If previous experience indicates that a material number of stock options will be

forfeited before they vest, the fair value estimate of the options on the grant date should

be adjusted to reflect that expectation.

During periods of falling prices, LIFO ending inventory will be less than FIFO ending

inventory.

Revenue on a multiple-element contract typically is allocated to independent parts of

the contract based on their relative selling prices.

The purpose of the conceptual framework is to provide a structure and framework for a

consistent set of GAAP.

In accounting for operating leases, the lessor, rather than the lessee, will recognize

depreciation on the leased asset.

Physical counts of inventory are never made with perpetual inventory systems.

When an equity method investment is sold, a gain or loss is recognized for the

difference between its selling price and its cost.

Noncash assets received as consideration for the issue of stock are always valued based

on the fair value of the stock.

Firms have free choice as to whether to recognize revenue over time or at a point in

time to account for a long-term contract.

Under IFRS, if it is probable that a contingent liability will result in a future payment

but there is a range of equally likely amounts that will be paid, the midpoint of the

range should be accrued as a loss.

Restricted stock units (RSUs):

A. are reported as a liability if payable in shares rather than cash.

B. are reported as part of shareholders’ equity if payable in shares rather than cash.

C. are reported as part of shareholders’ equity if payable in cash rather than shares.

D. are reported as part of shareholders’ equity if the recipient will receive cash or can

elect to receive cash.

The portion of the obligation that plan participants are entitled to receive regardless of

their continued employment is called the:

a. Vested benefit obligation.

b. Retiree benefit obligation.

c. Actual benefit obligation.

d. True benefit obligation.

Financial statement note disclosure is required for material potential losses when the

loss is at least reasonably possible:

a. Only if the amount is known.

b. Only if the amount is known or reasonably estimable.

c. Unless the amount is not reasonably estimable.

d. Even if the amount is not reasonably estimable.

A $500,000 bond issue sold at 98. Therefore, the bonds:

a. Sold at a discount because the stated rate of interest was lower than the effective rate.

b. Sold for the $500,000 face amount less $10,000 of accrued interest.

c. Sold at a premium because the stated rate of interest was higher than the yield rate.

d. Sold at a discount because the effective interest rate was lower than the face rate.

In a period when costs are falling and inventory quantities are stable, the lowest taxable

income would be reported by using the inventory method of:

a. Weighted average.

b. LIFO.

c. Moving average.

d. FIFO.

Romano Services provides room cleaning arrangements for hotels in Ohio. On April 1,

Silvia Hotels & Resorts signed an agreement to outsource its room cleaning functions to

Romano. The contract specifies the service fee to be $15,000 per month, and all

payments are to be made shortly after the end of each quarter. It also specifies that

Romano will receive an additional quarterly bonus of $3,000, if during that quarter,

Silvia receives no more than five complaints from customers about room cleanliness. –

On April 1, based on historical experience, Romano estimated that there is a 75%

chance that it will earn the quarterly bonus.

– On May 5, Romano learned that, during March, there were two complaints from

customers related to room cleanliness. Based on this new information, Romano revised

its estimate downward to 40% that it would earn the quarterly bonus.

– On June 30, Silvia notified Romano that, for the quarter ended, there were four

complaints associated with room cleanliness, so Romano would receive the bonus. Two

days later, Romano received all payments due for all services rendered in the second

quarter, including the bonus. Romano bases estimates of variable consideration on the

expected value of the consideration it expects to receive.

Prepare Romano’s June 30 and July 2 journal entries to record additional service

revenue earned, as well as any necessary adjustments to revenue and receipt of payment

from Silvia.

The percentage-of-completion method violates the general rule for revenue recognition

that:

a. Collection is reasonably assured.

b. Costs are known or reasonably estimated.

c. The earnings process is complete.

d. Collections have been received.

Fink Insurance collected premiums of $18,000,000 from its customers during the

current year. The adjusted balance in the Deferred premiums account increased from $6

million to $8 million dollars during the year. What is Fink’s revenue from insurance

premiums recognized for the current year?

a. $10,000,000.

b. $16,000,000.

c. $18,000,000.

d. $20,000,000.

Wayne Co. had an decrease in deferred tax liability of $20 million, a decrease in

deferred tax assets of $10 million, and an increase in tax payable of $100 million. The

company is subject to a tax rate of 40%. The total income tax expense for the year was:

a. $90 million.

b. $100 million.

c. $110 million.

d. $130 million.

Which of the following is an example of a change in accounting principle?

a. A change in inventory costing methods.

b. A change in the estimated useful life of a depreciable asset.

c. A change in the actuarial life expectancies of employees under a pension plan.

d. Consolidating a new subsidiary.

The primary historical reason for the FASB reversing its positions when political

pressures occur is:

a. The cost of gathering data was prohibitive.

b. The difficulties in measurement were too great.

c. They have no authority in such situations.

d. The SEC did not support the FASB position.

