1) Departmental contribution to overhead is the same as gross profit generated by that

department.

2) Treasury stock is stock that has been authorized, issued, and is outstanding.

3) The contract rate on previously issued bonds changes as the market rate of interest

changes.

4) A voucher system establishes procedures for verifying, approving, and recording

obligations for eventual cash disbursement.

5) A post-closing trial balance is a list of permanent accounts and their balances from

the ledger after all closing entries are journalized and posted.

6) Payments of FUTA are made quarterly to a federal depository bank if the total

amount due exceeds $500.

7) The person that borrows money and signs a promissory note is called the payee.

8) A variable cost changes in proportion to changes in the volume in activity.

9) The cash flow on total assets ratio can be used as an indicator of earnings quality.

10) A company owes its employees $5,000 for the year ended December 31. It will pay

employees on January 6 for the previous two weeks’ salaries. The year-end adjusting on

entry on December 31 will include a debit to Salaries Expense and a credit to Cash.

11) Planning is defining an organization’s ideas, goals, and actions.

12) An interest rate is also called a discount rate.

13) An out-of-pocket cost requires a future cash outlay and is relevant for decision

making.

14) When LIFO is used with the periodic inventory system, cost of goods sold is

assigned costs from the most recent purchases at the point of each sale, rather than from

the most recent purchases for the period.

15) A corporation had 50,000 shares of $20 par value common stock outstanding on

July 1. Later that day the board of directors declared a 10% stock dividend when the

market value of each share was $27. The entry to record this dividend is:

A.Debit Retained Earnings $135,000; credit Common Stock Dividend Distributable

$135,000

B.Debit Retained Earnings $135,000; credit Cash $135,000

C.Debit Retained Earnings $135,000; credit Common Stock Dividend Distributable

$100,000; credit Paid-In Capital in Excess of Par Value, Common Stock $35,000

D.Debit Retained Earnings $100,000; credit Common Stock Dividend Distributable

$100,000

E.No entry is made until the stock is issued

16) Damaged and obsolete goods that can be sold:

A.Are never counted as inventory

B.Are included in inventory at their full cost

C.Are included in inventory at their net realizable value

D.Should be disposed of immediately

E.Are assigned a value of zero

17) The matching principle prescribes:

A.That expenses be ignored if their effect on the financial statements is unimportant to

users’ business decisions

B.The use of the direct write-off method for bad debts

C.The use of the allowance method of accounting for bad debts

D.That bad debts be disclosed in the financial statements

E.That bad debts not be written off

18) Paoli Pizza bought $5,000 worth of merchandise from TechCom and signed a

90-day, 10% promissory note for the $5,000. TechCom’s journal entry to record the

sales portion of the transaction is:

A.Debit Accounts Receivable $5,000; credit Sales $5,000

B.Debit Notes Receivable $5,000; credit Sales $5,000

C.Debit Accounts Receivable $5,125; credit Sales $5,125

D.Debit Notes Receivable $5,125; credit Sales $5,125

E.Debit Notes Receivable $5,000; debit Interest Receivable $125; credit Sales $5,125

19) A company uses the percent of sales method to determine its bad debts expense. At

the end of the current year, the company’s unadjusted trial balance reported the

following selected amounts:

All sales are made on credit. Based on past experience, the company estimates 0.6% of

credit sales to be uncollectible. What adjusting entry should the company make at the

end of the current year to record its estimated bad debts expense?

