Z-Mart had $12,000 in accounts receivable and $320,000 in net sales for the period. To

one decimal, Z-Mart’s days’ sales uncollected was 13.7 days.

Three issues involving the Sales Journal include: (1) recording sales taxes (2) recording

sales returns and allowances and (3) recording purchase discounts.

Separation of duties divides responsibility for a series of transactions between two or

more employees or departments. Despite the increased complexity, separation of duties

reduces the risk of error and fraud.

Each sales transaction for sellers using a perpetual inventory system involves

recognizing revenue and cost of goods sold.

Factors that cause the bank statement balance of a chequing account to be different

from the business chequing account balance include: outstanding cheques, deposits in

transit, deductions for bank fees, additions for interest, and errors.

The principle of faithful representation provides the guidance in reporting inventory at

net realizable value when net realizable value is lower than cost.

The advantage of the allowance method of accounting for bad debts is that it identifies

the customers who won’t pay their bills.

Internal control over cash receipts ensures that all cash received is properly recorded

and deposited.

Accounting information systems are designed to capture information about a company’s

transactions and to provide output including financial statements and special purpose

reports.

Depreciation expense for a period is the portion of a plant asset’s cost that is allocated to

that period.

Collusion occurs when a person embezzles money from a company and tries to hide the

evidence.

On October 15, Gallery Corp. received $12,500 as a down payment on a consulting

contract. The amount was credited to Unearned Consulting Revenue. By October 31,

10% of the contract was completed. Gallery Corp. needs to prepare an adjusting entry

for $1,250.

The general rule for posting is that the controlling account is debited periodically for an

amount equal to the sum of the debits to the subsidiary ledger, and is credited

periodically for an amount equal to the sum of the credits to the subsidiary ledger.

The direct write-off method satisfies generally accepted accounting principles.

The purchaser usually records a purchase return by a credit memorandum.

Under the alternative method for recording unearned revenue, the receipt of cash in

advance of performing services would be recorded as a credit to Unearned Revenue and

a debit to Cash.

The Income Summary account is used to close all other temporary accounts at the end

of an accounting period.

The use of internal controls provides guaranteed protection against losses due to

operating activities.

Transactions that impact only assets do not require the accounting equation to stay in

balance.

In a perpetual inventory system, the cost of inventory purchased is recorded in the

Purchases account.

Money orders, cashier’s cheques, and certified cheques are examples of cash

equivalents.

Generally accepted accounting principles require companies to use a specific format for

financial statements.

The retail inventory method of estimating inventory uses the ratio of goods available for

sale at cost to goods available for sale at retail.

A post-closing trial balance is a list of permanent accounts and their balances from the

ledger after all closing entries are journalized and posted.

Revenues are the value of assets exchanged for products or services provided to

customers as part of the major operations of the business.

A work sheet is a tool of the accountant for bringing together information needed in

preparing the statements, adjusting the accounts, and preparing closing entries.

A Sales Journal is used to record sales of merchandise on credit.

Accounts receivable turnover shows how often a company converts its average

accounts receivable balance into cash during the period.

Operating expenses are classified into two categories: selling expenses and cost of

goods sold.

The legitimate claims of a business’s creditors take precedence over the claims of the

business owner or owners.

When taking a physical count of inventory, the use of pre-numbered inventory tickets

assists in the control process.

Revenue accounts should begin each accounting period with zero balances.

If financial information is relevant, this means that:

A. Decision makers can depend on it.

B. It can affect the types of decisions made by users.

C. The information is prepared using the same accounting procedures from one

accounting period to the next.

D. Users are able to compare different companies, if all the companies use similar

accounting practices.

E. The financial statements have not been prepared according to GAAP.

The basic components of an accounting system include:

A. Source documents.

B. Input devices.

C. Information processors.

D. Information storage.

E. All of these answers are correct.

Explain why closing entries are a necessary step in the accounting cycle.

