When interest is compounded, the stated rate of interest exceeds the effective rate of

interest.

Companies always recognize revenue when goods or services are transferred to

customers for the amount the company expects to receive in exchange for those goods

or services.

The projected benefit obligation may be less reliable than the accumulated benefit

obligation.

An implicit or imputed rate of interest must be used when long-term notes are issued at

a stated rate of interest that is materially different from the market rate of interest.

Balance sheet accounts are referred to as temporary accounts because their balances are

always changing.

The amount of variable consideration that can be recognized is limited to the amount

for which it is probable that there won’t be a significant reversal of revenue recognized

to date when uncertainty resolves in the future.

Segment reporting requires disclosure of each customer that accounts for more than 5%

of total enterprise revenue.

The adjusted trial balance contains only permanent accounts.

If the contract contains multiple performance obligations, revenue must be recognized

in an amount equal to the fair value of each of the separate performance obligations.

The Public Reform and Investor Protection Act of 2002 (Sarbanes-Oxley) changed the

entity responsible for setting auditing standards in the United States.

A common output method used to measure progress towards completion is to compare

cost incurred to date to total costs estimated to complete the job.

Under IFRS No. 9, cost can be used as an estimate of fair value in some circumstances.

In the current year, Hanna Company reported quality-assurance warranty expense of

$190,000 and the warranty liability account increased by $20,000. What were warranty

expenditures during the year?

a. $190,000.

b. $170,000.

c. $210,000

d. $ 0.

The second step, when using dollar-value LIFO retail method for inventory, is to

determine the estimated:

a. Ending inventory at current year retail prices.

b. Cost of goods sold for the current year.

c. Ending inventory at cost.

d. Ending inventory at base year retail prices.

The main issue in the debate over accounting for employee stock options was:

a. Which employees should receive options.

b. The amount of compensation expense that a company should recognize.

c. How many options should be granted to key executives.

d. The tax consequences of employee stock options.

Securities that are purchased with the intent of selling them in the near future to take

advantage of short-term price changes are classified as:

a. Securities available for sale.

b. Consolidating securities.

c. Held-to-maturity securities.

d. Trading securities.

Cost of goods sold is:

a. An asset account.

b. A revenue account.

c. An expense account.

d. A permanent equity account.

