Receipt stubs, carbon copies of receipts, cash register tapes, or memos of cash register

totals provide information about

a. cash payments.

b. cash receipts.

c. accounts payable.

d. purchases of goods or services.

Employers who have less than $2,500 due in federal income tax withholding and Social

Security and Medicare taxes at the end of the quarter should journalize the debt and pay

at the end of the

a. year.

b. quarter.

c. month following the end of the quarter.

d. next banking day.

Increases are entered on the credit side of a(n)

a. asset account.

b. liability account.

c. expense account.

d. drawing account.

Employers who have $100,000 or more due in federal income tax withholding and

Social Security and Medicare taxes on any day during the current quarter should

journalize the debt and pay at the end of the

a. year.

b. quarter.

c. month following the end of the quarter.

d. next banking day.

A business that purchases a product from another business to sell to customers is called

a

a. service business.

b. manufacturing business.

c. merchandising business.

d. nonprofit business.

To journalize the employer’s payroll taxes, we need to credit all of the following

accounts EXCEPT

a. Payroll Taxes Expense.

b. Social Security Tax Payable.

c. Medicare Tax Payable.

d. FUTA Tax Payable.

The check written to establish the petty cash fund is entered in the journal by

a. debiting Cash and crediting Petty Cash.

b. debiting Petty Cash and crediting Owner’s Capital.

c. debiting Owner’s Capital and crediting Petty Cash.

d. debiting Petty Cash and crediting Cash.

Match the terms with the definitions.

a. accrual basis of accounting

b. combination journal

c. Description column

d. General Credit column

e. General Debit column

f. modified cash basis

g. Posting Reference column

h. special columns 1>A journal with special and general columns.

2>Columns in journals for frequently used accounts.

3>A method of accounting that combines aspects of the cash and accrual methods. It

uses the cash basis for recording revenues and most expenses. Exceptions are made

when cash is paid for assets with useful lives greater than one accounting period.

4>A method of accounting under which revenues are recorded when earned and

expenses are recorded when incurred.

5>The column in the combination journal where the account number is entered after

posting.

6>The column in the combination journal used to debit accounts that are used

infrequently.

7>The column in the combination journal used to enter the account titles for the

General Debit and General Credit columns, to identify specific creditors when assets

are purchased on account, and to identify amounts forwarded.

8>The column in the combination journal used to credit accounts that are used

infrequently.

A petty cash fund of $200 has $17 in cash, $180 in petty cash vouchers, and $3 in

miscellaneous receipts not included with the petty cash vouchers. The proper journal

entry to replenish the fund would include a credit to Cash for

a. $3.

b. $17.

c. $180.

d. $183.

The accounting function of classifying is

a. thinking about how events affect the business.

b. gathering similar events to provide information that is easy to understand.

c. sorting and grouping similar items together.

d. deciding the meaning and importance of the information in various reports.

Owner’s equity can be increased through

a. withdrawals by the owner.

b. investments by the owner.

c. expenses exceeding revenues.

d. purchases of assets for cash.