A compound journal entry is:

A. A journal entry that has three or more debits and three or more credits.

B. A journal entry that affects at least three accounts.

C. A journal entry that affects at least four accounts.

D. A journal entry involving at least two accounting periods.

E. A journal entry involving only two ledger accounts.

A ledger is:

A. A book of original entry.

B. A journal in which transactions are first recorded.

C. A book in which a complete record of transactions is recorded and from which

transaction amounts are posted to the accounts.

D. A book of final entry.

E. Another name for the bank account.

An adjusting entry could be made for all of the following except:

A. Prepaid expenses.

B. Depreciation expense.

C. Owner withdrawals.

D. Unearned revenues.

E. Accrued revenues.

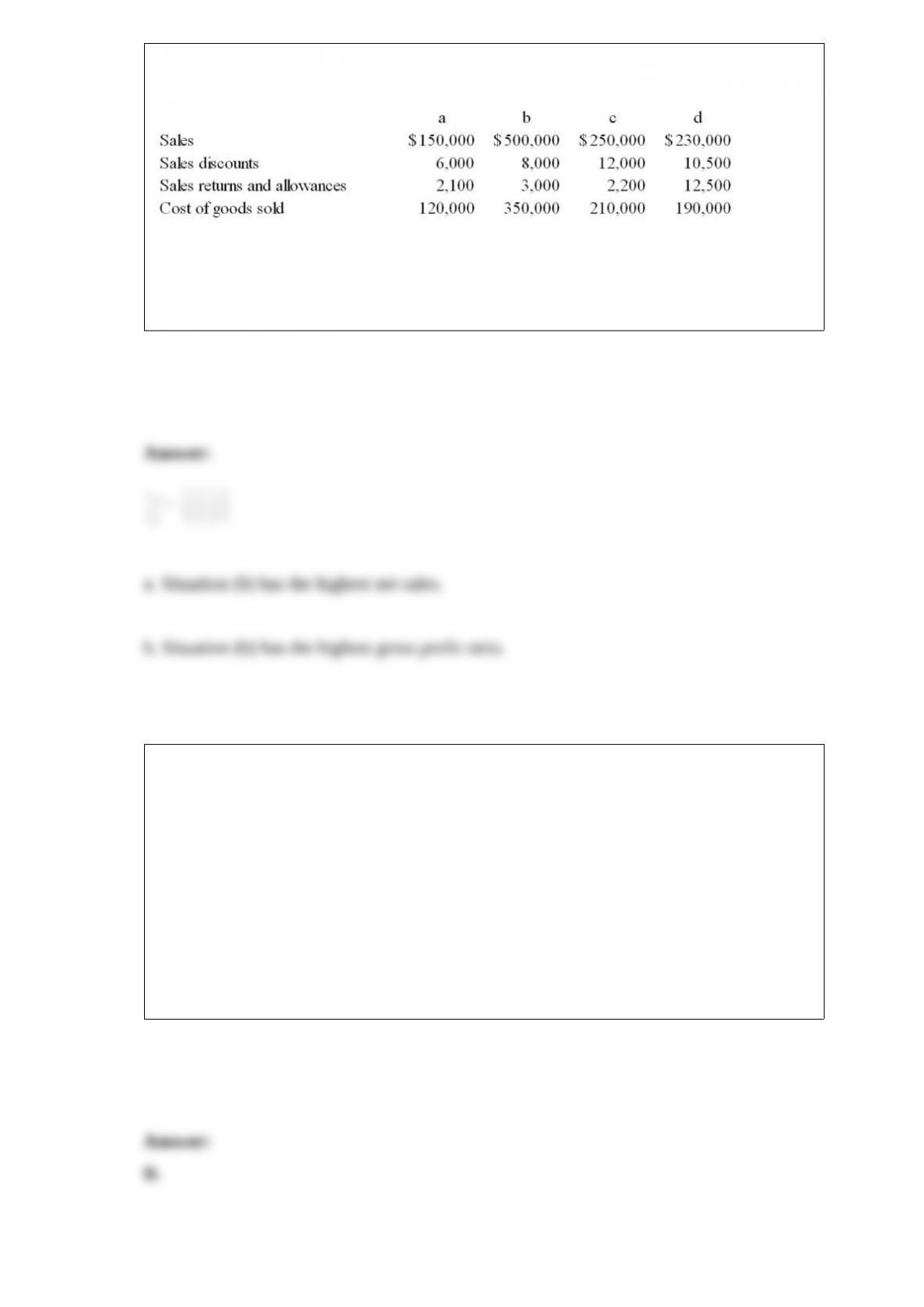

Calculate net sales, gross profit, and gross profit ratio for each of the following

