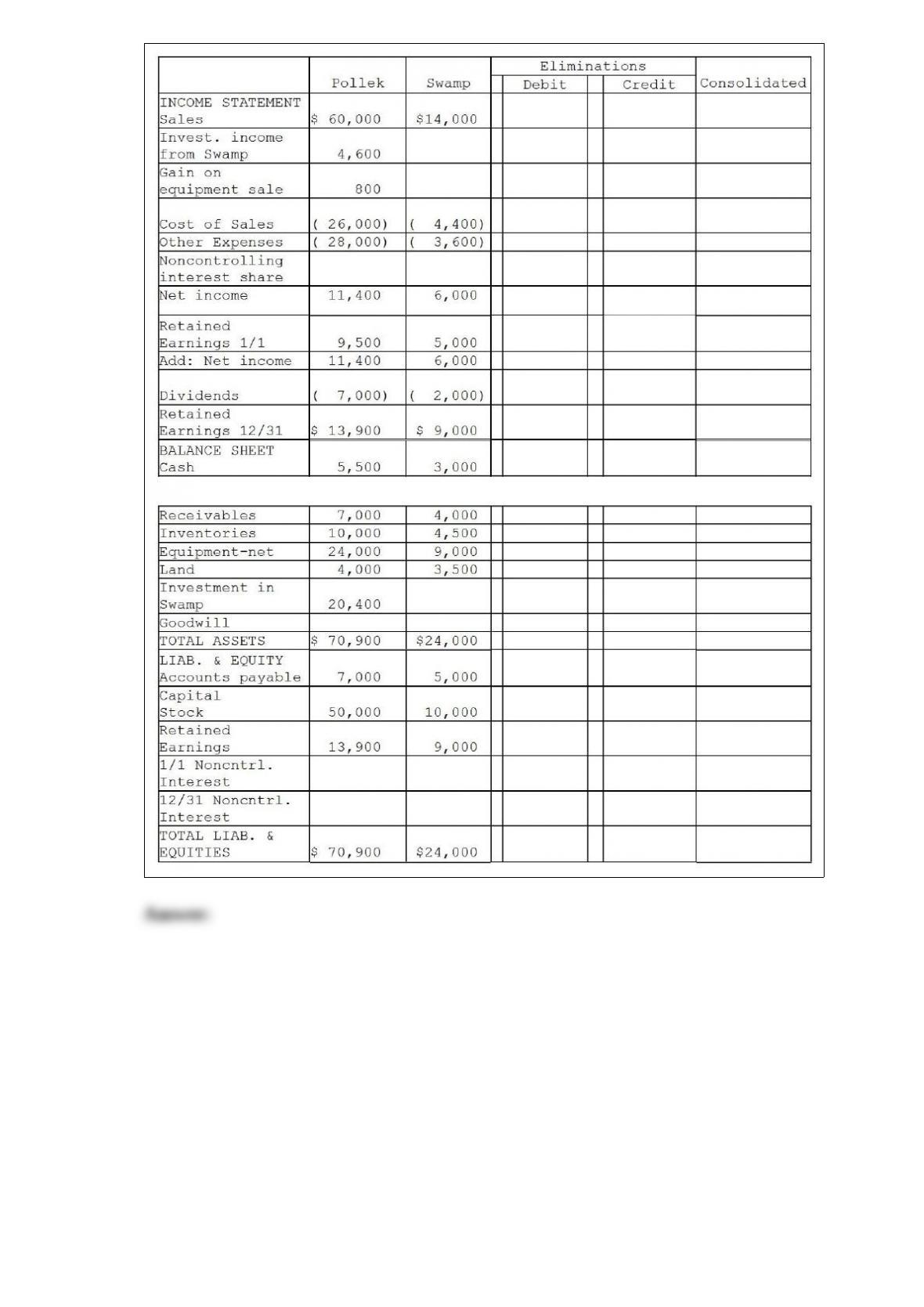

17) Pollek Corporation paid $16,200 for a 90% interest in Swamp Corporation on

January 1, 2011, when Swamp stockholders’ equity consisted of $10,000 Capital Stock

and $3,000 of Retained Earnings. The excess cost over book value was attributable to

goodwill.

