1) Which of the following audit risk components may be assessesed in non-quantitative

terms?

A)

B)

C)

D)

2) A major consideration in assigning staff to an audit engagement is the experience

levels required for the work, while a less important consideration is maintaining staff

continuity on the engagement.

A) True

B) False

3) An auditor has been assigned to perform tests of controls for a client’s cash

disbursement system. Client files are kept electronically with no paper audit trail. In this

case the auditor would need to rely on which of the following audit procedures?

A) Analytical procedures and Inquiry

B) Confirmations and Inquiry

C) Observation and Inquiry

D) Reperformance and Inquiry

4) The two primary classes of transactions in the sales and collection cycle are:

A) sales and sales discounts

B) sales and cash receipts

C) sales and sales returns

D) sales and accounts receivable

5) Which is usually included in the engagement letter?

A)

B)

C)

D)

6) Which of the following activities is allowed for a CPA firm’s attestation clients?

A) Contingent fees based on savings due to implementation of an information system

B) Commissions for referring a review client to an insurance agency for insurance

coverage

C) Preparation of tax returns for which fees are based upon client refunds

D) Each of the above is allowed

7) If a control total were to be computed on each of the following data items, which

would best be identified as a hash total for a payroll IT application?

A) gross wages earned

B) employee numbers

C) total hours worked

D) total debit amounts and total credit amounts

8) Rule 101, Independence, prohibits a CPA from performing both audit services and

bookkeeping services for the same public company in the same year.

A) True

B) False

9) The authorization of an issuance of capital stock normally includes all but which of

the following?

A) type of stock to be issued

B) number of shares to be issued

C) date shares are to be issued

D) amount of dividend to be paid on shares issued

10) A procedure to test for a cash receipts cutoff error is:

A) reconciling the bank statement

B) performing a four-column proof-of-cash

C) observing the counting of cash at the balance sheet date

D) tracing recorded cash receipts to bank deposits on the bank statement of a different

period

11) Which of the following best describes effective internal control over payroll?

A) The preparation of the payroll must be under the control of the personnel department

B) The confidentiality of employee payroll data should be carefully protected to prevent

fraud

C) The duties of hiring, payroll computation, and payment to employees should be

segregated

D) The payment of cash to employees should be replaced with payment by checks

12) If an auditor is not independent and the auditor knows that the company has not

followed GAAP, the auditor should immediately disclaim an opinion and not mention

the departure from GAAP in the audit report.

A) True

B) False

13) In which of the following circumstances would an auditor most likely express an

adverse opinion?

A) The CEO refuses to let the auditor have access to the board of director meeting

minutes

B) The financial statements are not in conformity with the FASB statement on loss

contingencies

C) Information comes to the auditor’s attention that raises substantial doubt about the

ability for the client to continue as a going concern

D) Tests of controls show that the internal control structure is so poor that the auditor

has to assess control risk at the maximum

14) When using nonstatistical sampling, the larger the sample size, the greater the

auditor’s confidence that the point estimate is close to the true population value.

A) True

B) False

15) The most important test of details of balances to determine the existence of

recorded accounts receivable is:

A) tracing details of sales invoices to shipping documents

B) tracing the credits in accounts receivable to bank deposits

C) tracing sales returns entries to credit memos issued and receiving room reports

D) the confirmation of customers’ balances

16) To test for overstatement cutoff amounts when auditing Accounts payable, the

auditor should trace receiving reports issued before year-end to related vendors’

invoices to make sure they are not recorded as Accounts payable.

A) True

B) False

17) Recklessness in the case of an audit is present if the auditor knew an adequate audit

was not done but still issued an opinion, even though there was no intent to deceive

financial statement users. This description is the legal term for:

A) ordinary negligence

B) gross negligence

C) constructive fraud

D) fraud

18) A direct financial interest violates independence in which of the following

circumstances?