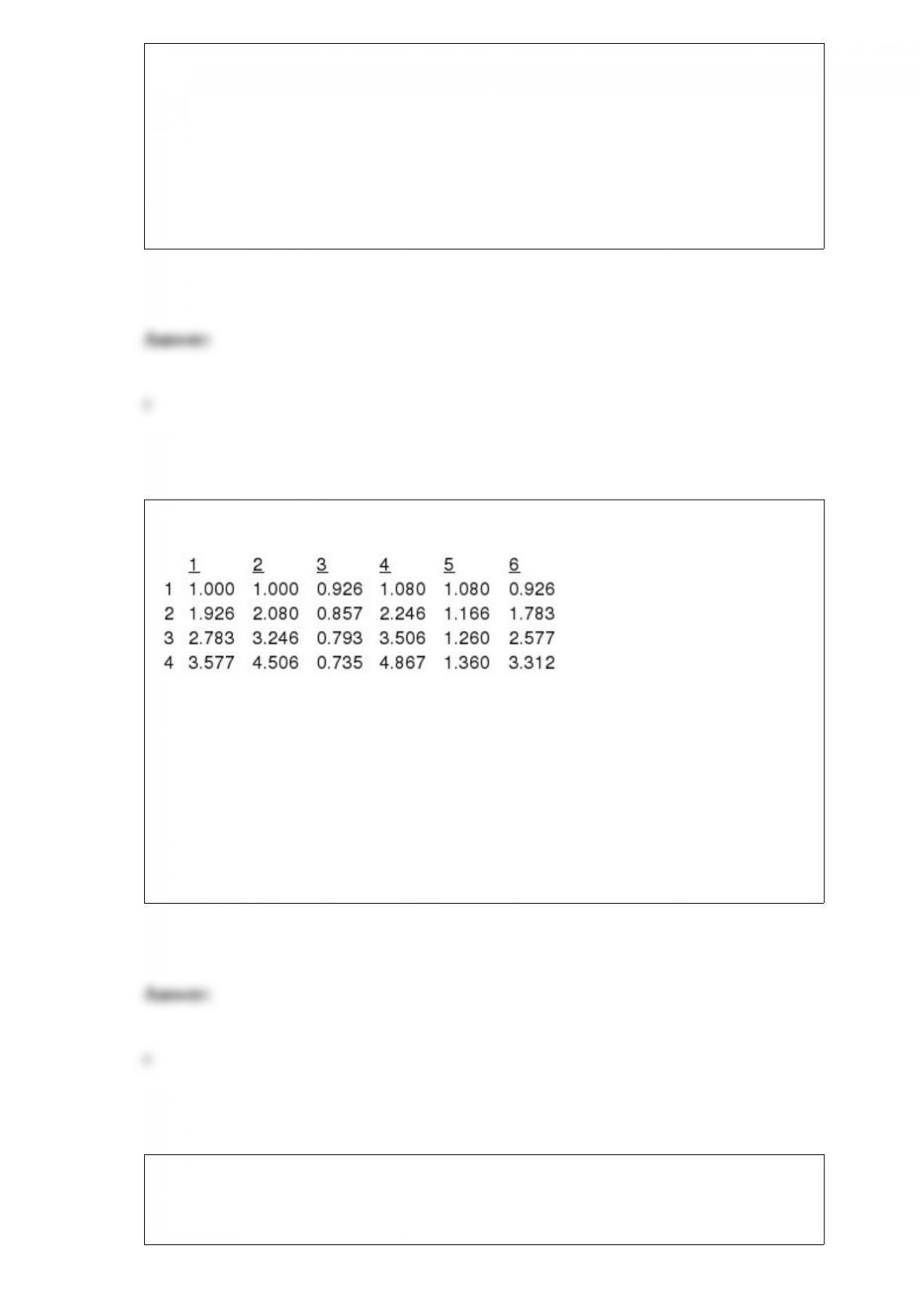

Below are excerpts from time value of money tables for the 8% rate.

Column 1 is an interest table for the:

a. Present value of an ordinary annuity of 1.

b. Future value of an ordinary annuity of 1.

c. Present value of an annuity due of 1.

d. Future value of an annuity due of 1.

Charlene Company sold a printer with a cost of $68,000 and accumulated depreciation

of $23,000 for $20,000 cash. This transaction would be reported as:

a. An operating activity.

b. An investing activity.

c. A financing activity.

d. None of these answer choices is correct.

The result of a stock split is:

a. A larger number of more valuable shares.

b. An increase in corporate assets.

c. An increase in shareholders’ equity.

d. A larger number of less valuable shares.

GAAP regarding accounting for income taxes requires the following procedure:

a. Computation of deferred tax assets and liabilities based on temporary differences.

b. Computation of deferred income tax based on permanent differences.

c. Computation of income tax expense based on taxable income.

d. Computation of deferred income tax based on temporary and permanent differences.

