Zvinakis Mining Company paid $200,000 for the rights to mine lead in southeast

Missouri. The cost to drill and erect a mine shaft was $2,400,000, and equipment to

process the lead ore before shipment to the smelter was $1,800,000. The mine is

expected to yield 2,000,000 tons of ore during the five years it is expected to be

operating. The equipment has an estimated residual value of $150,000 when mining is

concluded. The mine started operations on April 30, 2016. In 2016, 300,000 tons of ore

were extracted, and in 2017, 700,000 tons were mined.

Required:

1> Compute the depletion rate and the units-of-production depreciation rate.

2> Compute depletion and depreciation for 2016 and 2017.

Which of the following generally is associated with accounts payable?

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

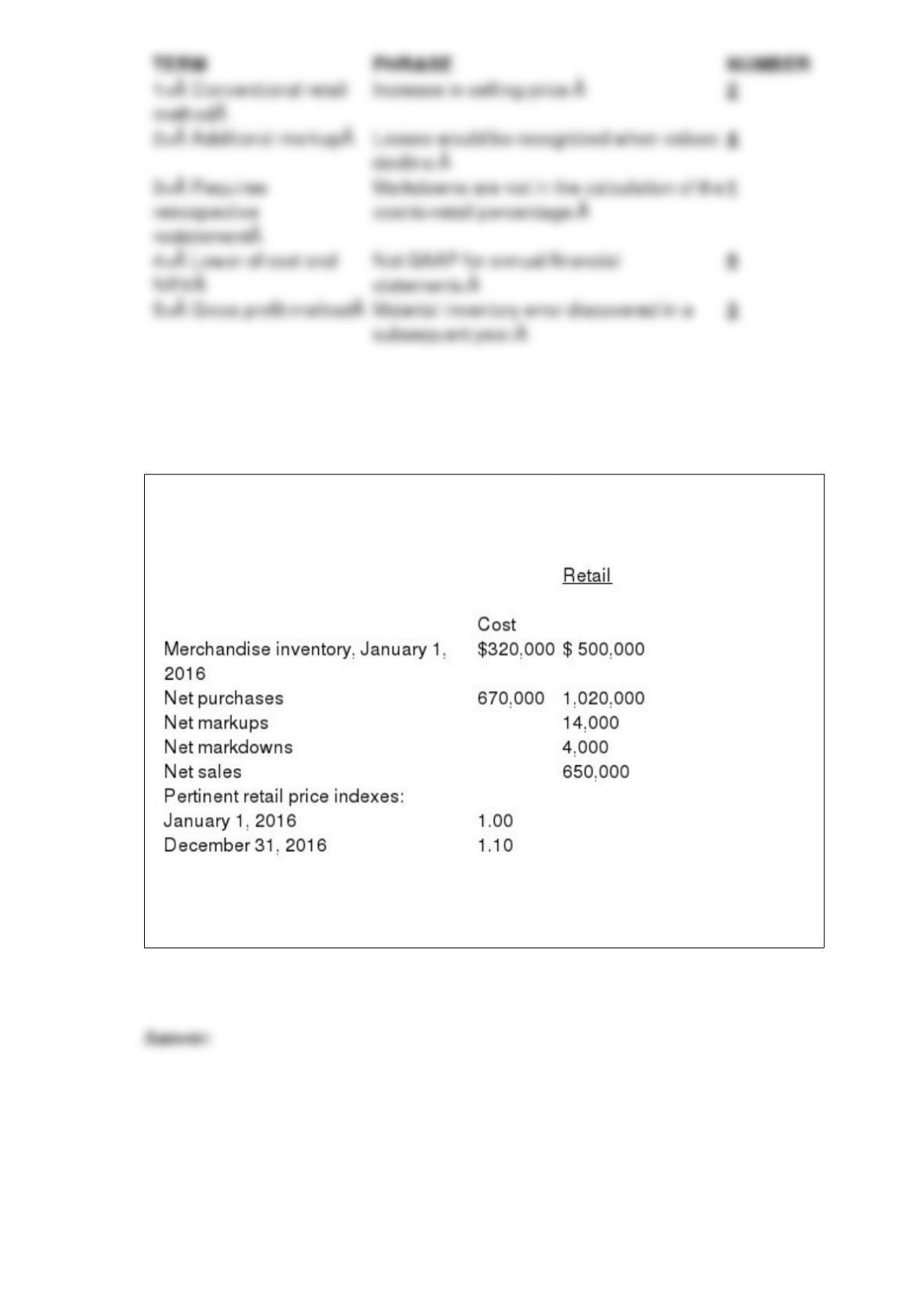

Charleston Company has elected to use the dollar-value LIFO retail method to value its

inventory. The following data has been accumulated from the accounting records:

Required:

Estimate the ending inventory for December 31, 2016.