A.Debit Bad Debts Expense $2,130; credit Allowance for Doubtful Accounts $2,130

B.Debit Bad Debts Expense $2,630; credit Allowance for Doubtful Accounts $2,630

C.Debit Bad Debts Expense $4,300; credit Allowance for Doubtful Accounts $4,300

D.Debit Bad Debts Expense $4,800; credit Allowance for Doubtful Accounts $4,800

E.Debit Bad Debts Expense $5,300; credit Allowance for Doubtful Accounts $5,300

20) Jackson Company has sales of $300,000 and cost of goods available for sale of

$270,000. If the gross profit ratio is typically 30%, the estimated cost of the ending

inventory under the gross profit method would be:

A.$60,000

B.$180,000

C.$30,000

D.$90,000

E.Impossible to determine from the information provided

21) The contribution margin per unit expressed as a percentage of the product’s selling

price is the:

A.Volume variance

B.Margin of safety

C.Contribution margin ratio

D.Break-even point

E.Rate of return on sales

22) The effective interest amortization method:

A.Allocates bond interest expense over the bond’s life using a changing interest rate

B.Allocates bond interest expense over the bond’s life using a constant interest rate

C.Allocates a decreasing amount of interest over the life of a discounted bond

D.Allocates bond interest expense using the current market rate for each interest period

E.Is not allowed by the FASB

23) Closing entries are required:

A.if management has decided to cease operating the business

B.only if the company adheres to the accrual method of accounting

C.if a company’s bookkeeper forgets to prepare reversing entries

D.if the temporary accounts are to reflect correct amounts for each accounting period

E.in order to satisfy the Internal Revenue Service

24) The balance in Tee Tax Services’ office supplies account on February 1 and

February 28 was $1,200 and $375, respectively. If the office supplies expense for the

month is $1,900, what amount of office supplies was purchased during February?

A.$1,075

B.$1,500

C.$1,525

D.$2,325

E.$3,100

25) The currency in which a company presents its financial statements is known as the:

A.Multinational currency

B.Price-level-adjusted currency

C.Specific currency

D.Reporting currency

E.Historical cost currency

26) The following information is available for Bosc, Inc. (all amounts are in millions):

a. Determine the segment return on assets for each geographic segment.

b. Comment on the results. How do the segments compare with respect to profitability?

27) A bond sells at a discount when the:

A.Contract rate is above the market rate

B.Contract rate is equal to the market rate

C.Contract rate is below the market rate

D.Bond has a short-term life

E.Bond pays interest only once a year

28) All of the following statements regarding a business segment are True except:

A.A business segment is a part of a company’s operations that serves a particular

product line

B.A segment has assets, liabilities, and financial results of operations that can be

distinguished from those of other parts of the company

C.A company’s gain or loss from selling or closing down a segment is reported

separately

D.A segment’s income for the period prior to the disposal and the gain or loss resulting

from disposing of the segment’s assets are combined and reported

E.A segment’s income for the period prior to the disposal and the gain or loss resulting

from disposing of the segment’s assets are reported separately

29) A company had fixed interest expense of $6,000, its income before interest expense

and any income taxes is $18,000, and its net income is $8,400. The company’s times

interest earned ratio equals:

A.0.33

B.0.71

C.1.40

D.3.00

E.12,000

30) All of the following statements regarding accounting treatments for liabilities under

U.S. GAAP and IFRS are True except:

A.Accounting for bonds and notes under U.S. GAAP and IFRS is similar

B.Both U.S. GAAP and IFRS require companies to distinguish between operating

leases and capital leases

C.The criteria for identifying a lease as a capital lease are more general under IFRS

D.Both U.S. GAAP and IFRS require companies to record costs of retirement benefits

as employees work and earn them

E.Use of the fair value option to account for bonds and notes is not acceptable under

U.S. GAAP or IFRS

31) A company issued 7%, 5-year bonds with a par value of $100,000. The market rate

when the bonds were issued was 7.5%. The company received $97,947 cash for the

bonds. Using the effective interest method, the amount of interest expense for the first

semiannual interest period is:

A.$3,500.00

B.$3,673.01

C.$3,705.30

D.$7,000.00

E.$7,346.03

32) An adjusting entry was made on year-end December 31 to accrue salary expense of

$1,200. Which of the following entries would be prepared to record the $3,000 payment

of salaries in January of the following year?