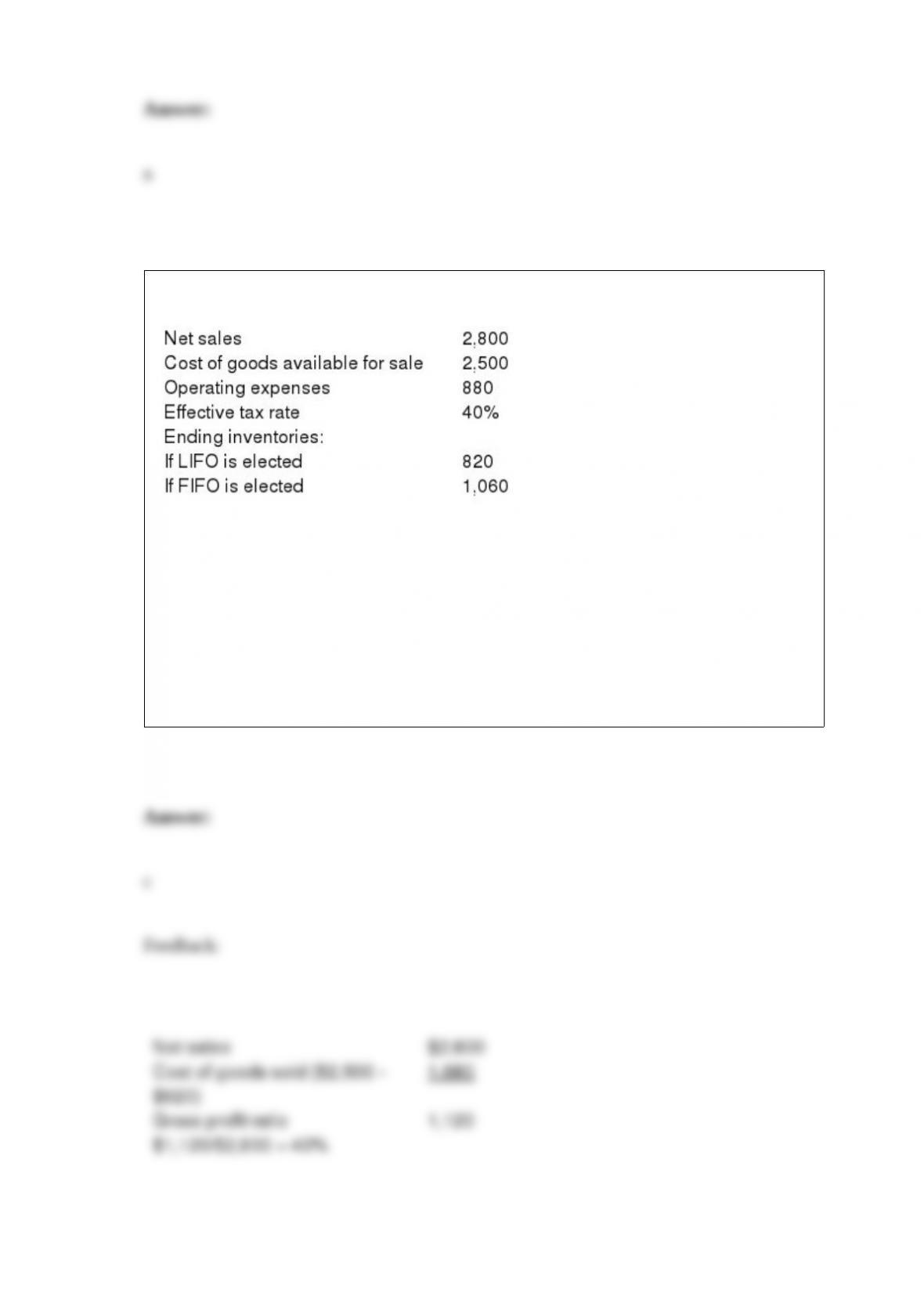

Nu Company reported the following pretax data for its first year of operations.

What is Nu’s gross profit ratio if it elects LIFO?

a. 80%.

b. 49%.

c. 40%.

d. 5%.

Sandra won $5,000,000 in the state lottery, which she has elected to receive at the end

of each month over the next 30 years. She will receive 7% interest on unpaid amounts.

To determine the amount of her monthly check, she should use a table for the:

a. Present value of an annuity due of 1.

b. Future value of an annuity due of 1.

c. Present value of an ordinary annuity of 1.

d. Future value of an ordinary annuity of 1.

The board of directors of Capstone Inc. declared a $0.60 per share cash dividend on its

$1 par common stock. On the date of declaration, there were 50,000 shares authorized,

20,000 shares issued, and 5,000 shares held as treasury stock. What is the entry for the

dividend declaration?