situations. Round the gross profit ratio figure to the nearest whole percent.

a. Which situation has the highest net sales?

b. Which situation has the highest gross profit ratio?

A statement of financial position is another name for:

A. The income statement.

B. The balance sheet.

C. The statement of cash flows.

D. The statement of changes in equity.

E. The accounting equation.

The maturity date of a note receivable:

A. Is the day of the credit sale.

B. Is the day the note was signed.

C. Is the day the note is due to be paid.

D. Is the date of the first payment.

E. Is the last day of the month.

The following is a list of users of accounting information. Match the appropriate user

groups to the following information needs. NOTE: Some needs may apply to more than

one user group.

(a) Employees

(b) Lenders

(c) External auditors

(d) Managers

(e) Suppliers

(f) Regulators

(g) Shareholders

_______(1) The level of sales necessary to break even.

_______(2) Verification that external reports are accurate.

_______(3) Computation of taxes.

_______(4) The ability of a company to repay its loans.

_______(5) The amount of current income.

_______(6) Fairness of wages.

_______(7) Promptness of customer payment of bills.

_______(8) Profit outlook.

In a periodic inventory system:

A. The company records the cost of new merchandise in the permanent Purchases

account.

B. The cost of merchandise on hand is determined by relating the quantities on hand to

records showing each item’s original cost.

C. The inventory value is not based on a physical count.

D. A continuous record of the amount of inventory on hand is maintained.

E. None of these answers apply.

Dell had net sales of $8,739 million and average accounts receivable of $864 million.

Its accounts receivable turnover was:

A. 10.1.

B. 9.9.

C. 36.1.

D. 9.1.

E. 12.8.

A debit entry:

A. Increases asset and expense accounts.

B. Decreases liability and equity accounts.

C. Increases the owner’s withdrawals account.

D. Decreases revenue accounts.

E. All of these answers are correct.

For each of the following transactions, identify the effect on the accounting equation.

Use “+” to indicate an increase and “-” to indicate a decrease. Use “A”, “L”, and “E” to

indicate assets, liabilities, and equity, respectively.

Which of the following statements is correct regarding sales invoices?

A. A sales invoice is a type of source document.

B. Sellers use them for recording sales.

C. Buyers use them for recording purchases.

D. They are required for information to be objective.

E. All of these answers are correct.

An example of a specialty component of an AIS is:

A. Subsidiary ledger.

B. Sales Journal.

C. Property, plant and equipment.

D. Cheque Register.

E. Voucher.

Interim financial reports are financial reports:

A. Covering less than one year, usually based on one- or three-month periods.

B. That are prepared before any adjustments have been recorded.

C. That show the assets above the liabilities and the liabilities above the equity.

D. In which revenues are reported in the income statement when cash is received and

expenses are reported when cash is paid.

E. In which the adjustment process is used to assign revenues to the periods in which

they are earned and to match expenses with revenues.

The 12-month period that ends when a company’s activities are at their lowest point is

called the:

A. Fiscal year.

B. Calendar year.

C. Natural business year.

D. Accounting period.

E. Interim period.

A promissory note from a customer:

A. Is a cash equivalent.

B. Is an account receivable.

C. Is a note receivable.

D. Is a short-term investment.

E. Is a note payable.

Which of the following assets is not depreciated?