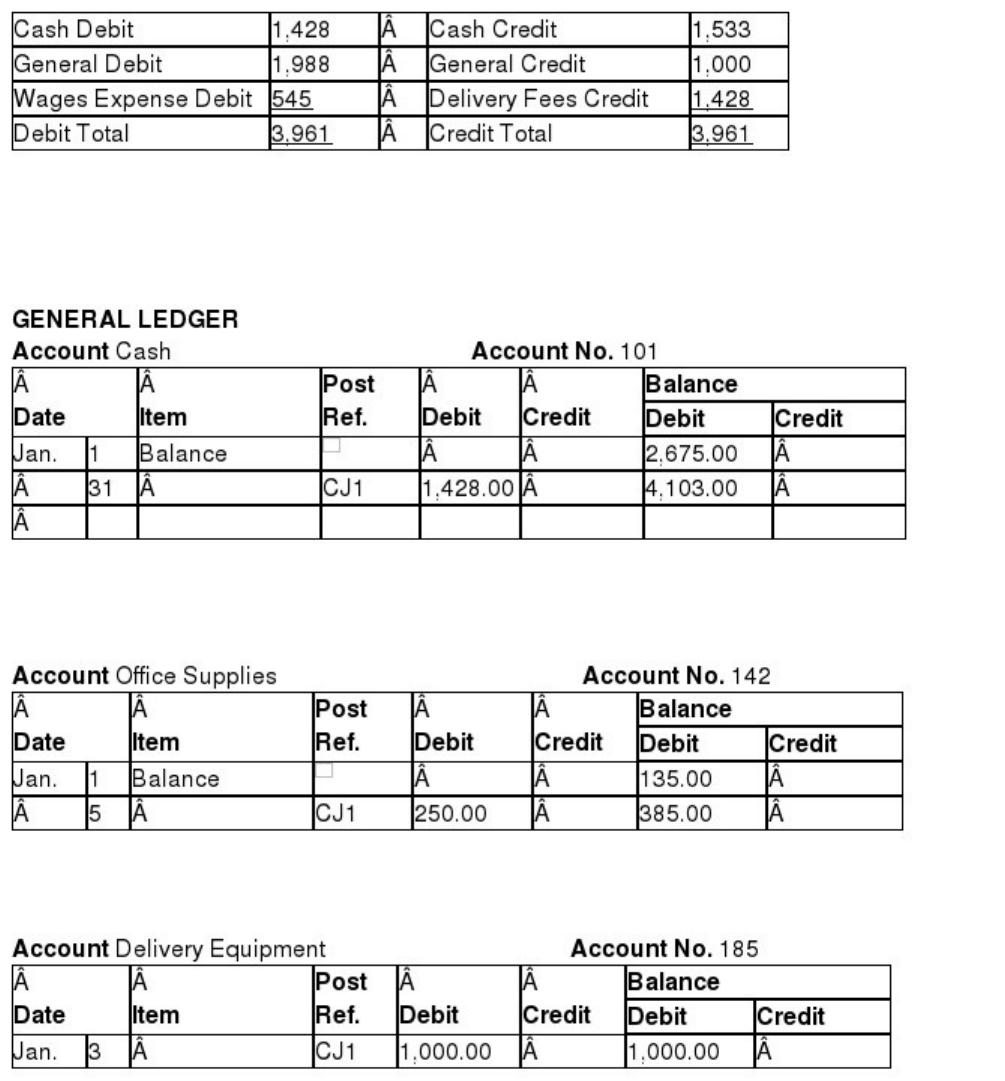

Copying the debits and credits from the journal to the ledger accounts is a process

called ____________________.

The ____________________ is a form used to pull together all of the information

needed to enter adjusting entries and prepare the financial statements.

Deductions for U.S. savings bond purchases, pension plan payments, and Social

Security taxes are considered voluntary deductions.

