Confirmation is most likely to be a relevant form of evidence with regard to assertions

about accounts receivable when the auditor has concerns about the accounts receivable’s

A) valuation.

B) classification.

C) existence.

D) completeness.

For listed clients, the audit committee should approve both the appointment of the

auditor and

A) all services that the PA firm provides to the client.

B) an engagement that might affect the appearance of independence, such as design of

control systems.

C) any services that are provided for senior management.

D) the material that is included in the management letter by the PA firm.

If the auditor is appointed after the year end of the client, the auditor

A) should qualify the audit opinion for the inventory balance and cost of sales.

B) could attend a current perpetual inventory count and roll backward with the records.

C) should do an inventory count as soon as he is appointed.

D) will inquire with management of the company about the inventory count performed

at year end.

A client representation letter is a written statement from a non-independent source and

therefore

A) cannot be regarded as reliable evidence on its own.

B) can be regarded as reliable evidence only if the auditor finds strong internal controls.

C) can be regarded as reliable evidence if the high-level corporate officials who sign it

are trustworthy.

D) needs to be confirmed by an outside, independent source such as a financial

institution, or law firm.

Simon owns a clothing store, Simonello. Simonello recently purchased a material

amount fabrics from Simonique Inc., a textile company also owned by Simon. With

regards to this transaction, the auditors should

A) request a confirmation from Simonique that the transaction took place.

B) inspect the textile received in the warehouse to ensure that the amount sent equals

the amount ordered.

C) qualify the audit report as this puts into question management’s integrity.

D) verify that the business relationship is disclosed in the financial statements.

As part of the review for subsequent events, the auditor will review financial statements

prepared after the balance sheet date. The purpose of this review is to examine changes

after year end and to look for

A) errors in capital versus maintenance charge allocations that occurred after the year

end.

B) subsequent payments to accounts payable and long term debt.

C) subsequent receipts in accounts receivable, especially for the larger customers.

D) changes in the business relative to results for the same period in the year under audit.

A risk of material misstatement in accounts receivable associated with the accuracy

balance-related audit objective is that ‘sales recorded at the incorrect price result in

revenue and accounts receivable that are over or under stated.” Which of the following

tests of detail of balances would respond to this risk?

A) select a sample of master file change forms and verify that all sales prices changes

were appropriately authorized

B) use audit software to match sales invoice price details to authorized prices in the

sales price master files

C) inquire of management with respect to the procedures used to update sales price

master file

D) match shipping details for a sample of invoices to the invoice details, on an item by

item basis

Fabio recently sold his restaurant for $650,000, the value of the net assets as reported

on the balance sheet. After the sale, Fabio realized that he could’ve sold the restaurant

for as much as $950,000 as the fair value of the assets was $300,000 higher than what

was reported on the balance sheet. Fabio is suing the auditors for his loss. The auditor’s

best defence is

A) absence of a misstatement.

B) lack of duty.

C) no damages.

D) absence of causal connection.

The information systems audit specialist on your audit team has indicated that the

general controls over program changes are inadequate for all application cycles. What

impact does this have upon your audit of sales invoice processing?

A) The auditor could potentially rely upon only manual controls.

B) Only interdependent controls should be considered for control testing.

C) It is likely that calculations, such as extensions, are performed consistently and

accurately throughout the year.

D) Unauthorized access to information recorded in the master files is likely.

Management’s objectives with respect to internal control include

A) having reasonable assurance that the financial statements are in accordance with

IFRS or ASPE.

B) ensuring that all policies and procedures are clearly documented to reduce employee

training costs.

C) preventing fraud and illegal activities at all costs.

D) providing reasonable assurance that the goals and objectives important to the entity

have been met.

Gabori Company would like to pay less income tax this year. It decided that it could do

this by understating its inventory values, increasing costs of goods sold. This was done

by deliberately pricing the inventory at incorrect amounts, so that it would be shown at

a lower value than it was really worth (for example, items worth five dollars each were

shown at fifty cents each). Which management assertion has been violated?

A) valuation

B) accuracy

C) statement presentation

D) completeness

In auditing the imprest payroll account, which of the following procedures will take the

least amount of auditor time?