A.Choice A

B.Choice B

C.Choice C

D.Choice D

E.Choice E

33) Shelby and Mortonson formed a partnership with capital contributions of $300,000

and $400,000, respectively. Their partnership agreement calls for Shelby to receive a

$60,000 per year salary. Also, each partner is to receive an interest allowance equal to

10% of a partner’s beginning capital investments. The remaining income or loss is to be

divided equally. If the net income for the current year is $135,000, then Shelby and

Mortonson’s respective shares are:

A.$67,500; $67,500

B.$92,500; $42,500

C.$57,857; $77,143

D.$90,000; $40,000

E.$35,000; $100,000

34) The Premium on Bonds Payable account is a(n):

A.Revenue account

B.Adjunct or accretion liability account

C.Contra revenue account

D.Contra asset account

E.Contra liability account

35) A company plans to decrease a $200 petty cash fund to $75. The current balance in

the account includes $45 petty cash payment in receipts and $165 in currency. The entry

to reduce the fund will include a:

A.Debit to Cash Short and Over for $10

B.Debit to Cash for $90

C.Debit to Miscellaneous Expenses for $35

D.Credit to Petty Cash for $165

E.Credit to Cash for $90

36) A company entered into the following transactions. Match each transaction with the

appropriate journal.

1>General journal A. Borrowed $5,000 cash from the bank.

2>Cash disbursements journal B. A customer returned a $250 item purchased on

account.

3>General journal C. Purchased merchandise on account, $2,700.

4>Cash receipts journal D. Purchased a display rack on account for $4,700.

5>General journal E. Paid $65,000 cash in wages and salaries.

6>Cash disbursements journal F. Paid a utility bill for $3,400 cash.

7>Purchases journal G. Purchased $1,590 of store supplies on account.

8>Purchases journal H. Recorded depreciation on store equipment of $4,000.

9>Cash receipts journal I. Returned defective inventory purchased on account, $2,900.

10>Purchases journal J. Recorded cash sales of $14,700.

37) A company’s product sells at $12 per unit and has a $5 per unit variable cost. The

company’s total fixed costs are $98,000.The contribution margin per unit is:

A.$5.00

B.$7.00

C.$8.17

D.$12.00

E.$17.00

38) Debt securities:

A.Can be short-term investments

B.Can be long-term investments

C.Can have a cost higher than the maturity value of the debt security

D.Can have a cost lower than the maturity value of the debt security

E.All of these

39) In cost-volume-profit analysis, the unit contribution margin is:

A.Sales price per unit less cost of goods sold per unit

B.Sales price per unit less unit fixed cost per unit

C.Sales price per unit less total variable cost per unit

D.Sales price per unit less unit total cost per unit

E.The same as the contribution margin ratio

40) The acid-test ratio:

A.Is also called the quick ratio.

B.Measures profitability.

C.Measures inventory turnover.

D.Is generally greater than the current ratio.

E.Measures return on assets.

41) Net Income:

A.Decreases equity

B.Represents the amount of assets owners put into a business

C.Equals assets minus liabilities

D.Is the excess of revenues over expenses

E.Represents owners’ claims against assets

42) The predetermined overhead allocation rate for Forsythe, Inc., is based on estimated

direct labor costs of $400,000 and estimated factory overhead of $500,000. Actual costs

incurred were:

(a) Calculate the predetermined overhead rate and calculate the overhead applied during

the year.

(b) Determine the amount of over- or underapplied overhead and prepare the journal

entry to eliminate the over- or underapplied overhead assuming that it is not material in

amount.

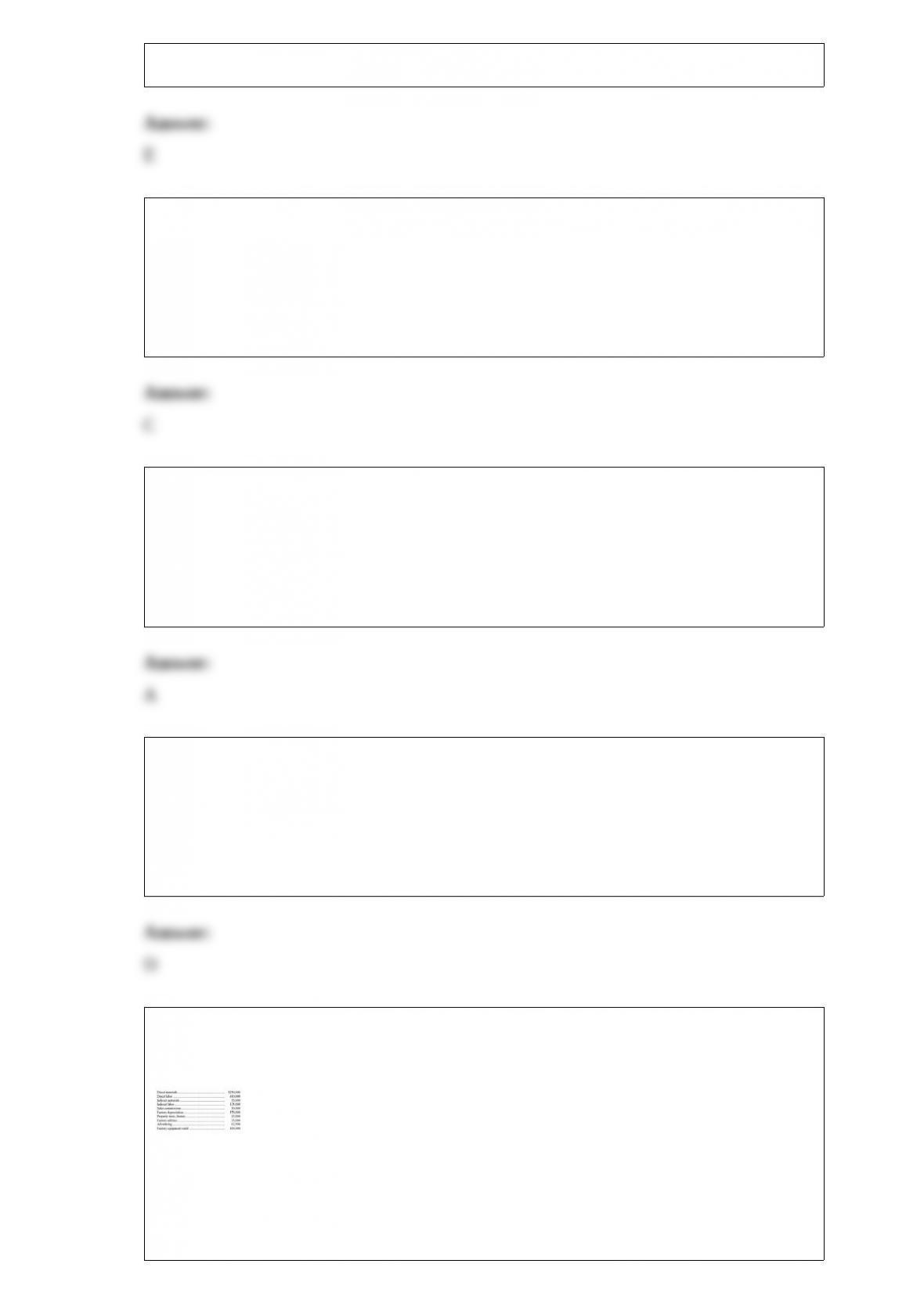

43) The following information comes from the records of Dina Co. for the current

period.

a. Compute the direct materials price and quantity variances, direct labor rate and

efficiency variances and state whether the variance is favorable or unfavorable.

b. Prepare the journal entries to charge direct materials and direct labor costs to goods

in process and the materials and labor variances to their proper accounts.

