Zulu Corporation hires a new chief executive officer and promises to pay her a signing

bonus of $2 million per year for 10 years, starting five years after she joins the

company. The liability for this bonus when the CEO is hired:

a. Is the present value of a deferred annuity.

b. Is the present value of an annuity due.

c. Is $20 million.

d. Is zero because no cash is owed for five years.

Under U.S. GAAP, a deferred tax asset for stock options:

a. is created for the cumulative amount of the fair value of the options the company has

recorded for compensation expense.

b. is the portion of the options’ intrinsic value earned to date times the tax rate.

c. is the tax rate times the fair value of all the options.

d. isn’t created if the award is “in the money;” that is, it has intrinsic value.

When outstanding bonds are converted into common stock, under either the book value

method or the market value method, the same amount would be debited to:

A rationale for recognizing revenue over the life of a contract rather than at a single

point in time is that:

a. Results are more conservative.

b. It provides a better measure of periodic accomplishment.

c. It is a better match with legal ownership.

d. It results in a lower income tax.

Which of the following is not usually part of the pension formula under a defined

benefit plan?

a. Age at retirement.

b. Number of years of service.

c. Seniority at time of retirement.

d. Compensation level.

In a period when costs are rising and inventory quantities are stable, the inventory

method that would result in the highest ending inventory is:

a. Weighted average.

b. Moving average.

c. FIFO.

d. LIFO.

Which of the following best demonstrates the full disclosure principle?

a. The multi-step income statement.

b. The auditors” report.

c. The company’s tax return.

d. Disclosure notes to financial statements.

On June 1, 2015, the Crocus Company began construction of a new manufacturing

plant. The plant was completed on October 31, 2016. Expenditures on the project were

as follows ($ in millions):

On July 1, 2015, Crocus obtained a $70 million construction loan with a 6% interest

rate. The loan was outstanding through the end of October, 2016. The company’s only

other interest-bearing debt was a long-term note for $100 million with an interest rate of

8%. This note was outstanding during all of 2015 and 2016. The company’s fiscal

year-end is December 31. What is the amount of interest that Crocus should capitalize

in 2015, using the specific interest method?

a. $1.90 million.

b. $1.95 million.

c. $2.96 million.

d. None of these answer choices are correct.

Paul Company issues a product recall due to an apparently preexisting and material

defect discovered after the end of its fiscal year. Financial statements have not yet been

issued. The action required of Paul Company for this reasonably estimable contingency

for the year just ended is:

a. To disclose it in a note to the financial statements.

b. To accrue a long-term liability.

c. To accrue the liability and explain it in a note to the financial statements.

d. To do nothing relative to the contingency.

Prior service cost is expensed immediately using:

a. U.S. GAAP.

b. IFRS.

c. Both U.S. GAAP and IFRS.

d. Neither U.S. GAAP nor IFRS.

Which of the following is not one of the approaches for reporting accounting changes?

a. The change approach.

b. The retrospective approach.

c. The prospective approach.

d. All of these answer choices are approaches for reporting accounting changes.