A. Store fixtures.

B. Computers.

C. Land.

D. Buildings.

E. Trucks.

Managers place a high priority on internal control systems because the systems assist

managers in the:

A. Prevention of avoidable losses.

B. Planning of operations.

C. Monitoring of company performance.

D. Monitoring of employee performance.

E. All of these answers are correct.

The entry necessary to establish a petty cash fund should include:

A. A debit to Cash.

B. A credit to Cash.

C. A debit to Petty Cash.

D. A credit to Petty Cash.

E. A credit to Cash and a debit to Petty Cash.

Mattel had net sales of $4,235 million and accounts receivable of $775 million. To one

decimal, Mattel’s days’ sales uncollected was:

A. 298.

B. 66.8.

C. 75.4.

D. 81.8.

E. 90.2.

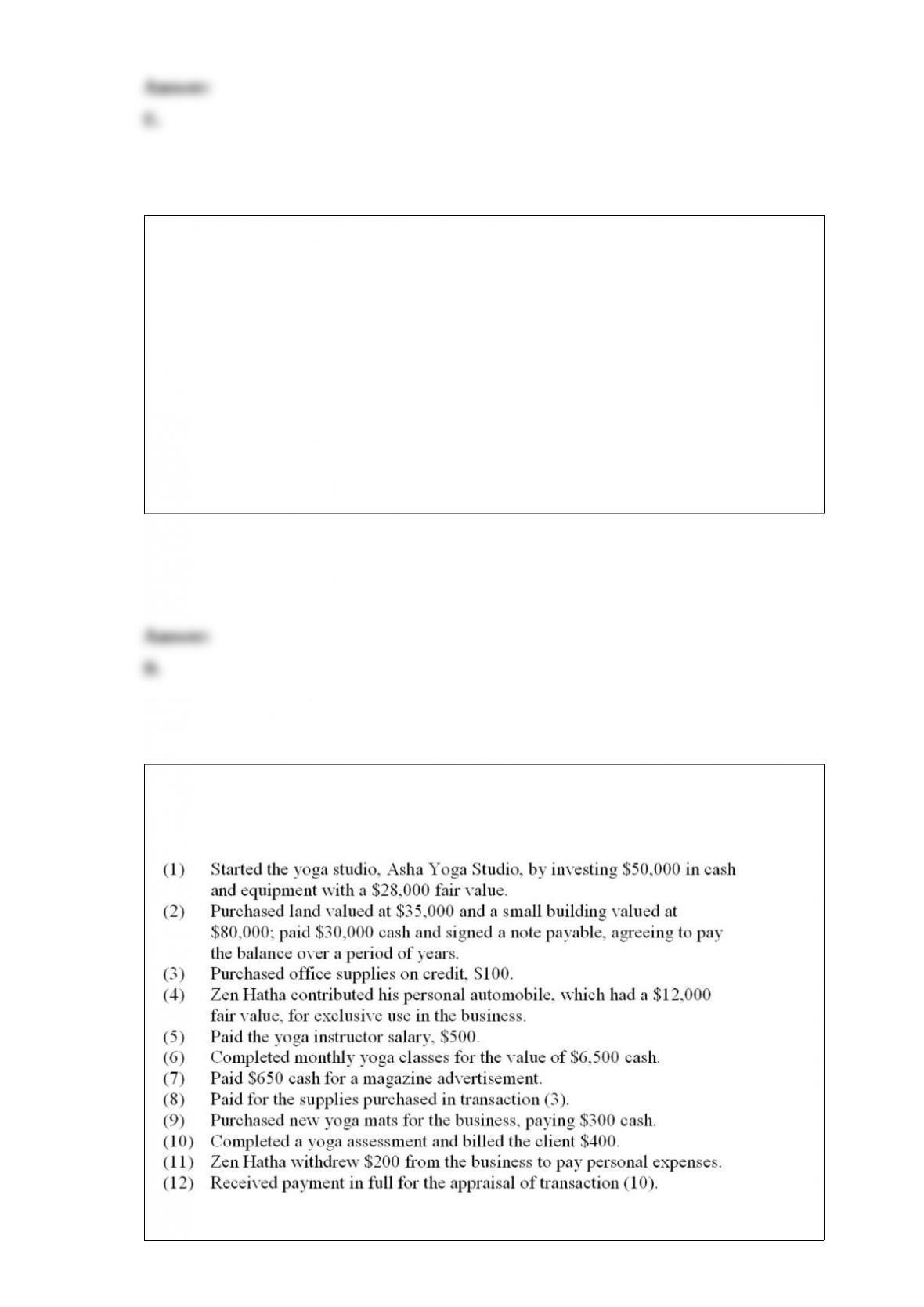

Zen Hatha opened a yoga studioand during a short period as a dealer completed these

transactions:

What was the total of the debit balances shown in the trial balance prepared after these

transactions were posted?

A. $152,300.

B. $167,700.

C. $173,950.

D. $181,900.

E. $243,620.

Bank debit cards get their name from:

A. The fact that a debit is made to Cash by the business receiving the money.

B. Banks debit your account when they take the money out of it.

C. It is the opposite of a credit card.

D. The fact that a debit is made to Cash by the business receiving the money and banks

debit your account when they take the money out of it.

E. None of these answers is correct.

The agreed cost of an item to be purchased by a business on credit is $4,000. The

applicable cost will be debited to advertising expense. The item is subject to 5% goods

and services tax (GST) and 7% provincial sales tax (PST). When this transaction is

recorded, what amount will be recorded as GST Receivable?

A. $200 debit

B. $200 credit

C. $240 debit

D. $240 credit

E. None of these answers is correct.

Compaq’s accounts receivable turnover rate was 5.7 for this year and 5.4 for last year.

Dell’s turnover rate was 6.8 for this year and 7 for last year. This means that:

A. Dell has the better turnover rate for both years.

B. Compaq has the better turnover rate for both years.

C. Dell’s turnover rate is improving.

D. Compaq’s turnover rate is improving.

E. Dell has the better turnover rate for both years and Compaq’s turnover rate is