A) tests of controls

B) risk analysis and obtaining an understanding of controls

C) analytical procedures

D) tests of details of balances

An investor suing an auditor for not discovering that the financial statements of a

company are materially misstated is an example of

A) criminal liability.

B) fiduciary duty.

C) third party liability.

D) liability to client under common law.

Proper accounting requires that an account receivable must be written off by the client

when

A) the client company concludes that an amount is no longer collectible.

B) the customer files for bankruptcy.

C) a collection agency cannot inspire the customer to pay the debt.

D) the account is at least six months old.

When the auditor examines the client’s documents and records to support recorded

transactions or amounts, it is commonly referred to as

A) inquiry.

B) confirmation.

C) vouching.

D) physical examination.

When the CICA Handbook is silent on an auditing issue, which of the following is the

best of other authoritative sources that the auditor could use?

A) audit technique studies

B) audit firm practice manuals

C) past practice at the client

D) reference to audit standards partner

The internal audit group typically reports directly to the

A) board of directors.

B) management of the company.

C) external auditor

D) audit committee.

A useful starting point for becoming familiar with the client’s inventory is for the

auditor to

A) obtain and review industry ratios.

B) review accounting theory covering special problems, such as gas and oil accounting,

or lease-purchase agreements.

C) read client’s Accounting Manual.

D) tour the client’s facility.

A common test of details of balances procedure for notes payable is “examine duplicate

copies of notes to determine whether notes were dated on or before the balance sheet

date.” Which audit assertion is this test of detail associated with?

A) allocation (accuracy)

B) allocation (cut-off)

C) existence

D) completeness

The information systems audit specialist on your audit team has indicated that the

general controls over program changes are excellent for all application cycles. What

impact does this have upon your audit of sales invoice processing?

A) Generalized audit software should be used to select a sample of sales transactions

for control testing.

B) Tests of controls should be omitted; only substantive tests may be conducted.

C) There could be problems with the accuracy of calculations for sales taxes and goods

and excise taxes.

D) The auditor can place reliance upon the programs performing sales calculations.

To do an audit, it is necessary to have information in a verifiable form and some criteria

by which the auditor can evaluate the information.

Required:

A) What information and criteria would a public accounting firm use when auditing a

company’s financial statements?

B) What information and criteria would a Canada Revenue Agency auditor use when

auditing that same company’s tax return?

C) What information and criteria would an internal auditor use when performing an

operational audit to evaluate whether the company’s computerized payroll processing

system is operating efficiently and effectively?

It is important for the auditor to obtain a good understanding of the industry of the

client to develop a client risk profile. If the auditor is looking at a client in the fashion

clothing industry, a risk specific to the industry would be

A) the high risk of poor governance and management oversight.

B) the high risk of defective products.

C) the high risk of obsolescence of their inventory.

D) the volatility in the stock market with regards to common stock.

The Rules of Professional Conduct require a successor auditor to communicate with the

previous auditor. The primary concern in this communication is

A) to acquire information which will help the successor auditor determine whether the

client management has integrity.

B) to learn about the client by examining the predecessor’s working papers.

C) to enable the successor to perform a more efficient audit.

D) to save the successor auditor time and money in gathering data.

The appropriate test of controls for separation of duties is

A) documentation.

B) confirmation.

C) examination.

D) observation.

A) Discuss three important differences between the human resources and payroll cycle

and other cycles in a typical audit.

B) Describe each of the six business functions in a typical human resources and payroll

cycle.

C) Describe each of the primary documents and records used in the timekeeping and

payroll preparationfunction in the payroll and personnel cycle.

D) Discuss each of the primary documents and records used in the (1) payment of

payroll function, and (2) preparation of employee withholdings and benefits remittance

forms function in the payroll and personnel cycle.

The test of details of balance procedure which requires the auditor to account for

unused inventory tag numbers to make sure none have been omitted is an attempt to

satisfy the objective of

A) allocation.

B) existence.

C) completeness.

D) accuracy.

The provincial institutes’ Rules of Professional Conduct state, in part, that a public

accountant should maintain integrity and due care. Integrity in the Rules refers to a

public accountant’s

A) ability to maintain an impartial attitude on all matters that come under the public

accountant’s review.