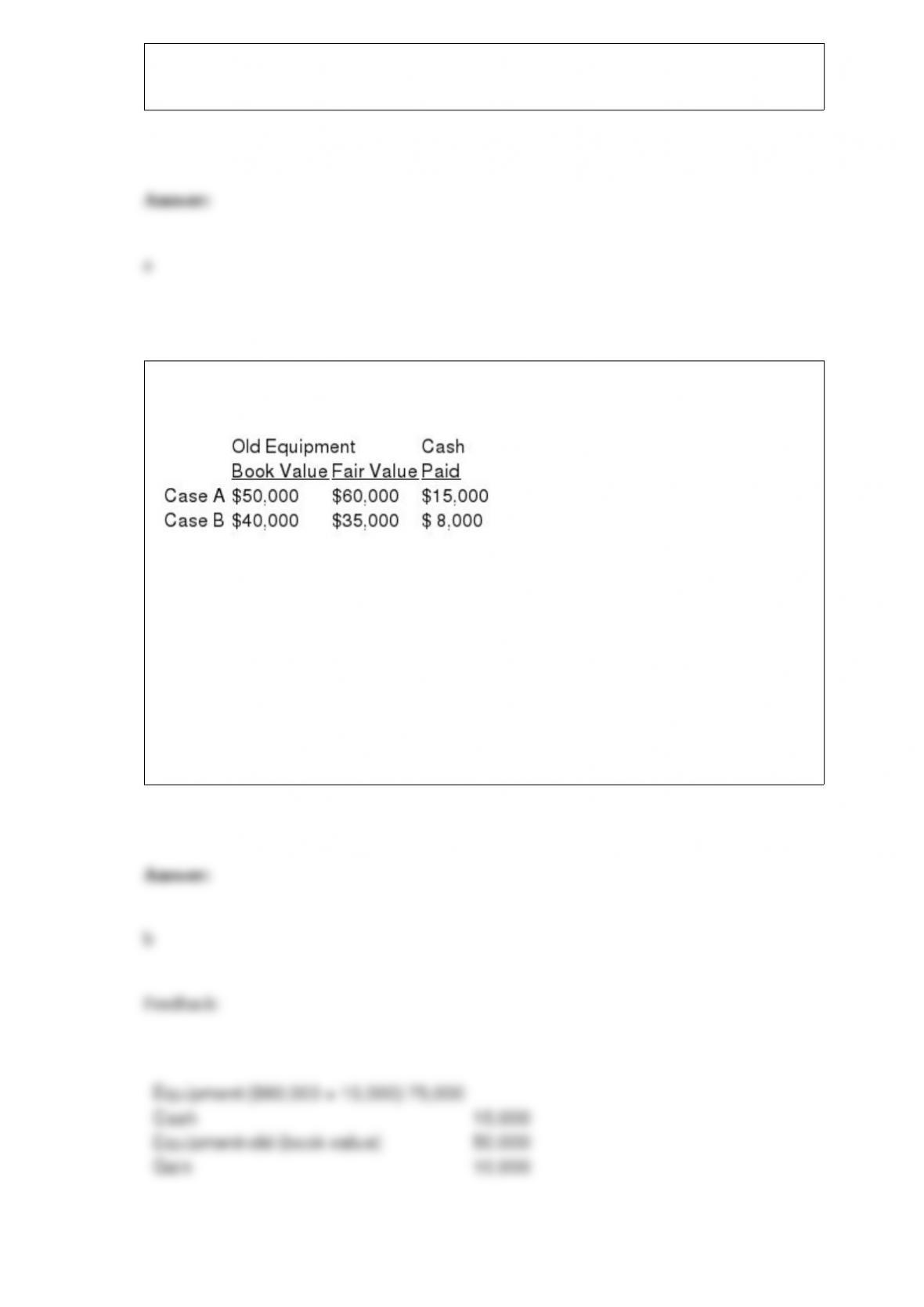

Below is information relative to an exchange of similar assets by Grand Forks Corp.

Assume the exchange has commercial substance.

In Case A, Grand Forks would record the new equipment at:

a. $65,000.

b. $75,000.

c. $50,000.

d. $60,000.

Which of the following is typically true for a bill-and-hold arrangement?

a. Revenue is recognized at the point in time when the arrangement is made.

b. Revenue is recognized at the point in time when goods are manufactured.

c. Revenue is recognized at the point in time when the delivery of goods is made.

d. Revenue is recognized at the point in time at which payment from the customer is

received.

What is meant by dilution of earnings per share?