improving.

A business sold some inventory on credit for $5,000 before taxes. The sale is subject to

5% goods and services tax (GST) and 7% provincial sales tax (PST). The business uses

a perpetual inventory system. What is the amount of the accounts receivable that was

recorded as a result of this sale?

A. $5,000

B. $5,300

C. $5,350

D. $5,600

E. None of these answers is correct.

Z-Mart made a bank deposit on September 30 that did not appear on September’s bank

statement. In preparing September’s bank reconciliation, the company should:

A. Deduct the deposit from the bank statement balance.

B. Send the bank a debit memorandum.

C. Deduct the deposit from September’s book balance and add it to October’s book

balance.

D. Add the deposit to the book balance of cash.

E. Add the deposit to the bank statement balance.

Electron borrowed $75,000 from TechCom by signing a promissory note and pledging

$85,000 in accounts receivable as security. TechCom’s entry to record the transaction

should include a:

A. Debit to Notes Receivable for $75,000.

B. Debit to Accounts Receivable for $75,000.

C. Credit to Notes Receivable for $75,000.

D. Debit Notes Payable for $75,000.

E. Credit to Sales for $75,000.

Identify the principles of internal control.

A(n) _______________ is a middleman who buys products from manufacturers and

sells to retailers.

The _____________ consists of the steps repeated each reporting period for the purpose

of preparing financial statements for users.

A dishonoured note receivable should be _______________________________.

A(n) _______________ is a list of all the accounts used by a company.

Discuss the types of adjusting entries used for prepaid expenses, depreciation, and

unearned revenues.

Identify the advantages for retailers of allowing credit cards to be used in making

purchases by their customers.

Myrex Corporation purchased $4,000 in parts from TechCom. Myrex signed a 60-day,

10% promissory note. TechCom should record the sale with a journal entry debiting

____________________ for $________ and crediting __________________ for

$________.

If, on January 1, Terry Chervinski Company paid $2,000 of its accounts payable in

cash, what would be the effect of this transaction on assets, on liabilities, and on equity?