a. Retained earnings 9,000

Dividends payable

9,000

b. Retained earnings 9,000

Cash

9,000

c. Retained earnings 10,000

Dividends payable

10,000

d. Retained earnings 10,000

Cash

10,000

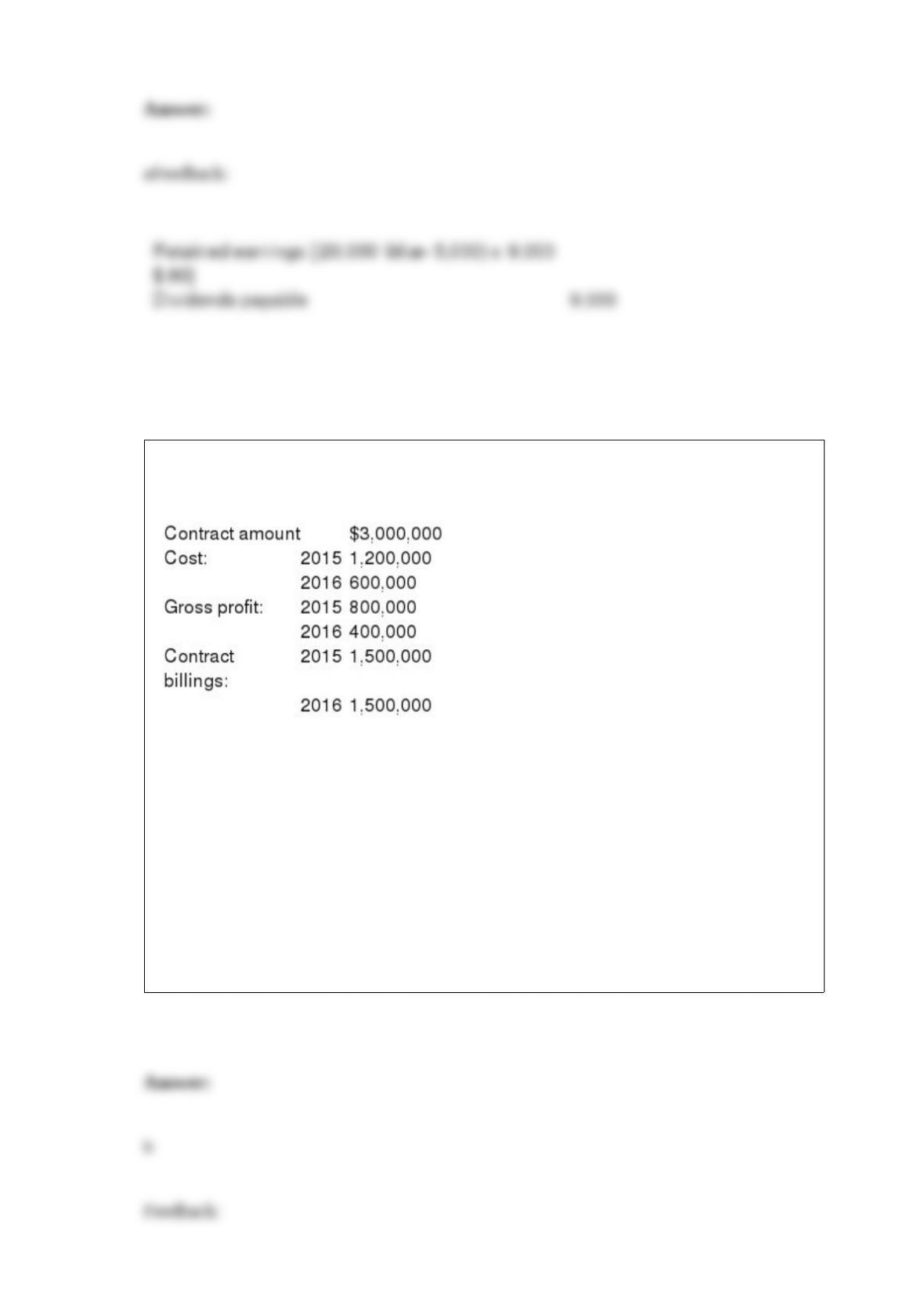

Arizona Desert Homes (ADH) constructed a new subdivision during 2015 and 2016

under contract with Cactus Development Co. Relevant data are summarized below:

ADH recognizes revenue upon completion of the contract.

In its December 31, 2015, balance sheet, ADH would report:

a. The contract asset, cost and profits in excess of billings, of $500,000.

b. The contract liability, billings in excess of cost, of $300,000.

c. The contract asset, contract amount in excess of billings, of $1,500,000.

d. The contract asset, deferred profit, of $400,000.

The rate of interest that actually is incurred on a bond payable is called the:

a. Face rate.

b. Contract rate.

c. Effective rate.

d. Stated rate.

