Investors should be wary of stock buybacks during down times because the resulting

decrease in shares and increase in earnings per share can be used to mask a slowdown

in earnings growth.

For a purchase commitment extending beyond the current fiscal year, if the market

price on the purchase date declines from the previous year-end price, the purchase is

recorded at the market price.

The choice of cost flow assumption (FIFO, LIFO, or average) does not depend on the

actual physical flow of the product.

An account receivable is recognized if the seller has a conditional right to receive

payment.

Unit LIFO is more costly to implement than dollar-value LIFO.

Which of the following is not a way of measuring the pension obligation?

a. Accumulated benefit obligation.

b. Vested benefit obligation.

c. Retiree benefit obligation.

d. Projected benefit obligation.

Lake Power Sports sells jet skis and other powered recreational equipment. Customers

pay one-third of the sales price of a jet ski when they initially purchase the ski, and then

pay another one-third each year for the next two years. Because Lake has little

information about the ability to collect these receivables, it uses the cost recovery

method to recognize revenue on these installment sales. In 2015, Lake began operations

and sold jet skis with a total price of $900,000 that cost Lake $450,000. Lake collected

$300,000 in 2015, $300,000 in 2016, and $300,000 in 2017 associated with those sales.

In 2016, Lake sold jet skis with a total price of $1,500,000 that cost Lake $900,000.

Lake collected $500,000 in 2016, $400,000 in 2017, and $400,000 in 2018 associated

with those sales. In 2018, Lake also repossessed $200,000 of jet skis that were sold in

2016. Those jet skis had a fair value of $75,000 at the time they were repossessed.

In 2017, Lake would recognize realized gross profit of:

a. $0.

b. $300,000.

c. $310,000.

d. $700,000.

Accumulated Other Comprehensive Income in the shareholders’ equity section of the

balance sheet reflects changes in the fair value of securities for which type of securities?

a. Securities available for sale.

b. Trading securities.

c. Consolidated securities.

d. Held-to-maturity securities.

Auerbach Inc. issued 4% bonds on October 1, 2016. The bonds have a maturity date of

September 30, 2026 and a face value of $300 million. The bonds pay interest each

March 31 and September 30, beginning March 31, 2017. The effective interest rate

established by the market was 6%. Assuming that Auerbach issued the bonds for

$255,369,000, what interest expense would it recognize in its 2016 income statement?

a. $0.

b. $3,830,535.

c. $5,107,380.

d. $7,661,070.

Coy, Inc., initially issued 200,000 shares of $1 par value stock for $1,000,000 in 2014.

In 2015, the company repurchased 20,000 shares for $200,000. In 2016, 10,000 of the

repurchased shares were resold for $160,000. In its balance sheet dated December 31,

2016, Coy, Inc.”s treasury stock account shows a balance of:

a. $ 0.

b. $ 40,000.

c. $100,000.

d. $200,000.

Udon Inc. adopted dollar-value LIFO (DVL) as of January 1, 2016, when it had an

inventory of $700,000. Its inventory as of December 31, 2016, was $777,000 at

year-end costs and the cost index was 1.05. What was DVL inventory on December 31,

2016?

a. $735,000.

b. $740,000.

c. $742,000.

d. $777,000.

You are the independent accountant assigned to the audit of Neophyte Company. The

company’s accountant, a graduate of Rival State University, has prepared financial

statements that contained the following questionable items:

a. The balance sheet reports land at $100,000. Included in this amount is a property held

for speculation at a cost of $30,000.

b. Current liabilities include $50,000 for long-term debt that is due in three months. The

company has received a suitable firm commitment to refinance the debt for five years

and intends to do so.

c. Investments in marketable securities include $20,000 in short-term, high-grade

commercial paper, which is a cash equivalent.

Required. Describe the appropriate balance sheet presentation for the above items.

A bond issue with a face amount of $500,000 bears interest at the rate of 10%. The

current market rate of interest is 11%. These bonds will sell at a price that is:

a. Equal to $500,000.

b. More than $500,000.

c. Less than $500,000.

d. The answer cannot be determined from the information provided.

The postretirement benefit obligation is the:

a. Future value of the estimated benefits during retirement.

b. Present value of the estimated benefits during retirement.

c. Fair value of the estimated benefits during retirement.

d. Actual value of estimated benefits during retirement.

Under the conventional retail method, which of the following are not included in the

denominator of the current period cost-to-retail conversion percentage?

a. Purchase returns.

b. Net markups.

c. Purchases.

d. Net markdowns.

When stock traded on an active exchange is issued for a machine:

a. No entry is recorded until restrictions are lifted.

b. An asset is recorded for the fair value of the stock.

c. An asset is recorded for the appraised value of the machine.

d. Paid-in capital is increased by the appraised value of the machine.

M Corp. has an employee benefit plan for compensated absences that gives each

employee 15 paid vacation days. Vacation days can be carried over indefinitely.

Employees can elect to receive payment in lieu of vacation days. At December 31,

2016, M’s unadjusted balance of liability for compensated absences was $30,000. M

estimated that there were 200 total vacation days available at December 31, 2016. M’s

employees earn an average of $150 per day. In its December 31, 2016, balance sheet,

what amount of liability for compensated absences is M required to report?

a. $ 0.

b. $ 30,000.

c. $225,000.

d. $450,000.

On February 1, 2016, Nell purchased $600,000 in zero-coupon bonds that mature on

February 1, 2036. The bonds pay no interest during the period of time they are

outstanding. The interest rate for such borrowings is at 12%.

Required: Calculate the price Nell paid for the bonds.

What was the average exercise price per share of stock issued under option plans in

2016?

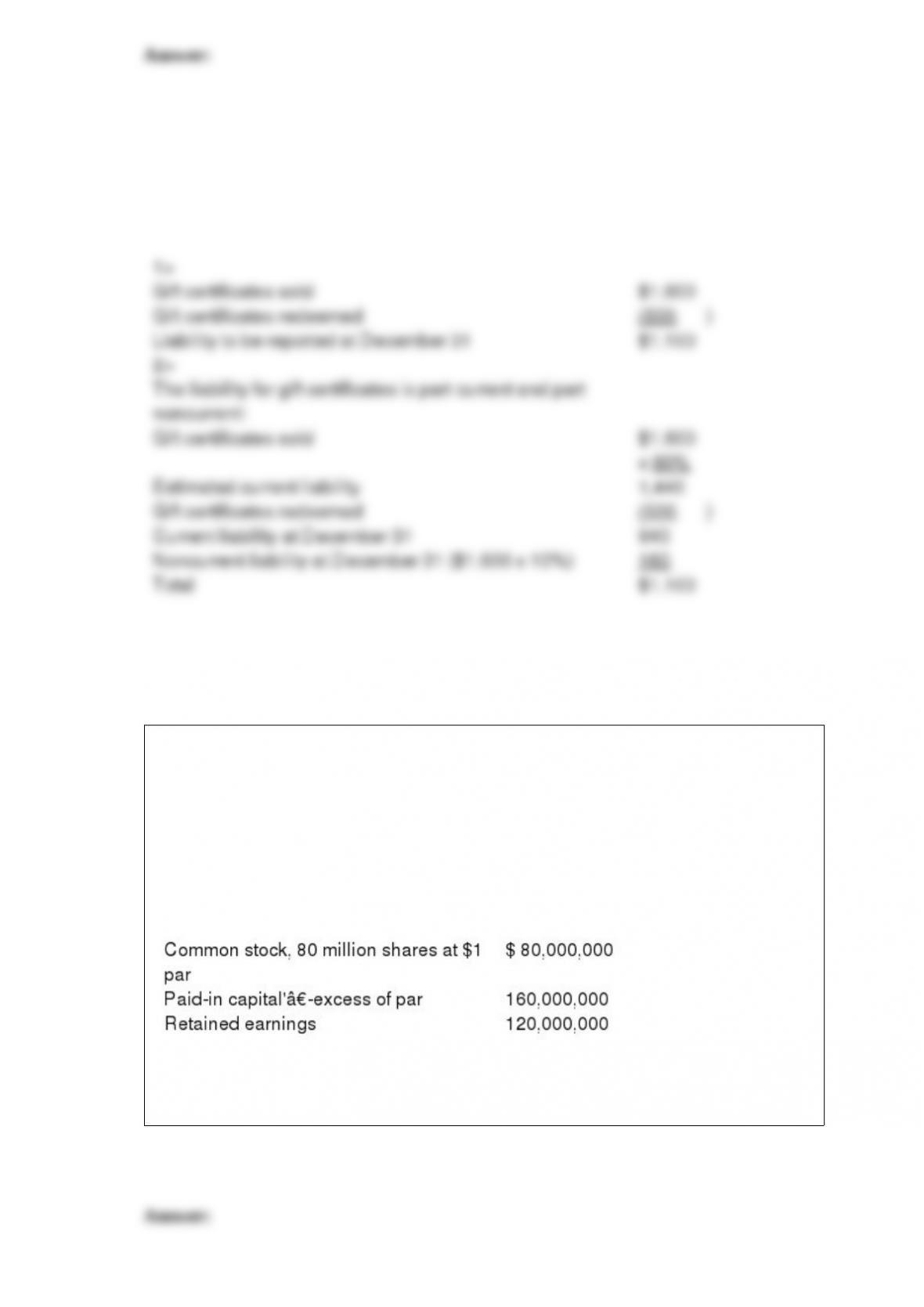

Mozart Music Co. began operations in December of 2016. The company sold gift

certificates during December in various amounts totaling $1,600. The gift certificates

are redeemable for merchandise within three years of the purchase date. However,

experience within the industry predicts that 90% of gift certificates will be redeemed

within one year. Certificates totaling $500 were presented for redemption during 2016

as part of merchandise purchases having a total retail price of $750.

Required:

1> Determine the liability for gift certificates to be reported in the December 31, 2016,

balance sheet.

2> What is the appropriate classification (current or noncurrent) of the liabilities at

December 31, 2016? Show calculations.

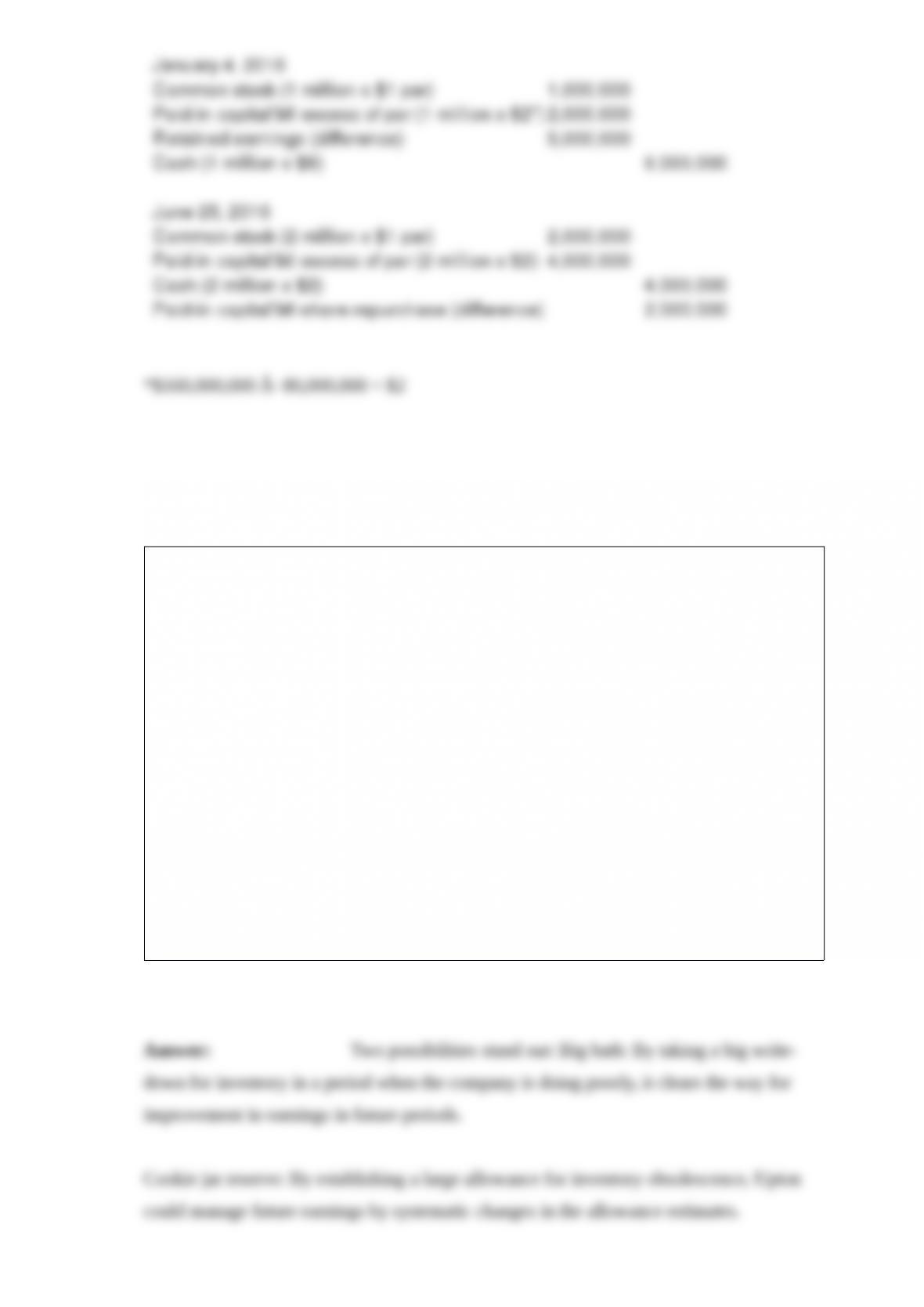

Cal Cookie Company (CCC) has 100 million shares of $1 par common stock

authorized. The transactions below caused changes in CCC’s outstanding shares.

January 4, 2016: Repurchased and retired 1 million shares at $8 per share.

June 25, 2016: Repurchased and retired 2 million shares at $2 per share.

Prior to the transactions, CCC’s shareholders’ equity included the following:

Required:

Record entries for the above transactions.

The following disclosure note appeared in the 2016 annual report to shareholders of

Upton Systems Inc.

Inventories are stated at the lower of cost and net realizable value. Cost is computed

using standard cost, which approximates actual cost, on a first-in, first-out basis. The

Company provides inventory allowances based on excess and obsolete inventories.

Another disclosure note in the annual report stated:

The Company recorded a provision for inventory, including purchase commitments,

totaling $1.40 billion during fiscal 2016, which included an additional excess inventory

charge as previously discussed. This additional excess inventory charge was due to a

sudden and significant decrease in demand for the Company’s products and was

calculated in accordance with the Company’s accounting policy.

A skeptic may conclude that Upton’s policy and practices threaten earnings quality.

Discuss how it may do so.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct number code for the term.

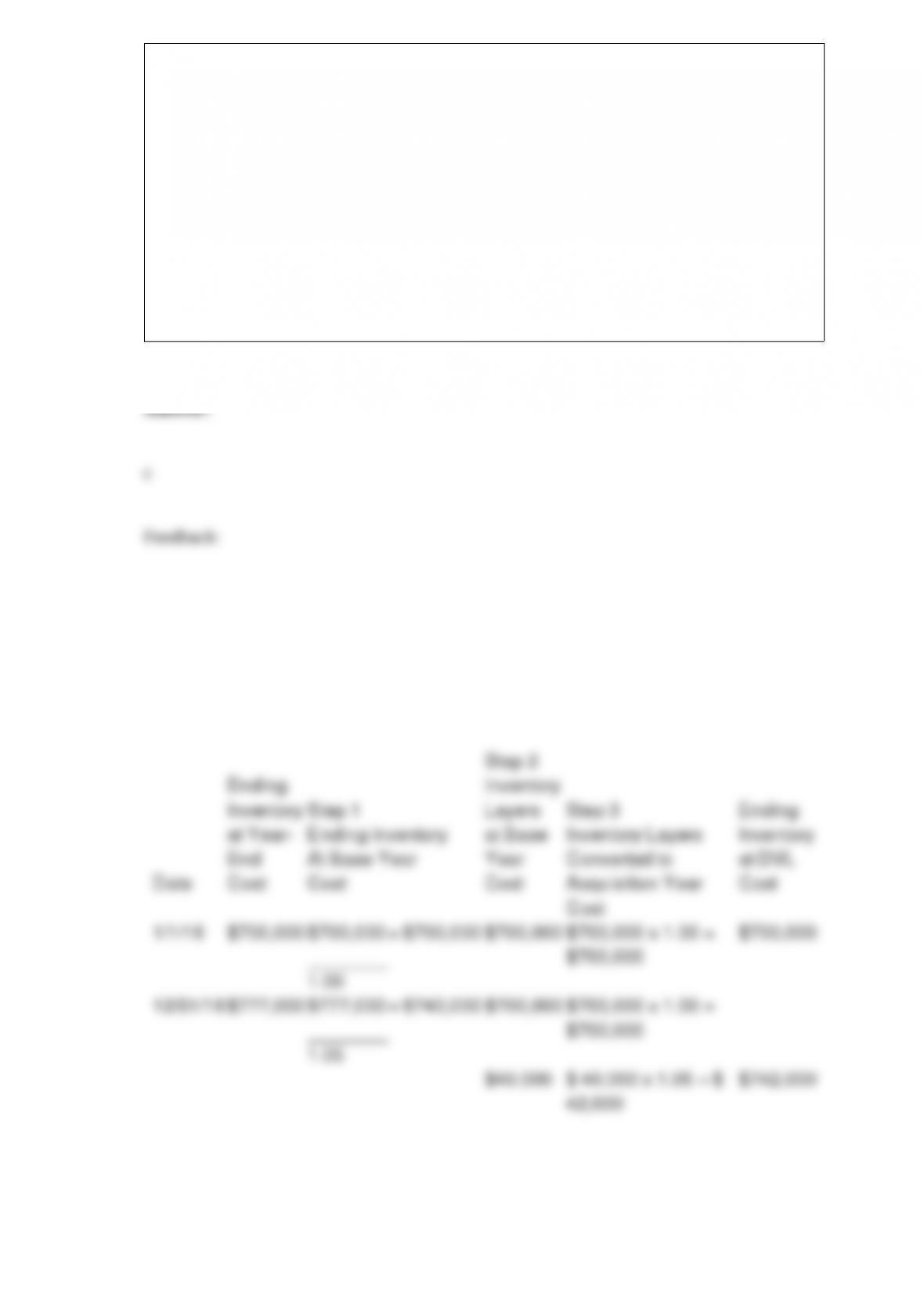

The Genworth Company adopted the dollar-value LIFO method on January 1, 2016

when the inventory value of its one inventory pool was $450,000. The company

decided to use an external index, the Consumer Price Index (CPI), to adjust for changes

in the cost level. On January 1, 2016, the CPI was 280. On December 31, 2016,

inventory valued at year-end cost was $504,000 and the CPI was 294. Required:

Calculate the inventory value at the end of 2016 using the dollar-value LIFO method.

On June 30, 2016, Blondie Fixtures was considering alternatives to bolster its cash

position. Option One called for transferring $400,000 in accounts receivable to

Dogwood Finance Company without recourse for a 5% fee. Option Two calls for

Blondie to transfer the $400,000 in receivables to Dogwood with recourse. Dogwood’s

charges a 4% fee for receivables factored with recourse. Option Two meets the

conditions to be considered a sale, but Blondie estimates a $3,000 recourse liability.

Under either option, Dogwood will immediately remit 90% of the factored receivables

to Blondie, and retain 10%. When Dogwood collects the remaining receivables, it

remits the amount, less the fee, to Blondie. Blondie estimates that the fair value of the

final 10% of the receivables is $25,000 (ignoring the factoring fee).

Required:

1> Prepare any necessary journal entry or entries if receivables are factored under

Option One.

2> Prepare any necessary journal entry or entries if receivables are factored under

Option Two.

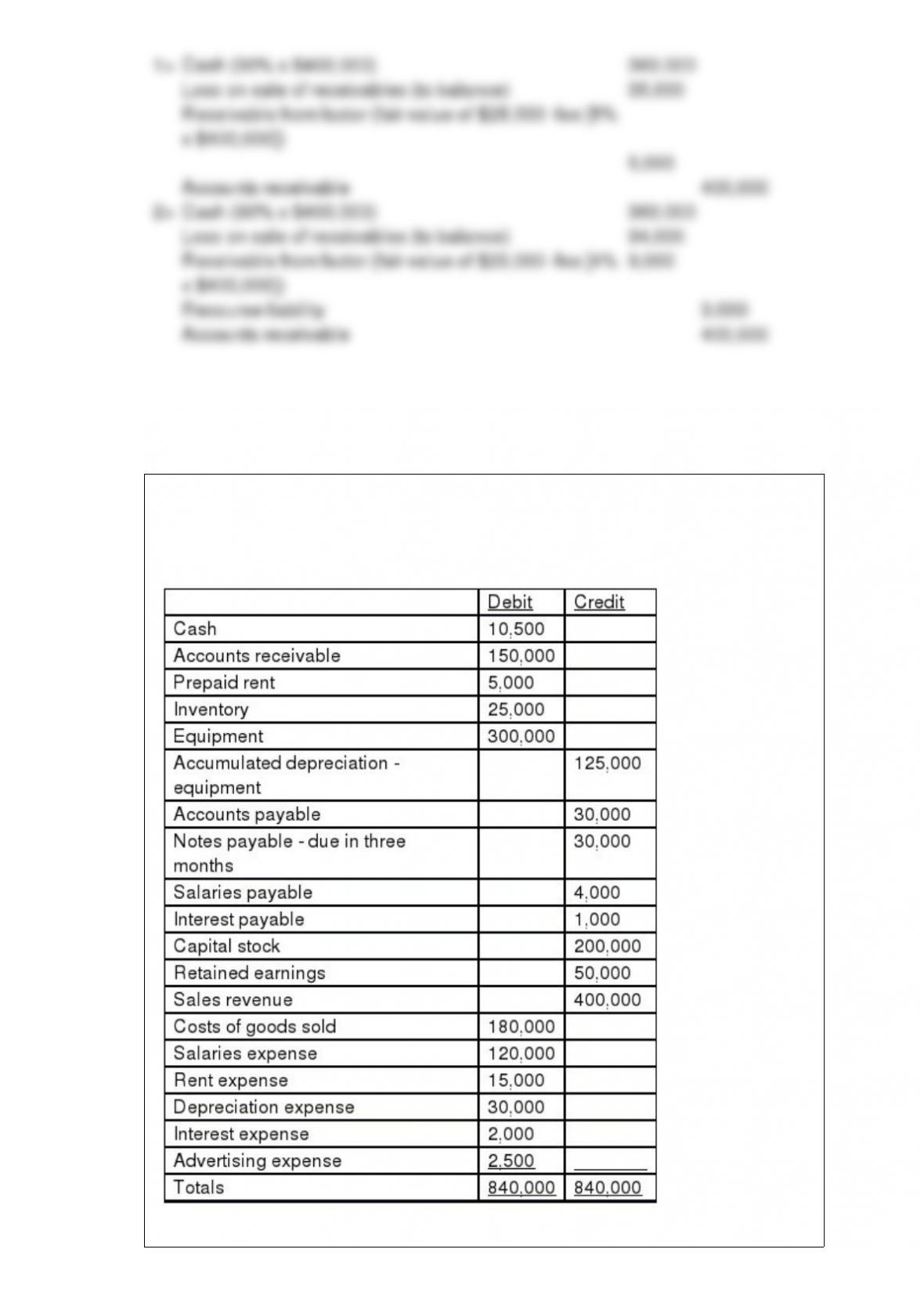

The adjusted trial balance for China Tea Company at December 31, 2016, is presented

below:

Prepare the closing entries for China Tea Company for the year ended December 31,

2016.