Omni-Resistor, Inc. specializes in waterproofing homes, office buildings and other

structures. Recently it completed a waterproofing renovation for a building at a local

university. The contract specifies that Omni-Resistor will receive a flat lump sum of

$100,000 for the renovation, and an additional $2,500 if there is no roof leaking through

the roof within the first year after the renovation. The seller estimates that there is an

85% chance that no leakage will occur within the first year. Required: (a) Assuming

Omni-Resistor uses the most likely value to estimate the variable consideration,

calculate the transaction price. (b) Assuming Omni-Resistor determines transaction

price as the “expected value” of the variable consideration, calculate the transaction

price. (c) Assume Omni-Resistor uses the “expected value” approach, but is very

uncertain of that estimate due to a lack of experience with similar renovations.

Calculate the transaction price.

Accruals occur when cash flows:

a. Occur before expense recognition.

b. Occur after revenue or expense recognition.

c. Are uncertain.

d. May be substituted for goods or services.

Roberto Corporation was organized on January 1, 2016. The firm was authorized to

issue 100,000 shares of $5 par common stock. During 2016, Roberto had the following

transactions relating to shareholders’ equity:

Issued 10,000 shares of common stock at $7 per share.

Issued 20,000 shares of common stock at $8 per share.

Reported a net income of $100,000.

Paid dividends of $50,000.

Purchased 3,000 shares of treasury stock at $10 (part of the 20,000 shares issued at $8).

What is total shareholders’ equity at the end of 2016?

a. $270,000.

b. $300,000.

c. $250,000.

d. $200,000.

Fryer Inc. owns equipment for which it paid $90 million. At the end of 2016, it had

accumulated depreciation on the equipment of $27 million. Due to adverse economic

conditions, Fryer’s management determined that it should assess whether an impairment

loss should be recognized for the equipment. The estimated undiscounted future cash

flows to be provided by the equipment total $60 million, and the equipment’s fair value

at that point is $40 million. Under these circumstances, Fryer:

a. Would record no impairment loss on the equipment.

b. Would record a $3 million impairment loss on the equipment.

c. Would record a $23 million impairment loss on the equipment.

d. None of these answer choices are correct.

Preferred shares that are participating may:

a. Vote for the board of directors.

b. Be exchanged for common stock.

c. Receive extra cash during corporate liquidation.

d. Receive additional dividends beyond the stated amount.

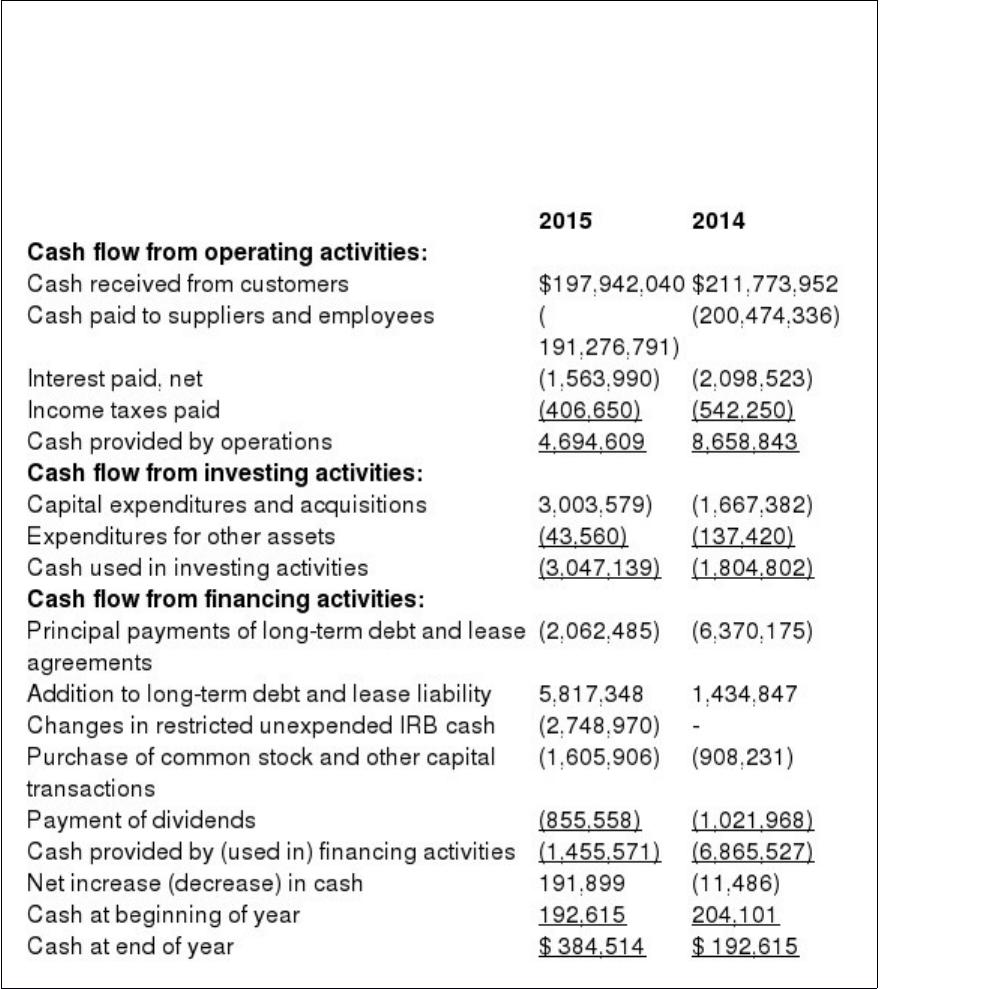

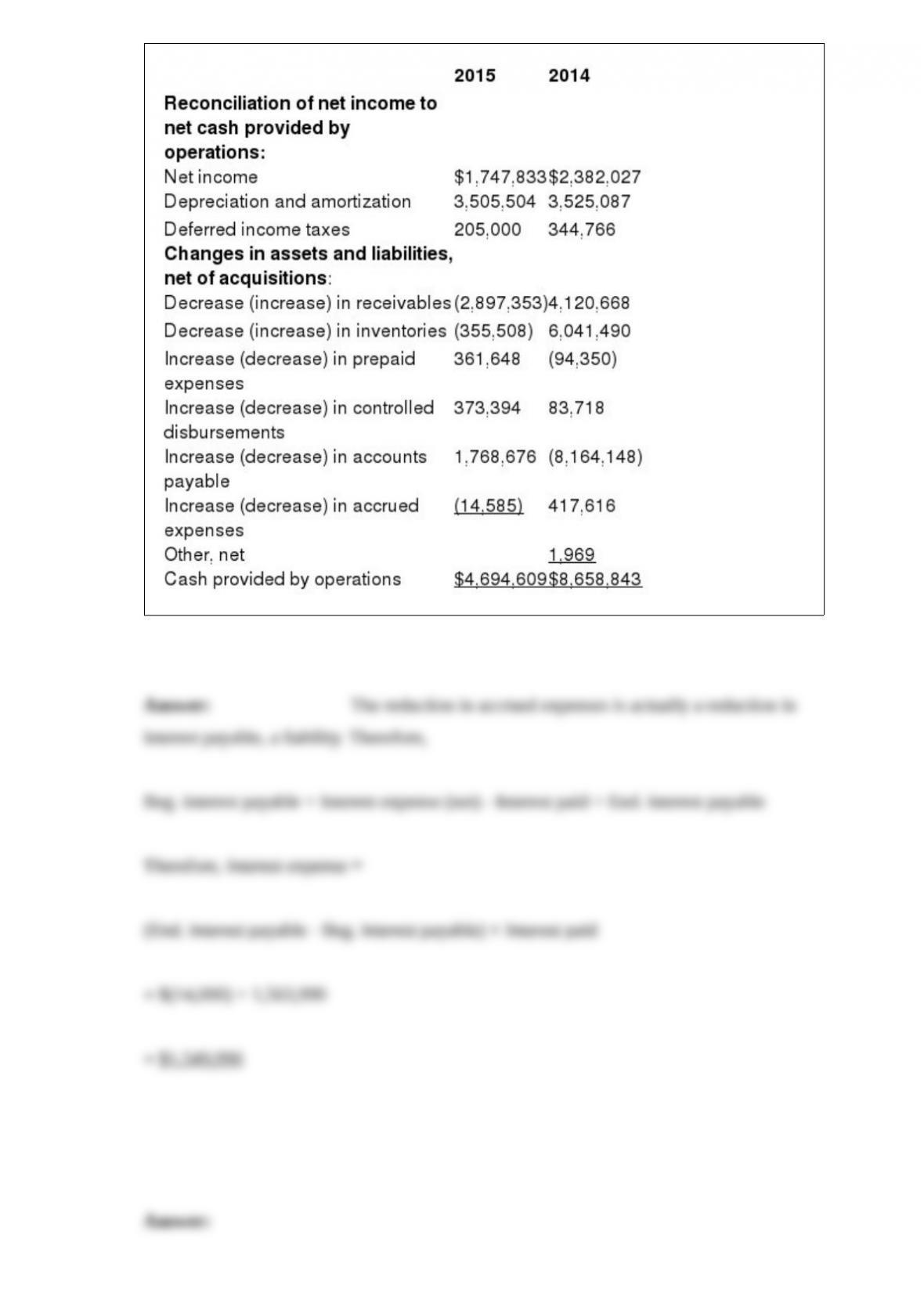

Assuming the decrease in accrued expenses during fiscal year 2015 included a $14,000

reduction due to interest on debt, compute the interest expense (net) for Kinney in that

year.

In its 2015 Annual Report to Shareholders, Kinney Inc. reported the following

Consolidated Statement of Cash Flows:

For the years ended December 31,

) Prepare the journal entries appropriate to record the quasi-reorganization on January 1,

2017.

There is not always a clear-cut distinction between a change in estimate and a change in

principle or a simultaneous change in estimate and change in principle. How are such

situations accounted for?