Which of the following is always reported as an outflow of cash?

a. The accrual of warranty expense.

b. The declaration of a cash dividend.

c. The purchase of equipment for cash.

d. Amortization expense.

Interest cost will:

a. Increase the PBO and increase pension expense.

b. Increase pension expense and reduce plan assets.

c. Increase the PBO and reduce plan assets.

d. Increase pension expense and reduce the return on plan assets.

Which of the following describes defined benefit pension plans?

a. They raise few accounting issues for employers.

b. Retirement benefits depend on how much money has accumulated in an individual’s

account.

c. They are simple to construct.

d. Retirement benefits are based on the plan benefit formula.

What is Falwell’s basic earnings per share for 2016, rounded to the nearest cent?

During 2016, Falwell Inc. had 500,000 shares of common stock and 50,000 shares of

6% cumulative preferred stock outstanding. The preferred stock has a par value of $100

per share. Falwell did not declare or pay any dividends during 2016.

Falwell’s net income for the year ended December 31, 2016, was $2.5 million. The

income tax rate is 40%. Falwell granted 10,000 stock options to its executives on

January 1 of this year. Each option gives its holder the right to buy 20 shares of

common stock at an exercise price of $29 per share. The options vest after one year.

The market price of the common stock averaged $30 per share during 2016.

a. $3.14.

b. $4.40.

c. $5.00.

d. None of these answer choices is correct.

On December 15, 2016, Rigsby Sales Co. sold a tract of land that cost $3,600,000 for

$4,500,000. Rigsby appropriately uses the installment sales method of accounting for

this transaction. Terms called for a down payment of $500,000 with the balance in two

equal annual installments payable on December 15, 2017, and December 15, 2018.

Ignore interest charges. Rigsby has a December 31 year-end. In its December 31, 2016,

balance sheet, Rigsby would report:

a. Realized gross profit of $100,000.

b. Deferred gross profit of $100,000.

c. Installment receivables (net) of $3,200,000.

d. Installment receivables (net) of $4,000,000.

Burnet Company had 30,000 shares of common stock outstanding on January 1, 2016.

On April 1, 2016, the company issued 15,000 shares of common stock. The company

had outstanding fully vested incentive stock options for 5,000 shares exercisable at $10

that had not been exercised by its executives. The average market price of common

stock was $9. The company reported net income in the amount of $189,374 for 2016.

What is the effect of the options?

a. The options are antidilutive.

b. The options will dilute EPS by $.09 per share.

c. The options will dilute EPS by $.33 per share.

d. The options will dilute EPS by $.17 per share.