Additional information:

1>.Pollek sells merchandise to Swamp at 120% of Pollek’s cost. During 2011, Pollek’s

sales to Swamp were $4,800, of which half of the merchandise remained in Swamp’s

inventory at December 31, 2011 . (The 2011 ending inventory was sold in 2012) During

2012, Pollek’s sales to Swamp were $6,000 of which 60% remained in Swamp’s

inventory at December 31, 2012 . At year-end 2012, Swamp owed Pollek $1,500 for the

inventory purchased during 2012 .

2>Pollek Corporation sold equipment with a book value of $2,000 and a remaining

useful life of four years and no salvage value to Swamp Corporation on January 1, 2012

for $2,800. Straight-line depreciation is used.

3>Separate company financial statements for Pollek Corporation and Subsidiary at

December 31, 2012 are summarized in the first two columns of the consolidation

working papers.

4>The following information is available for 2011:

Swamp’s income $4,000

Swamp’s dividends received by Pollek$1,800

Required:

Complete the working papers to consolidate the financial statements of Pollek

Corporation and subsidiary for the year ended December 31, 2012 .

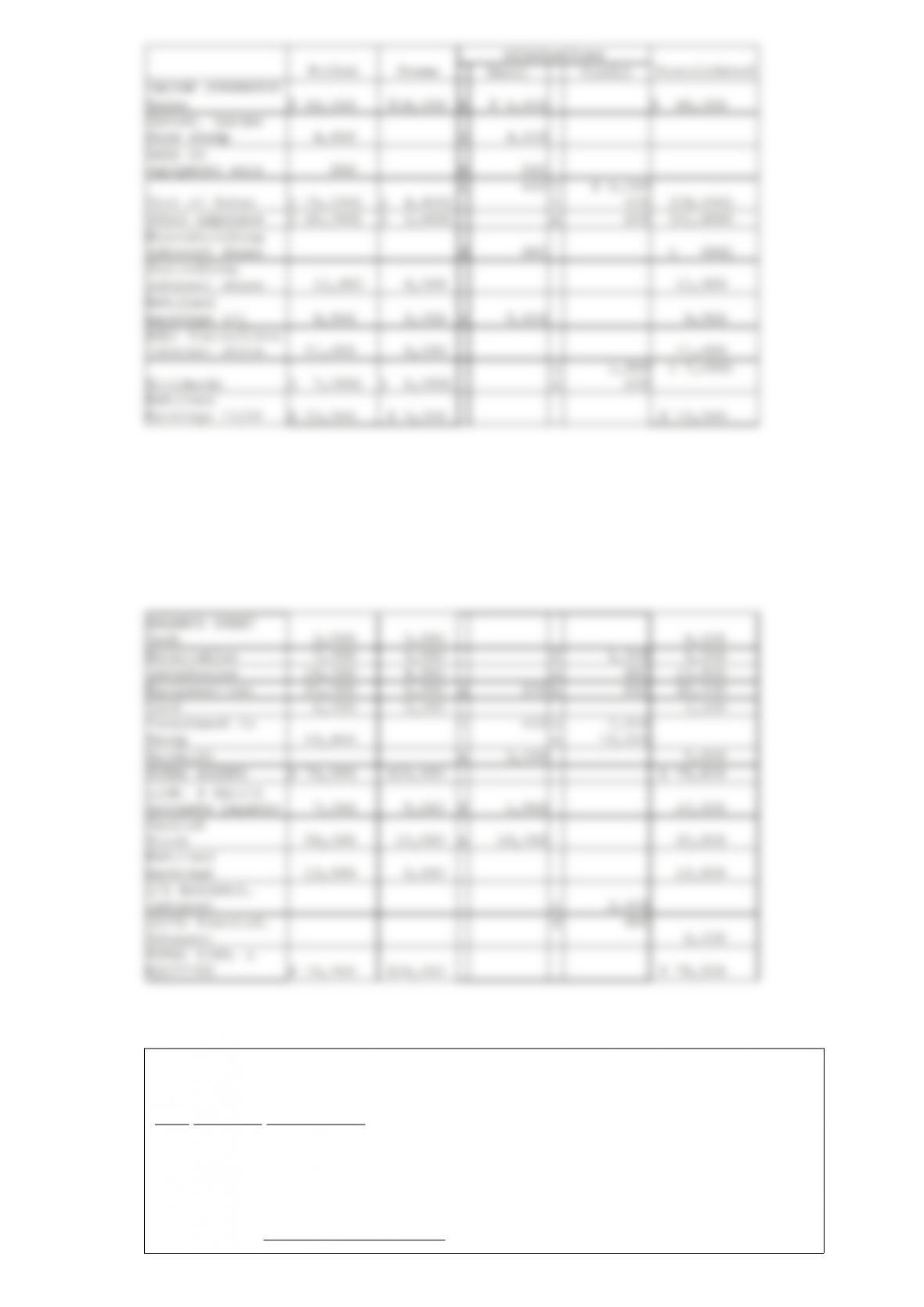

18) Separate company and consolidated income statements for Pitta and Sojourn

Corporations for the year ended December 31, 2011 are summarized as follows:

Pitta Soujourn Consolidated

Sales Revenue$ 500,000$ 100,000$ 600,000

Income from Sojourn19,900

Bond interest income6,000

Gain on bond retirement3,000

Total revenues519,900106,000603,000

Cost of sales$ 280,000$ 50,000$ 330,000

Bond interest expense9,0003,600

Other expenses 120,900 31,000 151,900

Total expenses 409,900 81,000 485,500

Consolidated net income 117,500

Noncontrolling interest share 7,500

Separate net income and

Control. interest share in

consolidated net income$ 110,000 $ 25,000$ 110,000

The interest income and expense eliminations relate to a $100,000, 9% bond issue that

was issued at par value and matures on January 1, 2016 . On January 2, 2011, a portion

of the bonds was purchased and constructively retired.

Required: Answer the following questions.

1>Which company is the issuing affiliate of the bonds payable?

2>What is the gain or loss from the constructive retirement of the bonds payable that is

reported on the consolidated income statement for 2011?

3>What portion of the bonds payable is held by nonaffiliates at December 31, 2011?

4>Is Sojourn a wholly-owned subsidiary? If not, what percentage does Pitta own?

5>Does the purchasing affiliate use straight-line or effective interest amortization?