B) ability to distinguish independently between accounting practices that are acceptable

and those that are not.

C) ability to be unyielding in all matters dealing with auditing procedures.

D) reputation for honesty and fair dealing.

Serena is the assistant controller of Opus Inc. As a result of a recent expansion the

controller has been very busy and delegated the signing authority of the cheques to

Serena. Further, due to the cash accountant leaving on maternity leave, Serena was

asked to perform the bank reconciliation until they found someone to replace the cash

accountant.

Serena is a qualified accountant and has been able to handle all of these additional

tasks. However, she asked her boss for a raise to compensate her for the additional

responsibilities that she currently has. Her boss indicated that this was only temporary

and the company could not afford a raise for now.

Serena created a vendor in the system with her home address. She has been paying this

vendor $2,000 for the past 3 months as a means of compensating herself. This theft has

yet to be discovered by Opus.

Required:

A) What internal controls are missing to enable the theft to occur?

B) What audit procedures might detect the theft?

Management assertions are

A) stated in the footnotes to the financial statements.

B) implied or expressed representations about the accounts in the financial statements.

C) explicitly expressed representations about the financial statements.

D) provided to the auditor in the engagement letter, but are not disclosed on the

financial statements.

Which of the following scenarios regarding a lawsuit filed against a client by a third

party would qualify as a “contingent liability”? A lawsuit has been filed

A) but not yet resolved.

B) and concluded with the client winning.

C) and concluded with a third party winning an award of $100,000, but the client hasn’t

paid yet.

D) and concluded with a third party winning an award of $100,000, which the client

paid after the balance sheet date but before the statements are issued.

When reading the corporate minutes, the auditor obtained information regarding the

loans that were authorized for borrowing. What audit step would the auditor likely

conduct with this information?

A) trace the authorized amounts to the bank statements

B) verify that notes payable have been recorded

C) calculate interest payable as of the end of the year

D) contact a credit rating agency to determine the rating of the lender

Each of the following situations involves a possible violation of the provincial

institutes’ Rules of Professional Conduct. For each situation, (1) decide whether or not

the Rules have been violated, and (2) briefly explain how the situation violates (or does

not violate) the Rules.

A) Johnny Line has a successful dentistry practice in Calgary. Johnny has

recommended one of his patients to Leslie King, public accountant. To show gratitude

for the referral, Leslie has agreed to pay Johnny 5% of the fee for audit services

rendered by Leslie to Johnny’s patient. Leslie discloses the payment agreement to her

new client.

Violation? Yes No

Explanation:

B) The accounting firm of Bayer & Peng, public accountants, is negotiating a fee with a

new audit client. They agree the client will pay $75,000 if Bayer & Peng issues a clean,

unqualified opinion, $50,000 if a qualified opinion is issued, $40,000 if an adverse

opinion is issued, and $10,000 if a denial of opinion is issued.

Violation? Yes No

Explanation:

C) Don Smith, public accountant, takes part in the audit of Shaw Corporation. Don is

not a partner or a manager in the public accounting firm, and does not own any stock in

Shaw Corporation. Don’s five year-old daughter, Betty Lou, received one share of Shaw

Corporation’s common stock for her fifth birthday. The stock was a gift from Betty

Lou’s grandmother. Betty Lou treasures that share of stock and is absolutely unwilling

to part with it.

Violation? Yes No

Explanation:

D) On August 5, 2012, Page Dane, public accountant, issued the audit report on Borhut

Corporation’s June 30, 2012 financial statements. On August 30, 2012, Borhut paid

Page’s audit fee with stock rather than cash. Page sold the stock on September 15, 2012,

two months prior to the beginning of the planning phase for the audit of the June 30,

2013, financial statements.

Violation? Yes No

Explanation:

When comparing the reliability of external versus internal documents, the external

documents are generally considered

A) more reliable.

B) less reliable.

C) equally reliable.

D) unreliable.

During your lunch, your audit team went to a local mall, in the food court, since they

needed to be quick today. You dropped off a photofinishing film at a film developer,

saying that you would pick it up after work that day. After telling you that she preferred

using her digital camera to using regular film, your supervisor said,

“Next week, you are going to be working at a client that just happens to be a group of

photography stores. Tell me, what controls do you think should be programmed into the

cash register to help ensure that sales transactions are accurate and complete?”

