1) Which of the following statements about the audit of fixed assets is the least correct?

A) The primary accounting record for manufacturing equipment and other property,

plant and equipment is generally a fixed asset master file

B) Manufacturing equipment and current assets are normally audited in the same

fashion regardless of the activity within a particular account

C) The emphasis on auditing fixed assets is on verification of current-period

acquisitions

D) Failure to record the acquisition of a fixed asset affects the income statement until

the assets are fully depreciated

2) Which of the following best describes an entity’s accounting information and

communication system?

A)

B)

C)

D)

3) An auditor learns that collections of accounts receivable during the first ten days of

January were debited to cash and credited to accounts receivable as of December 31 .

The effect generally will be to:

A) overstate the current ratio with no effect on working capital at December 31

B) overstate both working capital and the current ratio at December 31

C) overstate working capital with no effect on the current ratio at December 31

D) leave both working capital and the current ratio unchanged at December 31

4) As the auditor you are assessing the proper sample size to use in testing controls.

When using attributes sampling which of the following is most correct?

A) A 10% change in population size will have the least effect on sample size

B) A 10% change in the tolerable deviation rate will have the least effect on sample size

C) A 10% change in the expected deviation rate will have the least effect on sample size

D) A 10% change in the tolerable will have the least effect on sample size

5) Acceptable risk of incorrect acceptance is directly affected by acceptable audit risk.

A) True

B) False

6) Failure to record the acquisition of goods directly affects the balance in Accounts

payable and may result in an understatement of ending inventory.

A) True

B) False

7) Proper segregation of functional responsibilities calls for separation of:

A) authorization, execution, and payment

B) authorization, recording, and custody

C) custody, execution, and reporting

D) authorization, payment, and recording

8) The most important controls for petty cash relate to:

A)

B)

C)

D)

9) When the auditor develops supporting evidence for amounts posted to account

balances with documentary evidence, that process is called:

A) inquiry

B) confirmation

C) vouching

D) physical examination

10) Which of the following may present itself as the biggest risk to centralizing

information responsibilities that were traditionally separate?

A) IT personnel with access to software and master files may misappropriate assets

B) IT personnel with access to software and master files may lack the accounting skills

necessary to provide useful information to management

C) IT personnel with access to software and master files may not understand the

linkages between general and application controls

D) IT personnel with access to software and master files may not be able to convert the

company’s operational policies to an IT environment

11) Once the auditor has determined the company’s policy for accruing wages and

knows it is consistent with that of previous years, the appropriate audit procedure to test

for cutoff and accuracy is to:

A) recalculate the client’s accruals

B) compare the ledger balance with the journal and the tax form

C) confirm the amount with employees

D) compare the recorded accrued wages with the amount approved in the minutes of the

Board

12) Other than inquiring of management about policies they have established to prevent

illegal acts and whether management knows of any laws or regulations that the

company has violated, the auditor should not search for indirect-effect illegal acts

unless there is reason to believe they may exist.

A) True

B) False

13) Some companies have customers send payments directly to a post office box

address maintained by a bank. This is called a(n) ________ system.

A) direct deposit

B) funds transfer

C) lockbox

D) interbank transfer

14) When a customer disagrees with the amount shown on an account receivable

confirmation, the auditor should not ask the client to reconcile the difference.

A) True

B) False

15) Internal controls over the ship finished goods function in the inventory and

warehousing cycle are not normally tested by the auditor as a part of performing tests of

controls and substantive tests of transactions in the sales and collection cycle.

A) True

B) False

16) Which one the following procedures performed for the billing function provides

evidence for the completeness assertion?

A) Making sure that all shipments have been billed

B) Making sure that no shipment has been billed more than twice

C) Making sure that each shipment is billed at the correct amount

D) Making sure that each shipment is billed to the proper customer

17) Because fraud perpetrators are often knowledgeable about audit procedures, SAS

No. 99 requires auditors to incorporate unpredictability into the audit plan.

A) True

B) False

18) Most auditors assess inherent risk as high for related parties and related-party

transactions because:

A) of the unique classification of related-party transactions required on the balance

sheet

B) of the lack of independence between the parties

C) of the unique classification of related-party transactions required on the income

statement

D) it is required by generally accepted accounting principles

19) Whenever an auditor issues a qualified report, he or she must use the term “except

for” in the opinion paragraph.

A) True

B) False

20) When auditors verify accrued property taxes two audit objectives are especially

significant. These are:

A) completeness and accuracy

B) completeness and net realizable value

C) detail tie-in and completeness

D) accuracy and classification

21) Based on audit evidence gathered and evaluated, an auditor decides to increase the

assessed level of control risk from that originally planned. To achieve an overall audit

risk level that is substantially the same as the planned audit risk level, the auditor

would:

A) increase materiality levels

B) decrease detection risk

C) decrease substantive testing

D) increase inherent risk

22) The form that must be filed with the Securities and Exchange Commission

whenever a company plans to issue new securities to the public is the:

A) Form S-1

B) Form 8-K

C) Form 10-K

D) Form 10-Q

23) The

A) encourages

B) prohibits

C) allows

D) allows on a case-by-case basis

24) Imprisonment for a period of six months or longer will result in automatic

expulsion from the

A) True

B) False

25) Audit procedures designed to uncover credit sales made after the client’s fiscal year

end that relate to the current year being audited provide evidence for which of the

following audit objective?