6>Explain the calculation of Pitta’s $19,900 income from Sojourn.

19) Adam, Bella, and Chris operate a partnership with a complex profit and loss sharing

agreement. The average capital balance for Adam, Bella and Chris on December 31,

2011 is $120,000, $270,000, and $340,000, respectively. A 6% interest allocation is

provided to each partner based on the average capital balance on December 31, 2011 .

Adam and Bella receive salary allocations of $40,000 and $50,000, respectively. If

partnership net income is above $160,000, after the salary allocations are considered

(but before the interest allocations are considered), Chris will receive a bonus of 10% of

the income (pre-salary and interest, but net of the bonus). All residual income is

allocated in the ratios of 2:2:6 to Adam, Bella, and Chris, respectively.

Required:

1>Prepare a schedule to allocate income to the partners assuming that partnership net

income for 2011 is $330,000.

2>Prepare a journal entry to distribute the partnership’s income to the partners (assume

that an Income Summary account is used by the partnership).

20) On July 1, 2011, Polliwog Incorporated paid cash for 21,000 shares of Salamander

Company’s $10 par value stock, when it was trading at $22 per share. At that time,

Salamander’s total stockholders’ equity was $597,000, and they had 30,000 shares of

stock outstanding, both before and after the purchase. The book value of Salamander’s

net assets is believed to approximate the fair values.

Requirement 1: Prepare the journal entry that Polliwog would record at the date of

acquisition on their general ledger.

Requirement 2: Calculate the balance of the goodwill that would be recorded on

Polliwog’s general ledger, on Salamander’s general ledger, and in the consolidated

financial statements.

21) Phlora purchased its 100% ownership in Speshal many years ago at a time when

book values of assets and liabilities equaled market values.

On January 2, 2012, Phlora purchased $200,000 of Speshal Corporation’s 6% bonds for

$182,000. At that time, this was all of the bonds that had been issued by Speshal, and

unamortized premium on Speshal’s books was $3,500. The bonds pay interest on July 1

and January 1 and mature on January 1, 2017 . Both Phlora and Speshal use

straight-line amortization. Phlora uses the equity method of accounting for its

investment in Speshal.

Speshal reported the following for 2012:

Net income$38,000

Dividends$10,000

Required:

Prepare elimination/adjusting entries on the consolidating work papers for the year

ended December 31, 2012 .