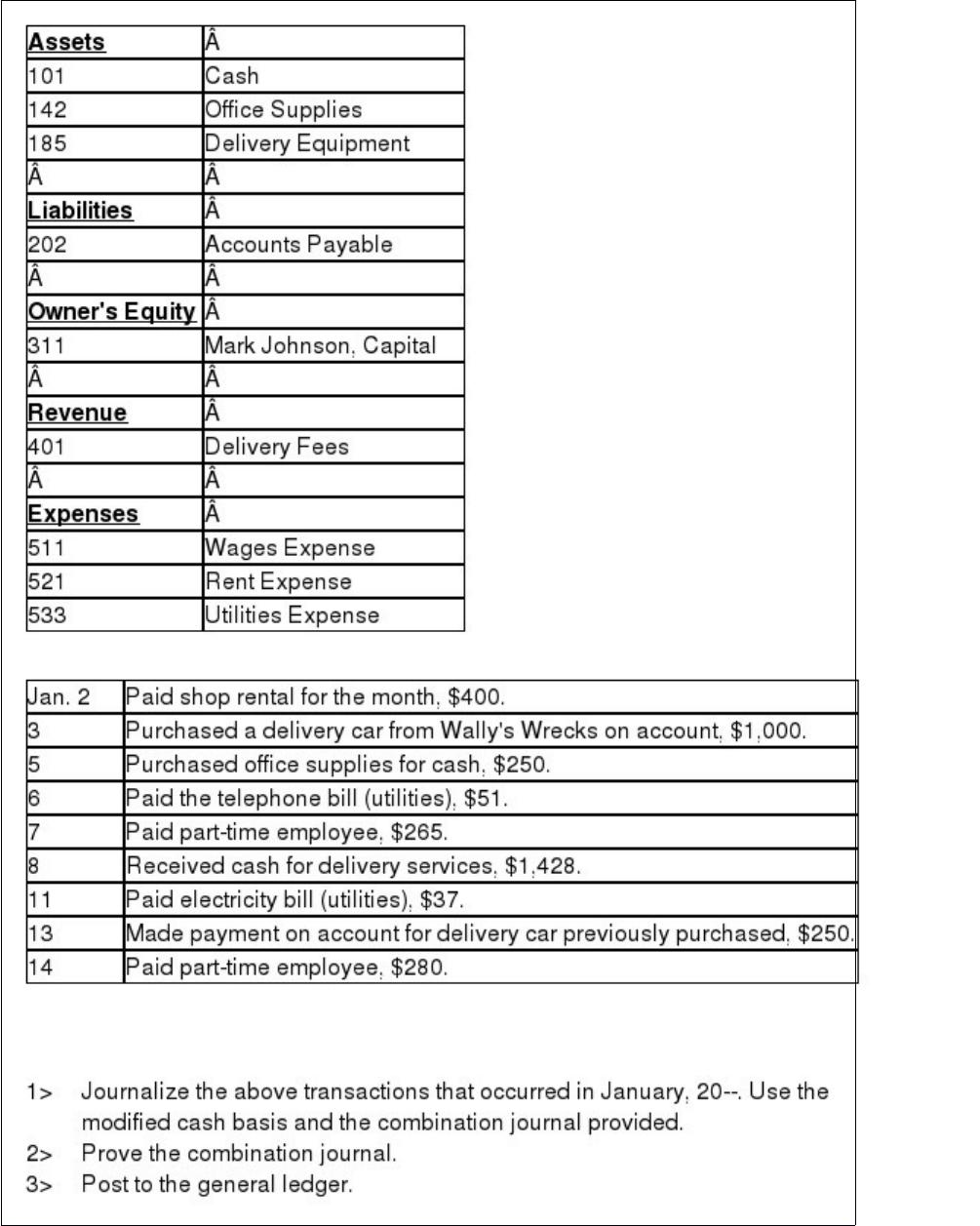

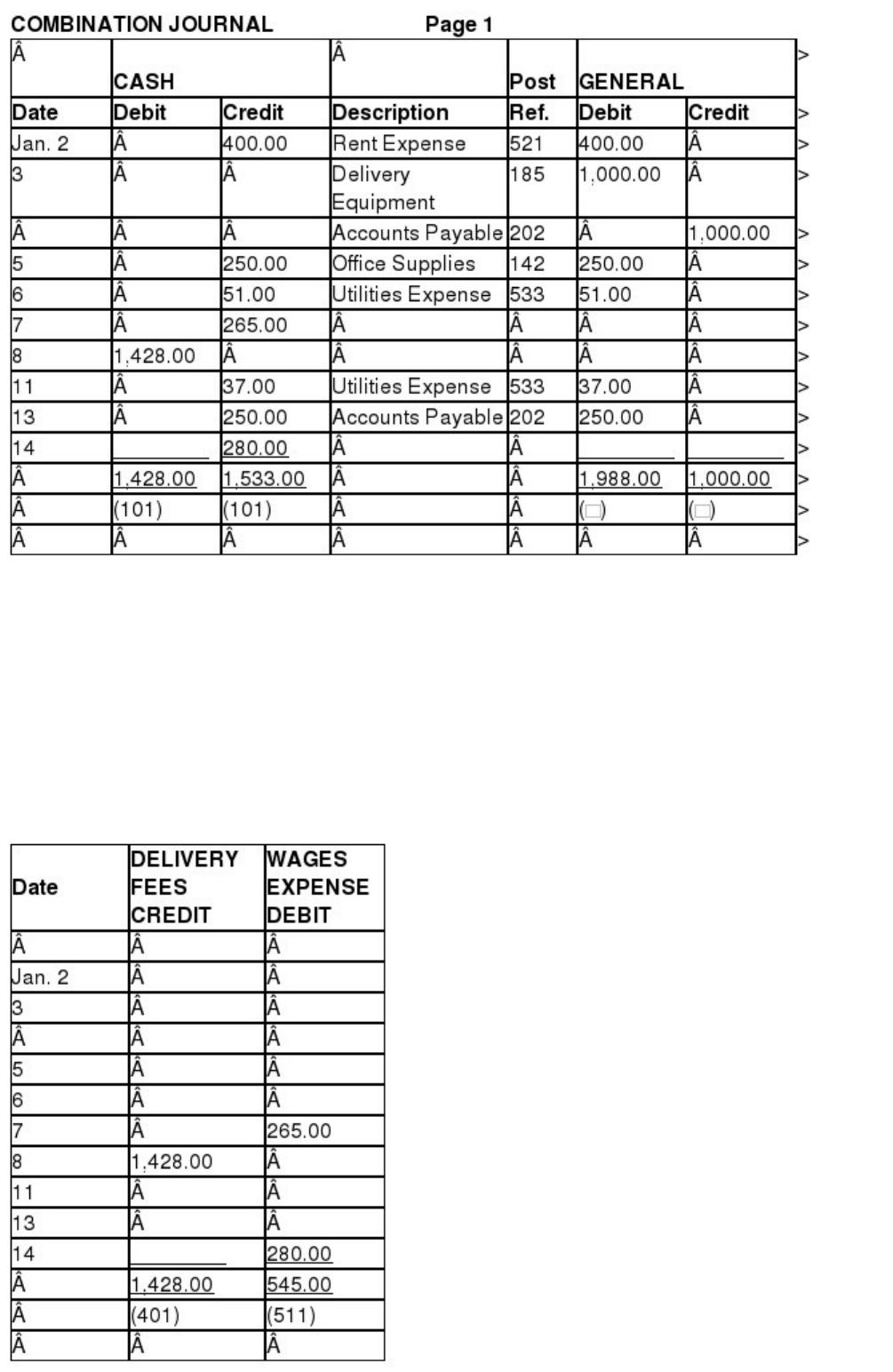

Mark Johnson opened a delivery service. His chart of accounts is shown below.

