Every financial statement should have “who, what, and when” in its heading. These

include the:

A) name of the person preparing the statement, the type of financial statement, and

when the financial statement was reported to the SEC.

B) name of the person preparing the statement, the name of the company, and the date

the statement was prepared.

C) name of the company, the type of financial statement, and the time period or date

from which the data were taken.

D) name of the company, the purpose of the statement, and when the financial statement

was reported to the IRS.

Which of the following statements about the presentation of a trial balance is correct?

A) The adjusted trial balance shows the end-of-year balance for Retained Earnings.

B) An adjusted trial balance presents account balances in the same level of detail as in

the presentation of the financial statements.

C) The order of accounts on a trial balance is as follows: assets, liabilities, stockholders’

equity, dividends, revenues and expenses.

D) The adjusted trial balance shows all the debit and credit postings to all the ledger

accounts.

The purpose of a statement of retained earnings is to:

A) estimate the current value of a company’s assets.

B) report the way that net income and dividends affected the financial position of the

company during the period.

C) show where the cash is flowing into and out of a company.

D) report the specific revenues and expenses arising during the period.

During March, the Long Life Consulting Company provides $23,000 in consulting

services for a customer. The customer paid $12,000; the other $11,000 was on account.

Which of the following statements about these transactions is correct?

A) Cash increases by $12,000, Consulting Revenue increases by $11,000, and Accounts

Receivable increases by $23,000.

B) Cash increases by $12,000, Accounts Receivable increases by $11,000, and

Consulting Revenue increase by $23,000.

C) Accounts Receivable increases by $11,000, Liabilities decrease by $12,000, and

Stockholders’ Equity increases by $1,000.

D) Revenues increase by $12,000, liabilities decrease by $12,000, and stockholders’

equity is unchanged.

Which of the following statements about preparation of the statement of cash flows is

correct?

A) GAAP allows the indirect method only.

B) GAAP allows the direct method only.

C) GAAP allows either the indirect or direct method.

D) Although GAAP allows either method for the preparation of the operating activities

section of the statement of cash flows, the indirect method must be used to prepare the

investing activities section of the statement of cash flows.

A company sells goods at a selling price of $20,000. The cost of the goods is $15,000.

Under a perpetual inventory system, the journal entries prepared to record the sale will

include one with a debit to:

A) Inventory and a credit to Sales Revenue for $15,000.

B) Cost of Goods Sold and a credit to Inventory for $15,000.

C) Inventory and credit to Sales Revenue for $20,000.

D) Cost of Goods Sold and a credit to Sales Revenue for $15,000.

Which of the following statements about receivables turnover analysis is correct?

A) The receivables turnover ratio indicates how many times, on average, the process of

selling to and collecting from customers occurs during the accounting period.

B) Companies of similar size in different industries tend to have similar receivables

turnover ratios.

C) A high turnover ratio may suggest the company is allowing too much time for

customers to pay.

D) The days to collect ratio is found by dividing the receivables turnover ratio by 365

days.

_________________ are of special importance because they are the only activities that

enter the financial accounting system.

A) External exchanges

B) Internal events

C) Documents

D) Transactions

All of the following might be used to evaluate cash flow performance, except:

A) the absolute amount of cash flow.

B) whether cash flow is positive or negative.

C) the relationship between net income and cash flow.

D) the trend in sales and operating expenses.

When the direct method is used to determine the cash flows from operating activities,

which of the following adjustments must be made to interest expense to determine total

interest payments?

A) Add all changes in Interest Payable

B) Add decreases in Interest Payable and subtract increases in Interest Payable

C) Add increases in Interest Payable and subtract decreases in Interest Payable

D) Subtract all changes in Interest Payable

Internal controls are concerned with:

A) only manual accounting systems.

B) the extent of government regulations.

C) protecting against theft of assets and enhancing accounting information.

D) preparing income tax returns.

Net income is the amount:

A) the company earned after subtracting expenses and dividends from revenue.

B) by which assets exceed expenses.

C) by which assets exceed liabilities.

D) by which revenues exceed expenses.

One of the most common sources of misstatement in financial statements is the:

A) use of alternating inventory costing methods.

B) failure to write down inventory when the market value is below cost.

C) failure to report stock issues appropriately.

D) incorrectly calculating the inventory turnover ratio.