Required:

Answer your supervisor’s question.

Discuss the audit tests the auditor would use to audit capital assets acquired in prior

years.

Discuss the ways the accounting profession and society encourage public accountants to

conduct themselves in a professional manner; i.e., the factors that influence the ethical

conduct of audit practitioners.

Discuss the purposes of tests of controls and tests of details of balances. Give an

example of each.

Outline the three performance standards of CICA Handbook section 5025, “Standards

for Assurance Engagements.”

Besides the search for contingent liabilities and the review for subsequent events, the

auditor has four important final evidence accumulation responsibilities, all of which are

required by current professional auditing standards. Discuss each of these four

responsibilities.

List four specific matters that should be included in a client representation letter.

Identify the reporting standards for compilation engagements.

The following are audit procedures in the sales and collection cycle.

1. Inspect a sample of shipping documents to determine if each has a sales invoice

number included on it.

2. Discuss with the sales manager whether any sales allowances have been granted after

the balance sheet date that may apply to the current period.

3. Add the columns on the aged trial balance and compare the total with the general

ledger.

4. Observe whether the controller makes an independent comparison of the total in the

general ledger with the trial balance of accounts receivable.

5. For the month of May, count the approximate number of shipping documents filed in

the shipping department, and compare the total with the number of sales invoices in the

sales journal.

6. Compare the date on a sample of shipping documents throughout the year with

related duplicate sales invoices and the accounts receivable master file.

7. Examine a sample of customer orders and see if each has a credit authorization.

8. Send letters directly to former customers whose accounts have been written off as

uncollectible to determine if any have actually been paid.

9. Examine the master file of accounts receivable to see if each has an indication of “C”

for a regular customer, “N” for interest-bearing receivables, and “R” for related parties.

10. Compare the date on a sample of shipping documents a few days before and after

the balance sheet date with related sales journal transactions.

Required:

For each procedure, identify the type of evidence being used. For each procedure,

identify either the transaction-related audit objective(s) being met or the balance-related

audit objective(s) being met.

State each of the five specific transaction-related audit objectives for acquisitions and,

for each objective, describe one common test of transactions.

A financial statement review emphasizes four broad areas, one of which is to “Perform

analytical procedures.” State the other three areas emphasized.

Your firm has been the auditor of Chappello Design and Construction Limited for

several years. During the current year, a consultant on staff at your firm assisted

Chappello in the selection and implementation of a new computer system. The audit

staff were not involved in this process.

The new system was an enterprise wide system that was to be implemented without

modification using the direct cut-over approach (the old system was discontinued and

the new one continued the next day). Unfortunately, staff had extreme difficulty using

the system, and discontinued it after two months. During that time, Chappello was

unable to document and bill its work for progress billings, and borrowed heavily to

continue to pay its employees while work continued. The company reverted to its old

system and claims that it has lost several hundreds of thousands of dollars in revenues

as it was unable to issue quotes and bids on new contracts.

Chappello has sued your firm for negligence with respect to the implementation of the

computer system.

Required:

Which defences should the firm use? Support your answer with reasons.

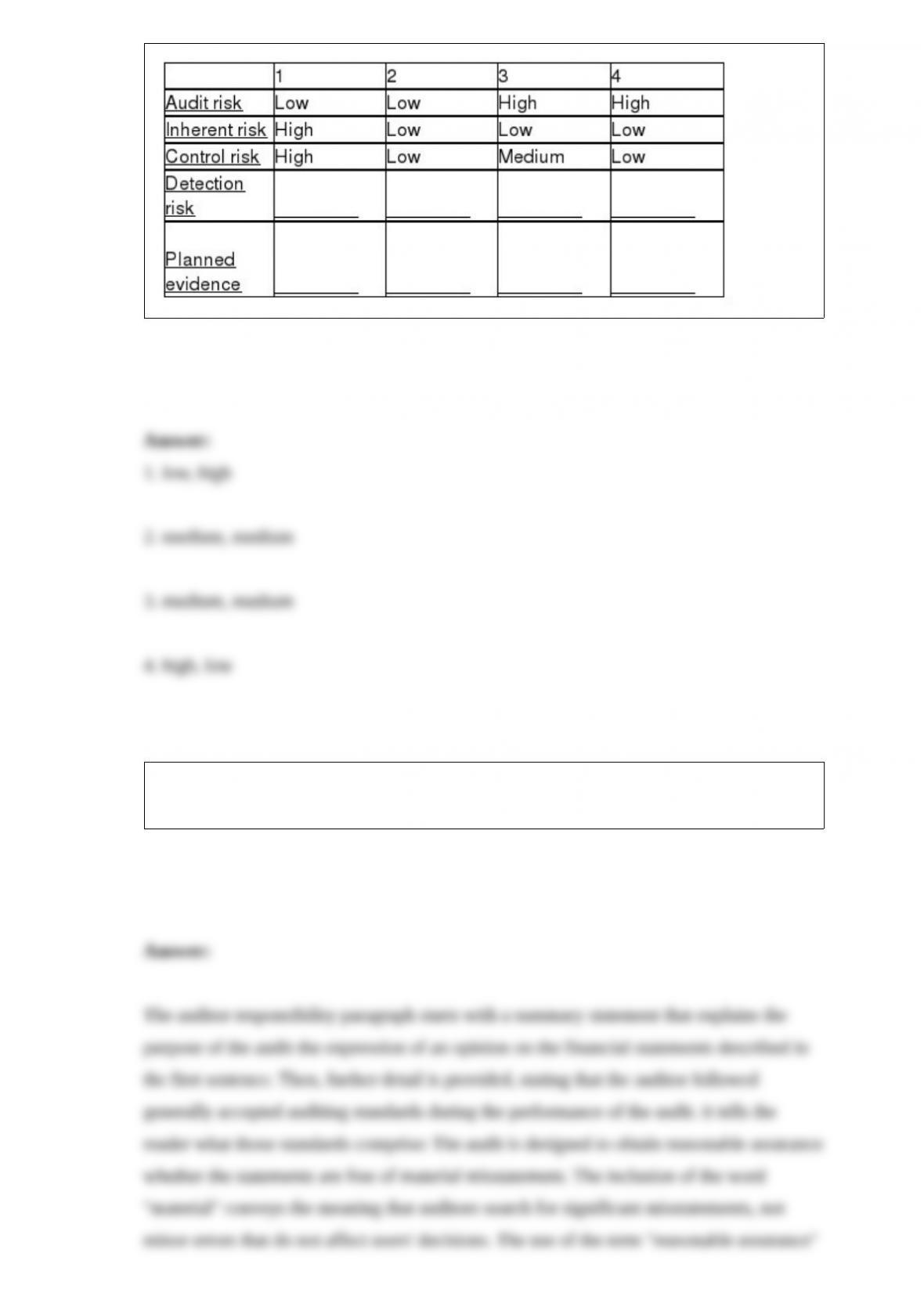

In practice, auditors rarely assign numerical probabilities to inherent risk, control risk,

or audit risk. It is more common to assess these risks as high, medium, or low. For each

of the four situations below, fill in the blanks for detection risk and the amount of

evidence you would plan to gather (“planned evidence”) using the terms high, medium,

or low.

SITUATION

Analyze the “Auditor Responsibility Section” of the standard Independent Auditor’s

Report, ie. explain the intended purpose of the sentences in this section.

Describe the audit procedures typically used to test for out-of-period liabilities (also

referred to as the search for unrecorded accounts payable).

There are six factors that affect the reliability of audit evidence. One factor is the

independence of the provider; i.e., evidence obtained from a source outside the client

company is more reliable than that obtained within. Identify and discuss the remaining

five factors that affect the appropriateness of evidence.

State the specific balance-related audit objectives applicable to notes payable and

interest and, for each objective, identify one common test of details of balances.

The audit of the inventory and distribution cycle consists of five parts. State the five

parts and, for each part, identify the cycle in which that part is tested by the auditor.

Discuss the differences and similarities between the roles of accountants and auditors.

What additional expertise must an auditor possess beyond that of an accountant?