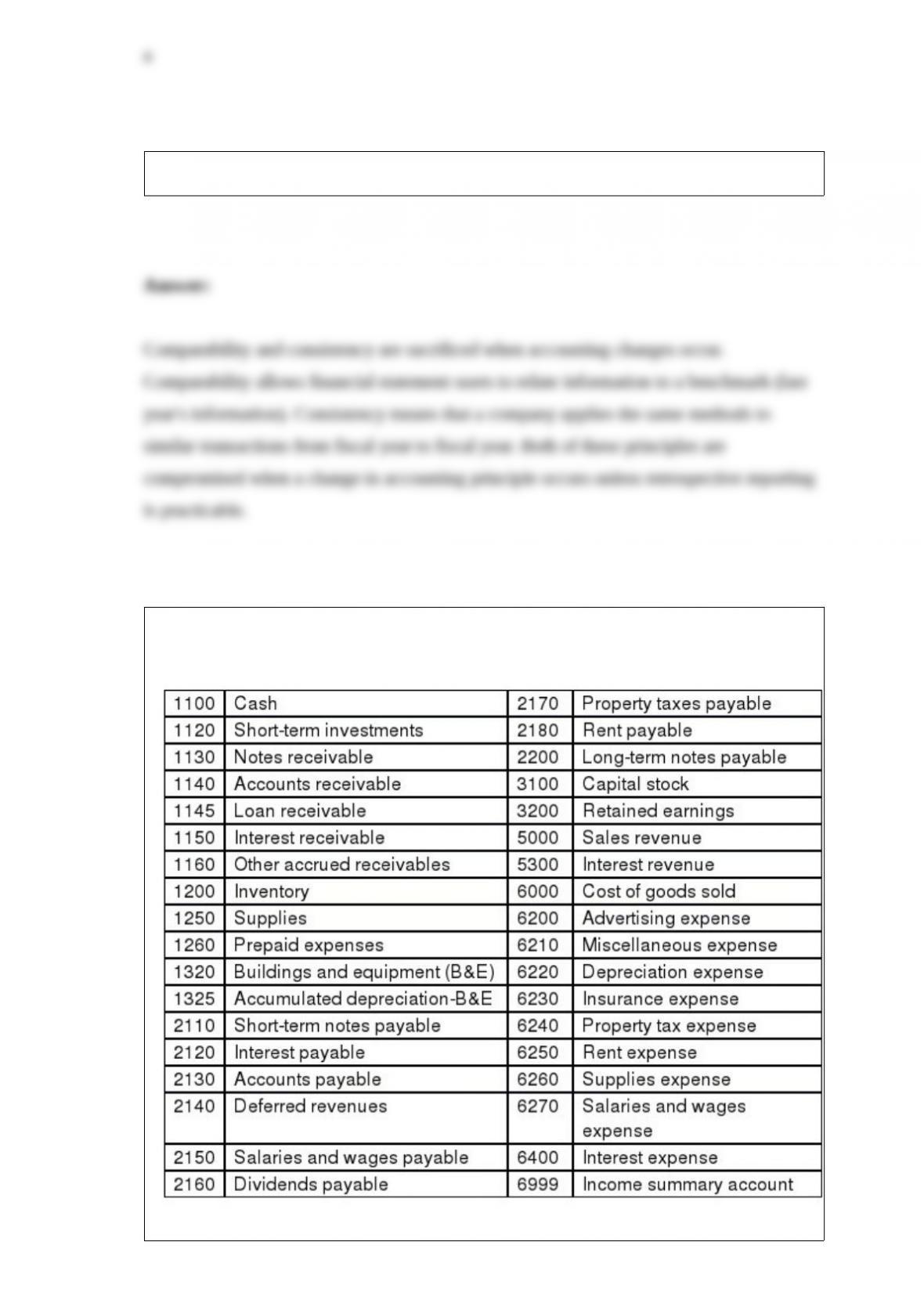

How may accounting changes detract from accounting information?