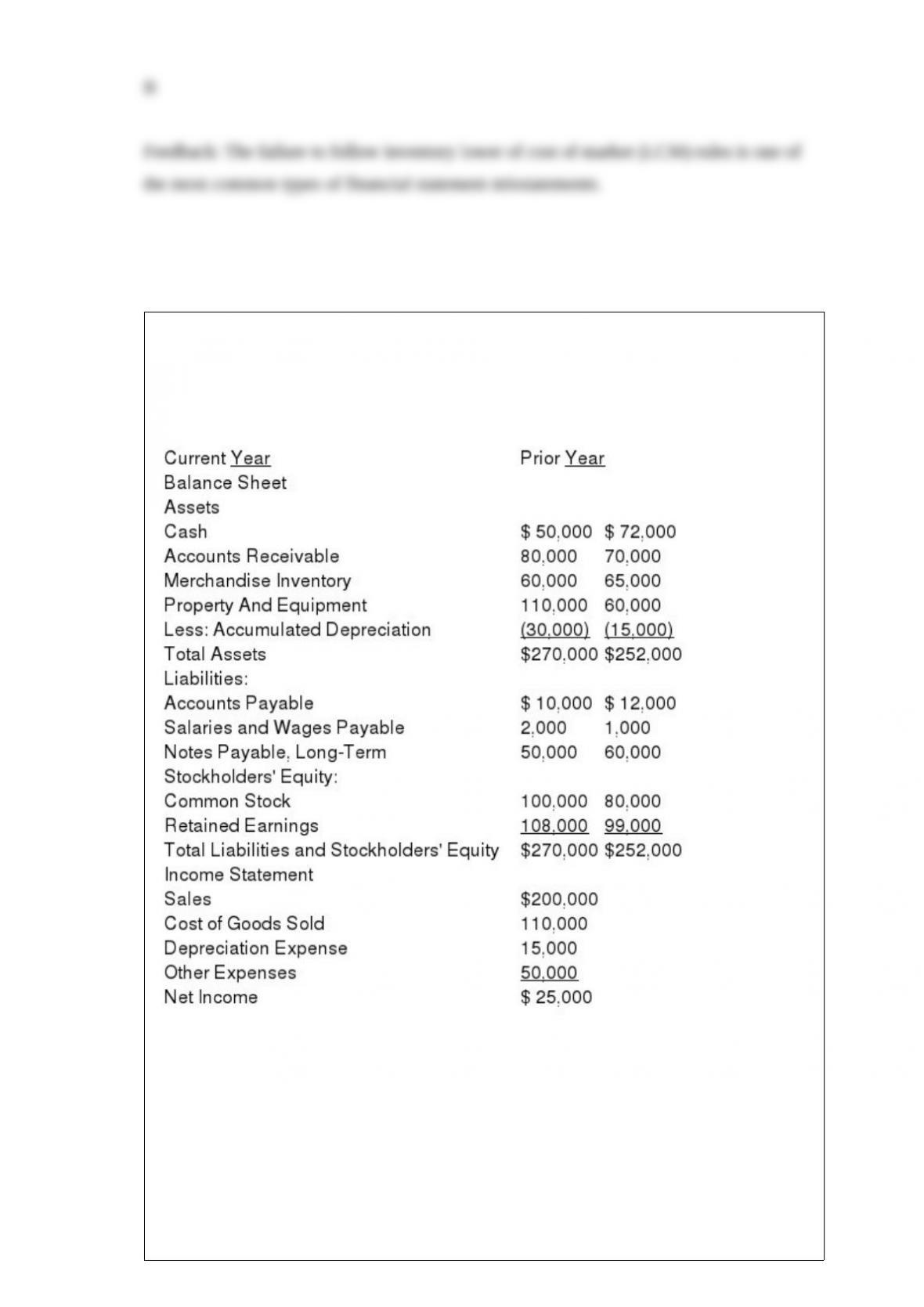

The management team of Wickersham Brothers Inc. is preparing its annual financial

statements. The statements are complete except for the statement of cash flows. The

completed comparative balance sheets and income statements are summarized.

Other information from the company’s records includes the following:

Bought equipment for cash, $50,000.

Paid $10,000 on long-term note payable.

Issued new shares of common stock for $20,000 cash.

Cash dividends of $16,000 were declared and paid to stockholders.

Accounts Payable arose from inventory purchases on credit.

Income Tax Expense ($4,000) and Interest Expense ($3,000) were paid in full at the end

of both years and are included in Other Expenses.

Required:

Part a. Prepare the statement of cash flows using the indirect method. Include any

supplemental disclosures.

Part b. Interpret the statement of cash flows by explaining the main sources and uses of

cash during the year.

Which of the following statements about the receivables turnover analysis is correct?

A) Accounts receivable decline as companies sell on credit.

B) Accounts receivable increase as companies receive payment.

C) Receivables turnover refers to how fast receivables are collected.

D) The days to collect will increase as the receivables turnover increases.