A) When close relatives such as nondependent children, brothers, and sisters have a

significant financial interest in the client

B) When close relatives such as nondependent children, brothers, and sisters have any

financial interest in the client

C) When the CPA owns shares in a mutual fund that has an ownership interest in the

client

D) When close relatives such as brother, sister, or in-laws are employed by the client

19) Which of management’s assertions with respect to implementing internal controls is

the auditor primarily concerned?

A) efficiency of operations

B) reliability of financial reporting

C) effectiveness of operations

D) compliance with applicable laws and regulations

20) The most significant audit issue that came as a result of the court decision in the

Escott et al. v. Bar Chris Construction Corporation case in 1968 was:

A) the court’s reaffirmation that the burden of proof was on the plaintiff to prove the

auditor was negligent

B) the affirmation of the increased auditor’s responsibility when performing an S-1

review, a review of events subsequent to the balance sheet, for registration statements

C) the increased auditor responsibility when associated with unaudited financial

statements

D) the court’s refusal to allow the percentage-of-completion method of accounting for

revenues

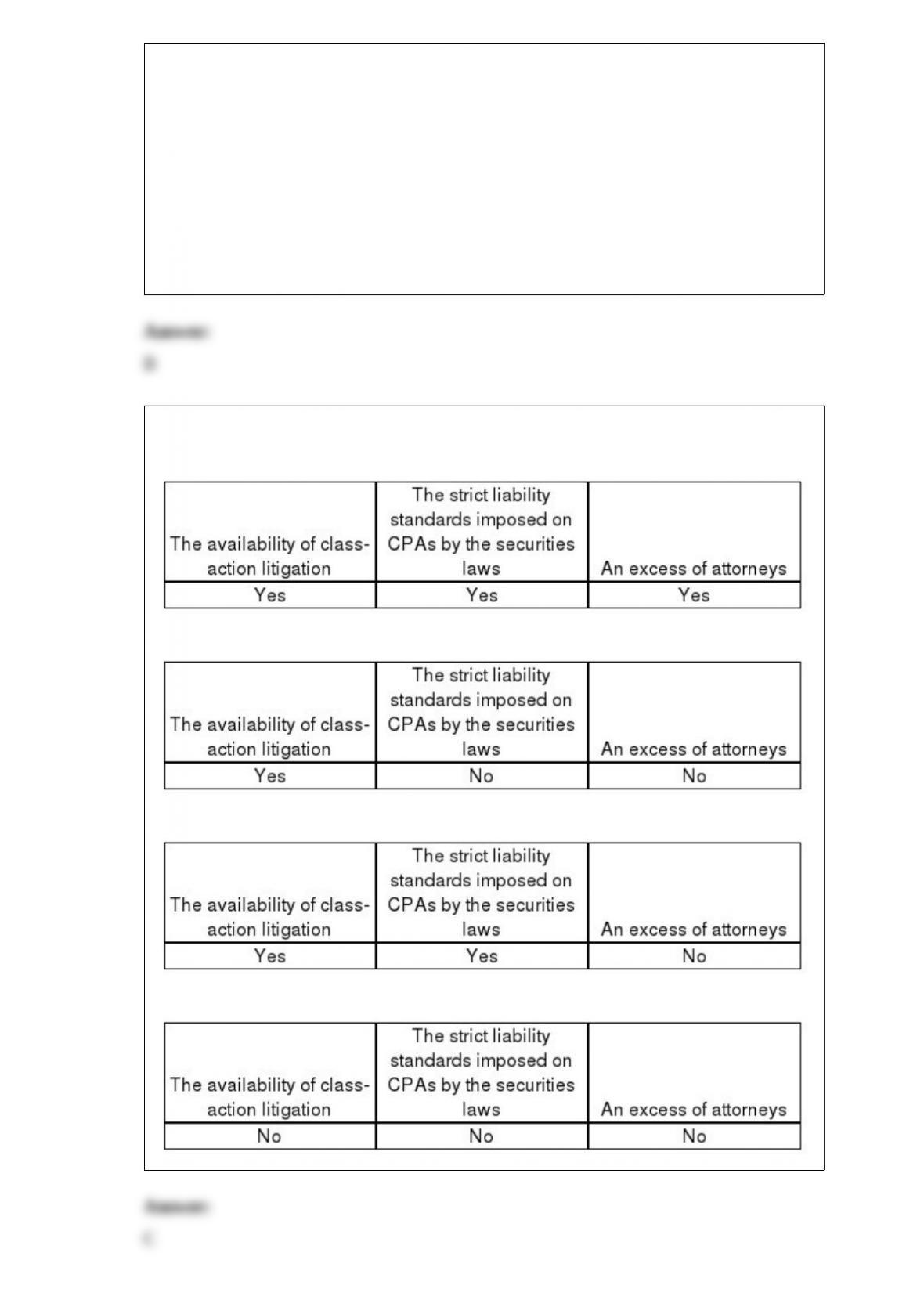

21) The increased litigation under the federal securities laws has resulted from:

A)

B)

C)

D)

22) In performing audit tests of the client’s cost accounting system, the auditor is

primarily concerned with which of the following?

A) System is functioning properly in providing costing and pricing information for

management

B) Costs have been properly assigned to finished goods, work-in-process, and cost of

goods sold

C) Inventory counts agree with the client’s accounting records

D) The client’s cost accounting system is designed on the basis on acceptable cost