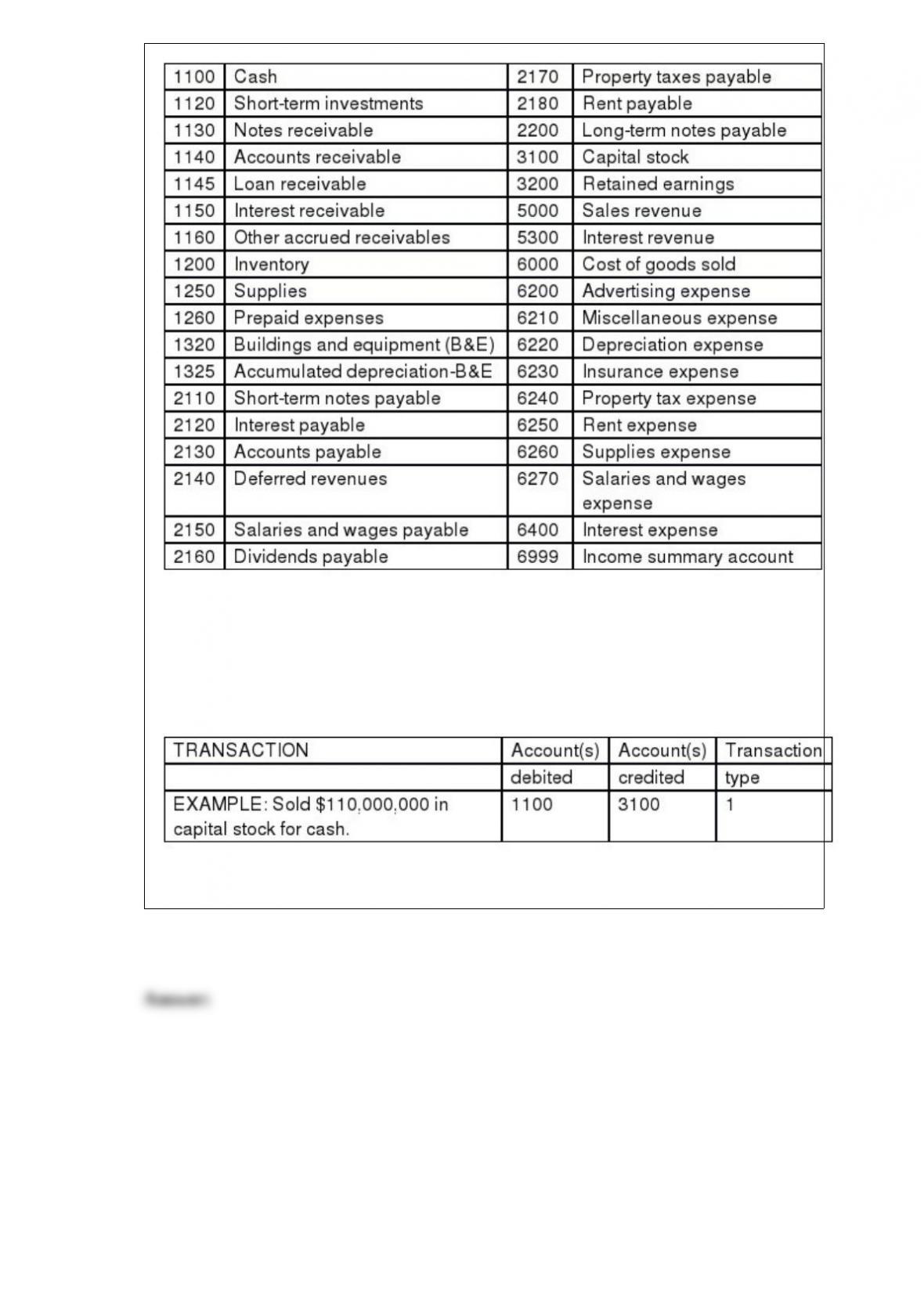

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

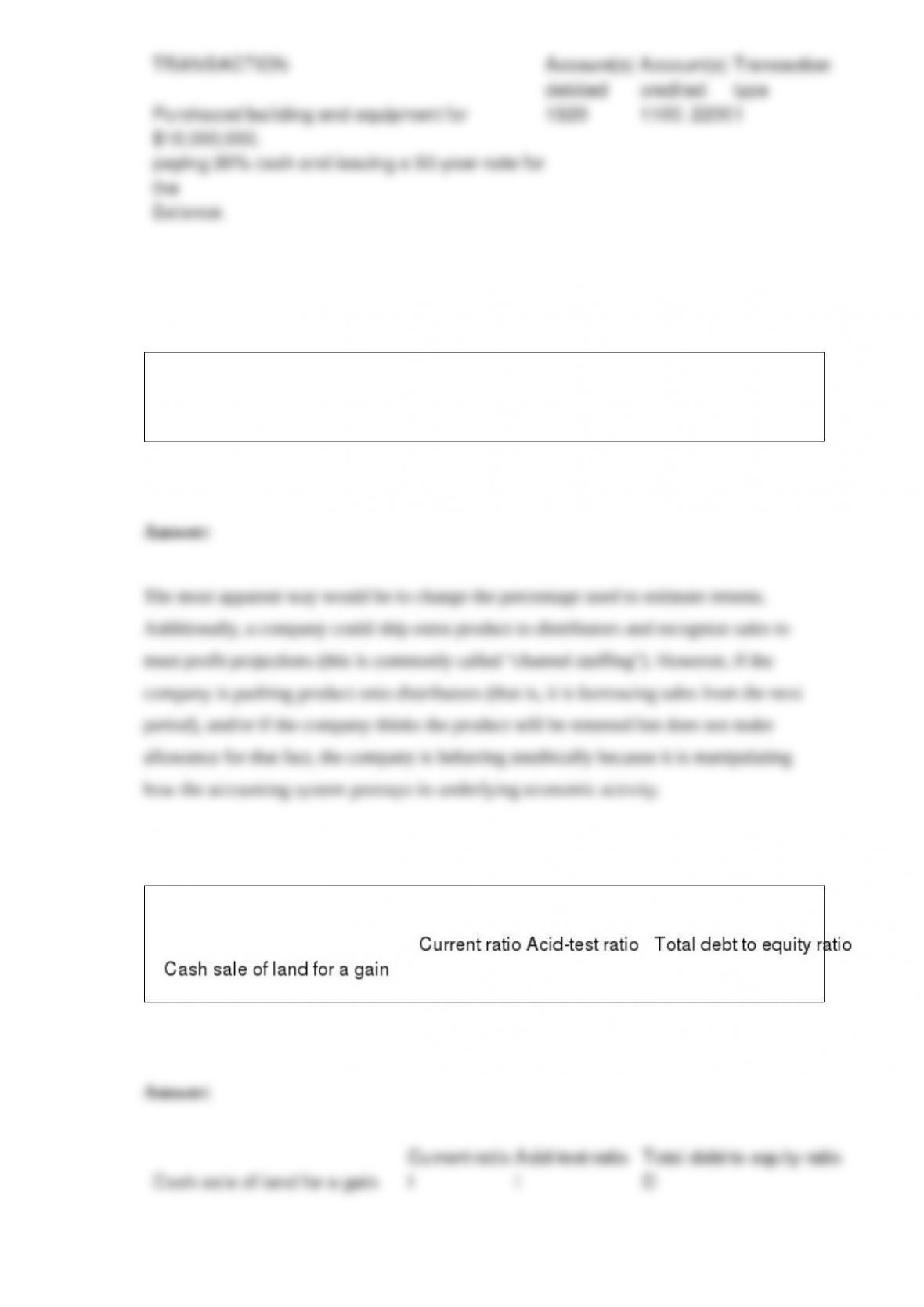

Purchased building and equipment for $10,000,000, paying 20% cash and issuing a

30-year note for the balance.

Explain briefly how a company who sells to distributors with a right of return might

manage earnings if the company was falling short of profit projections. What sort of

ethical problems could result from that earnings management?

In its 2016 annual report to shareholders, the Goodday Chemical Company included the

following disclosure note excerpts on CONTINGENCIES in its annual report to

shareholders: At December 31, 2016, Goodday had recorded liabilities aggregating

$66.5 million for anticipated costs related to various environmental matters, primarily

the remediation of numerous waste disposal sites and certain properties sold by

Goodday. These costs include legal and consulting fees, site studies, the design and

implementation of remediation plans, post-remediation monitoring and related activities

and will be paid over several years. The amount of Goodday’s ultimate liability in

respect of these matters may be affected by several uncertainties, primarily the ultimate

cost of required remediation and the extent to which other responsible parties

contribute. At December 31, 2016, Goodday had recorded liabilities aggregating $218.7

million for potential product liability and other tort claims, including related legal fees

expected to be incurred, presently asserted against Goodday. The amount recorded was

determined on the basis of an assessment of potential liability using an analysis of

available information with respect to pending claims, historical experience, and, where