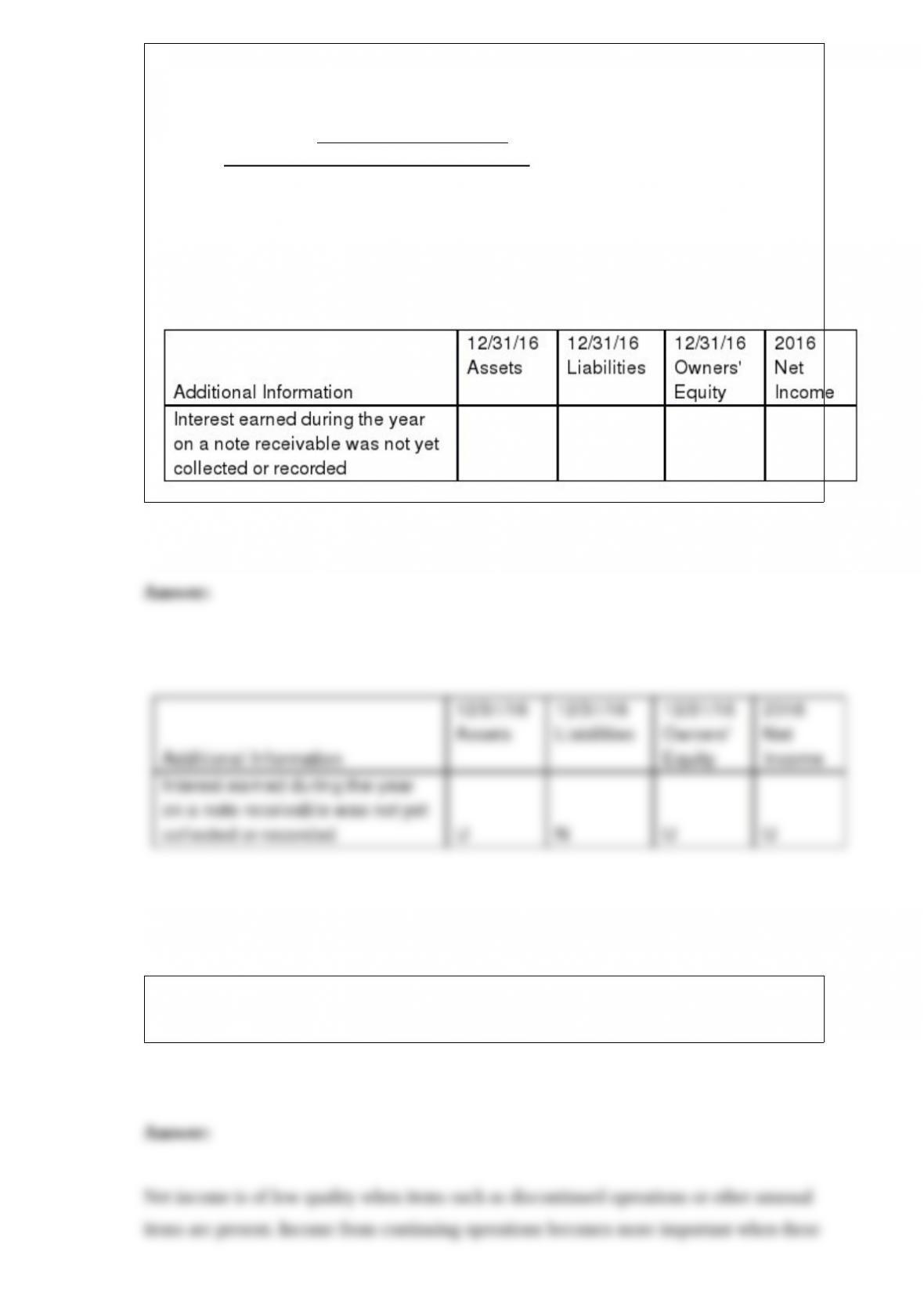

Use the following to answer questions 119-124: You are reviewing O’Brian Co.’s

adjusted trial balance for the year ended 12/31/16. You notice several omissions and

incorrect items during your review, some of which are noted below. For each one, you

are to determine what effect, if any, these items would have on the stated components of

O’Brian Co.’s 2016 Income Statement and 12/31/16 Balance Sheet if they are not

corrected or updated. Assume no income taxes. Use the following code for your

answers. You need not include any dollar amounts.

N = No Effect

O = Overstated

U = Understated

Net income, often referred to as “the bottom line,” is not always a good predictor of

future income. Explain this statement.

XYZ Company had 200,000 shares of common stock outstanding on December 31,

2015. On July 1, 2016, XYZ issued an additional 50,000 shares for cash. On January 1,

2016, XYZ issued 20,000 shares of convertible preferred stock. The preferred stock had

a par value of $100 per share and paid a 5% dividend. Each share of preferred stock is

convertible into 8 shares of common. During 2016, XYZ paid the regular annual

dividend on the preferred and common stock. Net income for the year was $300,000.

Required:

Calculate XYZ’s basic and diluted earnings per share (rounded to 2 decimal places) for

2016.