accounting systems

23) The audit report date on a standard unqualified report indicates:

A) the last day of the fiscal period

B) the date on which the financial statements were filed with the Securities and

Exchange Commission

C) the last date on which users may institute a lawsuit against either client or auditor

D) the last day of the auditor’s responsibility for the review of significant events that

occurred subsequent to the date of the financial statements

24) Under the cycle approach to segmenting an audit, transactions recorded in different

journals should never be combined with the general ledger balances that result from

those transactions.

A) True

B) False

25) Public companies whose stock is listed on a stock exchange must employ an

independent registrar.

A) True

B) False

26) When the auditor goes through a population and selects items using nonprobalistic

selection methods, without regard to their size, source, or other distinguishing

characteristics, it is called:

A) block sample selection

B) haphazard selection

C) systematic sample selection

D) statistical selection

27) The explanatory paragraph for a qualified opinion would:

A) easy precede the scope paragraph

B) follow the scope paragraph

C) follow the opinion paragraph

D) either precede or follow the opinion paragraph depending on the materiality

28) You are performing the audit of Jenkins and Company. Your tests of controls and

tests of transactions for accounts payable demonstrate that the controls are operating

effectively. This would normally allow you to:

A) eliminate the need for substantive testing of balances for accounts payable

B) reduce the need for substantive testing of balances for accounts payable

C) reduce control tests in other transactions cycles

D) increase the need for substantive testing of balances for accounts payable

29) Which of the following is not a characteristic of the reliability of evidence?