available, current trends. Goodday is a defendant in numerous lawsuits involving at

December 31, 2016, approximately 63,000 claimants alleging various asbestos-related

personal injuries purported to result from exposure to asbestos in certain rubber-coated

products manufactured by Goodday in the past or in certain Goodday facilities.

Typically, these lawsuits have been brought against multiple defendants in state and

federal courts. In the past, Goodday has disposed of approximately 22,000 cases by

defending and obtaining the dismissal thereof or by entering into a settlement. Goodday

has policies and coverage-in-place agreements with certain of its insurance carriers that

cover a substantial portion of estimated indemnity payments and legal fees in respect of

the pending claims. At December 31, 2016, Goodday has recorded an asset in the

amount it expects to collect under the policies and coverage-in-place agreements with

certain carriers related to its estimated asbestos liability. Goodday has also commenced

discussions with certain of its excess coverage insurance carriers to establish

arrangements in respect of their policies. Subject to the uncertainties referred to above,

Goodday has concluded that in respect of any of the above described liabilities, it is not

reasonably possible that it would incur a loss exceeding the amount recognized at

December 31, 2016, with respect thereto which would be material relative to the

consolidated financial position, results of operations, or liquidity of Goodday.

Show the summary journal entry that Goodday recorded for the environmental cleanup

and product liability/tort claim matters, described in the note disclosure.