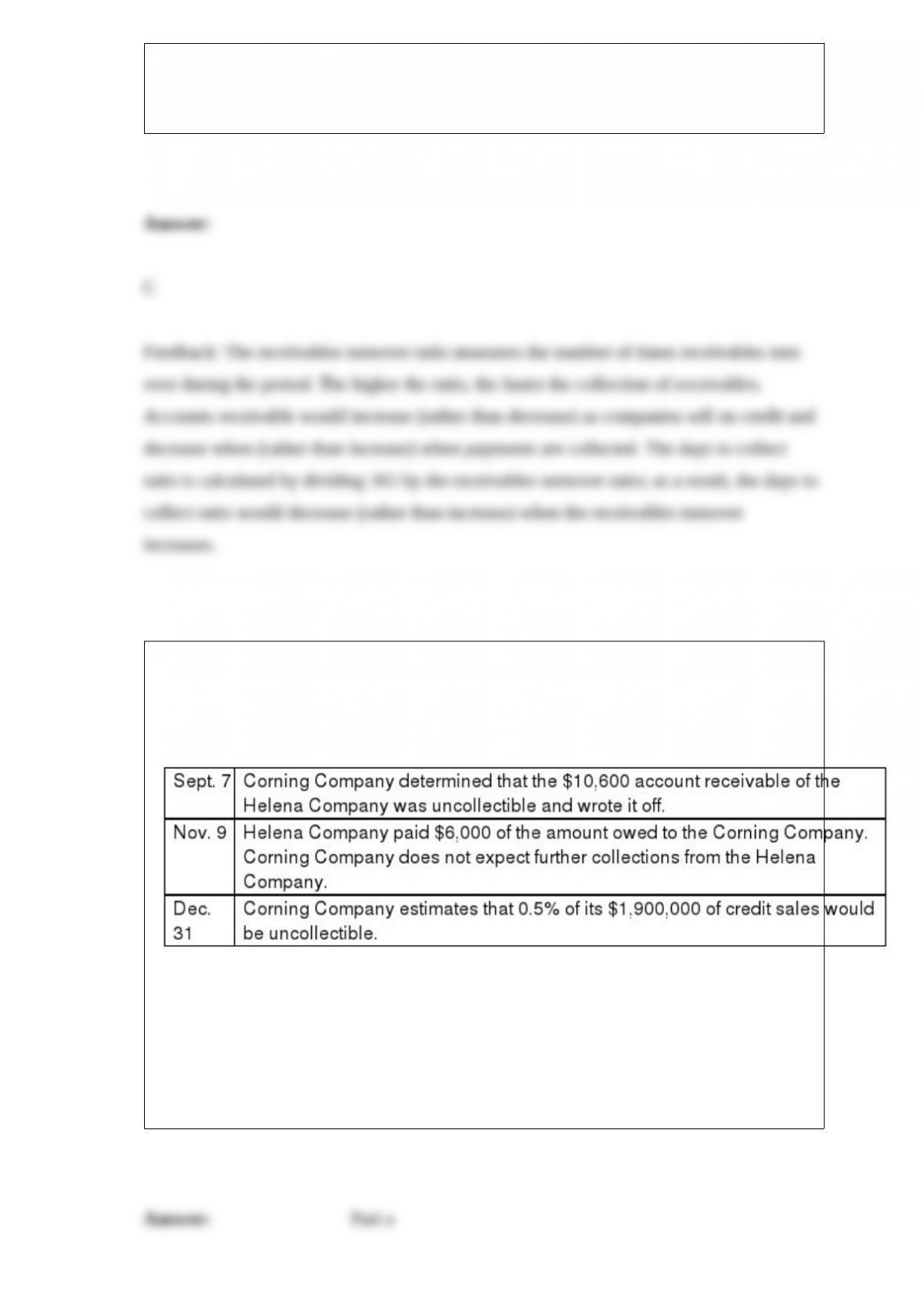

The Corning Company uses the percent of sales method of accounting for uncollectible

accounts receivable. At the beginning of the current year, the Allowance for Doubtful

Accounts had normal balance of $8,000. The following transactions took place during

the current year:

Required:

Part a. Prepare journal entries to record these transactions.

Part b. Determine the balance of the Allowance for Doubtful Accounts at the end of the

current year. Assume that the transactions above are the only transactions affecting this

account during the year.

Travis County Bank agrees to lend Brickyard Corporation $200,000 on January 1.

Brickyard signs a $200,000, 4%, 9-month note. Interest is due at maturity on September

30. The company’s fiscal year ends June 30 and adjusting entries are recorded at that

time only.

Use the information above to answer the following question. What journal entry will

Brickyard make when paying the interest at maturity?

A) Debit Notes Payable and credit Cash for $206,000

B) Debit Interest Expense for $4,000, and credit Cash for $4,000

C) Debit Interest Expense for $6,000 and Cash for $206,000

D) Debit Interest Payable for $4,000, credit Interest Expense for $2,000, and credit

Cash for $6,000