Required:

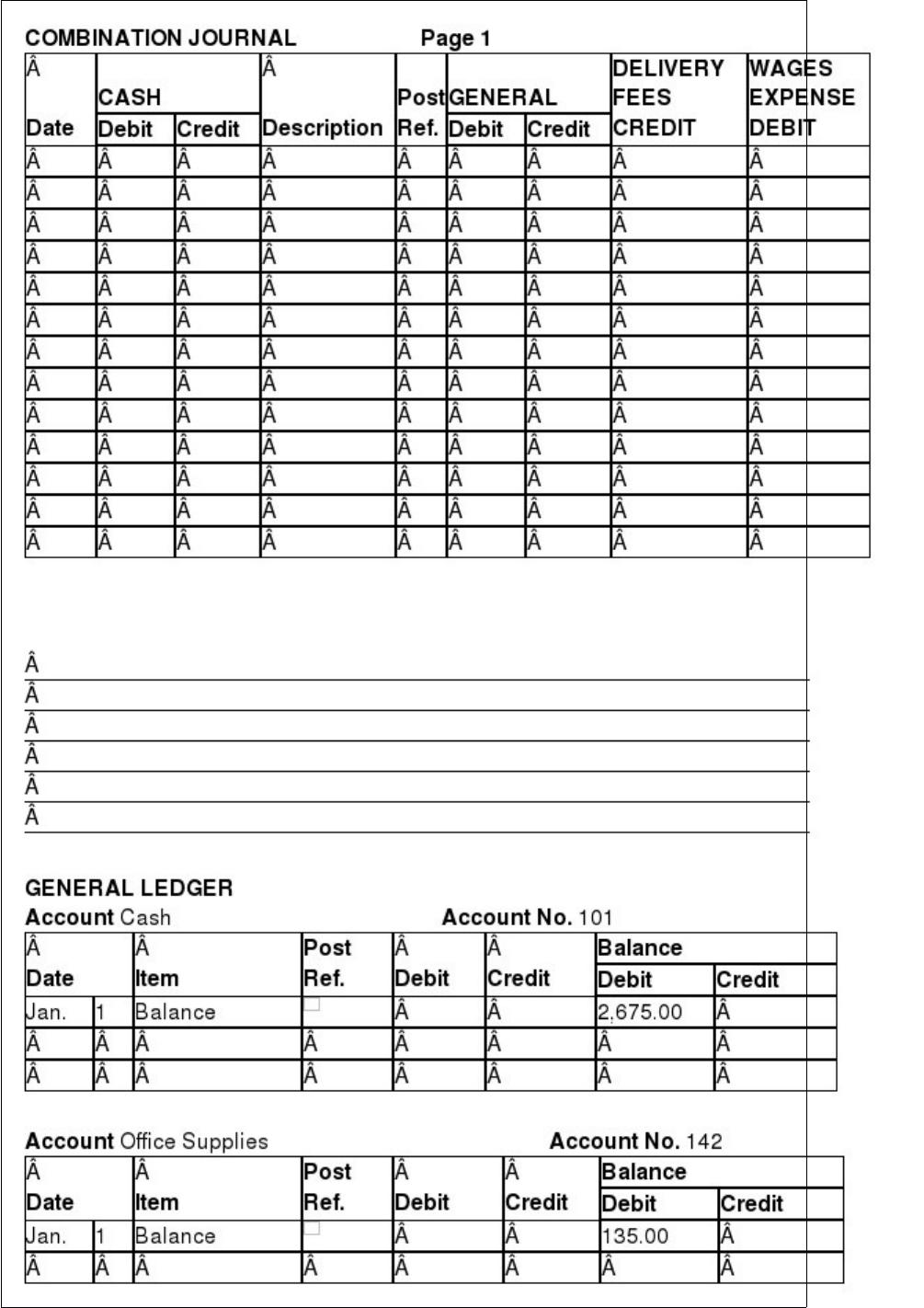

Proving the Combination Journal

The ____________________ balance is on the side that increases an account.

The payroll register is a summary of the annual earnings of each employee.

The cost of workers’ compensation insurance to a construction company with 500

employees would be higher than the cost of insurance to a small candy company with

only five employees.

The cash basis of accounting and the accrual basis of accounting result in the same

measures of net income.

The difference between an independent contractor and an employee is an important

legal distinction.