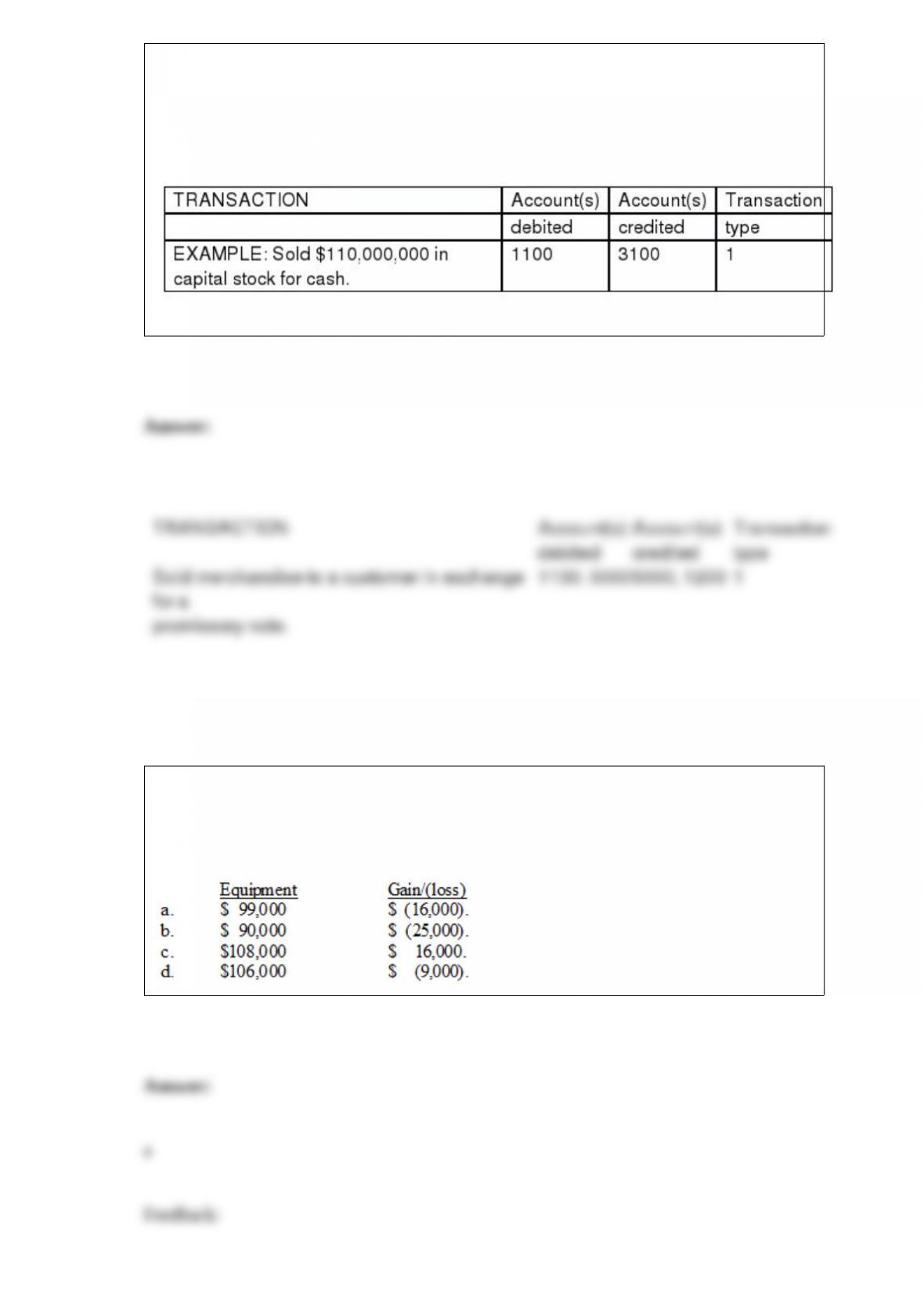

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Sold merchandise to a customer in exchange for a promissory note.

P. Chang & Co. exchanged land and $9,000 cash for equipment. The book value and the

fair value of the land were $106,000 and $90,000, respectively.

Chang would record equipment and a gain/(loss) of:

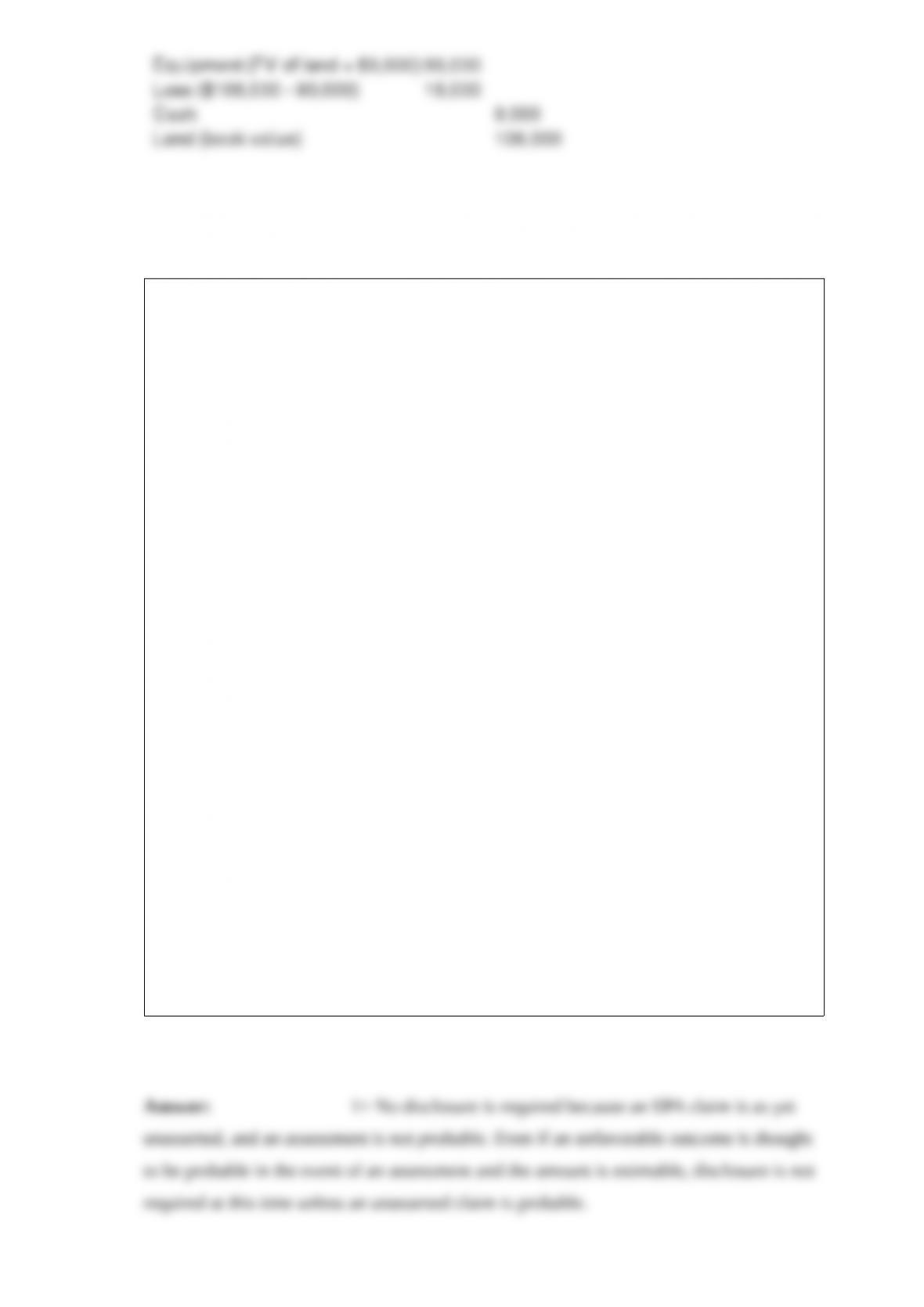

Barone, Inc. is involved with several situations that possibly involve contingencies.

Each is described below. Barone’s fiscal year ends December 31, and the 2016 financial

statements are issued on March 1, 2017.

1> At March 1, 2017, the EPA is in the process of investigating possible chemical leaks

at two of Barone’s facilities, but has not proposed a deficiency assessment. Management

feels an assessment is reasonably possible, and if an assessment is made an unfavorable

settlement of up to $8 million is reasonably possible.

2> Barone is the plaintiff in a $33 million lawsuit filed against Faze Corp. for damages

due to lost profits from rejected contracts and for unpaid receivables. The case is in

final appeal and legal counsel advises that it is probable that Finley will prevail and be

awarded $25 million.

3> In July 2015, the State of Arkansas filed suit against Barone, seeking civil penalties

and injunctive relief for violations of environmental laws regulating hazardous waste.

On February 12, 2017, Barone reached a settlement with state authorities. Based upon

discussions with legal counsel, the Company feels it is probable that $13 million will be

required to cover the cost of violations. Barone believes that the ultimate settlement of

this claim will not have a material adverse effect on the company.

4> Barone is involved in a lawsuit resulting from a dispute with a customer. On January

5, 2017, judgment was rendered against Barone in the amount of $16 million plus

interest, a total of $18 million. Barone plans to appeal the judgment and is unable to

predict its outcome though it is not expected to have a material adverse effect on the

company. Required:

1> Determine the appropriate means of reporting each situation. Explain your

reasoning.

2> Prepare any necessary journal entries and disclosure notes.

On March 1, 2016, Navy Corporation used excess cash to purchase U.S. Treasury bonds

for $103,000 plus accrued interest. The bonds were purchased at face value. The

appropriate interest rate is 6%. Interest on these bonds is payable on January 1 and July

1 of each year. Navy’s investment is accounted for as held to maturity. The fair value of

the Treasury bonds is $104,000 at year-end.

Required:

Prepare the appropriate journal entries to record the transactions for the year, including

any year-end adjustments. Show calculations, rounded to the nearest dollar.