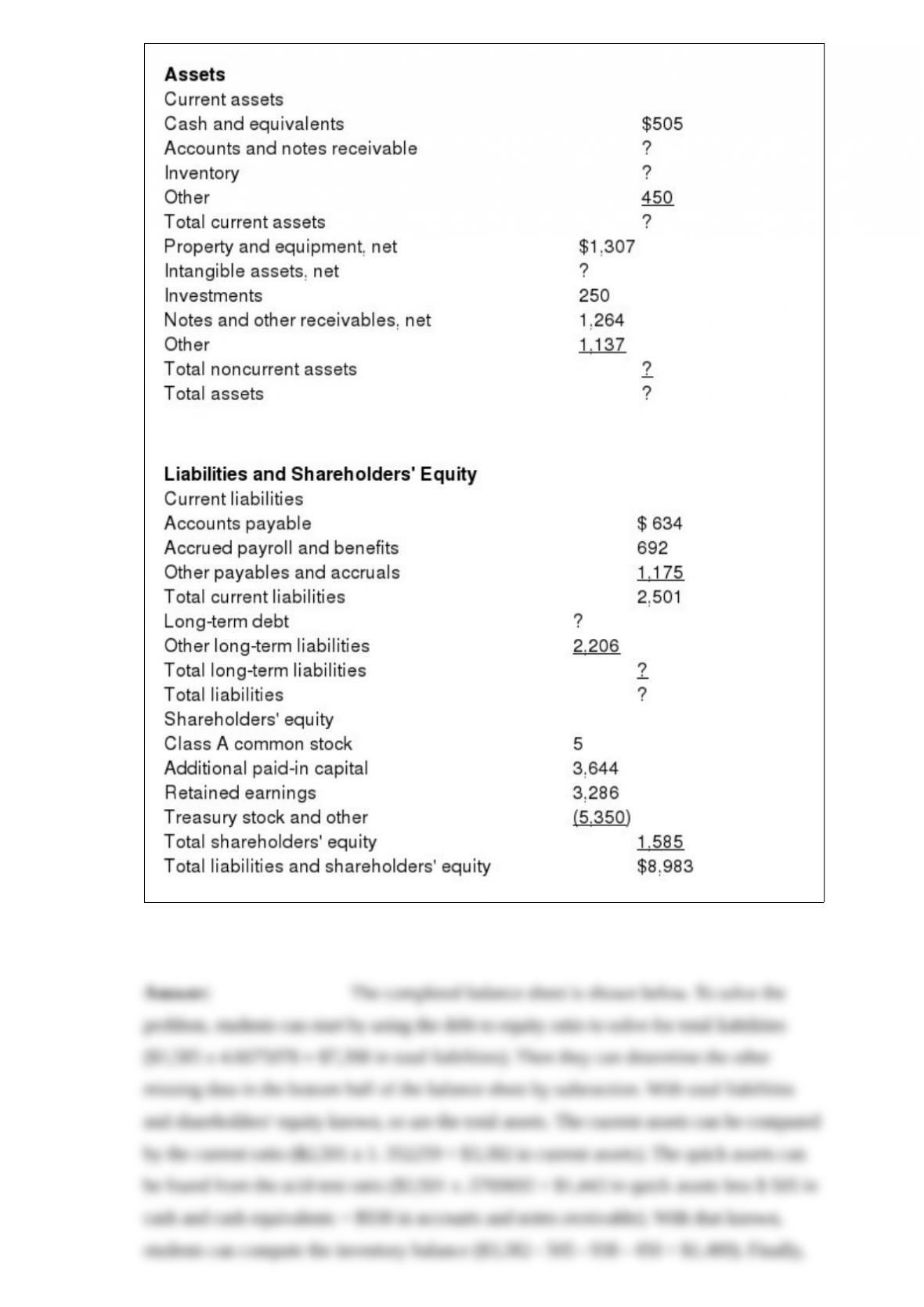

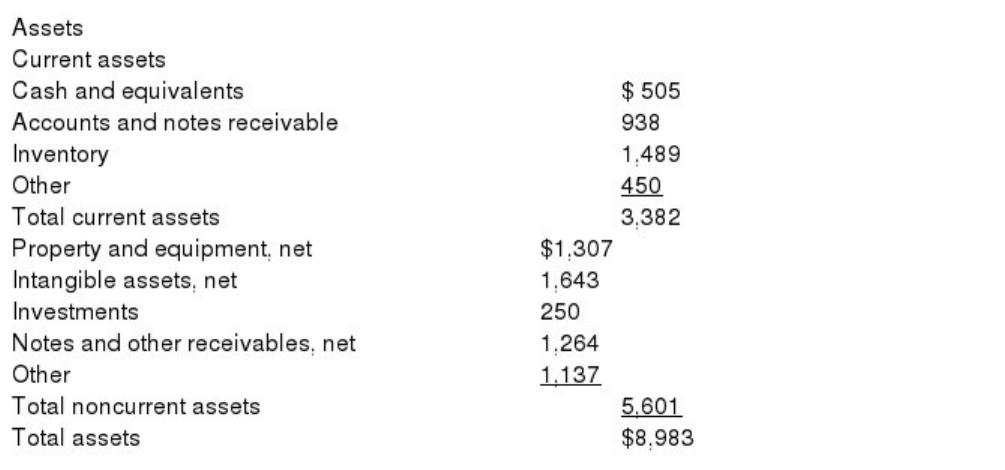

The following balance sheet information (in $ millions) comes from the Annual Report

to Shareholders of Merry International Inc. for the 2016 fiscal year. Certain amounts

have been replaced with question marks to test your understanding of balance sheets. In

addition, you are provided with the following information from an analysis of Merry’s

financial position at the same date:

Current ratio = 1.352259; Acid-test ratio = 0.5769692; Debt to equity ratio =

4.6675078.

Required: Compute the missing amounts (rounded to the nearest $ in millions) in the

balance sheet.

Beacon Inc. received a gift of land and building in Twin Pines Park as an inducement to

relocate. The land and buildings have fair values of $45,000 and $455,000.

Required: Prepare journal entries to record the above transactions.

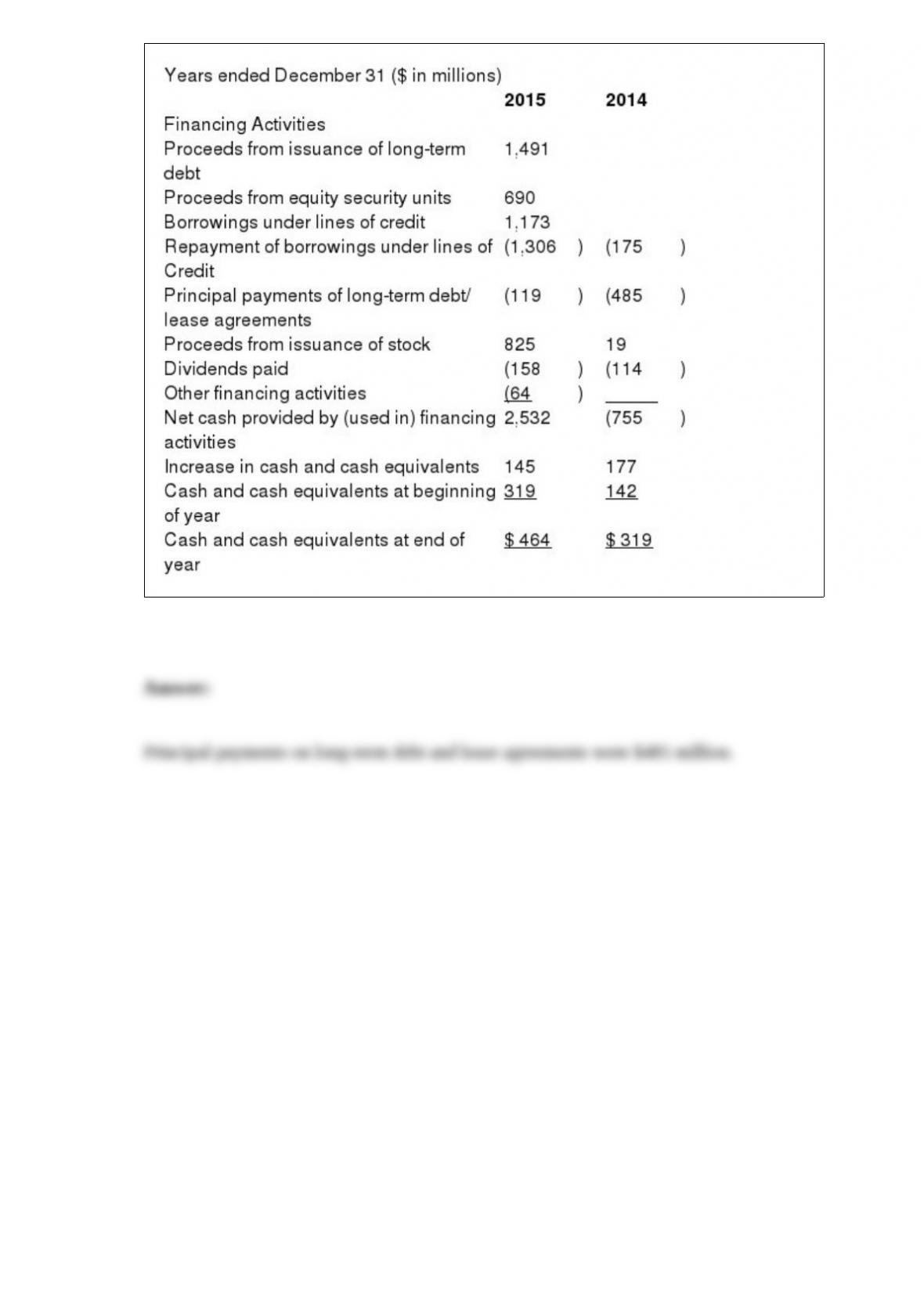

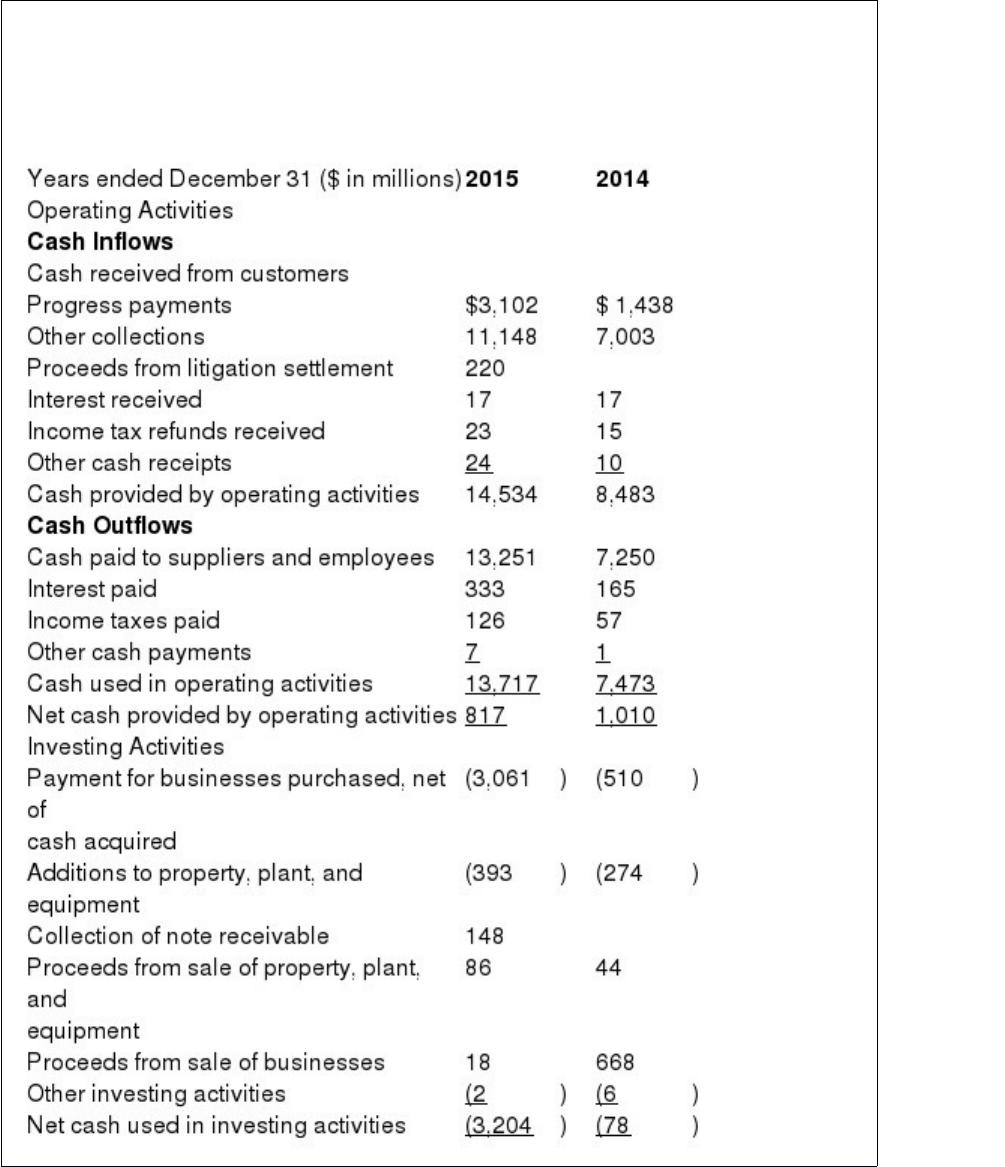

What was most responsible for the negative cash flow from financing activities during

2014? What amount was paid?

In its 2015 Annual Report to Shareholders, Henchman & Co. provided the following

Statement of Cash Flows: