1) Pardo Corporation paid $140,000 for a 70% interest in Spedeal Inc. on January 1,

2011, when Spedeal had Capital Stock of $50,000 and Retained Earnings of $100,000.

Fair values of identifiable net assets were the same as recorded book values. During

2011, Spedeal had income of $40,000, declared dividends of $15,000, and paid $10,000

of dividends. On December 31, 2011, the consolidated financial statements will show

A) investment in Spedeal account of $170,000

B) investment in Spedeal account of $165,000

C) consolidated goodwill of $50,000

D) consolidated dividends receivable of $5,000

2) On January 1, 2010, Shrimp Corporation purchased a delivery truck with an expected

useful life of five years, and a salvage value of $8,000. On January 1, 2012, Shrimp

sold the truck to Pacet Corporation. Pacet assumed the same salvage value and

remaining life of three years used by Shrimp. Straight-line depreciation is used by both

companies. On January 1, 2012, Shrimp recorded the following journal entry:

Debit Credit

Cash50,000

Accumulated depreciation18,000

Truck53,000

Gain on Sale of Truck15,000

Pacet holds 60% of Shrimp. Shrimp reported net income of $55,000 in 2012 and Pacet’s

separate net income (excludes interest in Shrimp) for 2012 was $98,000.

In the eliminating/adjusting entries on consolidation working papers for 2012, the Truck

account was

A) debited for $3,000

B) credited for $3,000

C) debited for $15,000

D) credited for $15,000

3) When considering an acquisition, which of the following is NOT a method by which

one company may gain control of another company?

A) Purchase of the majority of outstanding voting stock of the acquired company

B) Purchase of all assets and liabilities of another company

C) Purchase the assets, but not necessarily the liabilities, of another company

previously in bankruptcy

D) All of the above methods result in a company gaining control over another company

4) In reference to the potential taxation of an estate, which of the following statements

is correct?

A) An estate may be subject to taxation at both the state and federal level

B) The taxable amount of an estate is based on the book values of all estate assets at the

date of death

C) The estate value is not reduced by such expenses as funeral expenses, bequests to

qualified charities, or state-level taxes

D) Taxable estate assets do not include proceeds from life insurance policies

5) On January 1, 2011, the General Fund contributes $200,000 cash to the Internal

Service Fund. On January 1, 2011, the General Fund also loans $100,000 cash to the

Internal Service Fund. On January 1, 2011, what journal entry does the Internal Service

Fund prepare?

A) debit Cash $300,000, credit Other Financing Sources $300,000

B) debit Cash $300,000, credit Other Financing Sources $200,000, credit Advance from

General Fund $100,000

C) debit Cash $300,000, credit Advance from General Fund $300,000

D) debit Cash $300,000, credit Nonreciprocal Transfer from General Fund $200,000,

credit Advance from General Fund $100,000

6) In a nongovernmental, nonprofit hospital, contractual adjustments are

A) the discounted rate given to hospital employees

B) discounts arranged with third-party payors

C) recorded as a deduction from revenue or as an expense

D) additional amounts paid by select group participants

7) Page Corporation acquired a 60% interest in Ace Corporation at a price $40,000 in

excess of book value and fair value on January 1, 2010 . On the same date, Ace

acquired a 70% interest in Bader Corporation at a price $30,000 in excess of book value

and fair value. The excess purchase cost paid by Page and Ace was attributed to

goodwill. Separate net incomes (excluding investment income) for the three affiliates

for 2010 are as follows: Page, $500,000, Ace, $300,000, and Bader, $400,000.

Page’s controlling interest share of consolidated net income for 2010 is

A) $808,000

B) $848,000

C) $920,000

D) $960,000

8) In reference to international accounting for goodwill, U.S. companies have

complained that past U.S. accounting rules for goodwill placed them at a disadvantage

in competing against foreign companies for merger partners. Why?

A) Previous rules required immediate write off of goodwill which resulted in a one-time

expense that was not required under international rules

B) Previous rules required amortization of goodwill which resulted in an ongoing

expense that was not required under international rules

C) Previous rules did not permit the recording of goodwill, thus resulting in a lower

asset base than international counterparts would recognize

D) All of the above are correct

9) A gift-in-kind, for which the not-for-profit entity has no discretion on disposition,

should be accounted for by the not-for-profit, nongovernmental entity as

A) a special purpose contribution

B) an exchange transaction

C) an agency transaction

D) a conditional promise to give

10) In a Chapter 11 case, the debtor corporation filing the petition may continue in

possession of the corporation’s property, and is referred to as a(n)

A) examiner

B) trustee

C) liquidator

D) debtor in possession

11) Tank Corporation, a U.S. manufacturer, has a June 30 fiscal year end. Tank sold

goods to their customer in Columbia on May 27, 2011 for 18,000,000 Columbian pesos.

The customer agreed to pay pesos in 60 days. When the customer wired the funds to

Tank on July 26, Tank held them in their bank account until July 31 before selling them

and converting them to U.S. dollars. The following exchange rates apply:

May 27$0.00055

June 30$0.00052

July 26$0.00058

July 31$0.00056

Required:

Record the journal entries related to the dates listed above. If no entry is required, state

“no entry.”

12) On January 1, 2011, Klode Corporation acquired an 80% interest in Savy Company

for $400,000 when Savy’s stockholders’ equity was $500,000; with Common stock

$400,000 and Retained earnings $100,000.

On January 1, 2011, Savy purchased a 10% interest in Klode for $50,000 when Klode’s

total stockholders’ equity was $500,000; with Common stock $400,000 and Retained

earnings $100,000.

The following data was available for the year ending December 31, 2011:

Klode CompanySavy Company

Net income$70,000$50,000

Dividends00

Use the conventional approach to account for the mutually-held stock. Assume there

were no book value/fair value differentials for each investment. The separate net

incomes do not include investment income.

Required:

1> Prepare the journal entry for Klode on January 1, 2011 .

2> Prepare the journal entry for Savy on January 1, 2011 .

3> Prepare the journal entry to record the constructive retirement of 10% of Klode’s

outstanding stock due to Savy’s purchase of Klode’s stock.

4> Determine the incomes of Klode and Savy on a consolidated basis with mutual

income for 2011 using simultaneous equations.

5> What is controlling interest share of consolidated net income and noncontrolling

interest shares for 2011?