Factory overhead (based on budgeted production of 24,500 units)

Variable overhead $2.25/direct labor hour

Fixed overhead $1.95/direct labor hour

44) Cash flows from selling trading securities are usually reported in the statement of

cash flows as part of:

A.Operating activities

B.Financing activities

C.Investing activities

D.Noncash activities

E.None of these. This is not reported in the statement of cash flows

45) Continuous improvement:

A.Is a measure of profits

B.Is a measure of costs

C.Rejects the notion of “good enough.”

D.Is not applicable to most businesses

E.Is possible only in service businesses

46) A cost that remains constant over a limited range of volume, but increases by a

lump sum when volume increases beyond a maximum amount, is a(n):

A.Step-wise cost

B.Fixed cost

C.Curvilinear cost

D.Incremental cost

E.Opportunity cost

47) The sum of the variable overhead spending variance, the variable overhead

efficiency variance, and the fixed overhead spending variance is the:

A.Production variance

B.Quantity variance

C.Volume variance

D.Price variance

E.Controllable variance

48) A company issued a check for $7,900 in payment of the salaries expense for the last

half of the month. Identify the journal the transaction would be recorded in.

A.Cash disbursements journal

B.Sales journal

C.Cash receipts journal

D.Purchases journal

E.General journal

49) When a bond sells at a premium:

A.The contract rate is above the market rate

B.The contract rate is equal to the market rate

C.The contract rate is below the market rate

D.It means that the bond is a zero coupon bond

E.The bond pays no interest

50) Prepare the required general journal entries to record the following transactions for

the Bell Company.

a. Purchased $40,000 of raw materials on account.

b. Used $12,000 of direct materials in the production department.

c. Used $5,000 of indirect materials.

51) Partnership accounting:

A.Is the same as accounting for a sole proprietorship

B.Is the same as accounting for a corporation

C.Is the same as accounting for a sole proprietorship, except that separate capital and

withdrawal accounts are kept for each partner

D.Is the same as accounting for an S corporation

E.Is the same as accounting for a corporation, except that retained earnings is used to

keep track of partners’ withdrawals

52) Effective cash management involves applying all of the following cash

management principles except:

A.Encourage collection of receivables, offer discounts for payments received early

B.Keep only necessary levels of assets

C.Plan expenditures

D.Leave excess cash available for unexpected expenditures

E.Delay payment of liabilities until the last possible day

53) What are the types of adjusting entries used for prepaid expenses, depreciation and

unearned revenues?

54) What is the main difference between a cost center and a profit center?

55) A company records invoices at net amounts. On March 5, the company recorded

merchandise purchased, invoice price $17,000, terms 2/15, n/60. On March 24, this

company discovered that the invoice had been incorrectly filed and the discount had

been lost. The invoice was paid on April 1. Prepare journal entries to record these

events.

56) Beginning inventory plus the net cost of purchases is the ____________________.

57) Identify the differences between accrual accounting and cash basis accounting.

58) A graphic presentation of cost-volume-profit data is known as a

__________________ graph (or chart); this presentation is also sometimes called a

______________ chart.

59) The ________________________ methods use balance sheet relations to estimate

bad debts – mainly the relation between accounts receivable and the allowance amount.

60) David, Inc., is preparing its master budget for the second quarter. The following

sales and production data have been forecasted:

Finished goods inventory on March 31: 120 units

Raw materials inventory on March 31: 450 pounds

Desired ending inventory each month:

Finished goods: 30% of next month’s sales

Raw materials: 25% of next month’s production needs

Number of pounds of raw material required per finished unit: 4 lb.

How many pounds of raw materials should be purchased in April?

61) Explain how the owner of Cheezburger Network uses the accrual basis of

accounting.

62) A company needed a new building. It found a suitable location with an existing old

building on the land. The company reached an agreement to buy the land and the

building for $960,000 cash. The old building was demolished to make way for the

needed new building. Following is information regarding the demolition of the old

building and construction of the new one:

Prepare a single journal entry to record the above costs assuming all transactions are

paid in cash.