A) effectiveness of client internal controls

B) education of auditor

C) independence of information provider

D) timeliness

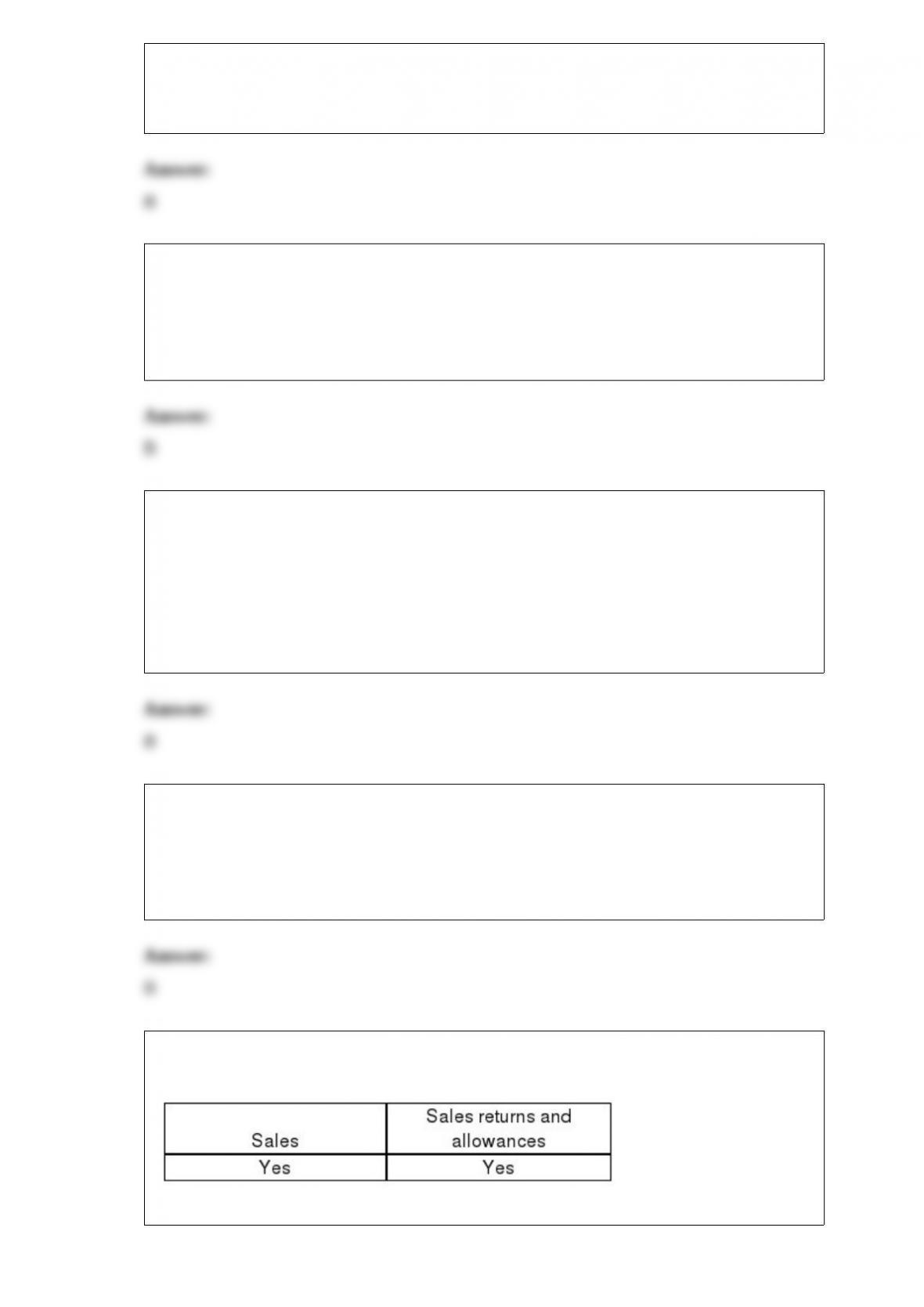

30) Cutoff misstatements can occur for:

A)

B)

C)

D)

31) Harker, CPA is in the audit planning phase of Dracule Industries. An understanding

needs to be established regarding the responsibilities of Harker and Dracule’s

Management. For each of the task items listed below indicate the responsible party

from the list of choices given. Each choice may be used once, more than once or not at

all.

Task to be performed: 1> Obtain an understanding of internal controls 2> Preparation of

the financial statements 3> Assess inherent risk 4> Following GAAP or IFRS 5>

Establish internal controls 6> Detect Material Error 7> Comply with laws and

regulations 8> Assess the risk of the allowance for doubtful accounts estimate 9>

Determine the known and likely errors or misstatements Responsible Party: a. Auditor

is responsible b. Management is responsible c. Both are responsible d. Neither are

responsible

32) Confirmation is the most common test of details of balances for the accuracy of

accounts receivable.

A) True

B) False

33) The general cash account is considered a significant account in almost all audits:

A) where the ending balance is material

B) even when the ending balance is immaterial

C) except those of not-for-profit organizations

D) where either the beginning or ending balance is material

34) One advantage of using statistical techniques when performing analytical

procedures is that they eliminate the need for auditor judgment.

A) True

B) False

35) Analytical procedures provide fewer types of evidence than any other type of audit

test.

A) True

B) False