A) realizable value

B) accuracy

C) cutoff

D) existence

26) With what types of contingencies might an auditor be concerned?

27) Discuss each of the following primary documents and records used in the (1)

payment of payroll function, and (2) preparation of payroll tax returns and payment of

taxes function in the payroll and personnel cycle: payroll check, W-2 form, and payroll

tax returns.

28) The transaction-related audit objectives and the client’s methods of controlling

misstatements are essentially the same for credit memos as for sales with the exception

of two differences. What are the two differences from the auditor’s perspective?

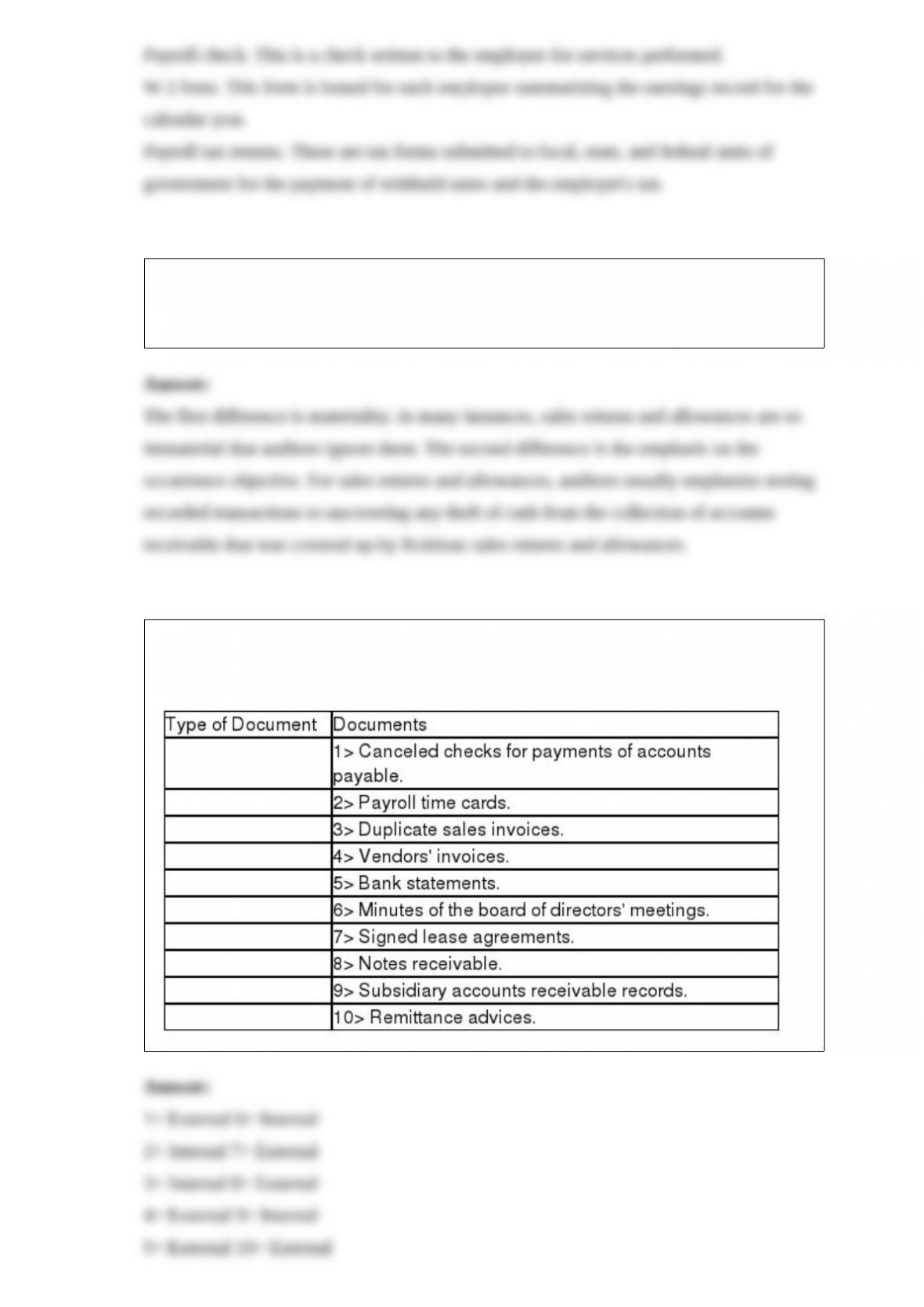

29) Below are 10 documents typically examined during an audit. Classify each

document as either internal or external.

30) Explain each of the following types of documents and indicate the class of

transactions in which they are commonly used.

1>Customer order

2>Shipping document

3>Remittance advice

4>Sales returns and allowance journal

5>Uncollectible account authorization form

31) Describe each of the following types of confirmations:

Positive confirmation

Blank confirmation

Invoice confirmation

Negative confirmation