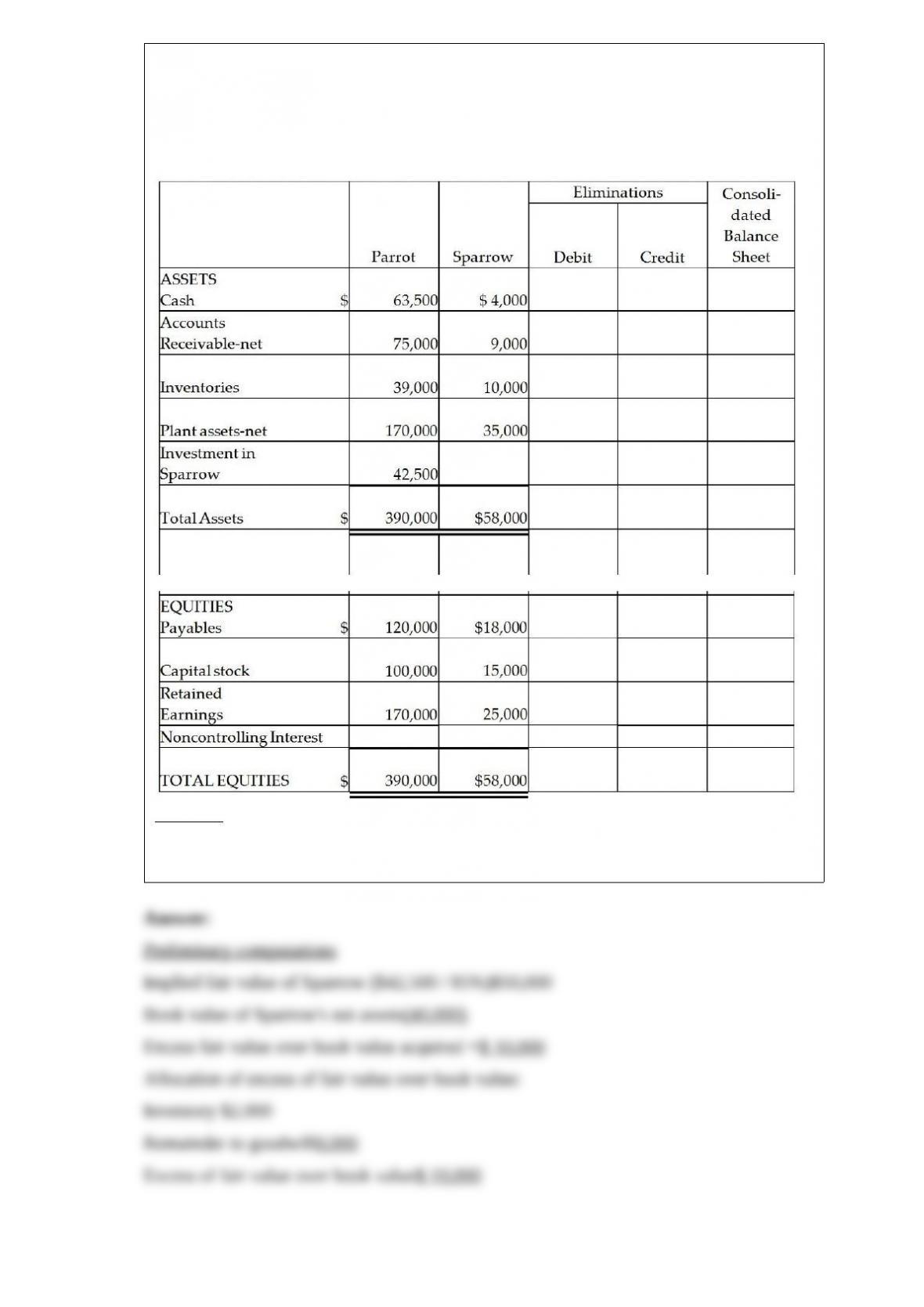

13) Parrot Inc. acquired an 85% interest in Sparrow Corporation on January 2, 2011 for

$42,500 cash when Sparrow had Capital Stock of $15,000 and Retained Earnings of

$25,000. Sparrow’s assets and liabilities had book values equal to their fair values

except for inventory that was undervalued by $2,000. Balance sheets for Parrot and

Sparrow on January 2, 2011, immediately after the business combination, are presented

in the first two columns of the consolidated balance sheet working papers.

Required:

Complete the consolidation balance sheet working papers for Parrot and subsidiary at

January 1, 2011 .

14) A summary balance sheet for the partnership of Maddy, Nelson and Olsen on

December 31, 2011 is shown below. Partners Maddy, Nelson and Olsen allocate profit

and loss in their respective ratios of 9:6:10.

Assets

Cash$ 50,000

Marketable securities120,000

Inventory75,000

Land80,000

Building-net400,000

Total assets$725,000

Equities

Maddy, capital$425,000

Nelson, capital225,000

Olsen, capital75,000

Total equities$725,000

The partners agree to admit Poosh for a one-tenth interest. The fair market value for

partnership land is $180,000, and the fair market value of the inventory is $150,000.

Required:

1>Record the entry to revalue the partnership assets prior to the admission of Poosh.

2>Calculate how much Poosh will have to invest to acquire a 10% interest.

3>Assume the partnership assets are not revalued. If Poosh paid $200,000 to the

partnership in exchange for a 10% interest, what is the bonus that is allocated to each

partner’s capital account?

15) The Leo, Mark and Natalie Partnership had the following capital balances and

profit/loss sharing percentages:

BalanceSharing %

Leo$200,00050%

Mark$160,00040%

Natalie$140,00010%

Newsome is going to buy into the partnership by paying $200,000 for a 20% ownership

in the partnership.

Required:

1>If Newsome pays the partnership directly, what are the four partner capital balances

immediately following Newsome’s admission to the partnership using the bonus

method? Assume the partnership assets are not revalued.

2>If Newsome pays the partnership directly, what are the four partner capital balances

immediately following Newsome’s admission to the partnership using the goodwill

method? Assume the partnership assets are revalued. The $200,000 amount paid by

Newsome is fair value for a 20% share of the partnership.

16) On February 1, 2011, George, Hamm, and Ishmael began a partnership in which

George and Ishmael each contributed cash of $25,000; and Hamm contributed property

with a fair value of $50,000 and a tax basis $40,000. Hamm receives a 5% bonus of

partnership income. George and Ishmael receive salaries of $10,000 each. The

partnership agreement of George, Hamm, and Ishmael provides that all partners receive

5% interest on capital, and that profits and losses of the remaining income be

distributed to George, Hamm, and Ishmael by a 1:3:1 ratio.

Required:

Prepare a schedule to distribute $25,000 of partnership net income to the partners.

17) For each of the following events or transactions, identify the fund or funds that will

be affected.

1>A city government charges a fee for the use of the municipal golf course.

2>Interest is paid on state government revenue bonds.

3>A motor pool was established to handle the vehicle needs of a county government.

4>Paid salaries for general governmental employees.

5>Accrued salaries for general governmental employees.

18) Trustin Corporation is in a Chapter 7 bankruptcy liquidation. For each of the

following transactions, show the journal entry that would be required by the trustee of

the estate.

1>An electric bill is received for $1,000 which had not yet been recorded by Trustin.

2>Inventory recorded net at $18,000 is sold for $16,000 cash.

3>Recorded patents in the amount of $7,000 are determined to be worthless and are

written off.

4>Equipment recorded net at $24,000 is sold for $20,000 cash.

5>A building recorded net at $78,000 is sold for $87,000 cash.

6>Trustee fees of $2,500 are accrued.

7>The fully secured mortgage is paid in the amount of $70,000.

8>Wages payable that were recorded in the amount of $9,000 are paid.

9>An equipment lease, which was recorded as prepaid equipment lease, is cancelled

and a $1,500 refund is received.

10>Accounts receivable amounting to $12,000 are collected, and an additional $3,000

is determined to be uncollectible.

19) Piglet Incorporated purchased 90% of the outstanding stock of Sourgrape Company

several years ago at book value. At January 1, 2010, Sourgrape sold land with a book

value of $30,000 to Piglet at its fair market value of $40,000. At the same time,

Sourgrape sold the building that was on the land to Piglet. The building had a book

value of $80,000 and was sold at its fair value of $120,000. The building had a

remaining useful life of 8 years and is depreciated using the straight-line method. The

building has no salvage value. On January 1, 2012, Piglet sold the land and building to

a third party. The sales price was allocated so that the land was sold for $50,000 and the

building was sold for $150,000. Income statements for Piglet and Sourgrape for the

year ended December 31, 2012 are summarized below:

Piglet Sourgrape

Sales$252,000 $90,000

Gain on sale of land and building40,000

Cost of sales(140,000)(40,000)

Depreciation expense(60,000)(20,000)

Other expenses(20,000)(10,000)

Net income$72,000 $20,000

Required:

Prepare the eliminating/adjusting entries related to the land and building on the

consolidated working papers on the following dates:

1> December 31, 2010

2> December 31, 2011

3> December 31, 2012

20) Avery died testate early in 2011 . The following transactions occurred relating to

Avery’s estate.

1>Avery’s estate included bonds with a fair (market) value of $120,000. On the date of

Avery’s death, there was $2,000 of accrued but unpaid interest. Two months after

Avery’s death, a check arrived in the amount of $3,000, representing the normal

semiannual interest payment.

2>Avery’s will stated a specific transfer to the Bird Sanctuary in the amount of $10,000.

Avery’s estate should be adequate to cover all obligations and devises, and the amount

is paid.

3>Funeral expenses amounted to $12,500.

4>A bank statement is received from the First National Bank indicating a cash balance

of $8,600. This bank account was not known or included on the estate inventory.

5>Probate fees are paid to the court amounting to $900.

Required:

Prepare the journal entries for the listed transactions. Disregard the impact of estate and

income taxes.